AI Momentum Expands, But Crowding and Concentration Continue to Build

Markets continue to push higher, supported by strong earnings momentum, improving economic data, and a liquidity backdrop that remains firmly supportive of risk assets. The NASDAQ 100 closed above 30,000 for the first time, while the S&P 500 extended its winning streak to nine consecutive weeks. Capital continues flowing aggressively toward AI infrastructure, semiconductors, and technology leadership, reinforcing one of the strongest thematic trends markets have seen in years.

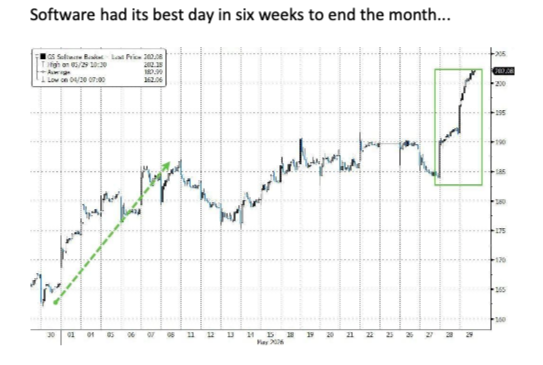

At the same time, the character of the move is beginning to evolve. Participation is broadening beyond semiconductor leadership as software stocks start to recover, but concentration remains elevated, sentiment remains heavily skewed toward upside participation, and several technical and positioning indicators suggest markets are becoming increasingly vulnerable to disappointment. The trend remains constructive, but the internal structure continues to warrant closer attention.

Market Overview: Strong Leadership Continues to Pull Capital Higher

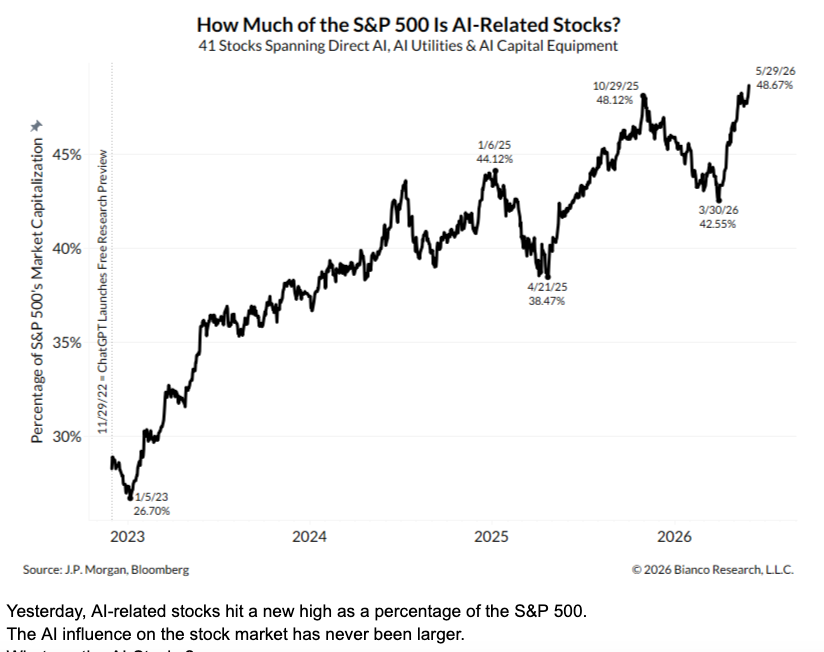

The dominant market theme remains the continued expansion of the AI ecosystem. What began as enthusiasm around a handful of technology leaders has evolved into a broader investment cycle spanning semiconductors, memory chips, infrastructure providers, and software. Investors continue viewing AI as a long-duration capital expenditure cycle rather than a short-term technology trend.

That theme strengthened further during the week as demand expectations across the AI supply chain remained robust. At the same time, software stocks have started participating more meaningfully in the rally, suggesting leadership may be broadening beyond semiconductors alone.

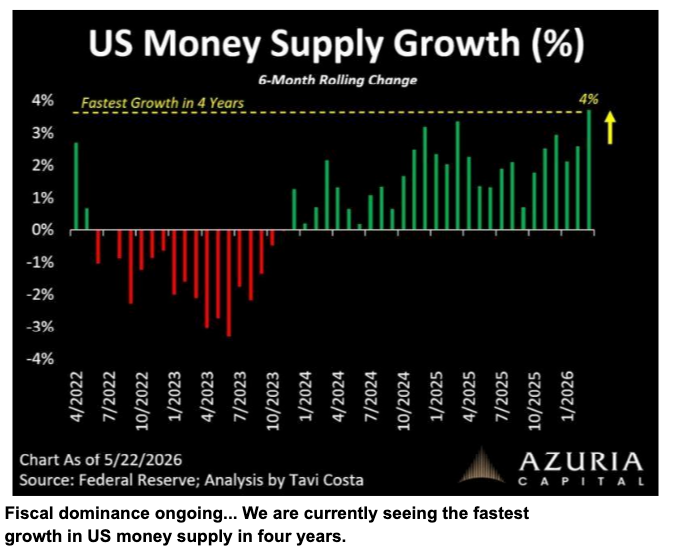

The broader backdrop remains supportive. Economic data continues to surprise to the upside, recession expectations remain subdued, and liquidity conditions continue to improve. Together, these factors have helped reinforce risk appetite despite ongoing concerns surrounding concentration and positioning.

The trend remains constructive, but a growing share of market performance continues to be driven by a relatively narrow group of themes. The key question is whether participation can continue broadening as the rally matures.

Macro & Policy Watch: Growth Holds Firm as Geopolitics Ease

The macro environment remains centred around growth resilience, geopolitical developments, and liquidity conditions.

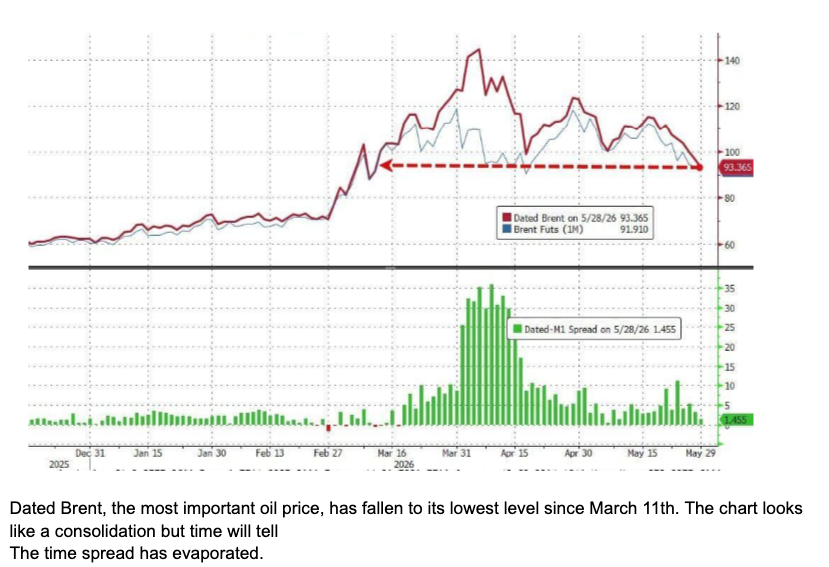

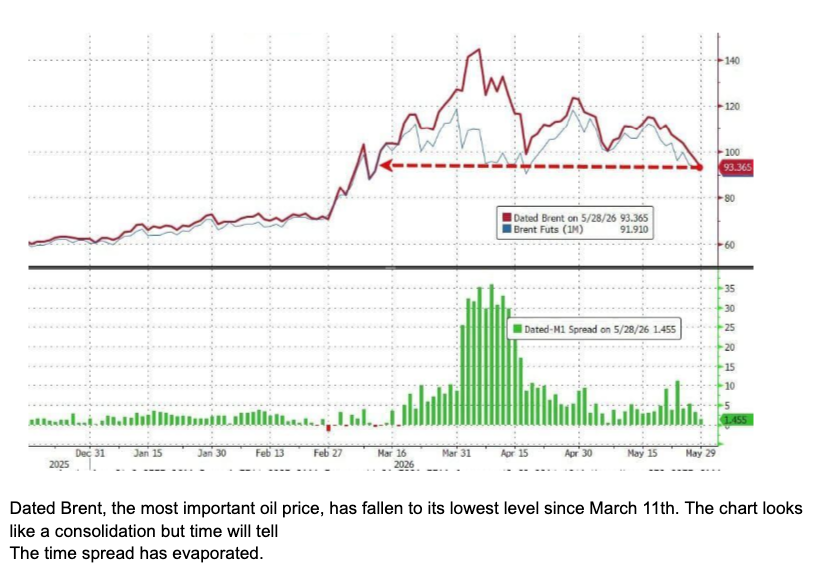

A major focus during the week was the apparent progress toward extending the ceasefire agreement between the United States and Iran. Markets responded positively as expectations grew that disruptions to shipping and energy markets could ease. Falling oil prices became one of the clearest expressions of that shift in sentiment.

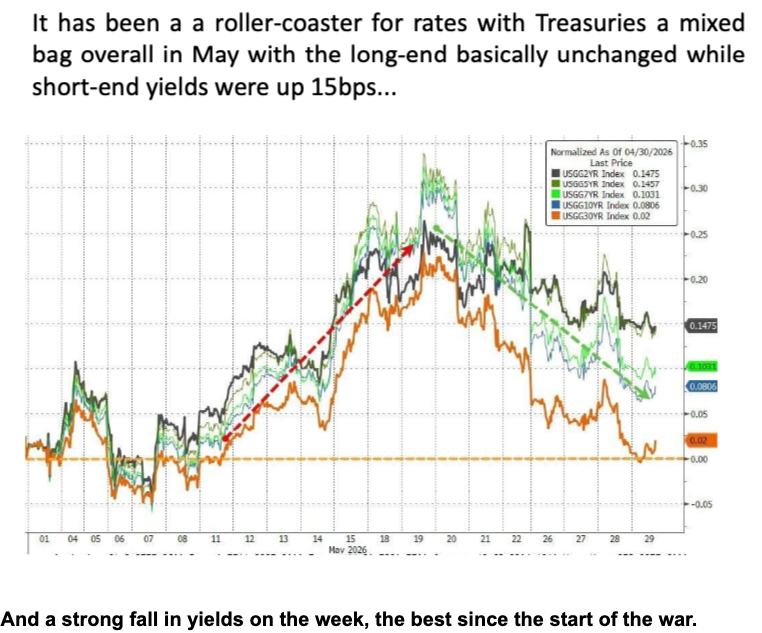

Lower energy prices helped alleviate some inflation concerns and supported both equities and bonds. Treasury markets posted one of their strongest weeks since the conflict began, reflecting improved sentiment and a reduction in immediate inflation fears.

However, markets continue to recognise that energy remains highly sensitive to geopolitical developments. Shipping constraints, inventory concerns, and infrastructure challenges continue to leave commodity markets vulnerable to renewed volatility should negotiations deteriorate.

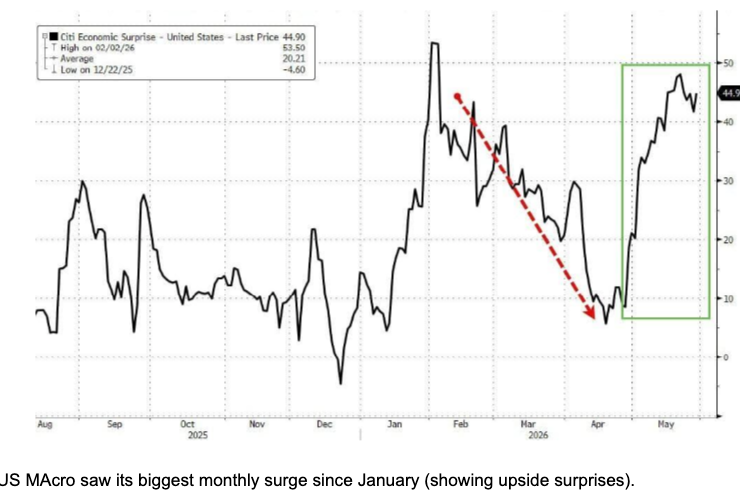

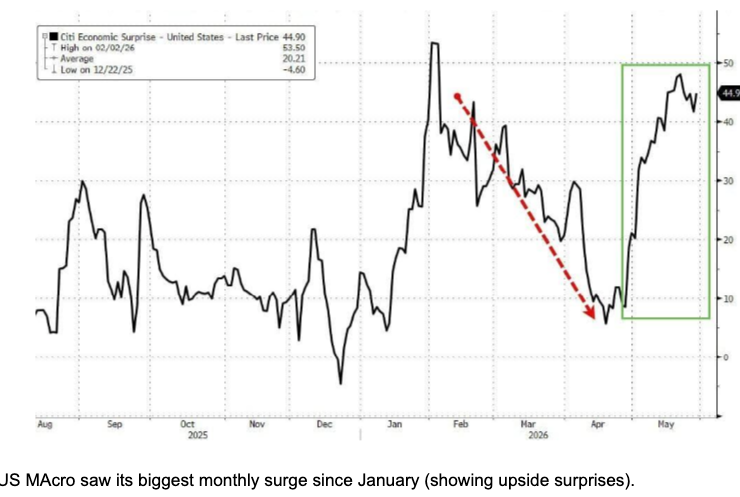

At the same time, economic data continued supporting a growth-oriented narrative. Durable goods orders remained constructive, economic surprise indices improved, and broader activity data continued to suggest growth remained resilient.

The result is a macro backdrop that remains supportive overall, even as investors continue monitoring geopolitical developments and inflation expectations closely.

Technical & Sentiment Breakdown: Supportive, but Increasingly Fragile

The broader trend remains constructive, with momentum, earnings, and liquidity continuing to support higher prices. However, several indicators suggest the market is becoming increasingly dependent on positioning and sentiment rather than broad participation.

The NASDAQ 100 has advanced into a significant technical resistance zone defined by multiple long-term trend channels. Momentum remains strong, but the market is approaching an area where consolidation would not be unusual.

The S&P 500 is facing a similar challenge as it approaches a major confluence of resistance levels. The broader structure remains bullish, but upside progress is becoming increasingly dependent on maintaining current momentum.

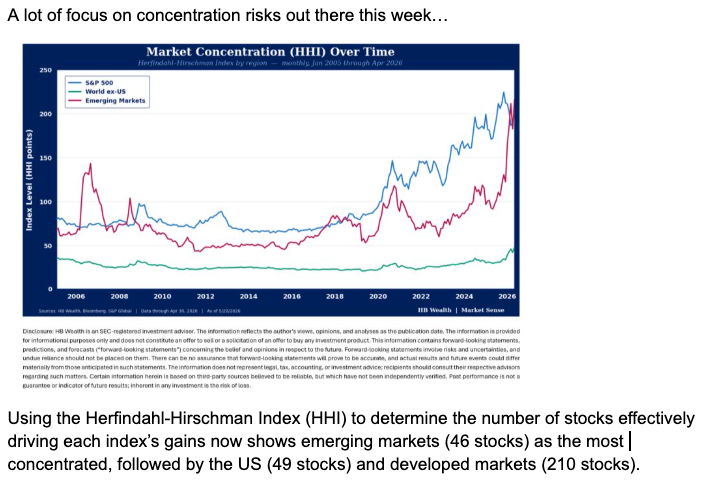

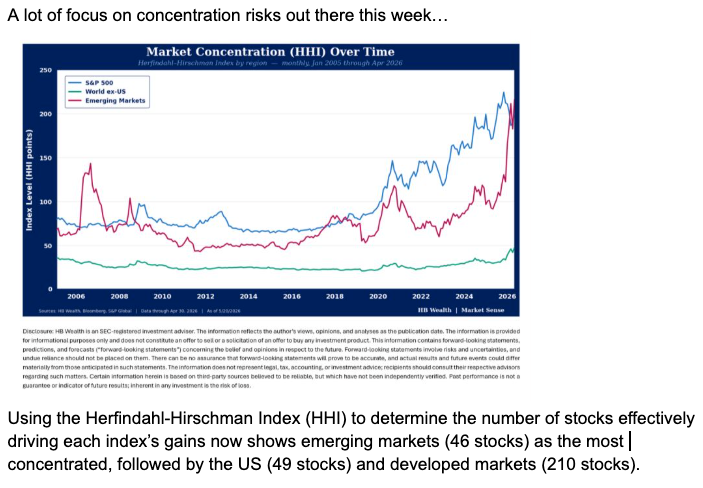

Beneath the surface, concentration remains one of the market's defining characteristics. A relatively small number of stocks continue driving a substantial share of index-level gains, creating an environment where leadership matters more than ever.

The AI theme remains central to that concentration story. Exposure to AI-related companies continues dominating flows, performance, and investor attention, reinforcing both the strength and the fragility of current market leadership.

Sentiment indicators also suggest increasing confidence among investors. Downside protection remains limited while upside participation continues attracting capital. Dispersion remains elevated, correlations remain unusually low, and many participants continue positioning for further gains rather than preparing for volatility.

Several sentiment and cycle frameworks highlighted throughout the report suggest the possibility of a pause or consolidation phase developing during the coming weeks, even as the broader trend remains intact.

The trend remains constructive for now, but the combination of elevated positioning, concentration, and growing optimism suggests markets are becoming increasingly sensitive to disappointment.

Last Week’s Recap: Growth Resilience, AI Leadership, and Easing Energy Pressures

The past week was characterised by continued strength across equities as improving economic data, easing geopolitical tensions, and AI-driven earnings optimism combined to support risk assets. Beneath the headline gains, investors continued debating concentration risk, positioning, and the sustainability of current leadership.

Key Highlights:

- Macro:

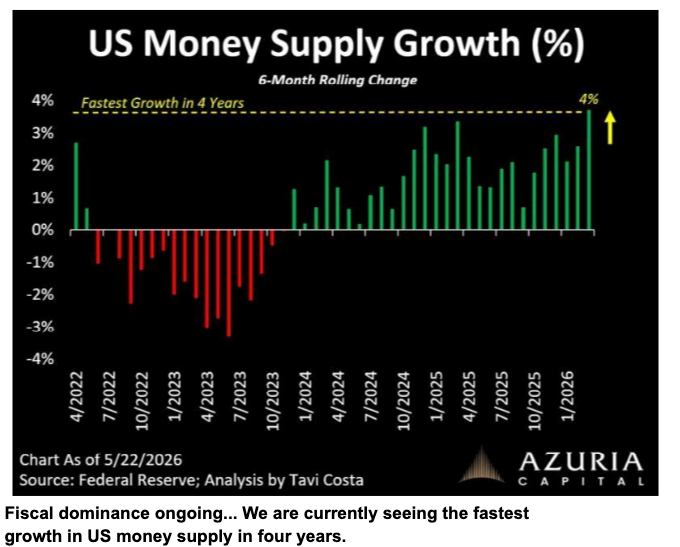

Economic data continued to surprise positively, while recession expectations remained subdued. Liquidity conditions improved further as money supply growth accelerated and growth expectations remained constructive.

- China:

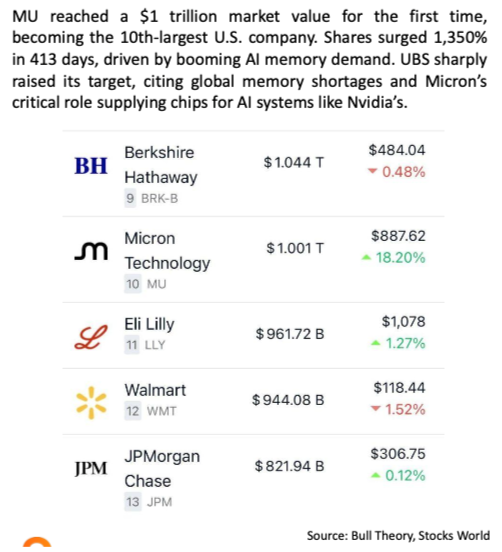

Taiwan and South Korea remained key beneficiaries of the AI investment cycle, with continued strength in semiconductor demand, memory-chip producers, and technology supply chains supporting regional equity performance.

- Earnings:

Earnings remained a key pillar of support for equities. AI infrastructure spending, semiconductor demand, and improving earnings expectations continued reinforcing the broader growth narrative, while attention increasingly shifted toward Broadcom as a major upcoming catalyst.

- Commodities:

Gold remained volatile but continued to hold key support levels as investors balanced easing geopolitical risks against ongoing liquidity expansion and macro uncertainty.

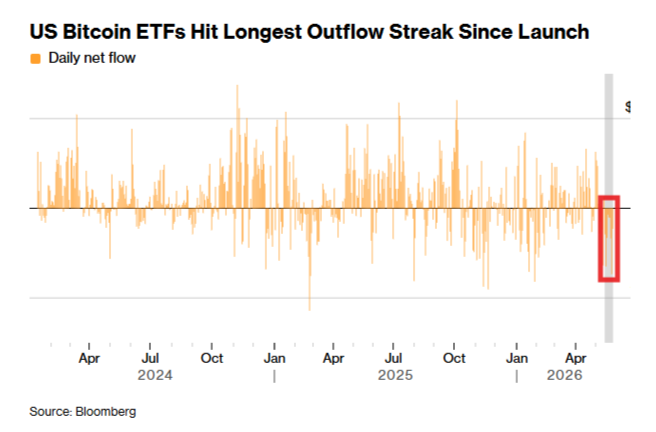

- Crypto:

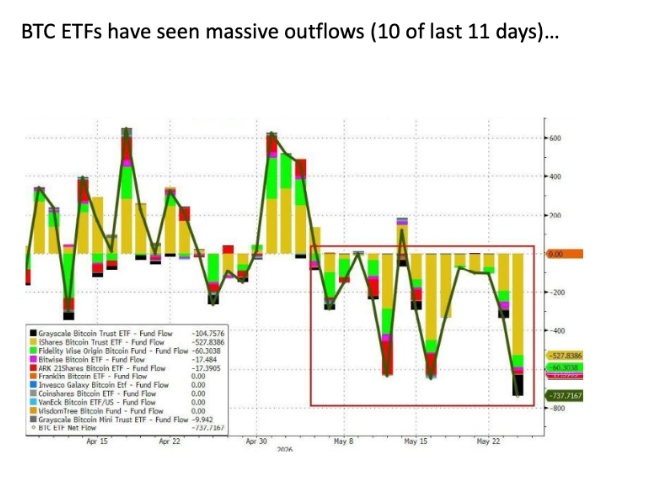

Crypto markets remained influenced by broader liquidity conditions and risk sentiment. Despite continued ETF outflows, Bitcoin remained relatively resilient during the week, with price action holding up better than flows would suggest. The divergence between persistent ETF outflows and stable price behaviour remained one of the more notable developments across the crypto market.

- Oil:

Oil prices moved lower as ceasefire progress reduced immediate concerns surrounding supply disruptions and shipping access through the Strait of Hormuz.

The Week Ahead: Key Data and Market-Moving Signals

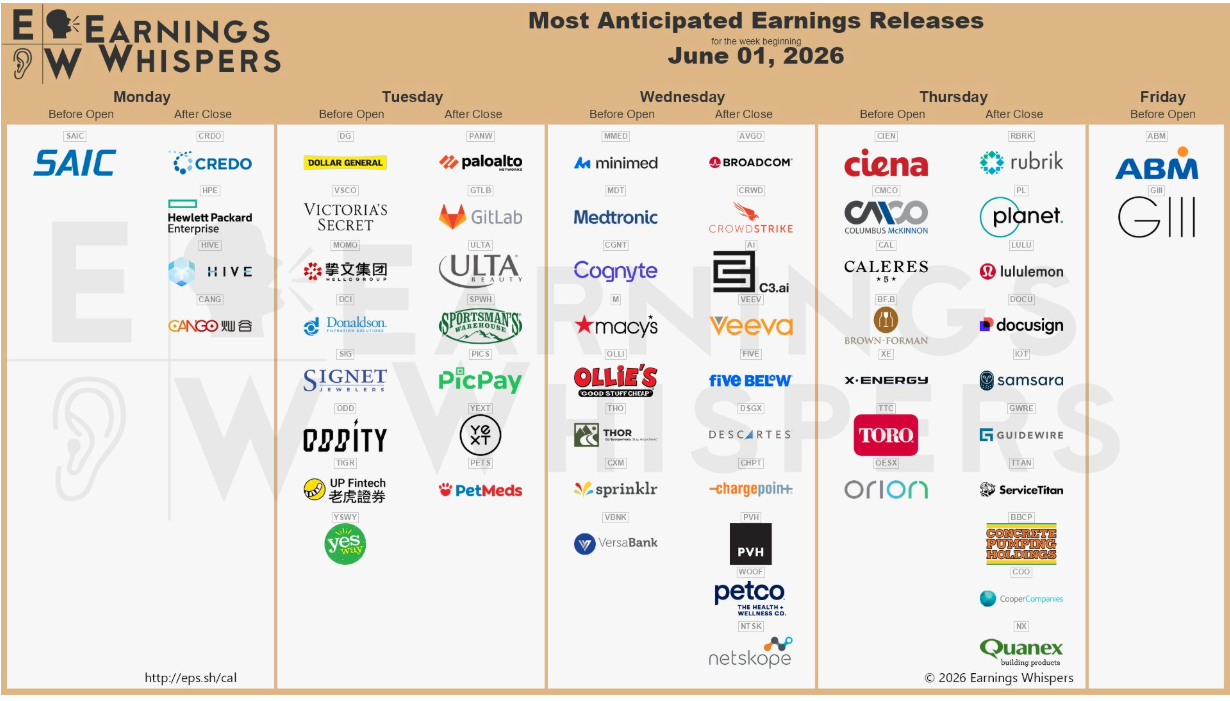

The week ahead is packed with market-moving catalysts, beginning with Global Manufacturing PMIs and US ISM data before attention shifts to Eurozone inflation, US job openings, Services PMIs, and the Fed's Beige Book. Friday's Nonfarm Payrolls report will be the key macro event of the week, while Broadcom and CrowdStrike earnings, alongside a busy schedule of Fed speakers, will provide further insight into AI demand, growth expectations, and the policy outlook.

Monday, June 1

• Global: Manufacturing PMIs

• US: ISM Manufacturing PMI

• US: ISM Manufacturing Prices

• US: Construction Spending

• US: Atlanta Fed GDPNow Update

• Eurozone: Unemployment Rate

• US: Fed Chair Powell Speaks

• US: Fed Governor Waller Speaks

Tuesday, June 2

• South Korea: CPI

• UK: Mortgage Lending & Consumer Credit

• Eurozone: CPI & Core CPI

• US: JOLTS Job Openings

• US: Redbook Retail Sales

• US: FOMC Member Kashkari Speaks

• UK: BoE Governor Bailey Speaks

Wednesday, June 3

• Global: Services PMIs

• US: ISM Services PMI

• US: ADP Employment Report

• US: Federal Reserve Beige Book

• US: Factory Orders

• US: Broadcom Earnings

• US: CrowdStrike Earnings

• US: Fed Vice Chair Barr Speaks

• US: Fed Logan Speaks

Thursday, June 4

• Switzerland: CPI

• Eurozone: Retail Sales

• US: Initial Jobless Claims

• US: Nonfarm Productivity

• US: Unit Labour Costs

• US: Continuing Jobless Claims

• Eurozone: ECB President Lagarde Speaks

• UK: BoE Governor Bailey Speaks

• US: FOMC Member Daly Speaks

Friday, June 5

• US: Nonfarm Payrolls

• US: Unemployment Rate

• US: Average Hourly Earnings

• Eurozone: GDP

• Eurozone: Employment Data

• India: Interest Rate Decision

• Canada: Employment Report

• UK: BoE Governor Bailey Speaks

Alpha Takeaway: Momentum Remains Strong, But Crowding Is Becoming Harder to Ignore

Markets remain supported by strong earnings, resilient growth data, improving liquidity conditions, and continued enthusiasm surrounding AI investment. The broader trend remains constructive, but the conversation is increasingly shifting from whether the rally can continue to how dependent it has become on a relatively small group of leaders.

- Equities:

Equities continue benefiting from earnings momentum and expanding participation, particularly as software stocks begin catching up to semiconductor leadership. However, concentration remains elevated, and positioning has become increasingly crowded around a narrow set of themes.

- Gold & Silver:

Precious metals continue navigating the balance between easing geopolitical risks and a supportive liquidity backdrop. Recent price action remains more consistent with consolidation than a decisive change in trend.

- Crypto:

Crypto continues responding primarily to liquidity conditions and risk sentiment. Despite continued ETF outflows, Bitcoin has remained relatively resilient, with price stability diverging from flow dynamics.

- Macro:

Growth remains resilient, recession expectations remain low, and liquidity continues expanding. At the same time, markets are navigating elevated valuations, concentrated leadership, and continued sensitivity to geopolitical developments.

The broader trend remains supportive, but the internal structure continues to become more dependent on leadership concentration and optimistic positioning. Momentum remains powerful, but leadership is narrowing, positioning is crowded, and downside hedging remains limited. As long as liquidity and earnings continue supporting risk assets, the trend can persist, but concentration remains one of the key risks beneath the surface.

CTA: https://docs.google.com/document/d/11bjcwc3smLLxwBDXtG3UK7xy_YBU6sL2KDE3Q2eG8l4/edit?usp=sharing