Growth Holds Firm, But Positioning and Rates Are Starting to Matter

Markets entered June with momentum still firmly on their side, supported by resilient economic data, strong earnings trends, and a technology investment cycle that continues to expand beyond a handful of headline names. Even after Friday's selloff, the broader backdrop remains one of growth rather than deterioration, with activity indicators, employment data, and earnings expectations continuing to surprise to the upside.

At the same time, the market's character is beginning to evolve. Rising yields, elevated positioning, and crowded exposure to AI-related themes are creating a more fragile environment beneath the surface. The debate is no longer centred on recession risks, but on whether stronger growth and higher rates can coexist with stretched valuations, concentrated leadership, and increasingly optimistic sentiment.

Market Overview: Growth Continues to Drive the Narrative

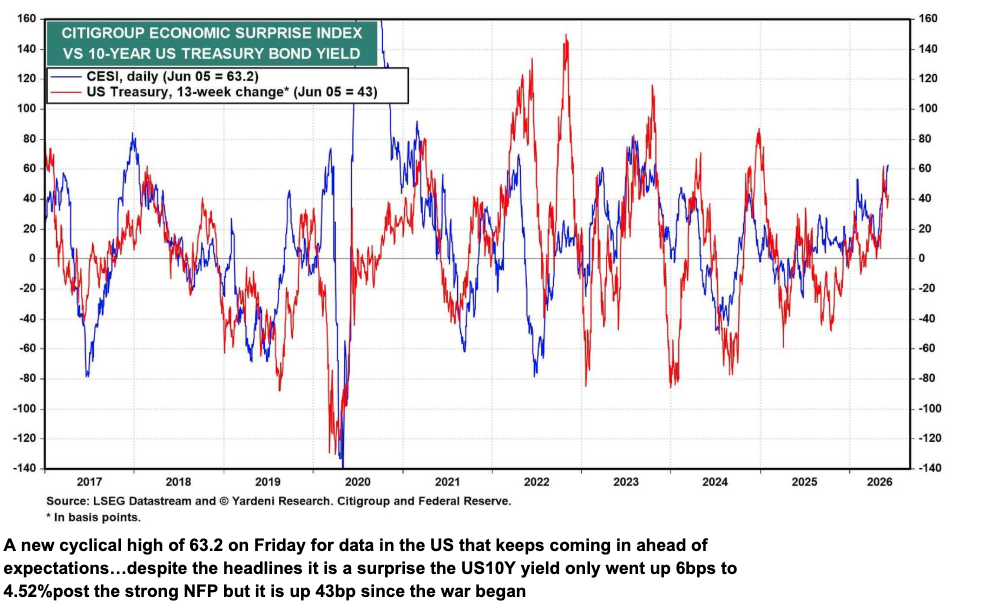

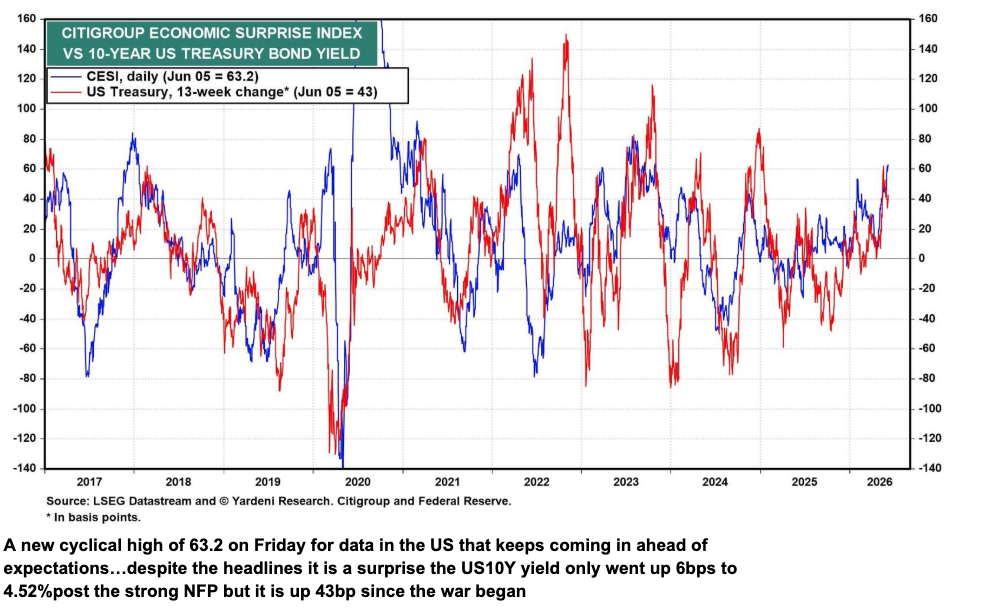

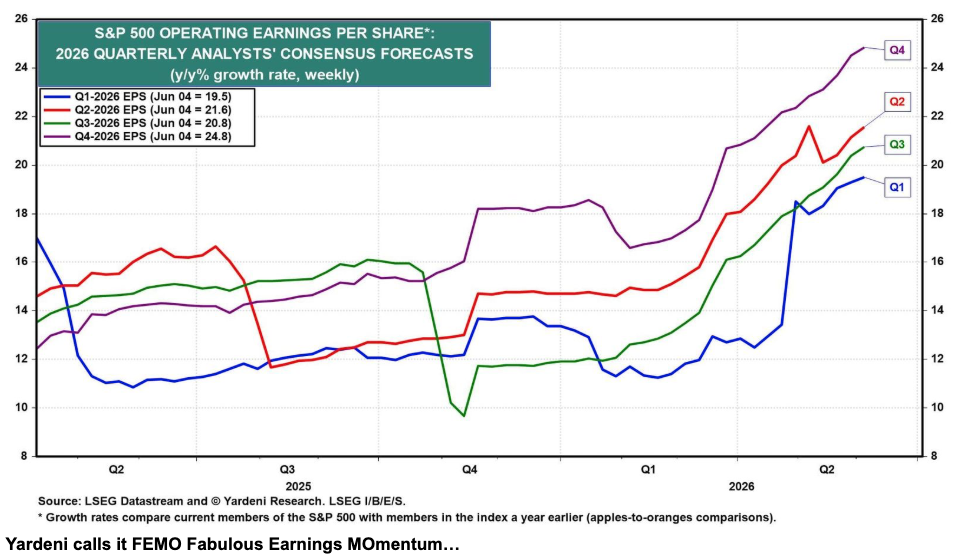

The dominant theme remains growth. Incoming economic data continued to exceed expectations, reinforcing a backdrop that remains far more resilient than many anticipated earlier in the year. Manufacturing activity strengthened, services activity remained firmly in expansion territory, payroll growth held up well, and economic surprise indices pushed to fresh cyclical highs.

Yet despite the positive macro backdrop, markets experienced their sharpest bout of selling pressure in weeks. Broadcom and CrowdStrike became symbolic catalysts for the move as technology, semiconductors, and cyclical sectors came under pressure following an extended rally from the March lows.

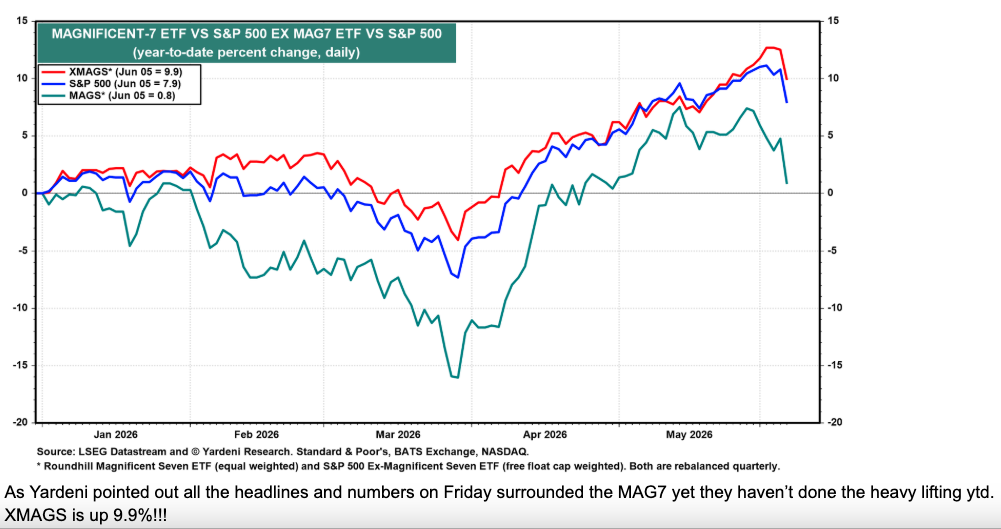

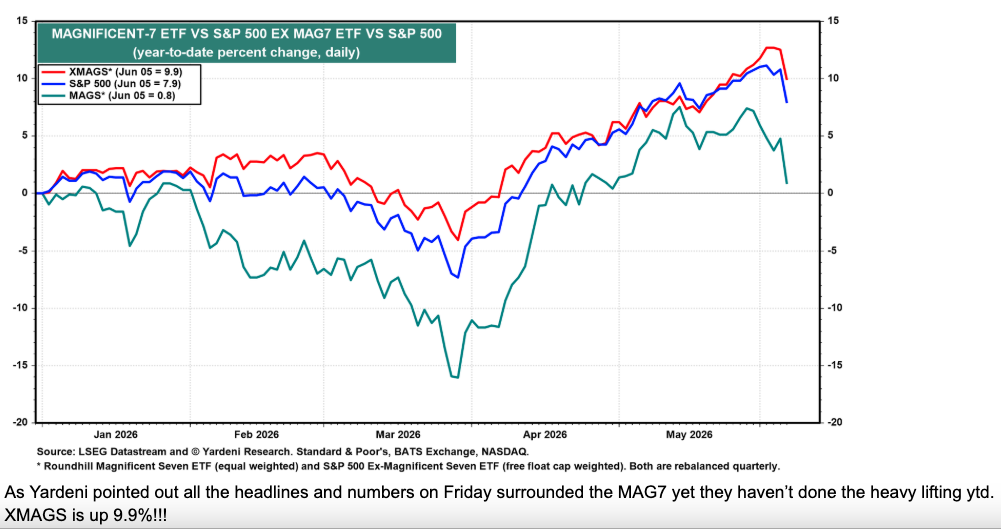

One of the more important observations from the week was that the rally has not been driven solely by the Magnificent Seven. While headlines continue to focus on mega-cap technology, broader participation across the technology ecosystem has played a far greater role than many investors appreciate.

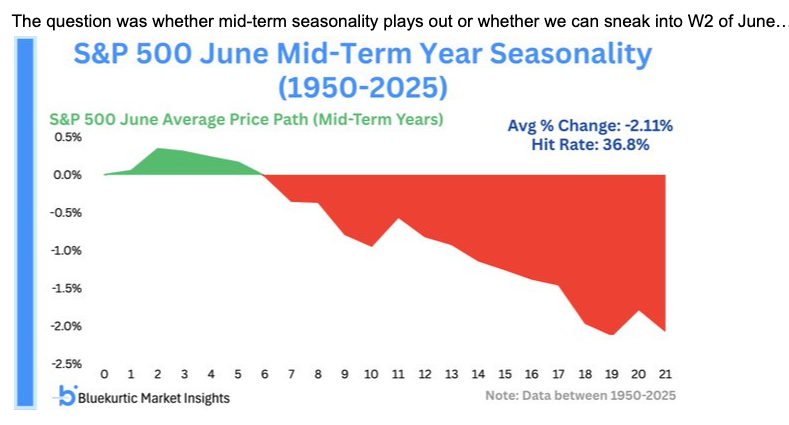

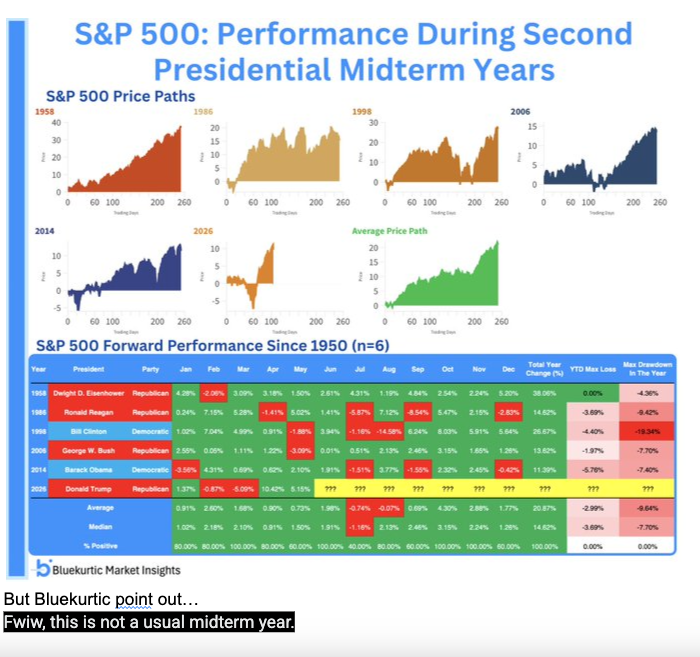

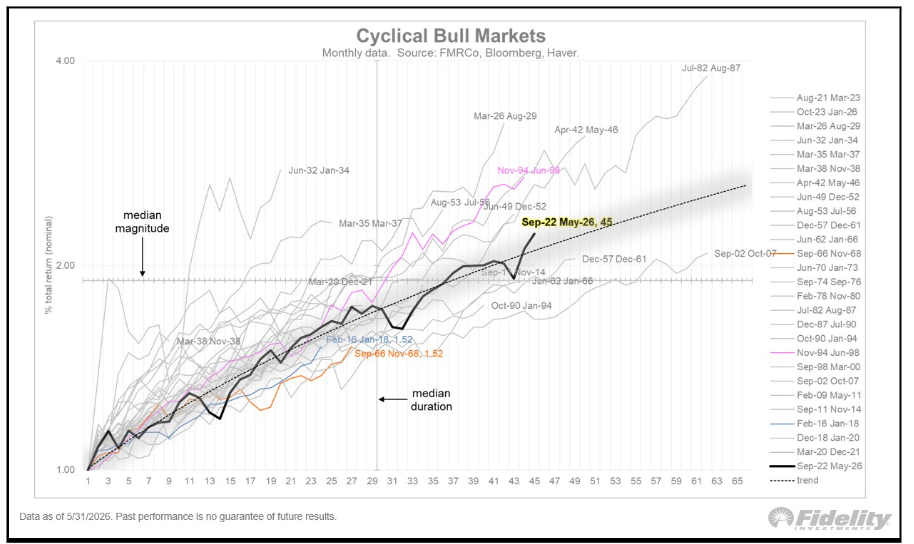

Seasonality is also attracting attention. Historical midterm-year patterns suggest June can be a more challenging month for equities, particularly following a weak first quarter.

However, history is not offering a one-sided message. Current weakness follows a nine-week winning streak, and second-term presidential midterm years have historically delivered positive June outcomes.

Historical patterns point to a more volatile June backdrop, while incoming economic data continues to surprise to the upside. Markets now find themselves balancing seasonal headwinds against a growth backdrop that remains resilient.

Macro & Policy Watch: Growth, Rates and Liquidity

The macro backdrop continues to revolve around one central theme: growth is proving more resilient than expected.

For much of the past year, markets repeatedly debated recession risks, hard landings, soft landings, and stagflation scenarios. Recent data has challenged those concerns. Manufacturing and services activity both remain in expansion, labour market conditions continue showing resilience, and economic surprise indices have continued moving higher.

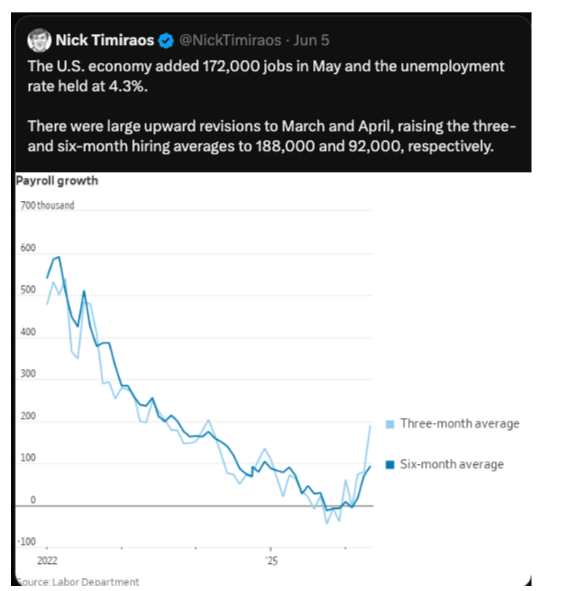

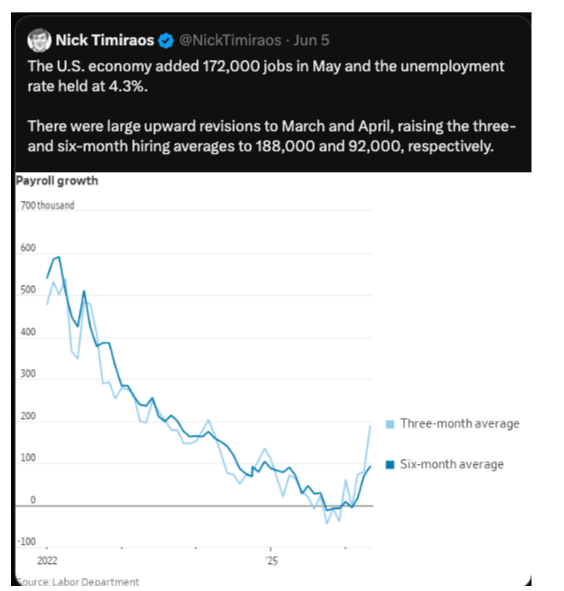

Employment data reinforced that narrative. Payroll growth remained firm, revisions improved, and labour market conditions continue to suggest an economy that is expanding rather than contracting.

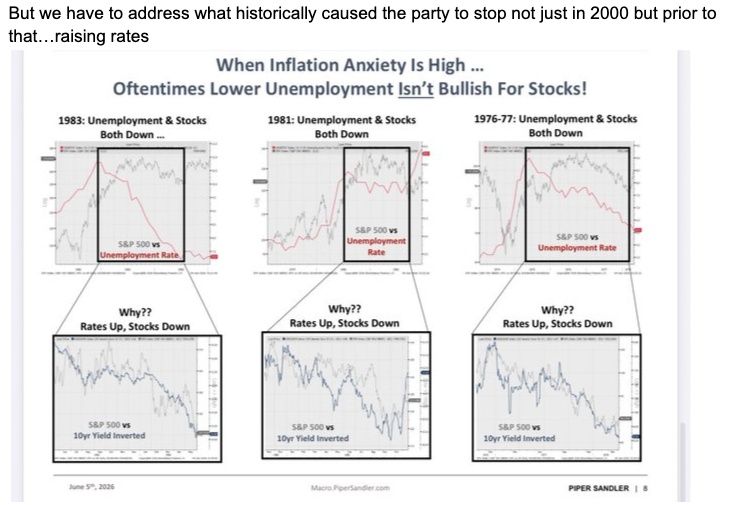

That resilience is beginning to influence policy expectations. Rate-cut expectations have faded considerably, while discussions around a more neutral or even tighter policy stance have become increasingly common. Rising yields reflect that shift.

Stronger growth continues supporting earnings and economic activity, while simultaneously reducing the urgency for policy easing. As growth expectations improve, markets are increasingly reassessing the path of rates and yields.

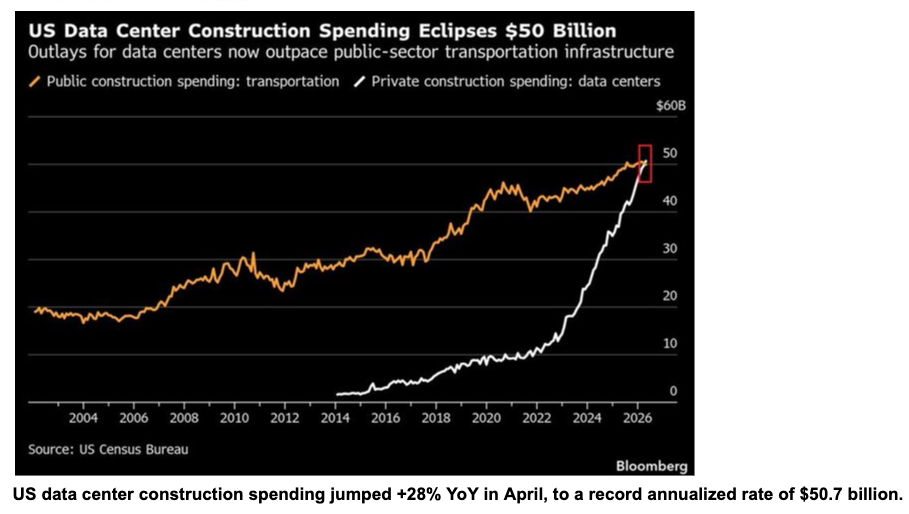

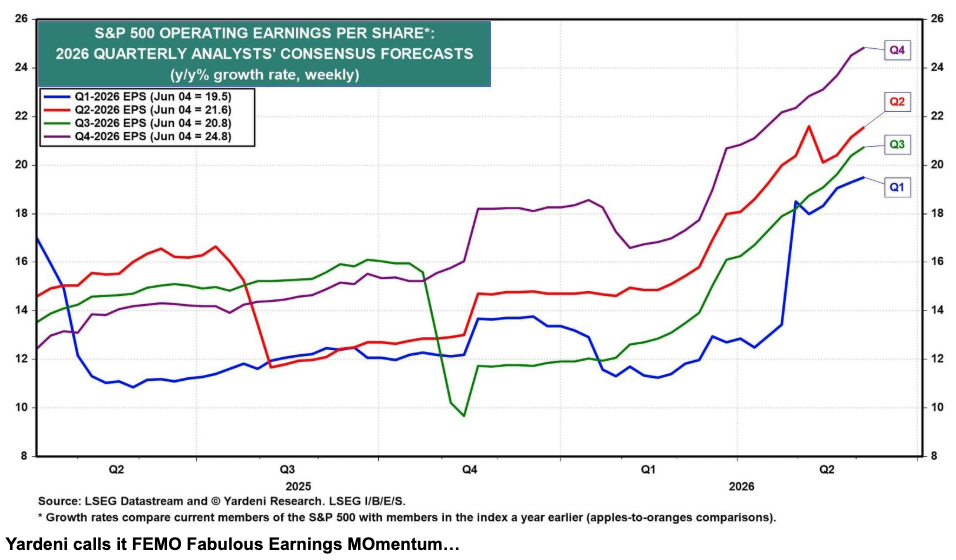

The AI investment cycle remains one of the strongest structural themes in the market. Capital expenditure expectations continue rising, data-centre investment remains robust, and infrastructure buildout shows little evidence of slowing.

The AI story is increasingly evolving beyond hardware into software, services, and broader productivity applications. While investors continue debating valuations and crowding, the underlying investment cycle remains intact.

Technical & Sentiment Breakdown: Supportive, but Increasingly Fragile

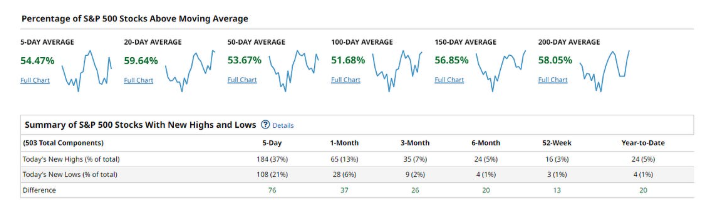

The broader trend remains constructive, but the internal structure of the market has become increasingly dependent on positioning and sentiment.

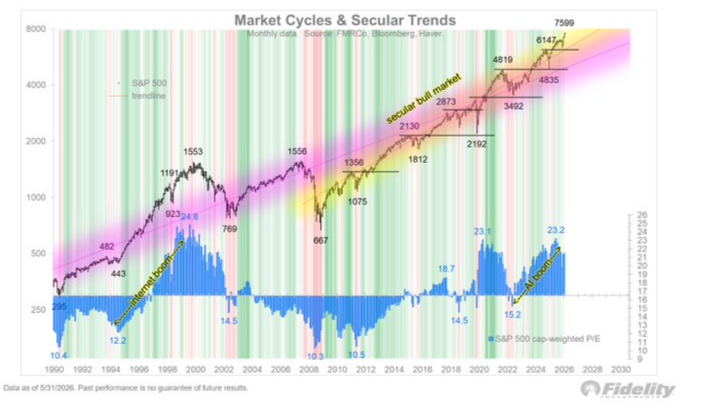

From a technical perspective, the recent selloff appears more consistent with consolidation than a major trend reversal. Following an exceptionally strong rally from the March lows, markets were vulnerable to a reset in expectations and positioning.

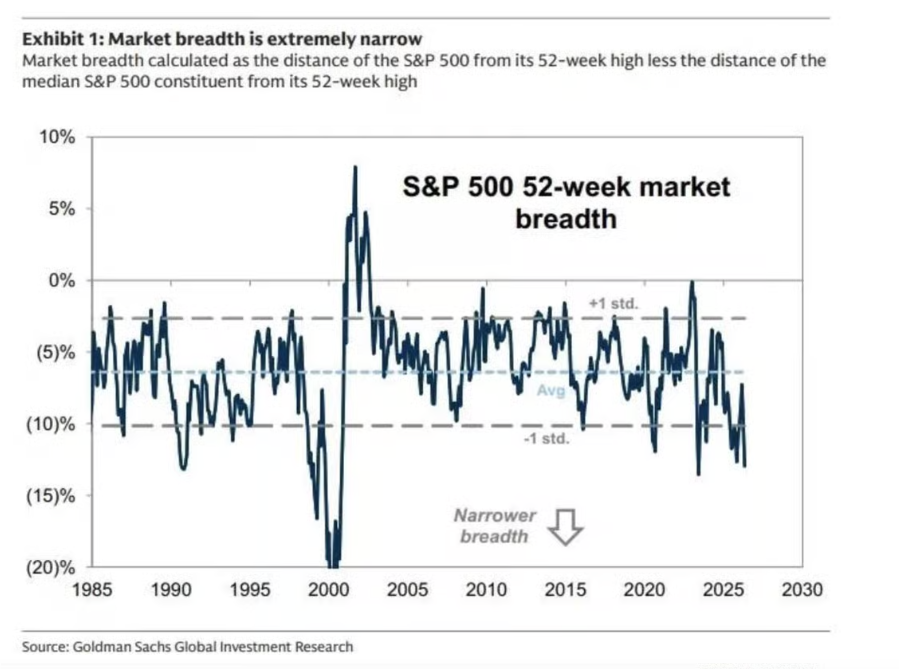

Participation remains one of the key areas to monitor. While major indices continue holding above important long-term trend measures, breadth beneath the surface remains less convincing.

Beneath the surface, participation remains a critical area to monitor. A growing share of stocks had already begun weakening before Friday's selloff, highlighting a divergence between index performance and broader market participation.

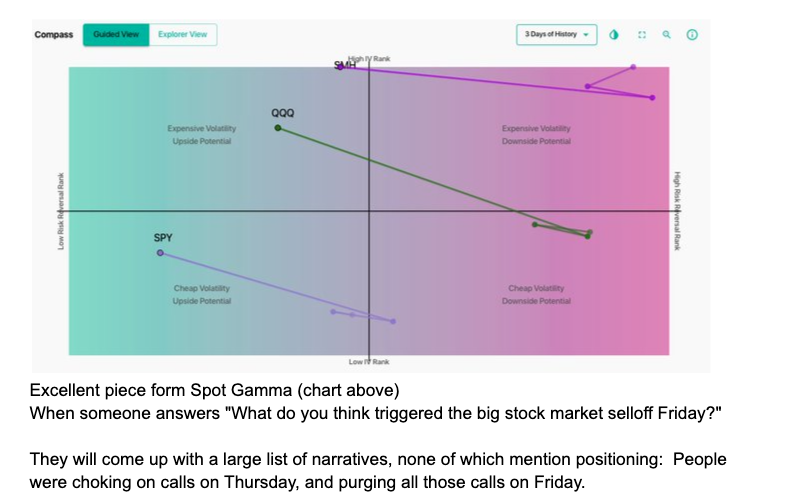

Positioning appears to have played a significant role in Friday's move. Technology exposure had become increasingly crowded, leaving markets vulnerable to a rapid unwind once momentum began to fade.

The AI theme remains central to the positioning story. Exposure to AI beneficiaries continues dominating flows and investor attention, contributing to increasingly crowded positioning across parts of the technology complex.

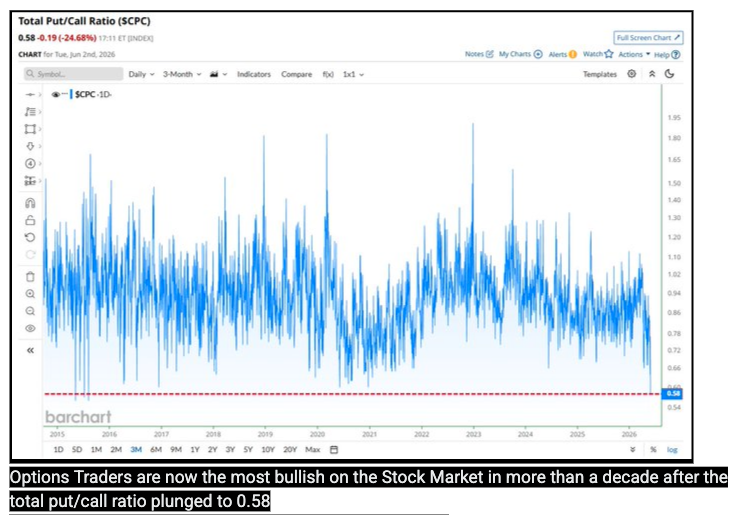

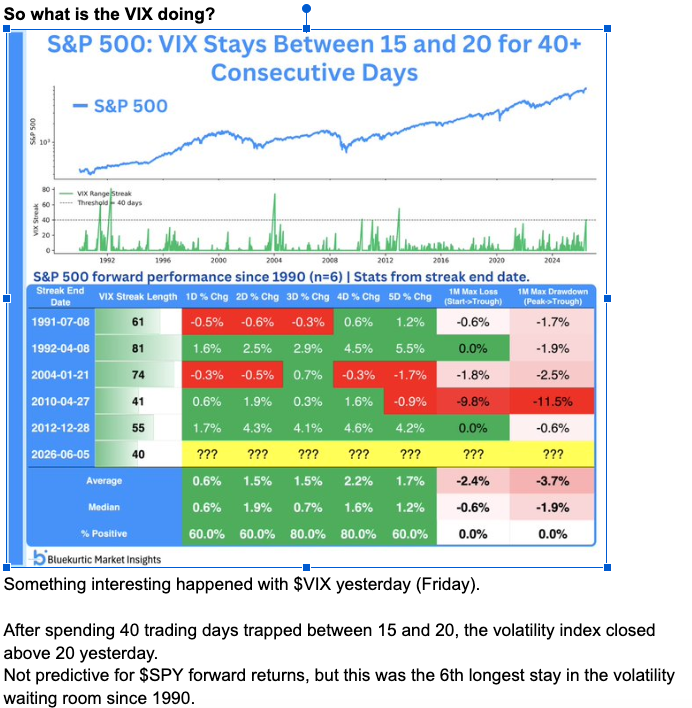

Sentiment indicators continue reflecting elevated optimism and crowded positioning.

Volatility has also started to re-emerge after an unusually prolonged period of calm.

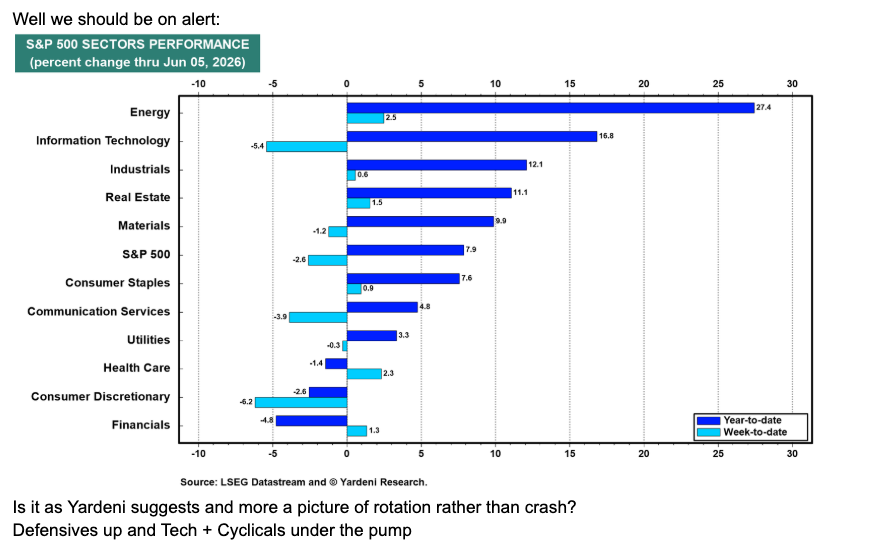

Despite the weakness, the move continues to look more like a positioning reset than a deterioration in fundamentals. Defensive sectors outperformed while technology and cyclicals absorbed the majority of the selling pressure, reinforcing the view that rotation rather than panic remains the dominant theme.

The trend remains constructive for now, but the combination of elevated positioning, concentrated leadership, and increasingly optimistic sentiment suggests markets have become more sensitive to disappointment.

Last Week’s Recap: Growth Resilience Meets a Technology Shakeout

The past week was characterised by stronger-than-expected economic data, rising yields, and a meaningful reset across technology and cyclical sectors. While fundamentals remained supportive, positioning and sentiment became increasingly important drivers of price action.

Key Highlights:

Macro:

Economic data continued to surprise to the upside. Manufacturing and services activity remained in expansion territory, payroll growth strengthened, and economic surprise indices reached fresh cyclical highs. As a result, markets increasingly shifted their focus from rate cuts toward the possibility of a more restrictive policy path.

China:

Technology-related trade remained an important source of support, with higher technology prices continuing to influence both exports and imports. Reflation expectations also remained part of the broader discussion as investors assessed regional growth trends.

Earnings:

Broadcom and CrowdStrike became key market catalysts during the week. While the broader earnings backdrop remains constructive, elevated expectations and crowded positioning contributed to selling pressure across technology and semiconductor names. The broader AI earnings story, however, remains intact.

Commodities:

Commodities continue to be viewed as a preferred hedge against inflation risks, liquidity concerns, and structural investment trends. Copper remained one of the clearest examples of consolidation finding support after a significant advance.

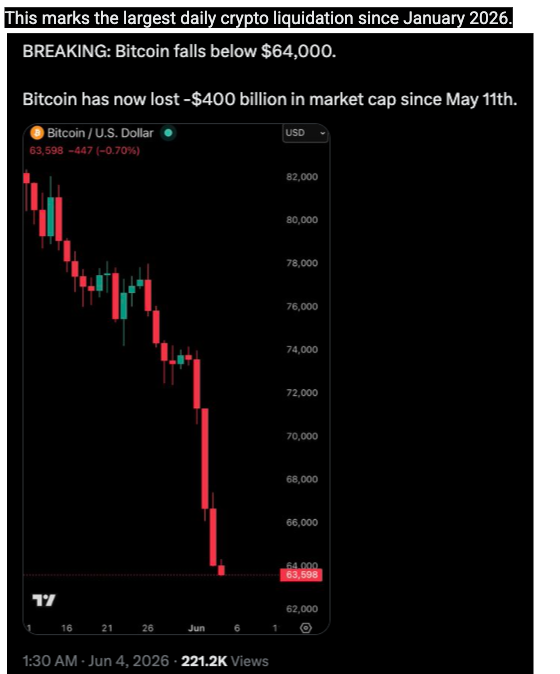

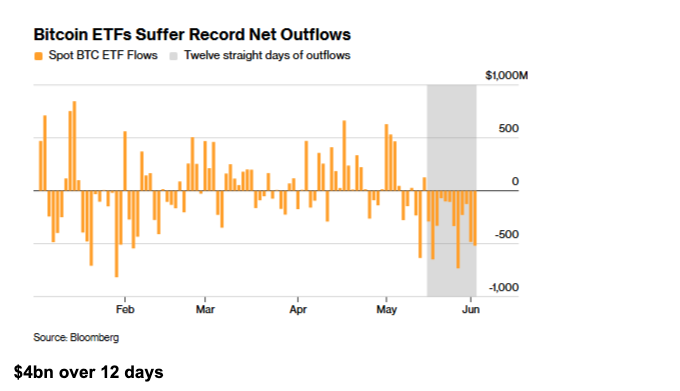

Crypto:

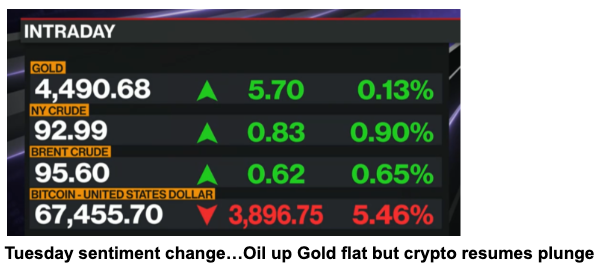

Crypto markets experienced a significant washout as ETF outflows, leveraged liquidations, and renewed selling pressure combined to drive sharp declines. Bitcoin briefly traded below key support levels before entering deeply oversold territory.

Oil:

Energy markets remained heavily influenced by geopolitical developments and supply-chain concerns. Market participants continued assessing both the risks to supply and the infrastructure investments designed to reduce future disruptions.

The Week Ahead: Key Data and Market-Moving Signals

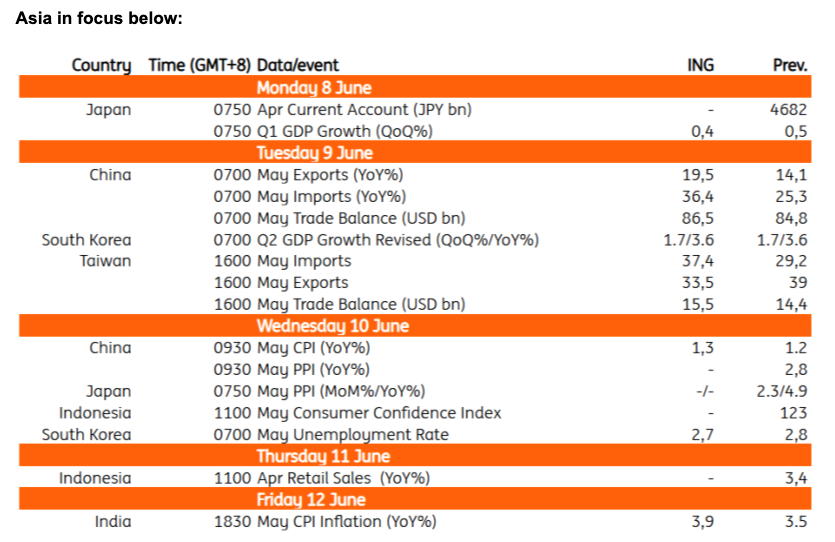

The week ahead is packed with market-moving catalysts, with US CPI, BoC and ECB rate decisions taking centre stage. Oracle earnings stand out as a potential risk point for technology sentiment, while the possibility of a SpaceX listing later in the week could provide another test for investor appetite toward high-profile growth stories. China trade and inflation data, Taiwan exports, and India CPI will provide further insight into global growth, AI demand, and inflation pressures.

Monday, June 8

• JP: GDP & GDP Annualized (Q1)

• JP: Current Account Data

• JP: Bank Lending

• JP: Economy Watchers Survey

• AU: Private Sector Credit

• DE: Factory Orders

• EU: Sentix Investor Confidence

• CA: Leading Index

• US: CB Employment Trends Index

• US: NY Fed Consumer Inflation Expectations

Tuesday, June 9

• KR: GDP

• JP: M2 Money Stock & M3 Money Supply

• AU: NAB Business Confidence & Business Survey

• CN: Trade Balance, Exports & Imports

• DE: Industrial Production

• DE: Trade Balance

• US: NFIB Small Business Optimism

• US: Trade Balance

• US: Existing Home Sales

• US: Wholesale Inventories

• US: Atlanta Fed GDPNow Update

• US: EIA Short-Term Energy Outlook

• US: API Crude Oil Stocks

• US: 3-Year Treasury Auction

Wednesday, June 10

• CN: CPI & PPI

• AU: Building Approvals

• US: CPI & Core CPI

• US: MBA Mortgage Applications

• CA: BoC Interest Rate Decision

• CA: BoC Rate Statement

• CA: BoC Press Conference

• US: Crude Oil Inventories

• US: Federal Budget Balance

• US: 10-Year Treasury Auction

• US: Oracle Earnings

Thursday, June 11

• JP: BSI Manufacturing Conditions

• EU: ECB Interest Rate Decision

• EU: ECB Monetary Policy Statement

• EU: ECB Press Conference

• US: PPI & Core PPI

• US: Initial Jobless Claims

• US: Continuing Jobless Claims

• CA: Building Permits

• US: OPEC Monthly Report

• US: WASDE Report

• EU: Eurogroup Meetings

Friday, June 12

• IN: CPI

• UK: GDP

• UK: Manufacturing Production

• UK: Industrial Production

• DE: CPI & HICP

• FR: CPI & HICP

• ES: CPI & HICP

• US: Michigan Consumer Sentiment

• US: Michigan 1-Year Inflation Expectations

• US: Michigan 5-Year Inflation Expectations

Alpha Takeaway: Strong Fundamentals, Rising Sensitivity

Alpha Takeaway: Strong Fundamentals, Rising Sensitivity

Markets remain supported by resilient growth, firm earnings expectations, and an AI investment cycle that continues expanding across the technology ecosystem. At the same time, elevated positioning, higher yields, and increasingly optimistic sentiment suggest markets have become more sensitive to disappointment.

Equities:

The broader earnings backdrop remains constructive. AI infrastructure spending continues supporting growth expectations, while earnings revisions remain firm. However, participation needs to broaden further, and positioning needs additional normalisation following the recent selloff.

Gold & Silver:

Precious metals continue balancing rising real yields against structural support from long-term supply-demand dynamics and central-bank demand. Recent weakness appears more closely linked to rates repricing than a change in the broader investment case.

Crypto:

Crypto remains in a significant de-risking phase. Liquidations, ETF outflows, and weaker sentiment have pressured prices, but attention remains focused on whether key support levels can stabilise positioning and confidence.

Macro:

Growth continues to dominate the narrative. Economic activity remains resilient, recession concerns remain muted, and policy expectations continue evolving in response to stronger data and firmer inflation pressures.

The broader trend remains supported by resilient growth, firm earnings expectations, and an AI investment cycle that continues attracting capital across the technology ecosystem. At the same time, rising yields, crowded positioning, and increasingly concentrated leadership suggest markets may become more sensitive to volatility as they work through a period of consolidation. As long as growth remains supportive and earnings expectations remain intact, the trend can persist, but positioning and participation are likely to remain key areas of focus beneath the surface.

CTA: https://docs.google.com/document/d/1QrWnaVQ3w52URJWOtazFakdZIafPDonm2baVbWC_lMQ/edit?tab=t.0