Liquidity Still Supporting Risk, But Inflation and Yield Stress Continue to Tighten Conditions

Markets continue to push higher, but the character of the move increasingly reflects a market being sustained by positioning and concentrated leadership rather than broad macro clarity. Strong earnings and persistent AI-related demand continue pulling capital back into equities, even as geopolitical developments and inflation pressures remain elevated beneath the surface.

At the same time, the broader structure is becoming more uneven. Bond markets continue to flash concern through higher yields, commodity markets remain sensitive to geopolitical headlines, and participation across equities continues to narrow. The result is a market that remains constructive overall, but with growing sensitivity to rates, inflation expectations, and leadership concentration.

Market Overview: Strong Leadership Continues to Mask Narrow Participation

Equities continue to hold firm, supported primarily by demand for AI infrastructure, technology leadership, and resilient earnings delivery. The rally remains heavily concentrated in large-cap growth and semiconductor exposure, with investors continuing to focus on pricing power, secular growth durability, and AI-linked capital expenditure themes.

The broader tone remains supportive as positioning continues pulling under-owned participants back into the market. Despite repeated geopolitical escalations and inflation concerns, volatility remains remarkably muted.

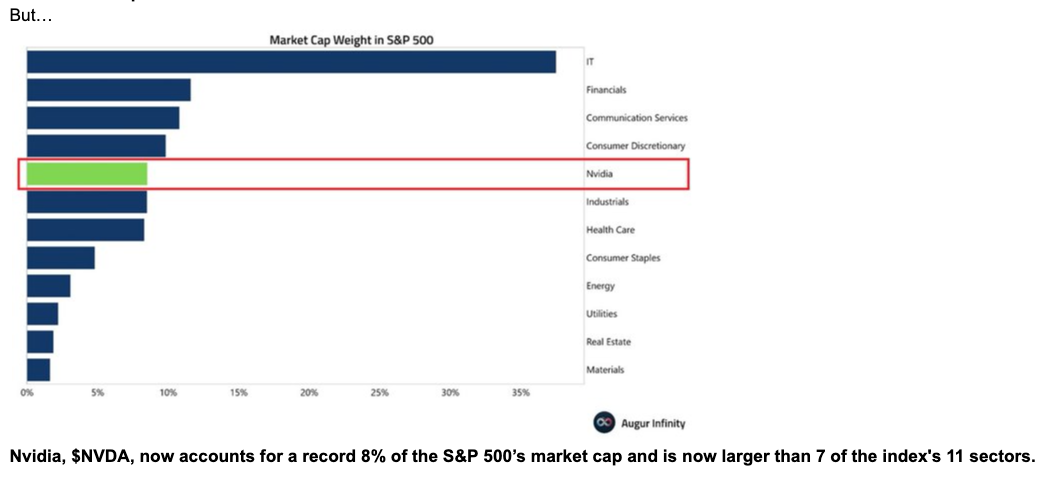

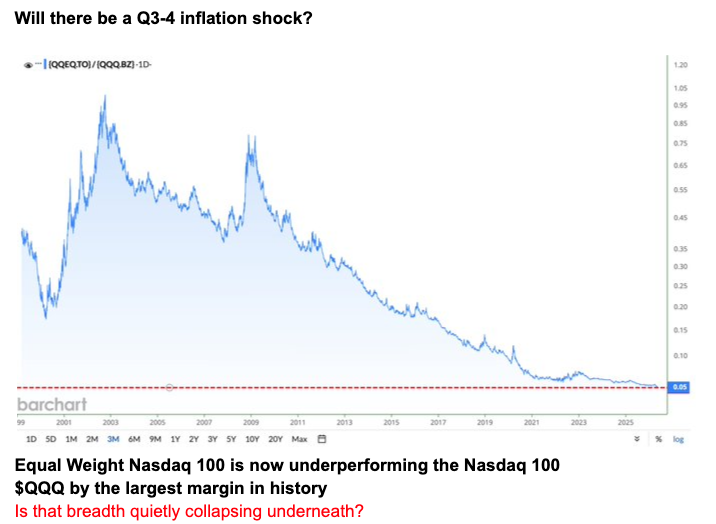

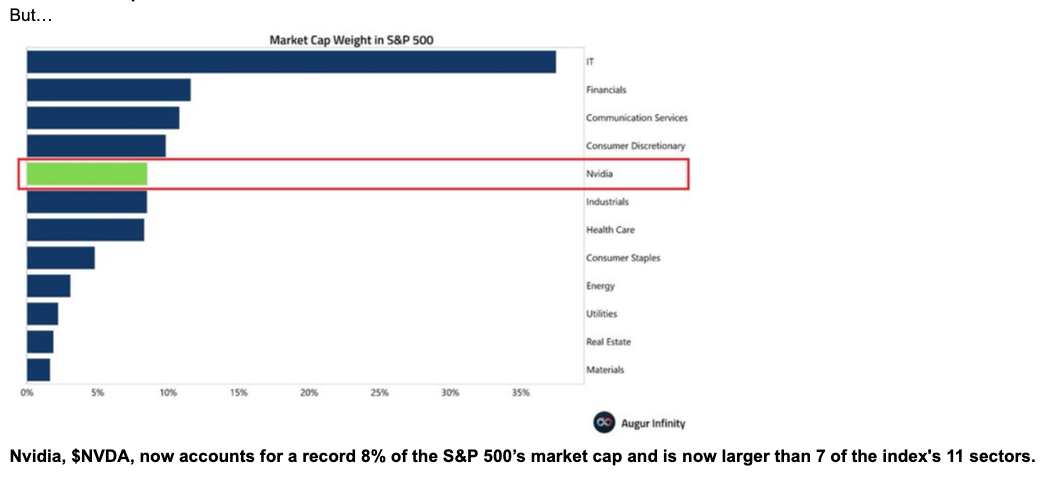

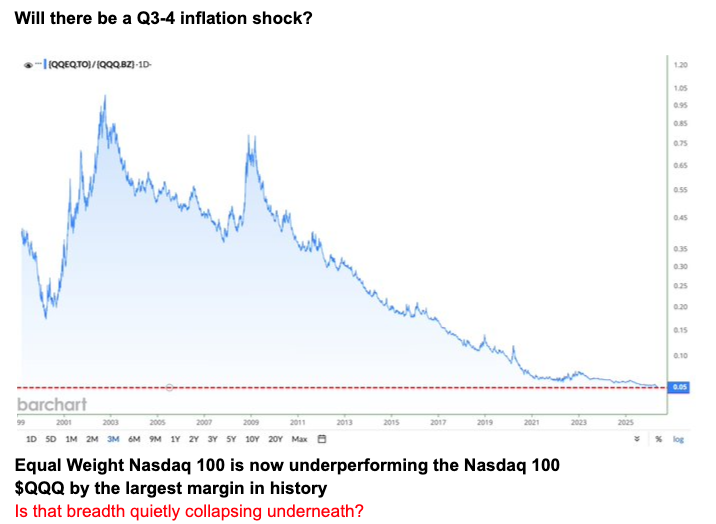

At the same time, participation continues lagging behind headline index performance. The market continues to show increasingly narrow leadership, with a relatively small group of AI-linked names carrying a significant portion of index gains.

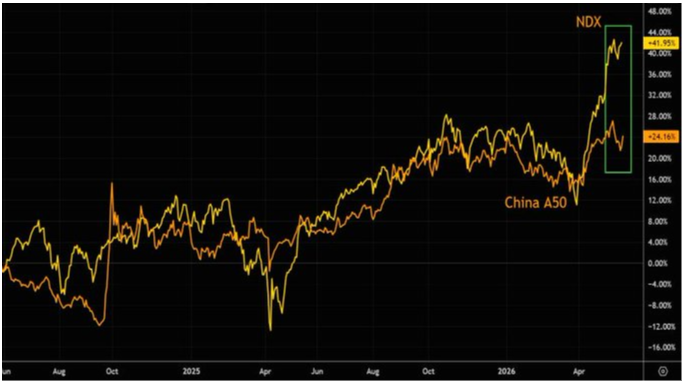

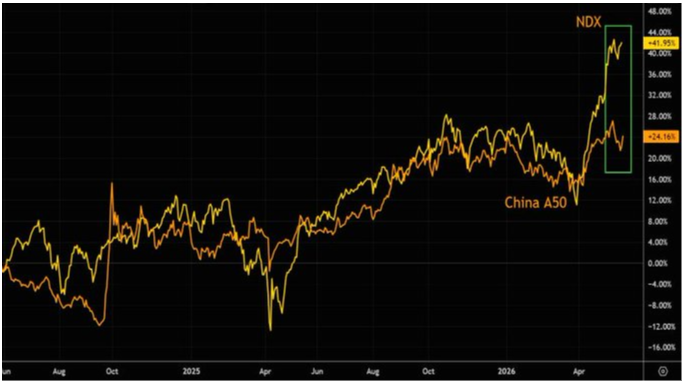

The AI narrative itself continues to broaden globally. China’s acceleration in AI model usage and token growth has become increasingly important for markets, reinforcing the idea that the AI race is becoming more globally competitive rather than concentrated entirely within the US.

The trend remains intact, but the internal quality of the move continues to weaken as concentration rises and broader participation struggles to keep pace with price.

Macro & Policy Watch: Inflation Risks Continue Feeding Through Rates and Commodities

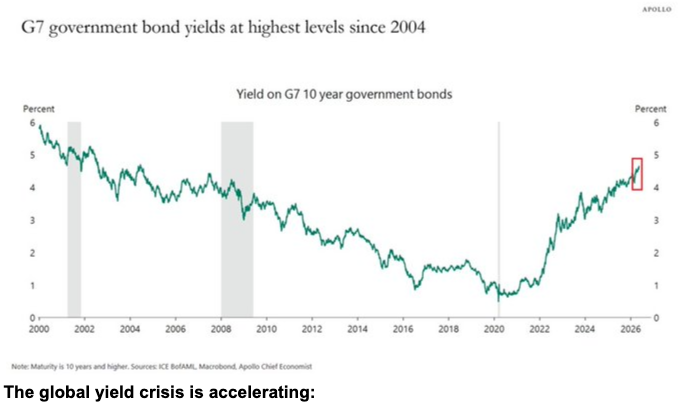

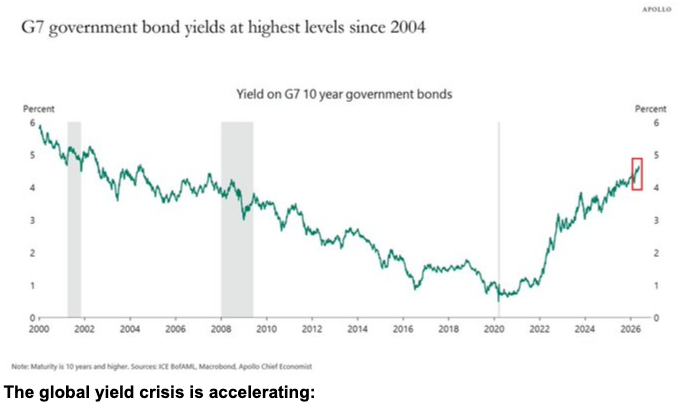

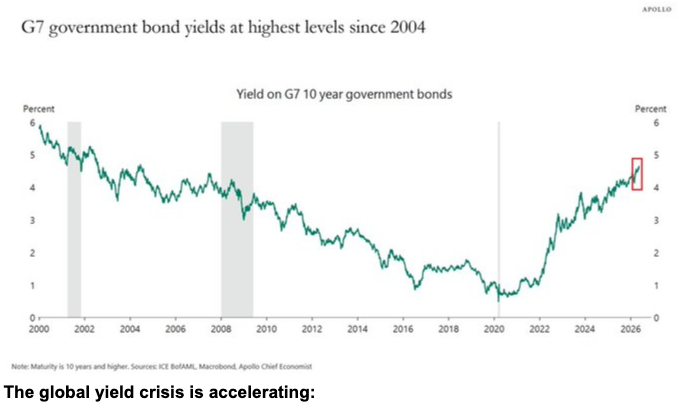

The macro environment continues revolving around inflation persistence, geopolitical risk, and tightening financial conditions through higher global yields.

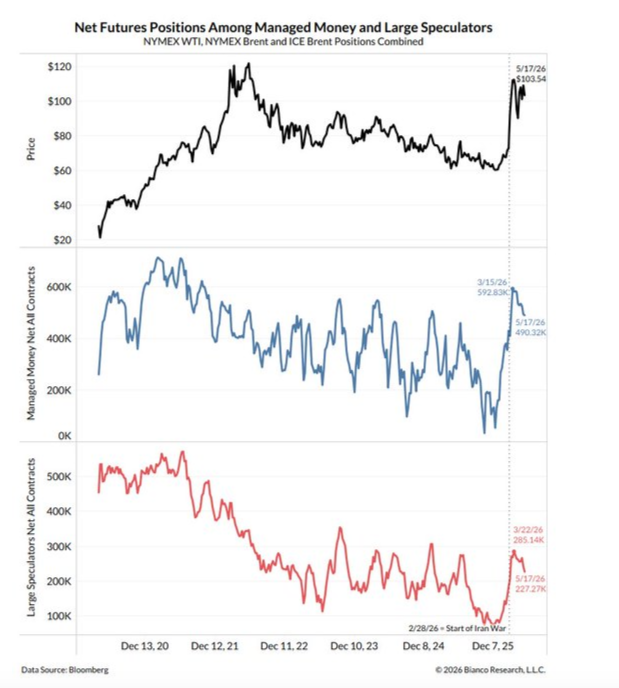

The ongoing conflict surrounding Iran and the Strait of Hormuz remains central to the broader macro narrative. Markets repeatedly shifted between optimism surrounding negotiations and renewed escalation concerns, creating sharp reversals across oil, rates, and risk assets. The market continues trading in a “deal or no deal” environment, with geopolitical headlines driving short-term positioning and commodity volatility.

At the same time, inflation concerns continue feeding directly into sovereign bond markets. Global government bond yields remain elevated as investors increasingly demand compensation for inflation persistence, large fiscal deficits, and ongoing geopolitical instability.

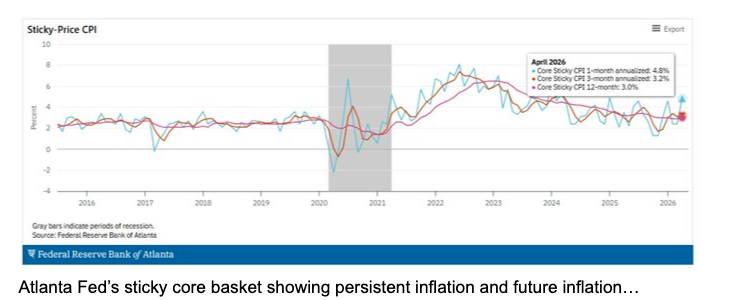

The report repeatedly highlights that inflation pressure remains more persistent than many expected. Sticky inflation measures, shelter costs, and energy-linked pricing continue reinforcing the “higher for longer” policy backdrop across developed markets.

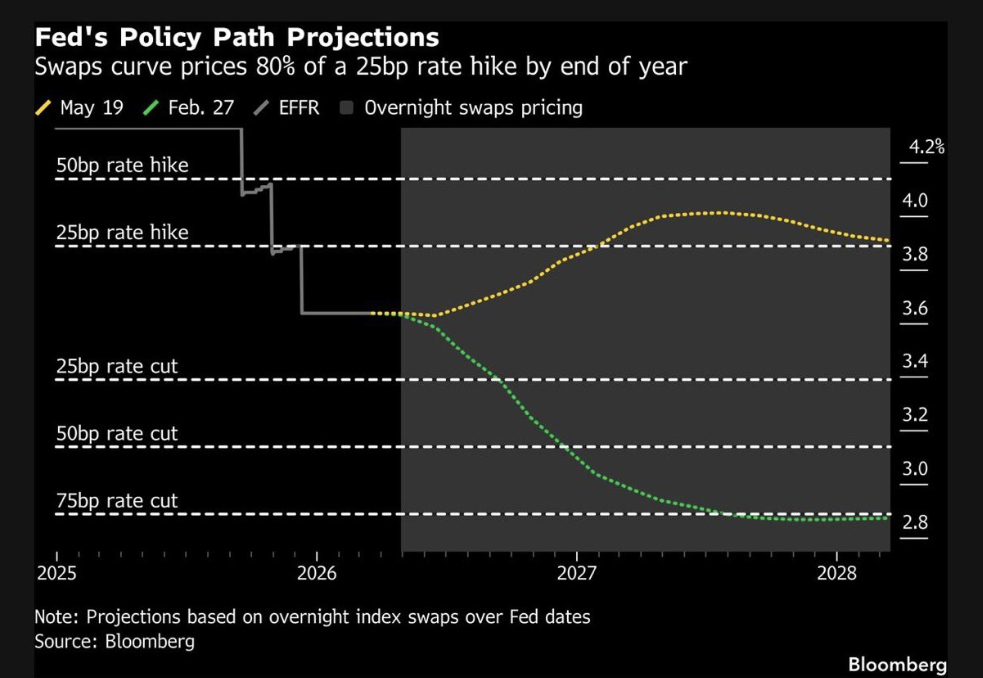

Markets continue to reprice policy expectations accordingly. Swaps continue implying that rate cuts may remain limited while the probability of tighter policy remains elevated relative to earlier expectations.

Meanwhile, commodities continue reflecting both geopolitical instability and structural inflation pressure. Oil remains central to the broader macro narrative, while precious metals continue consolidating within a supportive macro backdrop driven by inflation and sovereign debt concerns.

Overall, macro conditions remain increasingly restrictive beneath the surface as higher yields, persistent inflation, and geopolitical uncertainty continue interacting simultaneously.

Technical & Sentiment Breakdown: Supportive, but Increasingly Fragile

The broader trend remains constructive, with equities continuing to push higher as liquidity conditions and earnings momentum remain supportive. Historical trend structures continue to support the broader uptrend while volatility remains contained.

However, internal confirmation continues weakening. Breadth deterioration remains one of the clearest themes beneath the surface, with fewer stocks increasingly responsible for sustaining index-level performance.

Positioning also remains heavily concentrated. Crowded growth exposure, elevated call skew, and continued systematic participation all suggest that the market remains increasingly dependent on concentrated leadership and positioning support.

At the same time, passive inflows and ETF-related participation continue supporting broader indices despite increasingly selective participation underneath the surface.

The broader trend remains intact for now, but the combination of concentrated leadership, weakening breadth, and elevated positioning suggests a market that is becoming more sensitive to disappointment, particularly if rates continue rising or earnings leadership begins to soften.

Last Week’s Recap: Strong Earnings, Rising Yields, and Persistent Inflation Concerns

The past week was characterised by continued strength across equities despite increasingly visible pressure building across rates, inflation expectations, and geopolitical markets. AI leadership and earnings momentum remained supportive, while bond markets and commodities continued reflecting persistent macro stress beneath the surface.

Key Highlights:

- Macro:

Global yields continued moving higher as inflation concerns remained persistent across energy, housing, and sovereign debt markets. Sticky inflation dynamics and elevated commodity prices continued to reinforce the broader “higher for longer” narrative.

- China:

China remained central to the broader AI narrative as token usage and model adoption continued accelerating. Markets also continued focusing on China’s role within the broader global growth and industrial demand backdrop.

- Earnings:

Earnings remained a key pillar of support for equities, particularly across technology, semiconductors, and AI-linked leadership. Strong delivery and forward guidance continued to reinforce the broader growth narrative despite rising macro pressure. - Commodities:

Commodity markets remained firm as geopolitical developments and inflation concerns continued to feed through energy and industrial pricing dynamics. Gold continued consolidating while broader commodity strength remained intact.

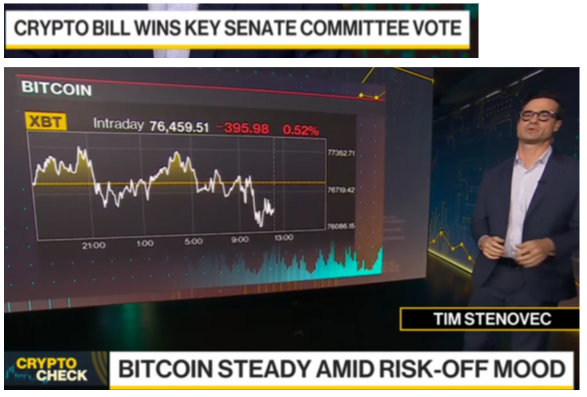

- Crypto:

Crypto markets remained volatile alongside broader liquidity and positioning dynamics. Bitcoin retraced alongside risk-off flows, though broader technology-driven participation remained supportive overall.

- Oil:

Oil markets remained highly sensitive to geopolitical headlines throughout the week, with repeated reversals driven by developments surrounding Iran, Strait of Hormuz tensions, and ceasefire speculation.

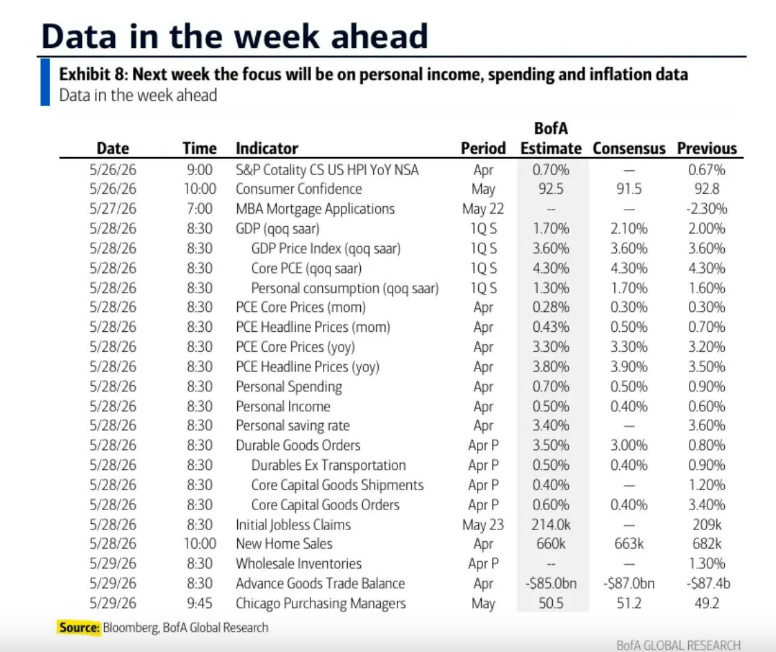

The Week Ahead: Key Data and Market-Moving Signals

The week ahead is lighter on macro data, but PCE inflation, GDP components, housing data, and inflation readings across Europe and Japan will remain central for rate expectations. Markets will also closely watch heavy Fed and central bank commentary for further confirmation of the “higher for longer” policy backdrop.

Monday, May 25

• US: Memorial Day Holiday

• UK: Spring Bank Holiday

• Switzerland: Whit Monday Holiday

• Hong Kong: Birthday of the Buddha Holiday

• South Korea: Vesak Day Holiday

• China: FDI Data

• Canada: Wholesale Sales and Corporate Profits

Tuesday, May 26

• Japan: BoJ Core CPI and Leading Index Data

• Spain: PPI Data

• UK: CBI Distributive Trades Survey

• US: Chicago Fed National Activity Index

• US: Case-Shiller Home Price Data

• US: Consumer Confidence

• US: M2 Money Supply

• ECB Financial Stability Review

• ECB’s Sleijpen Speaks

• US: 2-Year Note Auction

Wednesday, May 27

• Australia: CPI and Inflation Measures

• China: Industrial Profits

• New Zealand: RBNZ Interest Rate Decision

• US: ADP Employment Change

• US: Richmond Fed Manufacturing Data

• US: API Crude Oil Inventories

• Fed’s Kashkari Speaks

• Fed Logan Speaks

• ECB Press Conference

• BoJ Governor Ueda Speaks

Thursday, May 28

• South Korea: Interest Rate Decision

• Europe: Consumer Inflation Expectations

• US: Initial Jobless Claims

• US: Core PCE Price Index

• US: PCE Inflation Data

• US: GDP and GDP Price Index

• US: Durable Goods Orders

• US: Personal Spending and Income

• US: Corporate Profits

• US: New Home Sales

• US: Crude Oil Inventories

• FOMC Member Williams Speaks

• ECB President Lagarde Speaks

• ECB’s Schnabel Speaks

Friday, May 29

• Japan: Tokyo CPI and Industrial Production

• France: CPI and GDP Data

• Spain: CPI Data

• Germany: CPI and Labour Market Data

• Italy: CPI and GDP Data

• Canada: GDP Data

• US: Goods Trade Balance

• US: Wholesale Inventories

• US: Chicago PMI

• BoE Governor Bailey Speaks

• Fed’s Bowman Speaks

Alpha Takeaway: Liquidity Still Supportive, But Internal Conditions Continue Tightening

Markets remain supported by earnings, AI leadership, and positioning flows, but the broader balance of risks continues shifting as inflation persistence, higher yields, and geopolitical pressures build beneath the surface.

- Equities:

Equities continue benefiting from strong earnings delivery and concentrated AI leadership, though participation remains increasingly narrow and dependent on a relatively small group of leaders. - Gold & Silver:

Precious metals continue reflecting broader inflation, sovereign debt, and geopolitical dynamics rather than functioning purely as defensive assets. - Crypto:

Crypto remains closely tied to broader liquidity and positioning dynamics, with volatility continuing to respond to shifts in market positioning. - Macro:

Higher yields, persistent inflation pressures, and geopolitical energy risks continue tightening macro conditions, even as headline equity indices remain resilient.

The broader trend remains constructive, but the internal structure continues to become more fragile as participation narrows and macro pressure builds underneath the surface. The market continues moving higher, though participation and breadth remain increasingly uneven. A deal feels imminent with Iran but what concessions are required. Flows will move elsewhere out of necessity. Early oil speculators are moving on and bond players are extreme short. Will June end Q2 on a high or will a solution to the SoH be a travel and arrive moment?