Stabilising Uncertainty, Resilient Structure Beneath Softening Growth

Markets are beginning to adjust to a more defined risk environment, where uncertainty has not disappeared, but has become more measurable. The shift from unknown outcomes to priced risk is allowing markets to stabilise, even as headlines continue to dominate the narrative.

Liquidity remains supportive, and indices continue to hold, but participation is not broad-based conviction. Beneath the surface, growth is softening, and sentiment remains cautious, creating a market that is functioning through uncertainty rather than resolving it.

Market Overview: Resilience Holding Despite Macro Friction

Equity markets continue to show resilience, with broader participation beginning to improve after a period of narrow leadership. The structure suggests that while conviction is not overwhelming, flows are gradually returning, particularly as uncertainty becomes more defined.

The key driver remains the interaction between macro uncertainty and positioning. As uncertainty stabilises, even without fully resolving, it reduces the need for elevated risk premia. This has allowed markets to hold levels despite ongoing concerns around inflation, growth, and geopolitics.

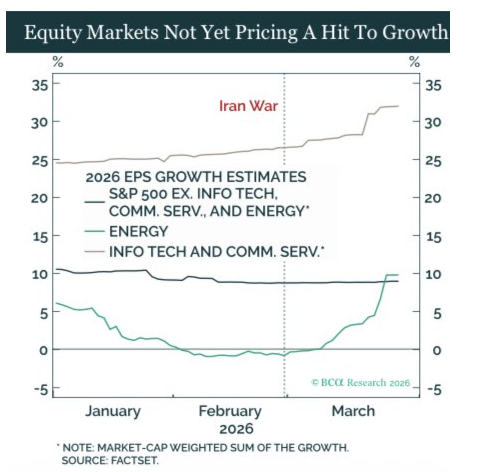

At the same time, earnings expectations remain intact, and there is no clear evidence yet of a meaningful deterioration in forward projections. This continues to act as a stabilising anchor for equities.

Macro & Policy Watch: Inflation Contained, Growth Losing Momentum

The macro backdrop remains finely balanced.

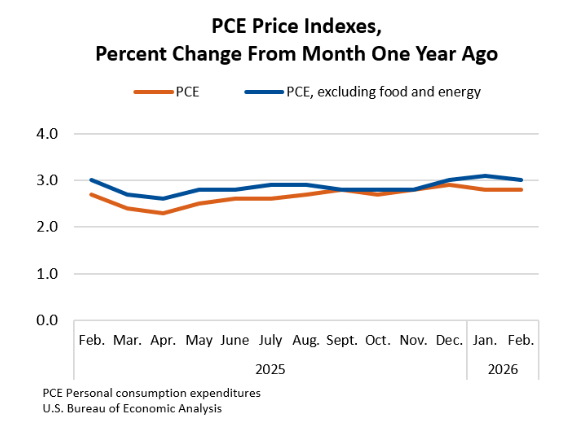

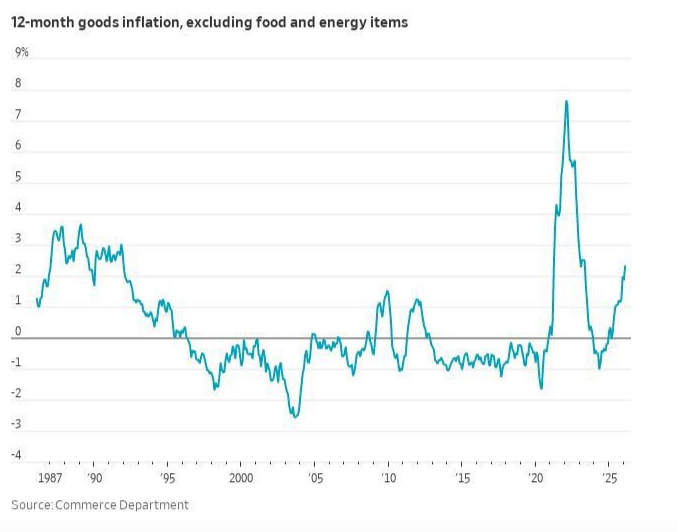

Inflation data continues to show limited pass-through into core measures. Price pressures are primarily concentrated in goods, while services and housing remain relatively muted. Core inflation is elevated, but not accelerating in a way that forces immediate policy response.

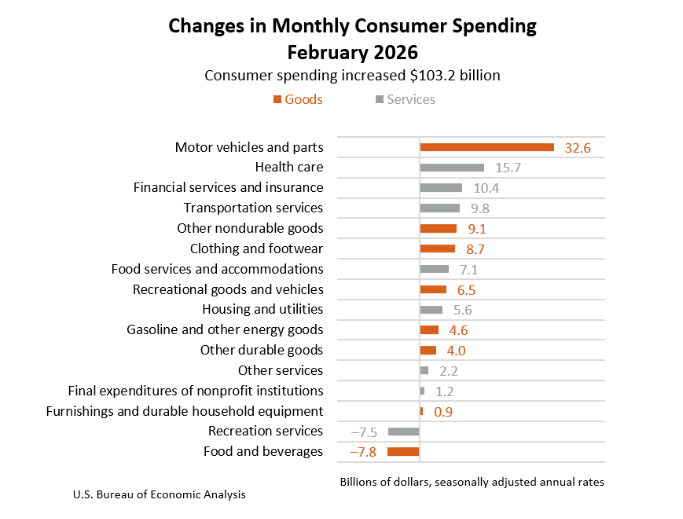

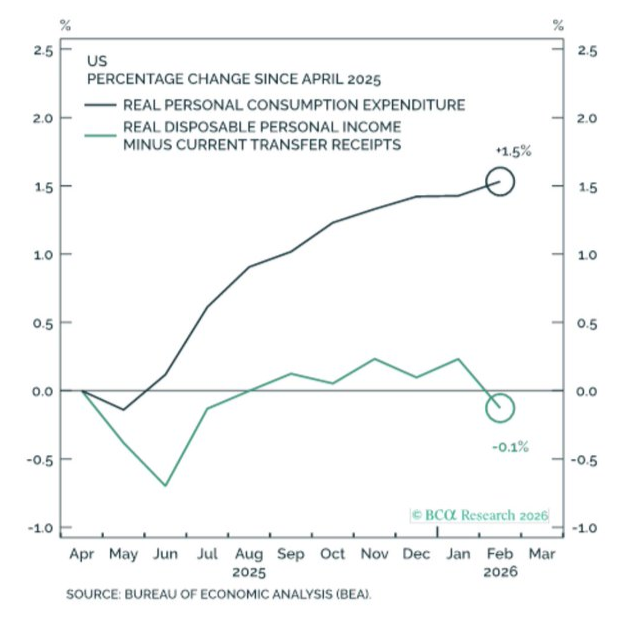

At the same time, growth is beginning to soften. Consumer spending is weakening, and income trends are slipping, with increasing reliance on transfers rather than organic demand.

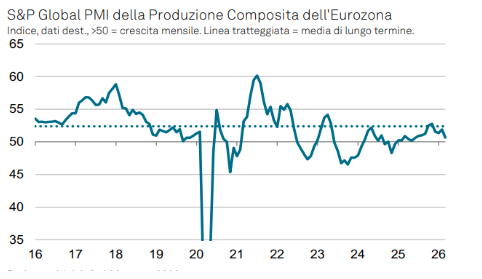

Globally, the divergence remains clear. While the US continues to show resilience, Europe is flatlining, with business activity stagnating and momentum fading across major economies.

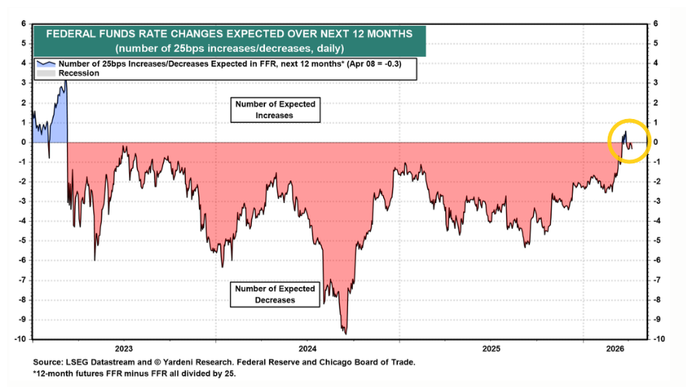

Policy remains caught between these opposing forces. Central banks are navigating dual-sided risks, with neither inflation nor growth providing a clear directional signal.

Technical & Sentiment Breakdown: Supportive, but Increasingly Fragile

Market structure remains intact, but there are signs that momentum is becoming more dependent on flows than conviction.

Breadth has improved, and key indices are holding important levels, suggesting that underlying demand remains present. However, this demand appears reactive rather than aggressive, with positioning still relatively light.

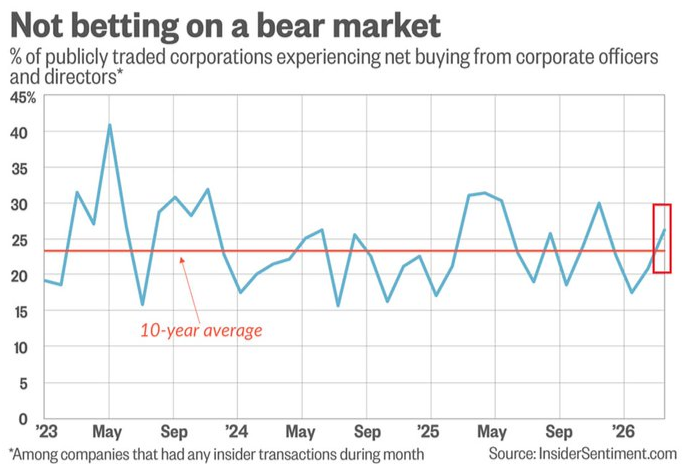

Sentiment indicators show a shift away from extreme bearishness, with bears reducing exposure and insiders increasing activity. This supports the view that the market is transitioning from defensive positioning toward a more neutral stance.

At the same time, volatility measures are easing, and correlations are declining, both of which are typically supportive of equity markets. However, this also introduces a risk of complacency if macro conditions deteriorate.

The overall setup suggests a market that is supported, but not without fragility, particularly if macro data begins to weaken further.

Last Week’s Recap: From Volatility to Stabilisation

The past week saw a transition from headline-driven volatility toward a more stable footing, as macro data and geopolitical developments began to provide clearer direction.

Key Highlights:

Macro:

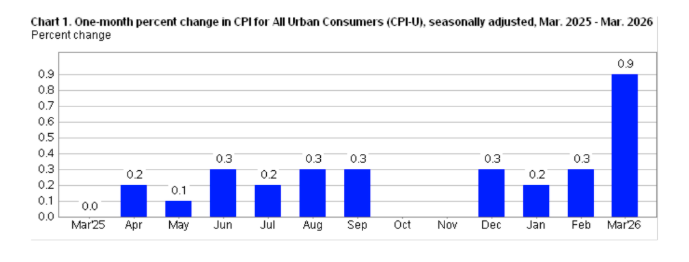

Inflation data surprised to the downside, with CPI missing expectations and core measures remaining stable. Growth indicators, however, showed early signs of slowing, particularly in consumption and income dynamics.

China:

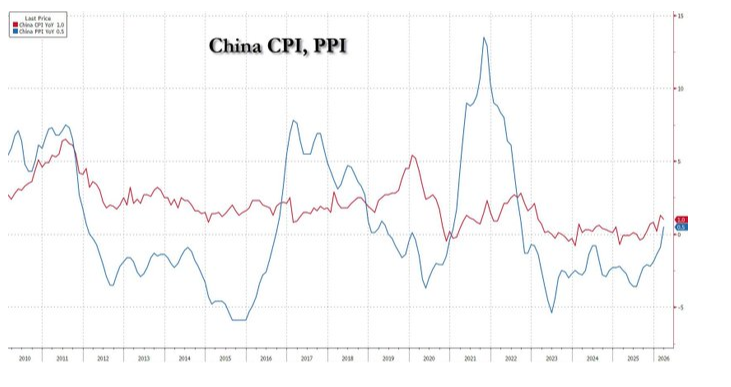

There are indications that deflationary pressures may be easing, with price dynamics stabilising after a prolonged period of weakness and policy support helping sentiment at the margin.

Earnings:

Earnings season is beginning, with focus shifting toward forward guidance, energy impacts, and the effect of rising input costs on margins and outlook expectations.

Commodities:

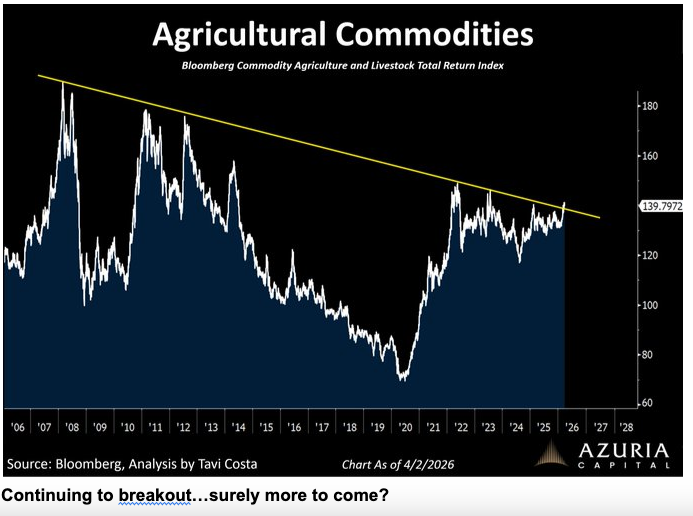

Commodities continue to show strength, with broader indices pushing higher and positioning suggesting continued interest as a macro hedge amid inflation uncertainty.

Crypto:

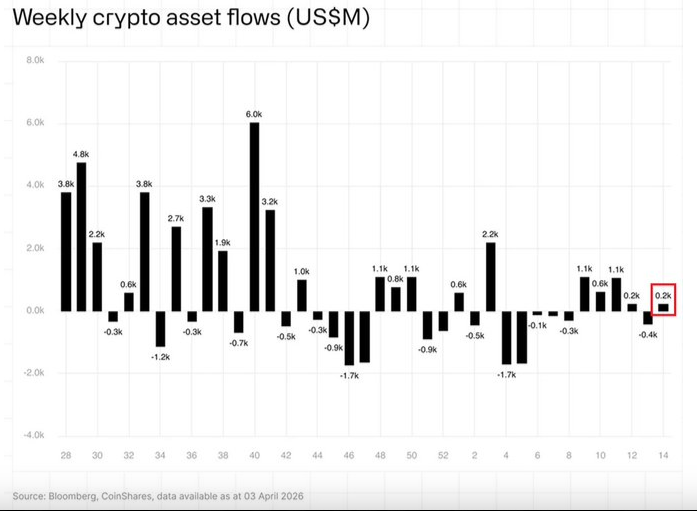

Crypto markets are testing key resistance levels, with flows turning positive after a period of weakness and inflows beginning to pick up again.

Oil:

Oil remains at a critical technical juncture, requiring a higher high to confirm strength, while failure to do so opens the risk of downside and potential trend weakness.

The Week Ahead: Key Data and Market-Moving Signals

The week is driven by a heavy macro calendar alongside the start of earnings season, with a focus on inflation signals, growth data, and China activity. Markets will be reacting through the lens of rates, commodities, and positioning, with data likely shaping expectations around growth resilience and inflation pass-through.

Monday, April 13

- China: New Loans, M2 Money Supply, Loan Growth

- US: Existing Home Sales (MoM, headline)

- Canada: Building Permits

- US: 3-month and 6-month bill auctions

- IMF Meetings

Tuesday, April 14

- China: Trade Balance, Exports and Imports

- Australia: Consumer Sentiment, Business Confidence

- Japan: Industrial Production, Capacity Utilisation

- Spain: CPI, Core CPI

- US: PPI (MoM, YoY) and Core PPI

- US: Small Business Optimism

- US: API crude oil inventories

- IEA Monthly Report

- BoE Governor Bailey speaks

Wednesday, April 15

- Korea: Trade Data (Exports, Imports, Balance)

- France: CPI, HICP

- EU: Industrial Production

- India: Trade Balance, Exports and Imports

- US: Empire Manufacturing Index

- US: Import and Export Prices

- US: Mortgage Data (Applications, Rates)

- US: Crude Oil Inventories

- US: Beige Book

- IMF Meetings

- BoE Governor Bailey speaks

Thursday, April 16

- China: GDP (QoQ, YoY), Industrial Production, Retail Sales, Unemployment

- UK: GDP, Industrial and Manufacturing Production, Trade Balance

- EU: CPI, Core CPI, HICP

- Switzerland: PPI

- US: Initial Jobless Claims, Continuing Claims

- US: Philadelphia Fed Index (Prices, Employment, New Orders)

- US: Industrial Production, Capacity Utilisation

- ECB Monetary Policy Account

- SNB Policy Assessment

- FOMC Member Williams speaks

Friday, April 17

- EU: Trade Balance, Current Account

- Italy: Trade Balance

- India: Bank Loan Growth, FX Reserves

- Canada: Housing Starts, Foreign Securities Purchases

- US: FOMC Member Barkin speaks

- IMF Meetings

Alpha Takeaway: Positioning Rebuild Meets Macro Uncertainty

Markets are transitioning into a phase where uncertainty is stabilising, but not resolved, and positioning is beginning to rebuild against that backdrop. Risk is becoming more measurable, allowing pullbacks to hold.

Equities:

Equity markets remain supported by stable earnings expectations and improving breadth, with equal-weight indices holding key levels. Upside depends on earnings holding and flows continuing to rebuild. Systematic flows are now positive unless VIX holds above 30.

Gold & Silver:

Precious metals remain supported by macro uncertainty and softer dollar dynamics, with lower rate expectations and EM pressure easing. Bonds and rates remain the key short-term driver.

Crypto:

Crypto is seeing improving flows and testing resistance, with inflows turning positive after weakness. Sustained momentum is needed for confirmation.

Macro:

The macro environment remains mixed, with inflation contained but growth slowing, and central banks balancing dual-sided risks. Consumer weakness and global divergence remain key concerns.

The setup reflects stabilising conditions with underlying fragility still present. As long as uncertainty continues to compress and no major negative surprises emerge, markets can continue to hold and grind within this range.