Tariffs, Tech, and Tactical Bottoms

This Week’s Trading Forecast Dives Into Tariff Turmoil, Macro Crosscurrents, Tech Tremors, and Golden Momentum

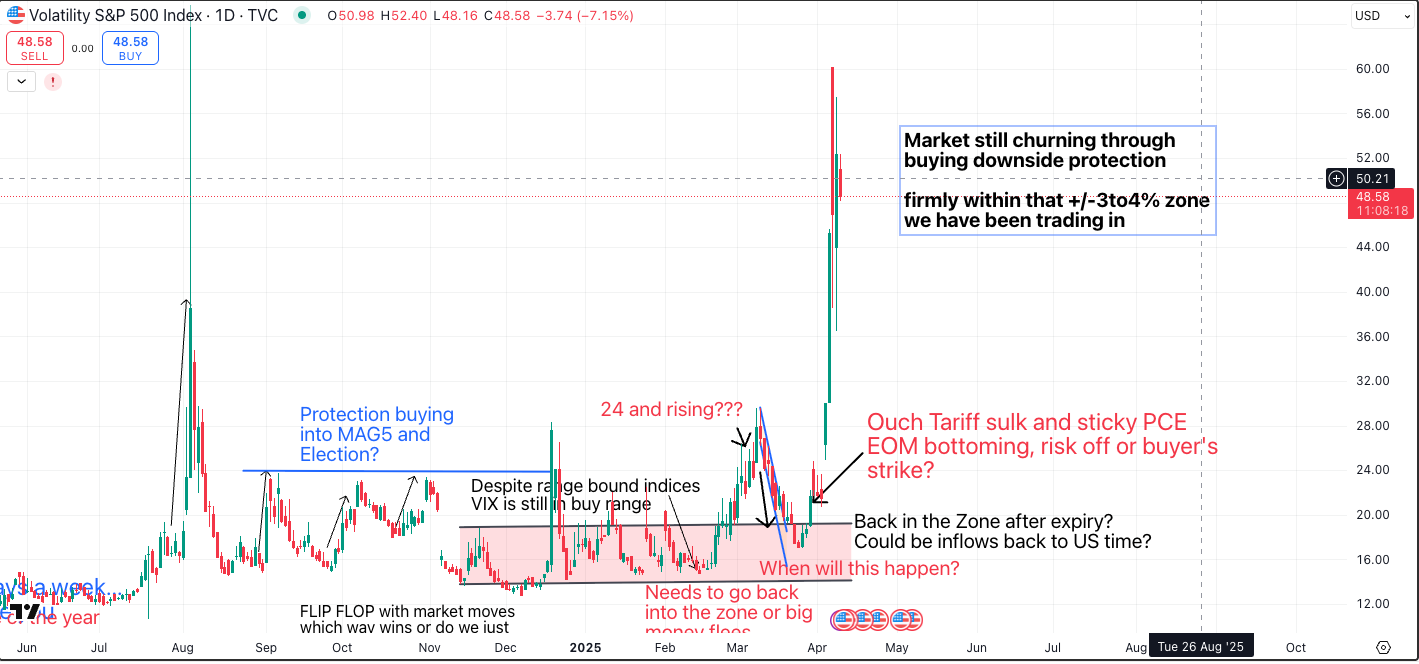

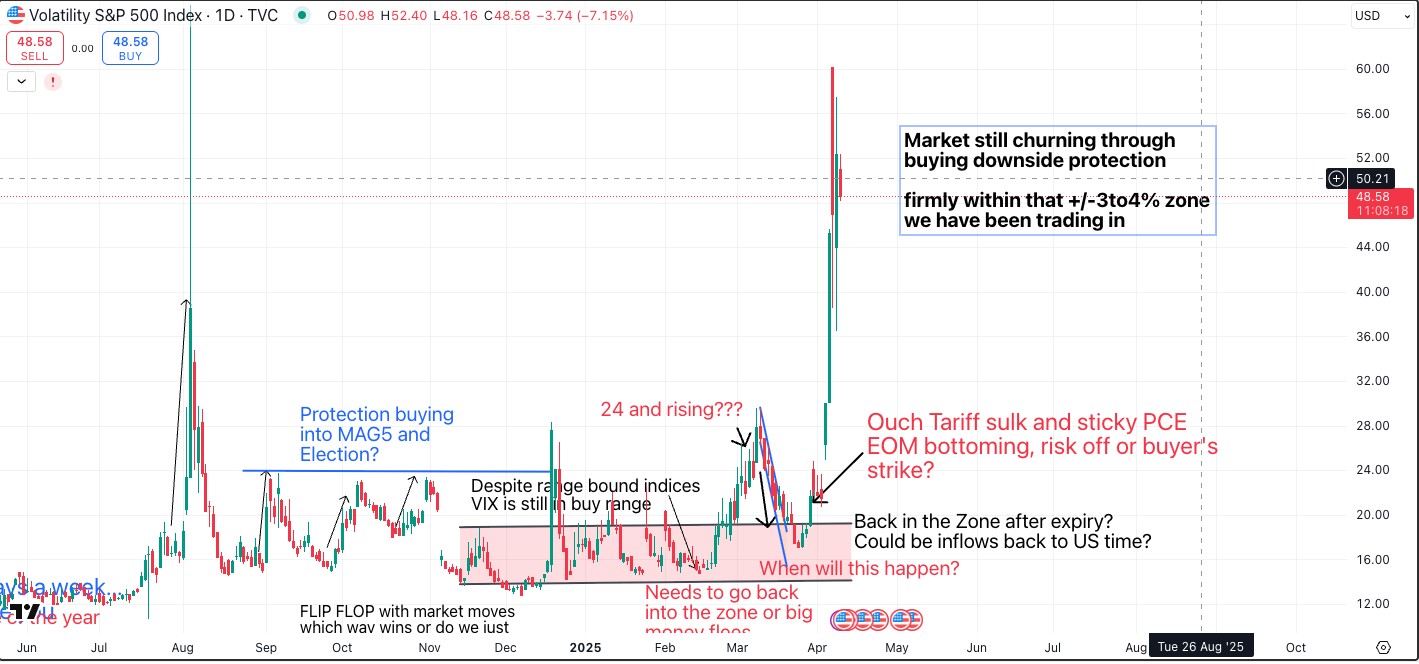

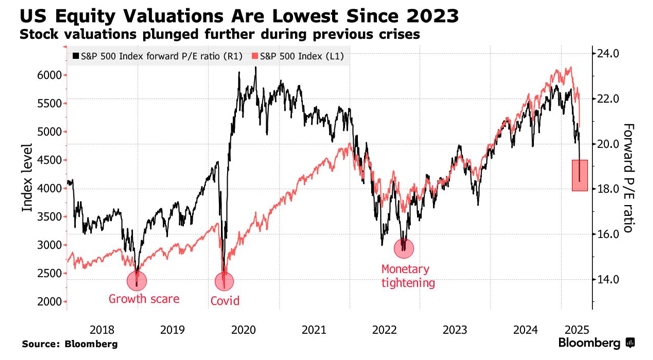

Markets flirt with a bottom as volatility spikes.

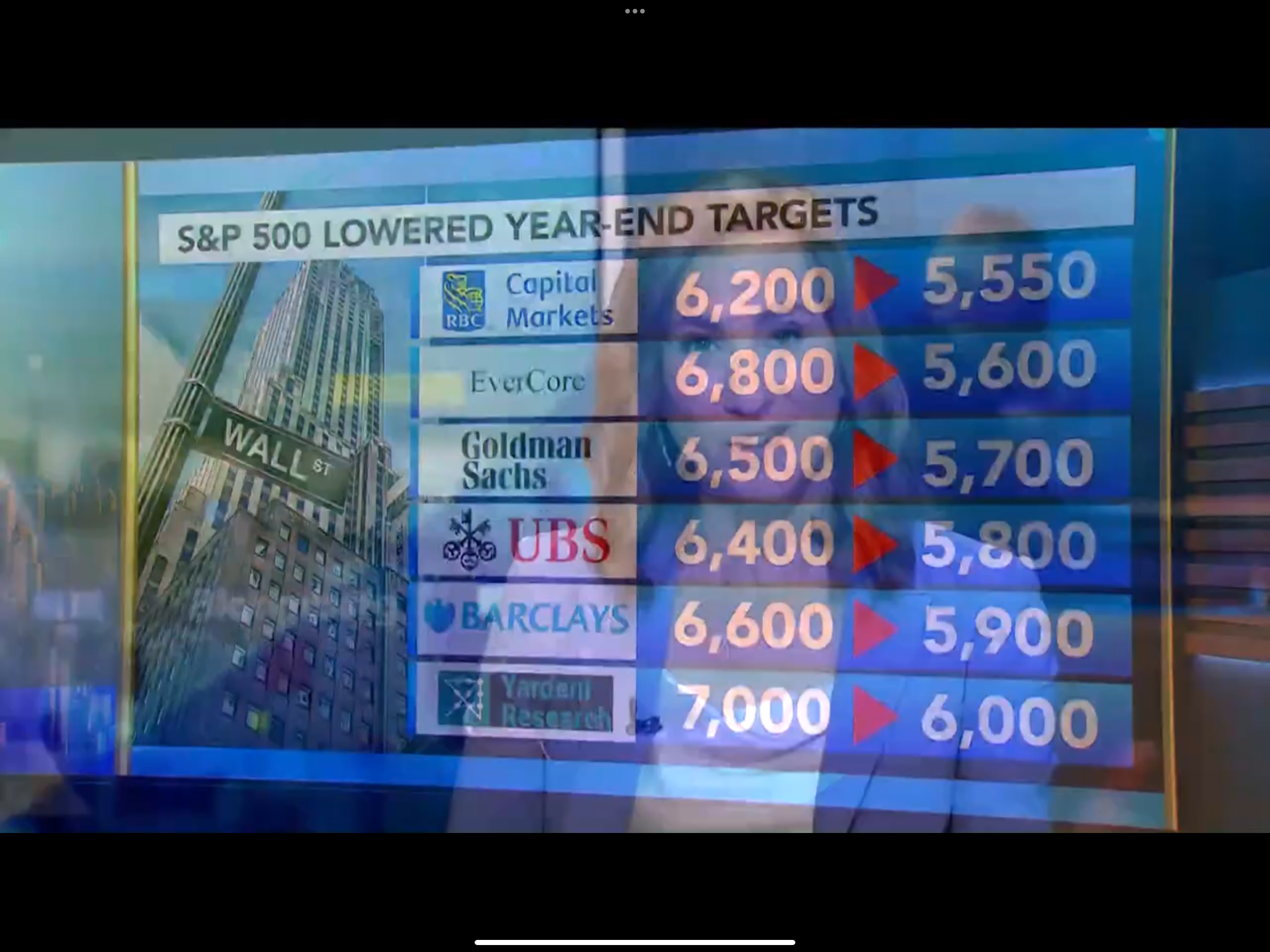

Market Overview: Bottoming or Just Bouncing?

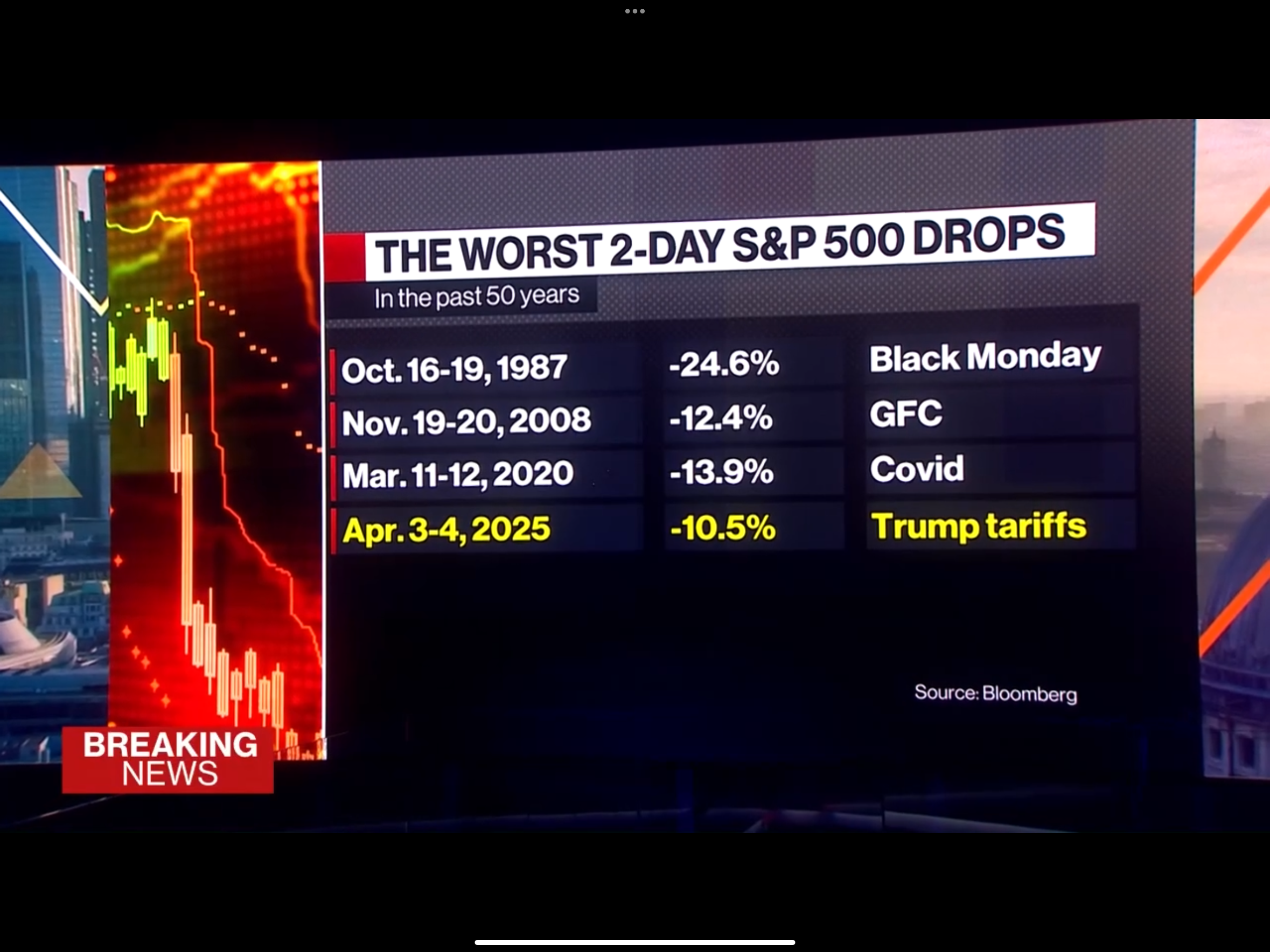

Last week was peak macro theater. Tariffs, fake news headlines, and bond market fireworks kept traders pinned to terminals. Equities staged a powerful bounce, but was it the start of something real, or just another dead cat in a bear suit?

- UoM sentiment at 2009 lows

- VIX spiked, then reversed sharply midweek

- S&P’s 2-day bounce among strongest in decades

- Fear is thick, but so is opportunity

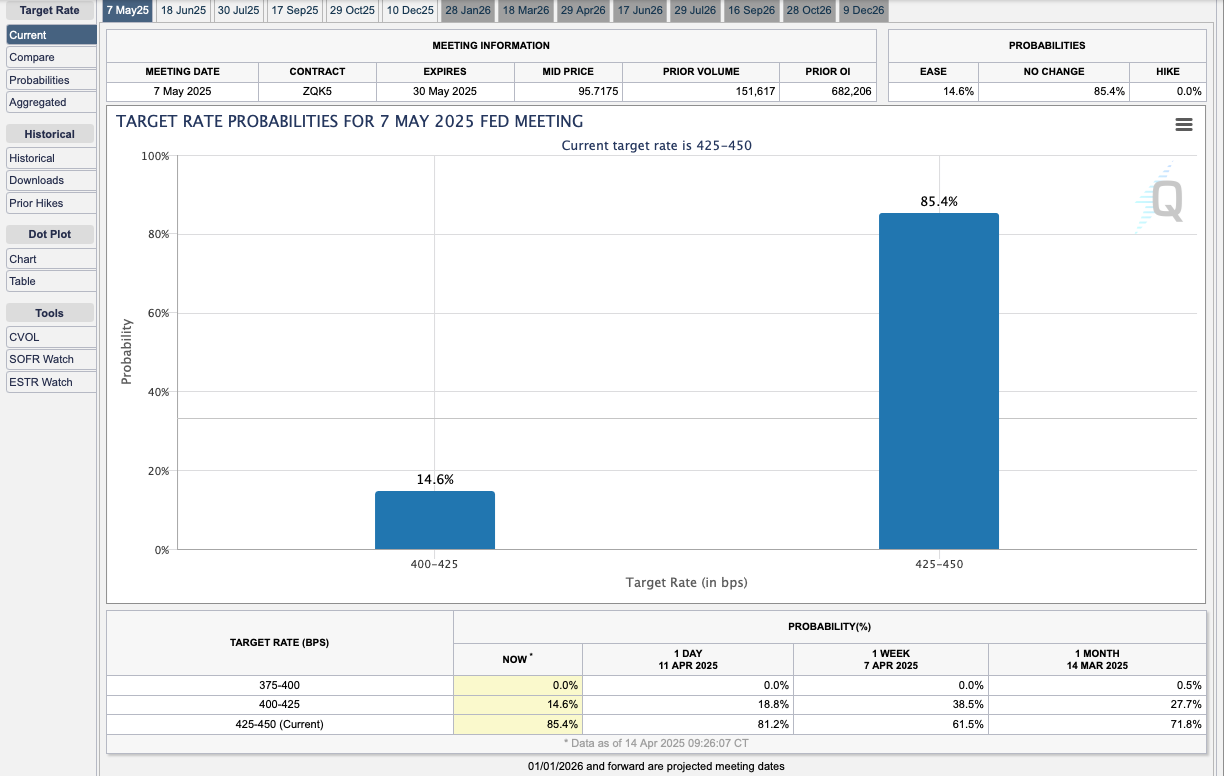

Macro & Policy Watch: Tariff Fireworks and Bond Tantrums

Trump’s Tech Targeting

Supply chains are a mess. Apple, Broadcom, and TSMC caught in the blast zone.

Broadcom’s $10B buyback was both signal and shield.

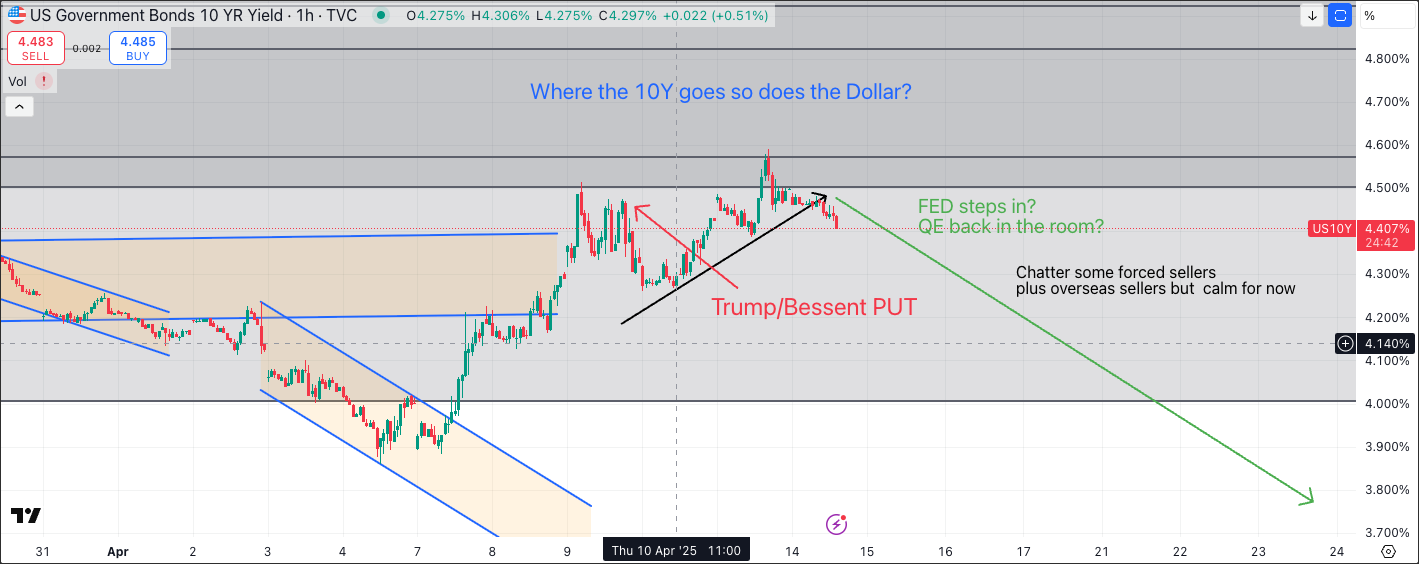

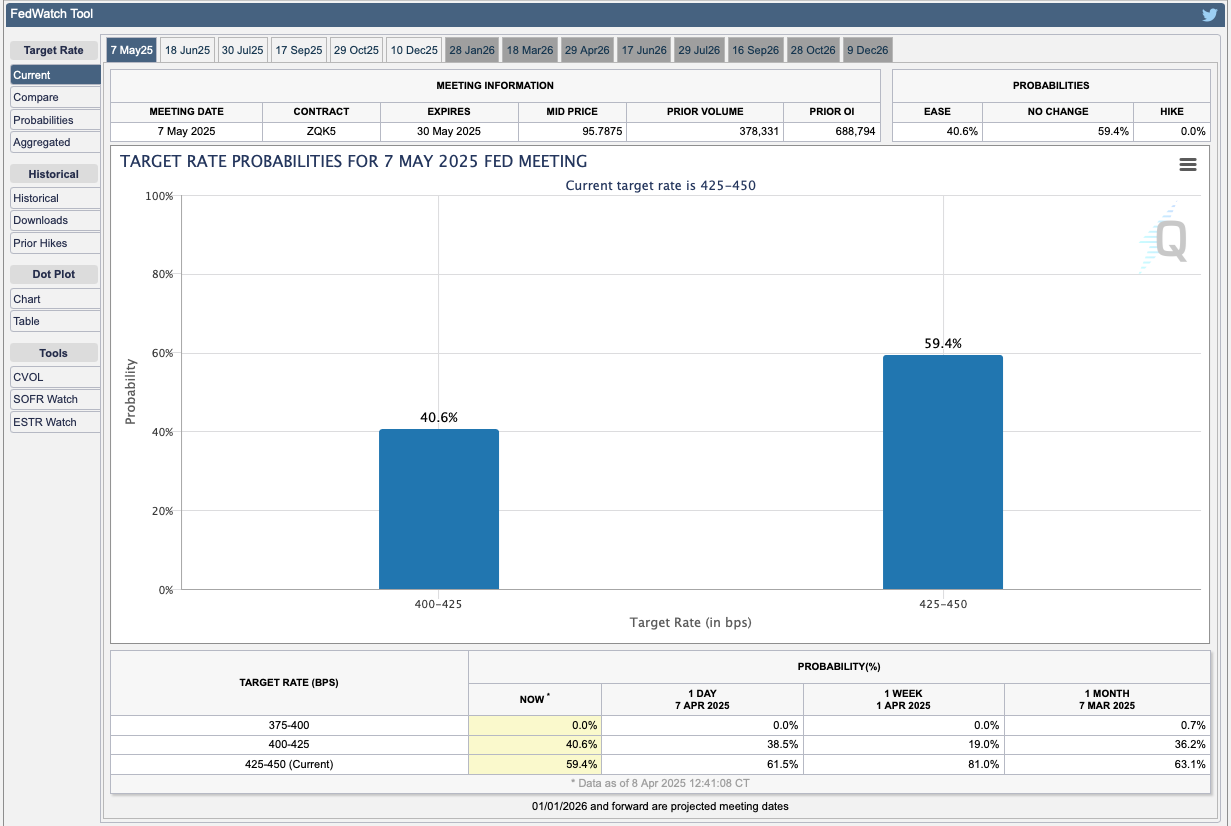

Bonds: Dysfunctional by Design?

The US10Y nearly touched 4.5% as yields screamed higher across the board. The market is panicking about inflation, but the Fed? Silent.

- ECB set to cut 25bps this week

- Cross-border bond selling suggests real stress, not just rate expectations

- DXY breakdown adds to the confusion

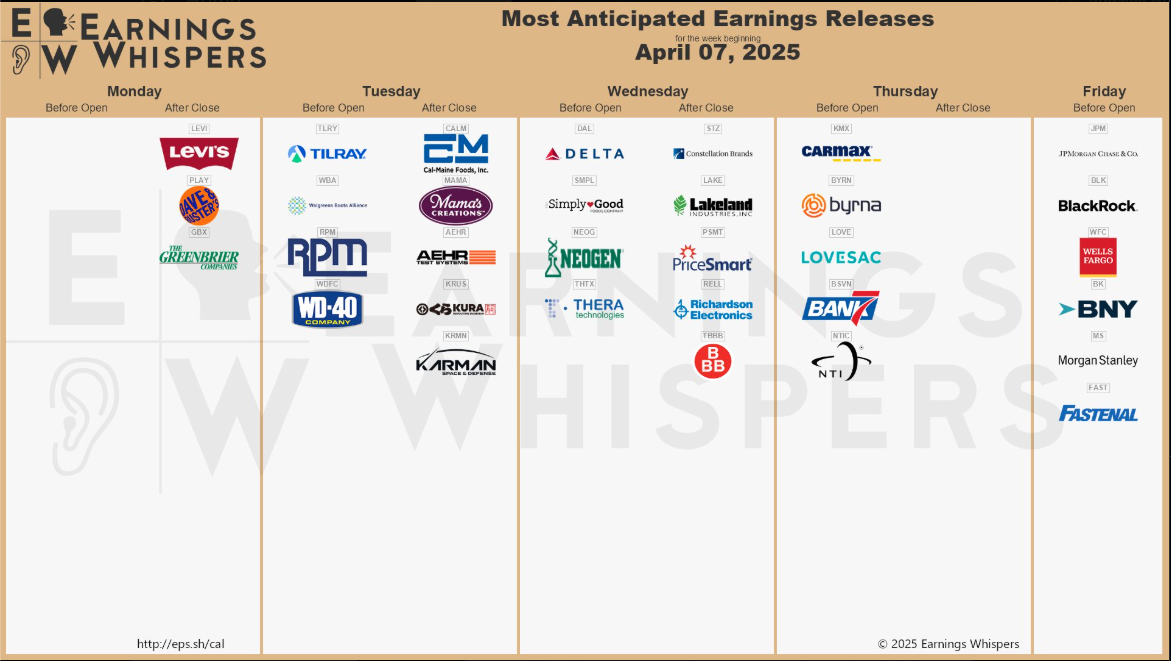

Earnings & Data Calendar: Q2 Starts Loud

Corporate Highlights

Taiwan chipmakers and Indian reroutes dominate the Section 232 narrative. The tariff “pause” was a head-fake, except for China, which remains the real target.

- Bank Earnings Roll In: GS, BoA, JPM, MS all reporting

- Tech Watch: Netflix & TSMC midweek, huge sentiment movers

- Luxury Pulse: LVMH, Hermes, L’Oréal as global consumer barometers

Macro Data to Track

- China GDP and credit impulse: Does deflation risk deepen?

- US Retail Sales and PPI: More signals for the Fed

- ECB decision: How dovish can Lagarde afford to sound?

Technical Setups & Sentiment

Gold: Exhaustion or Just a Breather?

Made fresh all-time highs, but RSI divergence suggests caution.

Silver lagging = possible retracement incoming.

Oil: Structural Breakdown Confirmed

Sub-$60 barrel for first time since 2021.

OPEC cuts not enough to halt momentum. Demand risk in full focus.

Equities: Tactical Rally or Trap?

SPX putting in higher lows, but breadth weak.

Risk-on mode may return if TSMC and Netflix impress.

Upcoming Week Preview: Day-by-Day Breakdown

This week has the hallmarks of a macro minefield. China’s growth pulse, US consumer resilience, ECB guidance, and early Q1 earnings all matter. With risk assets rattled and bonds volatile, every data point matters.

Monday, April 15

Bank earnings begin + US Treasury auctions

Goldman Sachs (GS) and M&T Bank kick off earnings season with insight into consumer credit and investment banking flows.

Treasury auctions continue to test appetite for duration after last week’s bond rout.

Traders will also eye early market sentiment after last week's wild swings in rates and risk.

Tuesday, April 16

China credit pulse + European credit stress

China’s Aggregate Financing and Loan Growth will show if Beijing’s reflation push is gaining traction.

In Europe, continued scrutiny on banks and periphery spreads ahead of Thursday’s ECB.

US Industrial Production could hint at underlying capex and manufacturing softness.

Wednesday, April 17

Triple Threat: US Retail Sales, China GDP, Netflix

US March Retail Sales is the macro print of the week. Strong data would undermine rate-cut expectations and challenge the market’s soft-landing view.

China Q1 GDP, Retail Sales, and Industrial Production are due pre-US open, setting the global tone.

After hours, Netflix (NFLX) earnings will be closely watched for subscriber growth, engagement metrics, and content cost outlook.

Thursday, April 18

ECB + TSMC + BOC = Volatility Triad

ECB Rate Decision: Market expects 25bps, but will Lagarde lean into future cuts? Euro, bunds, and EU credit will react.

TSMC Earnings: Seen as the AI supply chain proxy. Soft guidance could ripple across semis and Nasdaq.

Bank of Canada Rate Decision: No cut expected, but language could turn dovish amid weakening Canadian labor data.

Atlanta Fed GDPNow update due after key consumption and inventory revisions. Watch this closely as Q1 growth estimates are recalibrated.

Friday, April 19 — Good Friday

Western Markets Closed

- No major US data releases

- NYSE, Nasdaq, CME closed

Expect thin liquidity into the weekend. Positioning will likely be squared Thursday into the long weekend.

Actionable Takeaway: Macro Mayhem = Trader’s Playground

Traders should approach this environment with tactical discipline. There’s signal through the noise, but it requires zooming in when the rest of the market is zoomed out.

Key Alpha Reads

- Rate cut expectations rising, even if central banks deny it

- Gold may correct, but long-term momentum intact

- Bond volatility = equity fragility

- Watch Netflix & TSMC for a sentiment pivot this week