Risk-On Momentum Extends, Positioning Builds Beneath the Surface

Markets enter the week with a constructive tone, as risk assets continue to grind higher despite a volatile geopolitical backdrop. Price action reflects a market increasingly willing to look through uncertainty, with participation broadening and flows reinforcing upside momentum rather than fading it.

Geopolitics continues to shift rapidly between escalation and resolution, but the market is increasingly choosing to focus on outcomes rather than headlines. Beneath this strength, however, positioning is becoming increasingly stretched. Liquidity remains supportive, and systematic flows continue to drive price, but the move is increasingly being driven by flows rather than fresh conviction, leaving the market sensitive to shifts in narrative.

Market Overview: Broad Participation Supporting a Strong Advance

Equity markets have pushed higher with increasing consistency, supported by improved sentiment, stronger earnings signals, and easing geopolitical concerns. The structure of the rally suggests a market that is not purely driven by narrow leadership, but instead supported by broader participation across sectors and market caps.

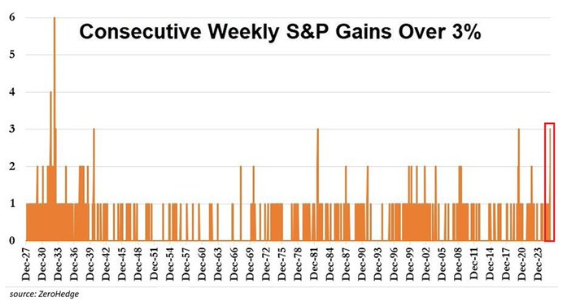

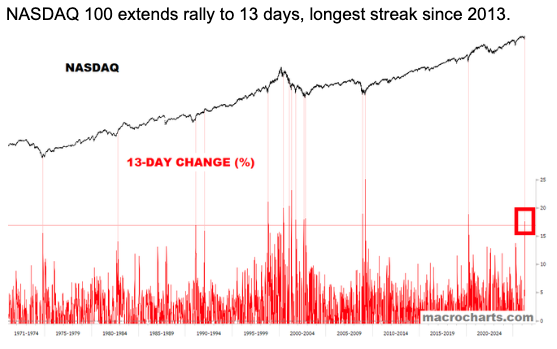

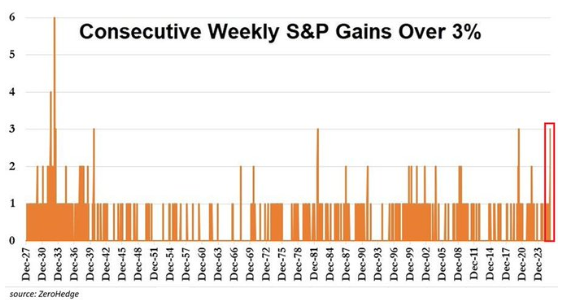

Momentum has been particularly evident in growth-heavy indices, with extended winning streaks reflecting persistent buying pressure. At the same time, the consistency of gains across multiple indices highlights a market where flows are actively reinforcing price action rather than fading it.

This type of environment typically reflects strong systematic and liquidity-driven participation. The steady climb higher, rather than sharp impulsive moves, suggests that flows remain in control, with systematic flows continuing to dominate price action

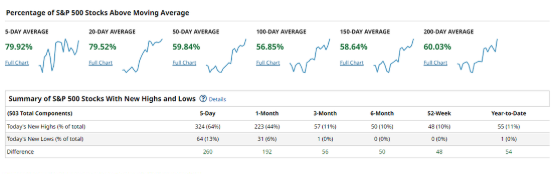

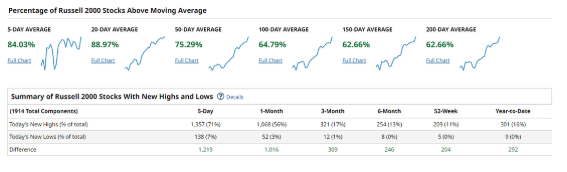

Breadth metrics confirm this dynamic, with a significant proportion of stocks trading above key moving averages and new highs consistently outpacing new lows. This reinforces the idea that the advance is not fragile in structure, but supported by widespread participation.

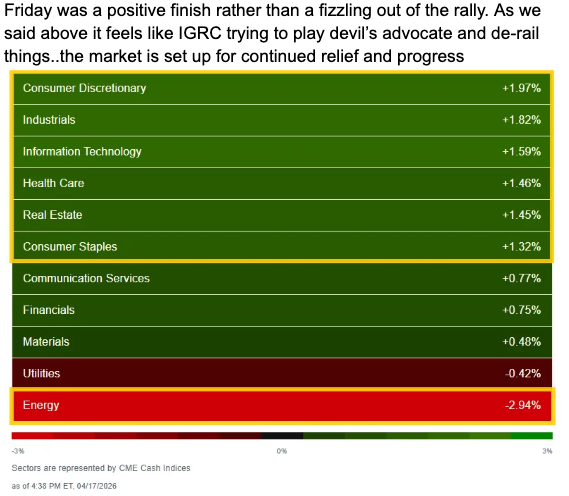

Sector performance further supports this view, with gains extending beyond mega-cap technology into broader cyclical and mid-cap exposures, suggesting participation is broadening beyond mega-cap leadership.

Macro & Policy Watch: Growth Resilience and Liquidity Support

The macro backdrop continues to be defined by the interaction between geopolitics, growth resilience, and liquidity conditions. While geopolitical developments remain active, the market has largely priced out the risk of a sustained escalation, allowing focus to shift back toward underlying economic trends.

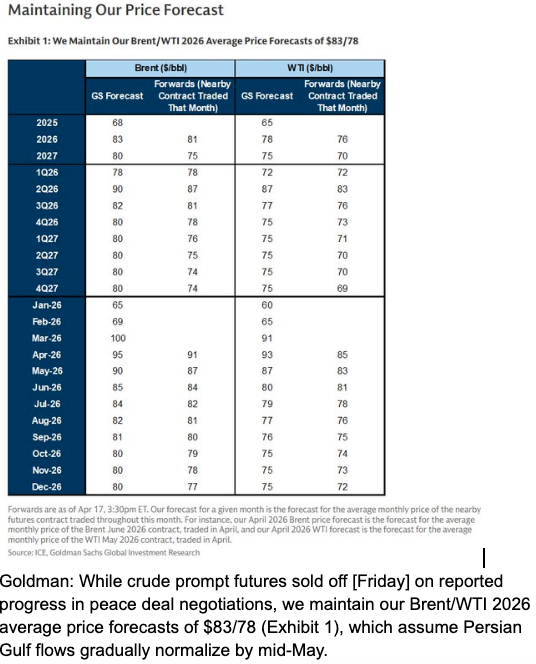

Energy markets have begun to reflect a more balanced outlook, with the reopening of flows removing one of the key overhangs on risk assets that had previously tightened financial conditions. This shift has supported broader risk sentiment and eased concerns around sustained supply shocks.

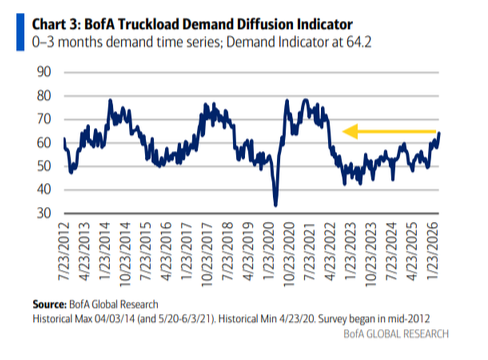

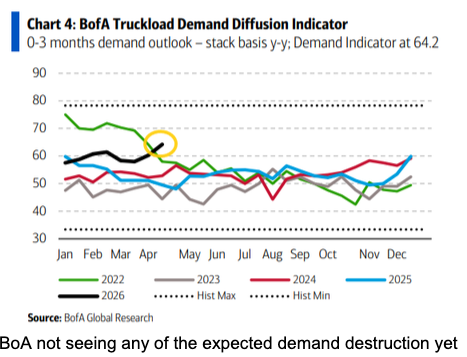

At the same time, growth indicators have shown resilience, with demand-related data holding up better than expected. This has contributed to a reassessment of downside risks and supported the continuation of the rally.

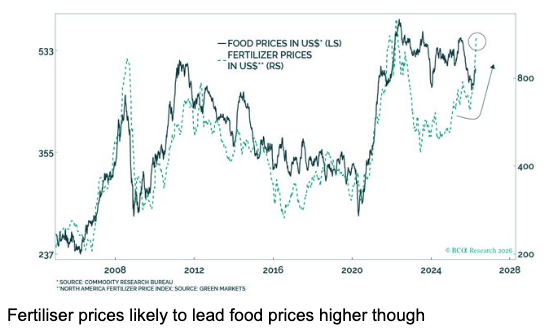

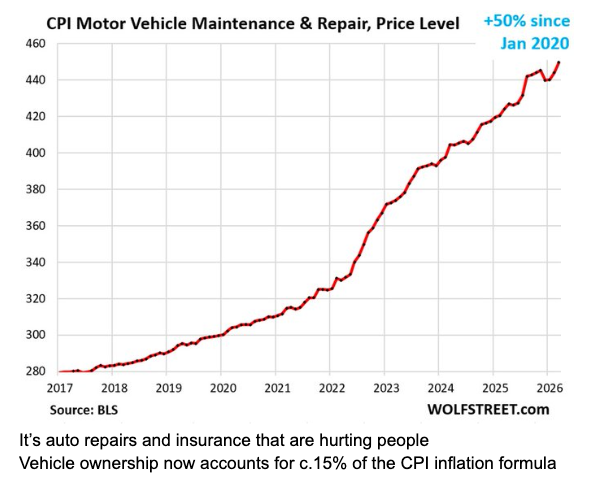

Inflation dynamics remain uneven, with certain components continuing to show persistence despite broader expectations of moderation.

This reinforces the risk that rates may struggle to come down as quickly as expected. Liquidity conditions continue to act as a key support, with strong demand across fixed income markets and sustained participation in credit.

The combination of resilient growth and supportive liquidity continues to underpin risk assets, even as policy expectations remain somewhat uncertain.

As has been the case throughout, growth continues to trump everything

Technical & Sentiment Breakdown: Supportive, but Increasingly Fragile

The broader technical structure remains supportive, with price trends continuing to move higher across major indices. However, the pace and consistency of the advance are beginning to push sentiment toward more extended levels.

Breadth remains strong, reinforcing the durability of the move, but also highlighting how far participation has expanded over a relatively short period. This type of broad strength often supports continuation, but can also reduce the margin for error.

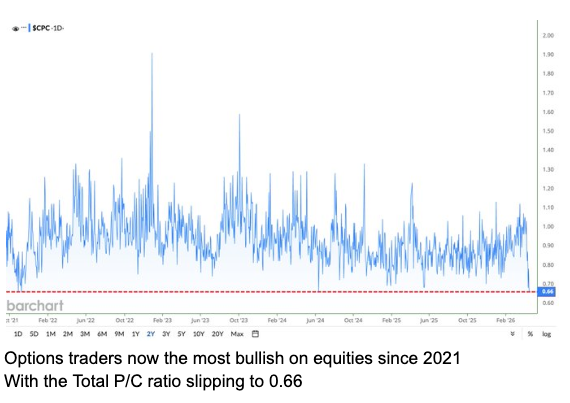

Positioning indicators suggest a shift toward increasingly bullish sentiment, with options activity reflecting a growing consensus around continued upside. This type of positioning can support momentum in the near term, but also introduces vulnerability to any change in narrative.

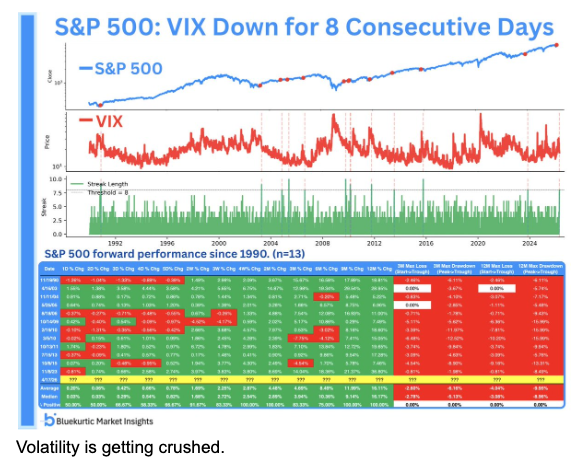

Volatility has compressed significantly, reflecting reduced demand for hedging and a market that is increasingly comfortable with current conditions. While this supports trend continuation, it also reflects a degree of complacency that can amplify reactions to unexpected developments.

Flow data further reinforces the strength of the current environment, with consistent inflows supporting the “buy-the-dip” dynamic that has defined recent price action.

Last Week’s Recap: Momentum Builds as Risk Perception Eases

The past week reflected a continuation of the constructive trend, with improving sentiment and supportive flows driving consistent gains across risk assets. The pricing out of geopolitical risk allowed markets to focus on underlying strength, reinforcing the upward move.

Key Highlights:

Macro:

Growth-related indicators continued to show resilience, with demand holding up and concerns around immediate slowdown easing. At the same time, inflation components remained uneven, highlighting ongoing pressure in specific areas.

China:

Positioning and broader flows reflected continued adjustments in global asset allocation, with ongoing shifts in holdings occurring in a gradual and controlled manner.

Earnings:

Early signals from earnings season indicated a shift toward more positive outcomes, with markets responding to improving expectations and reduced downside surprises.

Commodities:

Commodity dynamics reflected a more balanced outlook, with energy normalisation and continued structural support in other areas contributing to a mixed but stabilising environment.

Crypto:

Speculative positioning has remained concentrated in high-beta equity exposure, particularly within Nasdaq-linked flows

Oil:

Oil markets moved away from extreme pricing scenarios, with expectations shifting toward normalisation as supply concerns eased.

The Week Ahead: Key Data and Market-Moving Signals

The week is driven by a dense macro calendar alongside ongoing geopolitical developments, with a focus on central bank direction, inflation signals, global PMIs, and a heavy earnings slate, particularly across financials and technology.

Monday, April 20

- UK: House Price Index (Rightmove)

- China: Loan Prime Rate decisions (PBoC)

- Germany: PPI (MoM, YoY)

- Canada: CPI (Core, Median, Trimmed)

- EU: Construction Output

- US: 3-month & 6-month Bill Auctions

- ECB: President Lagarde speaks

Tuesday, April 21

- UK: Employment data, wages, unemployment rate

- EU / Germany: ZEW Economic Sentiment & Conditions

- US: Retail Sales (Core, Control Group, YoY)

- US: Business Inventories & Housing Data

- US: API Crude Oil Inventories

- US: Warsh Fed Chair Confirmation Hearing

- Fed / ECB speakers

Wednesday, April 22

- UK: CPI, Core CPI, PPI, RPI

- EU: Government Debt & Budget metrics

- US: Mortgage Applications & Rates

- US: Crude Oil Inventories

- US: 20-Year Bond Auction

- Earnings: Tesla, IBM

Thursday, April 23

- Global: Manufacturing & Services PMIs (US, EU, UK, Japan, India)

- US: Initial & Continuing Jobless Claims

- US: Chicago Fed Activity Index

- US: Fed Balance Sheet & Reserve Data

- US: KC Fed Manufacturing Index

- Earnings: Intel, SAP

Friday, April 24

- Japan: National CPI

- UK: Retail Sales

- Germany: Ifo Business Climate & Expectations

- Canada: Retail Sales

- US: Michigan Consumer Sentiment & Inflation Expectations

Alpha Takeaway: Momentum Supported, but Positioning Extended

The market continues to be supported by a combination of resilient growth, easing macro concerns, and strong liquidity conditions, allowing risk assets to extend their advance.

Equities:

Structure remains constructive with broad participation and consistent inflows supporting price action, though the pace of gains suggests positioning is becoming more extended.

Gold & Silver:

Precious metals continue to reflect broader liquidity dynamics, with price behaviour acting more as a liquidity indicator than a direct geopolitical hedge.

Crypto:

Momentum-driven participation remains strong, reflecting broader risk appetite and continued flow-based support.

Macro:

The interaction between growth resilience, inflation persistence, and policy expectations remains central, with liquidity continuing to act as the primary support for markets.

The environment remains supportive, but increasingly dependent on the continuation of current conditions. A shift in narrative or positioning could lead to more reactive price behaviour despite the underlying strength.