Flow-Driven Upside Continues While Structural Fragility Builds Beneath Leadership

Markets continue to push higher, but the character of the move reflects a market that was previously over-hedged and is now chasing upside. Participants remain under-owned, forcing a grab back into upside optionality as the rally extends. Strength is being sustained not by improving certainty, but by positioning being pulled into the move.

Beneath the surface, the structure is becoming more uneven. Liquidity remains supportive, and earnings are delivering, but the rally is increasingly concentrated and sensitive to continuation. With fundamentals and macro on the verge of confirming the bullish narrative, the move is being reinforced by positioning rather than fresh conviction.

Market Overview: Concentrated Leadership Driving a Flow-Led Advance

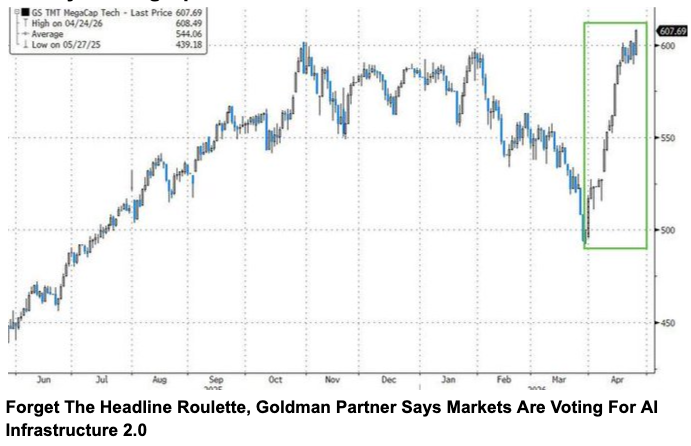

Equity markets continue to grind higher, but the structure of the rally reflects concentrated leadership rather than broad participation. The move is being driven by targeted inflows into specific segments, particularly those linked to structural growth themes, while broader participation remains less consistent.

This type of price action reflects a market that was previously under-positioned and is now being forced higher through short covering, gamma dynamics, and systematic flows. The rally is not being led by incremental buyers, but by positioning adjustment, catching up with price.

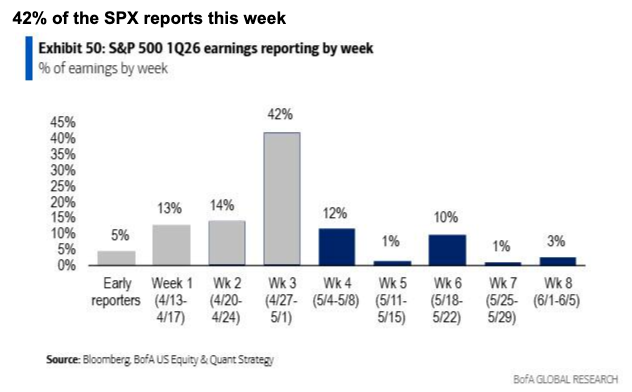

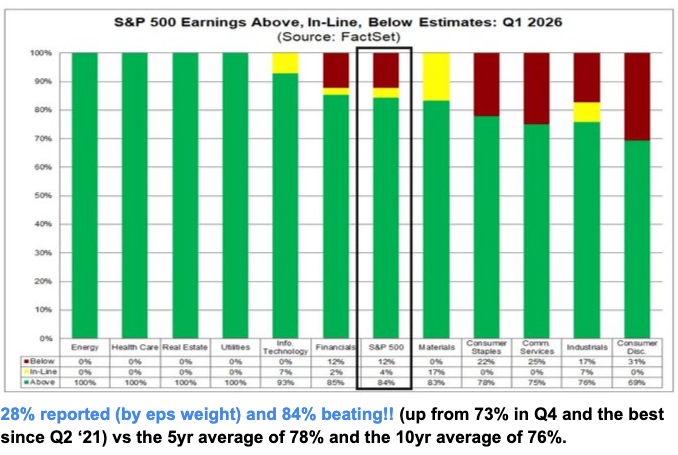

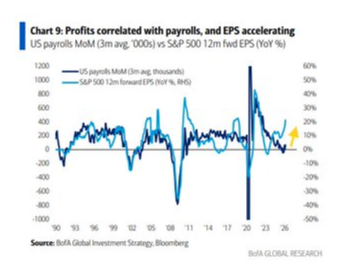

Earnings remain a key pillar supporting the move, with a significant portion of the index reporting within a compressed window. This creates a high-sensitivity environment where continued delivery reinforces flows, while any disappointment could disrupt the current structure.

So far, earnings outcomes have remained supportive, with a high proportion of companies exceeding expectations and margins holding firm. This has allowed markets to maintain their upward trajectory despite elevated expectations.

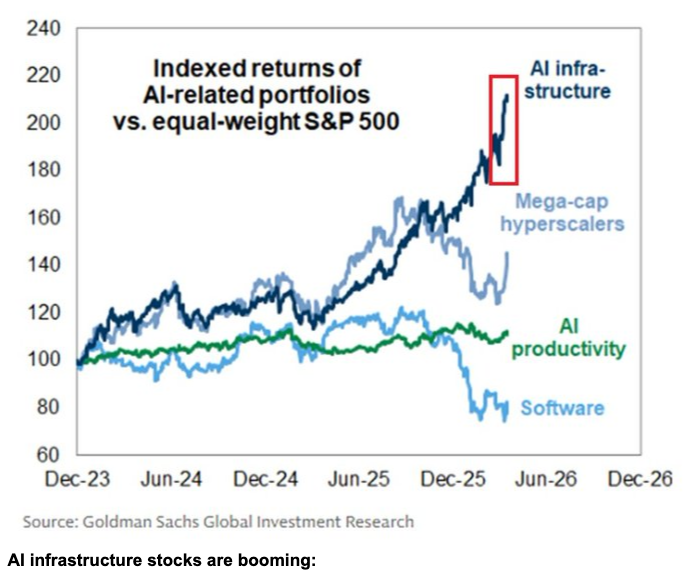

At the same time, leadership continues to be driven by AI-linked infrastructure and productivity themes, reinforcing the idea that capital is being allocated selectively rather than broadly.

Macro & Policy Watch: Stability Holds, Forward Pressures Building

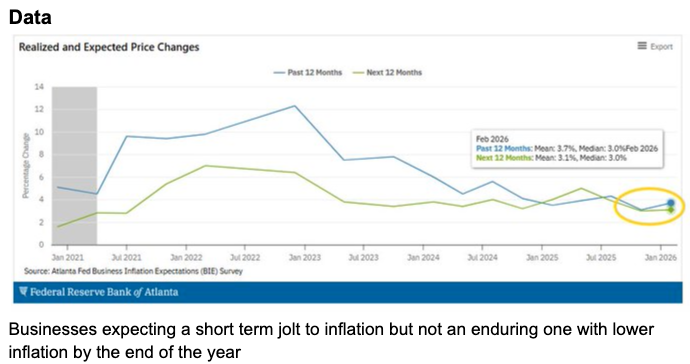

The macro backdrop remains supportive in the near term, with expectations that inflation pressures may not persist at current levels. This has helped anchor policy expectations and allowed markets to maintain a constructive tone.

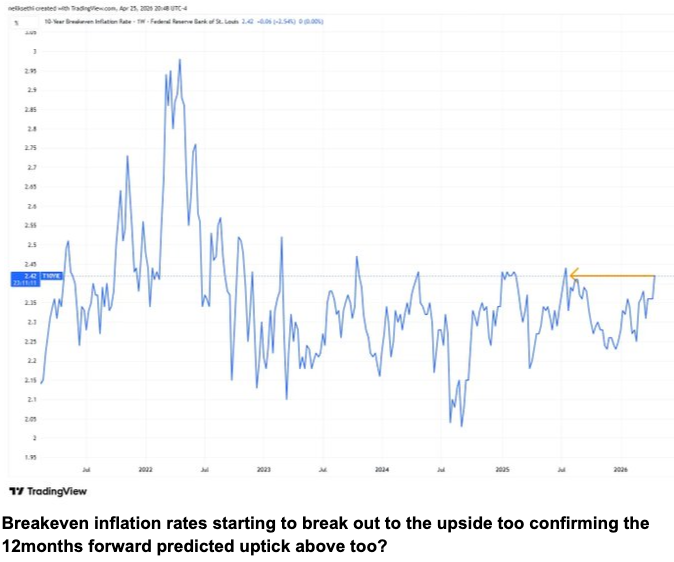

However, forward-looking indicators suggest that inflation expectations are beginning to shift higher at the margin. This introduces a potential divergence between current stability and future pricing, particularly if expectations begin to translate into realised data.

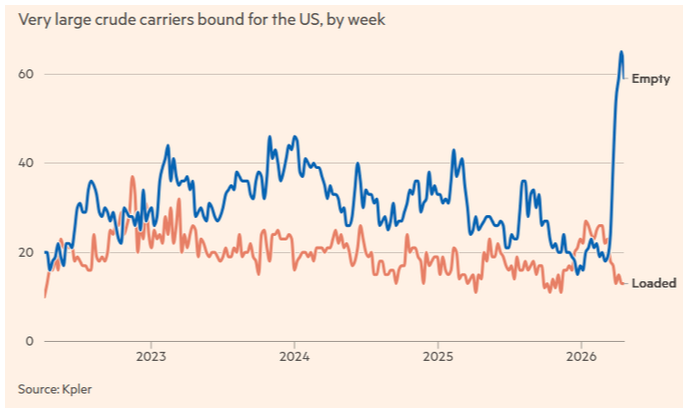

Geopolitical developments continue to revolve around energy supply dynamics and negotiations, but markets appear to be pricing outcomes over headlines. The focus remains on the timing of normalisation rather than escalation, suggesting that current pricing reflects a forward-looking adjustment rather than immediate disruption.

At the same time, broader conditions suggest that policy may not need to tighten further in the near term, with expectations gradually shifting toward a more accommodative stance later in the year.

Technical & Sentiment Breakdown: Supportive, but Increasingly Fragile

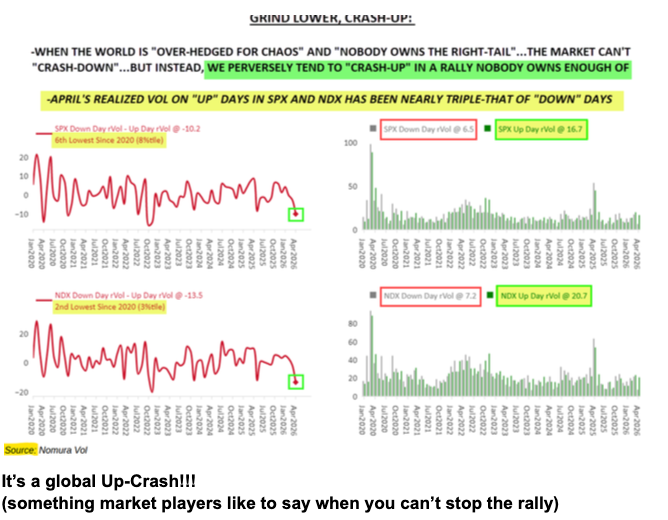

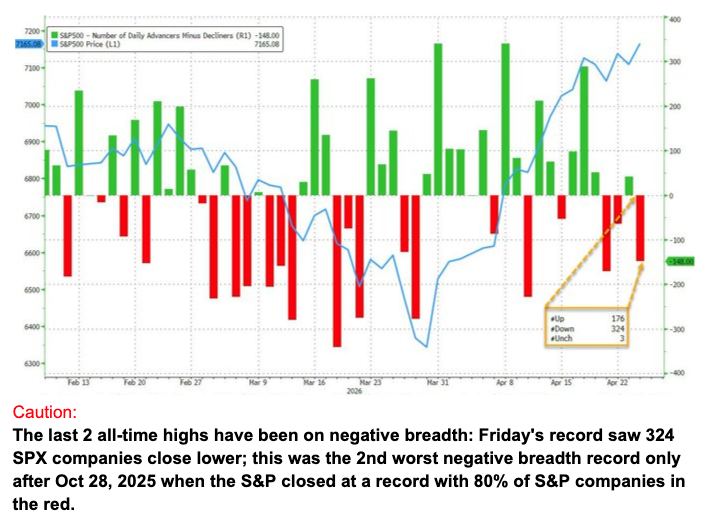

The broader trend remains intact, with indices continuing to push higher. However, internal signals suggest that the quality of the move is weakening, even as the price remains strong.

Breadth dynamics highlight this divergence, with strength increasingly concentrated in a smaller group of stocks. While this does not immediately invalidate the trend, it reduces the margin for error and increases sensitivity to changes in leadership.

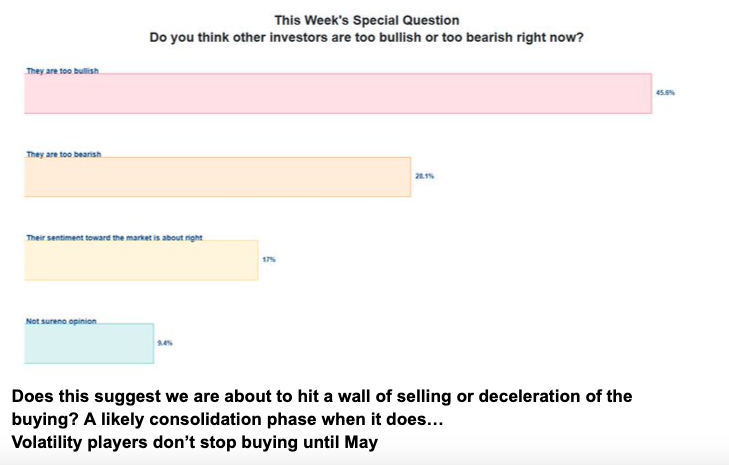

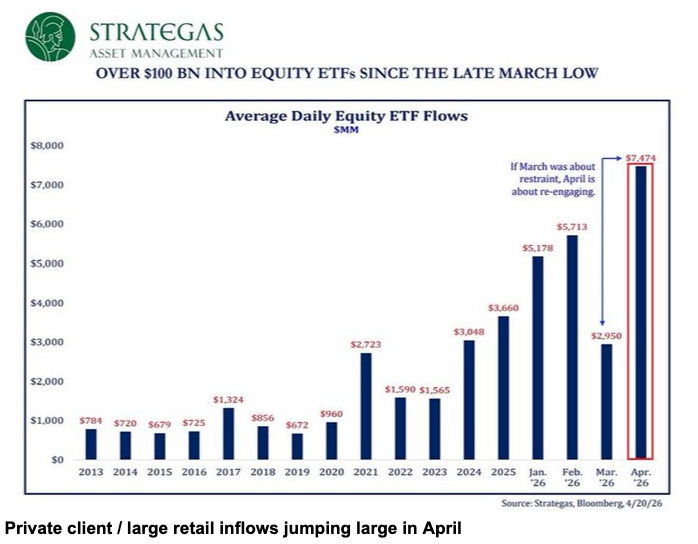

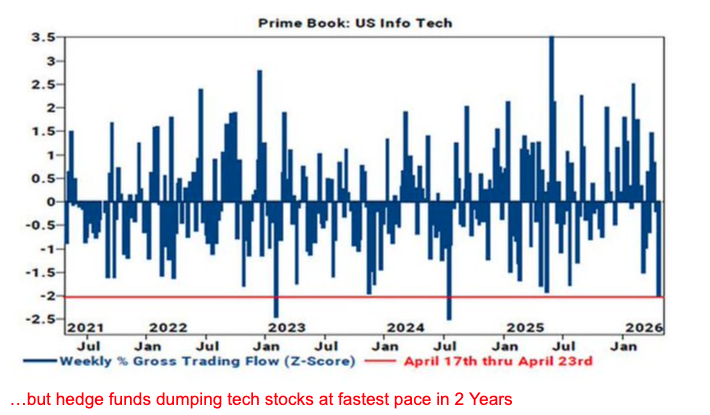

Positioning data reinforces the importance of flows in sustaining the move. Retail participation has increased, while hedge funds have begun to reduce exposure in key areas, particularly within technology.

This dynamic reflects a market where different participants are operating on different timeframes—with longer-term capital supporting structural themes, while shorter-term positioning adjusts around them.

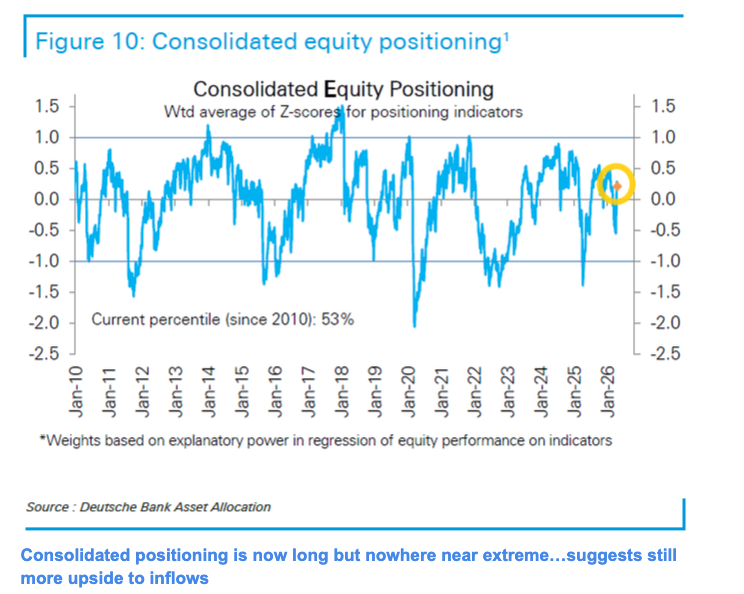

Despite this, overall positioning is not yet extreme, suggesting that flows still have the capacity to extend before reaching exhaustion.

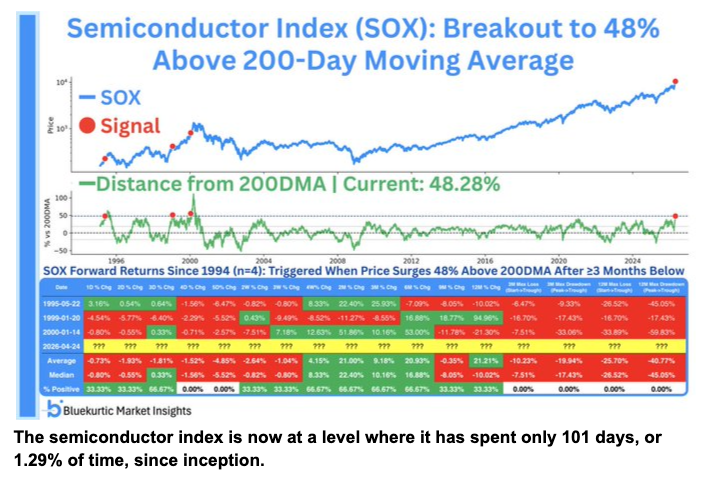

At the same time, certain segments appear stretched on a short-term basis, highlighting the potential for periods of consolidation within the broader trend.

Last Week’s Recap: Flow Acceleration Meets Earnings Support

The past week reflected a continuation of the upward trend, with flows and earnings working together to support price action. Markets continued to advance despite ongoing geopolitical developments, reinforcing the dominance of positioning and liquidity.

Key Highlights:

Macro:

Economic conditions continued to stabilise, with improving activity supporting expectations that policy may not need to tighten further in the near term.

China:

Geopolitical positioning remained fluid, with ongoing developments influencing broader sentiment without triggering immediate repricing across risk assets.

Earnings:

Earnings outcomes remained strong, with a high proportion of companies exceeding expectations and margins holding at elevated levels, reinforcing the current market structure.

Commodities:

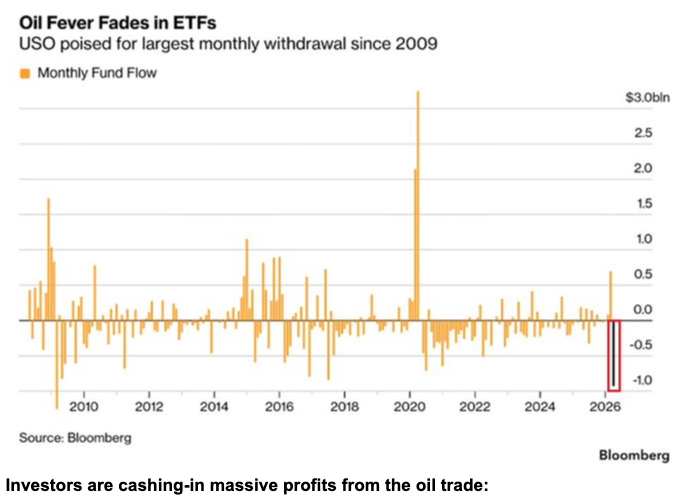

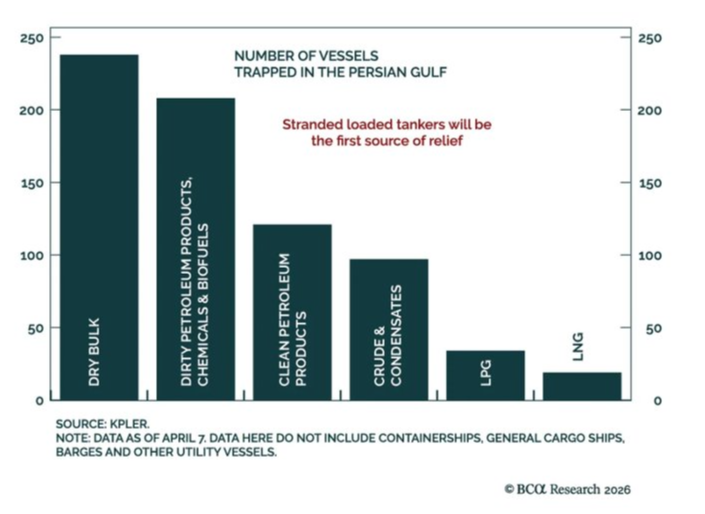

Energy markets continued to reflect supply dynamics and geopolitical developments, with price action influenced by both disruption and expectations of gradual normalisation.

Oil:

Supply constraints and logistical timelines suggest that normalisation will take time, with markets pricing a gradual adjustment rather than an immediate resolution.

The Week Ahead: Key Data and Market-Moving Signals

The week ahead is defined by a heavy calendar of central bank decisions alongside a concentrated week of MAG7 earnings. The combination of policy signals and earnings outcomes will be key in determining whether the current upside momentum is sustained or begins to fade.

Monday, April 27

- China: Industrial Profits (YTD)

- Japan: Leading Index, Coincident Indicators

- Germany: GfK Consumer Climate

- UK: CBI Distributive Trades Survey

- US: Dallas Fed Manufacturing Index

- US: 3M, 6M Bill Auctions | 2Y, 5Y Note Auctions

- EU: ECB Schnabel speaks

Tuesday, April 28

- Japan: BoJ Policy Statement & Rate Decision

- Japan: BoJ Outlook Report & Press Conference

- EU: ECB Bank Lending Survey

- Spain: Unemployment Rate, Retail Sales

- US: Consumer Confidence, House Price Index

- US: Richmond Manufacturing & Services Indices

- US: M2 Money Supply

- US: API Crude Oil Stocks

- UK: BoE Bailey speaks

- EU: ECB Lagarde speaks

Wednesday, April 29

- Australia: CPI (QoQ, YoY)

- Eurozone: M3 Money Supply, Loan Growth

- Germany: Regional CPI prints

- Italy: Business & Consumer Confidence

- US: Durable Goods Orders, Housing Data, Trade Balance

- Canada: BoC Rate Decision & Monetary Policy Report

- US: FOMC Rate Decision & Press Conference

- Brazil: Interest Rate Decision

- After Hours: Alphabet, Amazon, Meta, MicroSoft

Thursday, April 30

- China: Manufacturing & Non-Manufacturing PMI

- Japan: Industrial Production, Retail Sales

- Eurozone: CPI, GDP, Unemployment

- Germany, France, Italy, Spain: GDP & Inflation Data

- UK: BoE Rate Decision & MPC Vote

- Eurozone: ECB Rate Decision & Press Conference

- US: GDP (Q1), Core PCE, Jobless Claims

- US: Personal Income & Spending

- After hours: Apple

Friday, May 1

- Japan: Tokyo CPI

- UK: Manufacturing PMI, Mortgage Data

- US: ISM Manufacturing PMI & Prices

- US: Baker Hughes Rig Count

- Global: CFTC Positioning Data

Alpha Takeaway: Trend Intact, Sensitivity Increasing

The market remains supported by flows, earnings, and a stable macro backdrop, but the internal structure suggests increasing sensitivity to any shift in leadership or expectations.

Equities:

The trend remains constructive, supported by earnings and positioning, though increasing concentration raises the importance of continued leadership strength.

Gold & Silver:

Precious metals continue to reflect broader liquidity and inflation expectations, with price behaviour aligned more with macro dynamics than immediate geopolitical developments.

Risk Assets:

Price action remains closely tied to overall risk sentiment, reinforcing its role as a liquidity-driven asset class.

Macro:

Conditions remain supportive in the near term, but forward indicators suggest potential divergence that markets may need to reconcile.

The current environment continues to reward participation, with positioning driving the move rather than fresh conviction. As long as upside chasing persists, the trend can extend, but with the rally stretched and a pullback overdue, risk is beginning to build.

‘