Grinding Through Uncertainty, Positioning Drives the Tape, Macro Risks Still Linger

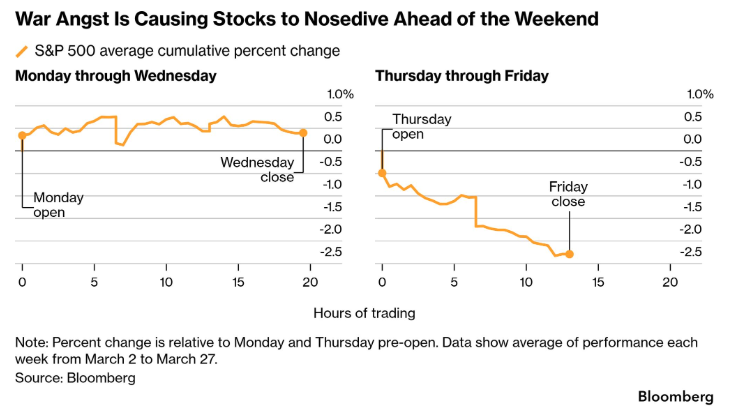

Markets enter the week with a more stable tone after the heavy liquidation phase seen through March, but the shift reflects stabilisation following heavy liquidation rather than a clear directional change. What initially looked like a recovery has instead evolved into a positioning-driven bounce, where flows are stabilising but conviction remains limited. The move higher has lacked follow-through, suggesting that participants are still cautious rather than re-engaging aggressively with risk.

Beneath the surface, the adjustment to a supply-driven macro shock continues to shape behaviour. Liquidity conditions remain uneven, with capital concentrating in more liquid areas while broader participation lags. The result is a market that feels reactive and sensitive to headlines, where stability exists but is not yet supported by a strong underlying foundation.

Market Overview: Stabilisation Driven by Positioning, Not Broad Participation

Equity markets have shown an ability to rebound from oversold conditions, but the nature of the move suggests a positioning-driven recovery rather than a structural shift. The price action into the end of last week reflected a familiar pattern — early weakness followed by a squeeze higher as shorts were forced to adjust. This type of behaviour is typically seen when positioning becomes stretched, where flows rather than fundamentals drive short-term direction.

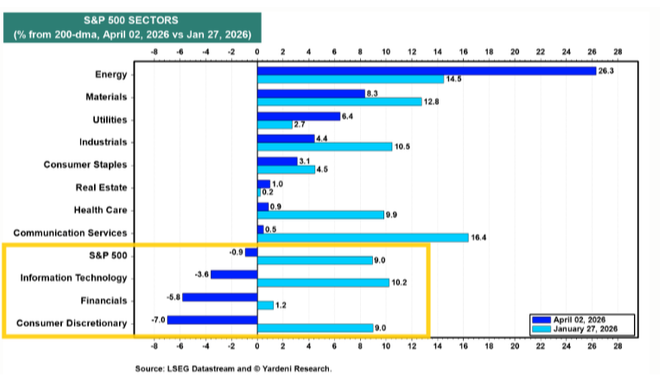

The underlying structure, however, remains incomplete. Participation continues to be led by large-cap and liquidity-heavy names, while broader market breadth lags. A significant portion of stocks are still trading below key moving averages, reinforcing the idea that the recovery is narrow and lacks depth. This divergence suggests that the market is being supported selectively rather than through broad-based demand.

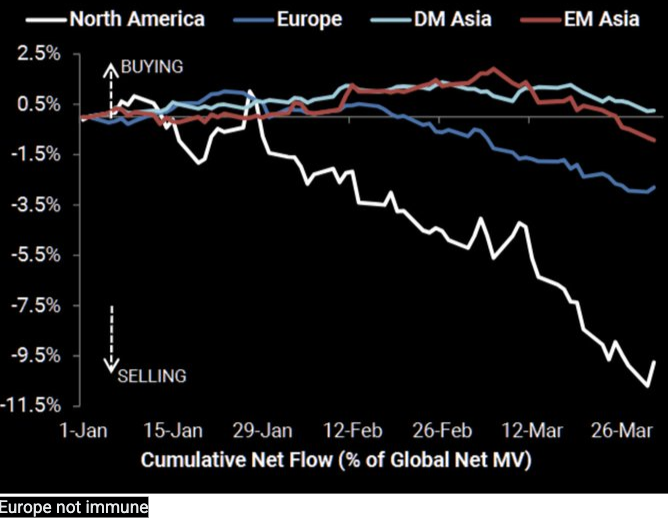

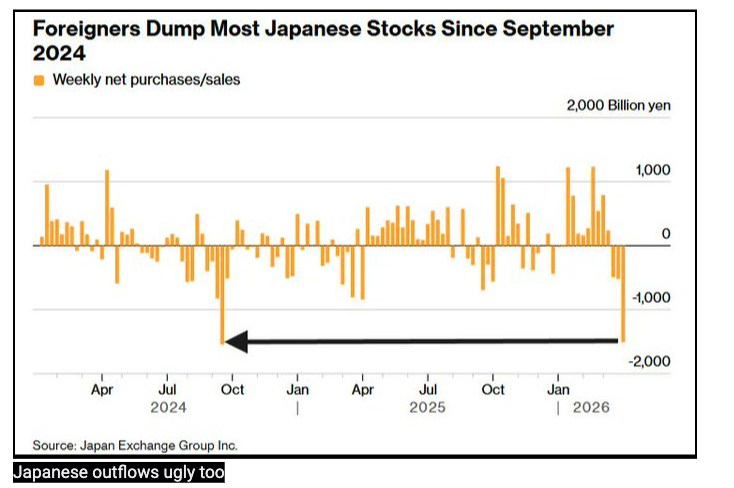

Flows further reinforce this picture. Global equity outflows, particularly from Europe and Japan, have been significant, contributing to their relative underperformance and highlighting a lack of sustained conviction outside the most liquid US exposures. This pattern reflects a market where capital is reallocating defensively rather than expanding risk, limiting the strength and durability of any upside move.

At the core, markets are being driven by positioning resets and flow adjustments, rather than a clear improvement in macro or earnings visibility.

Macro & Policy Watch: Energy Shock, Rates Pressure, and Policy Constraints

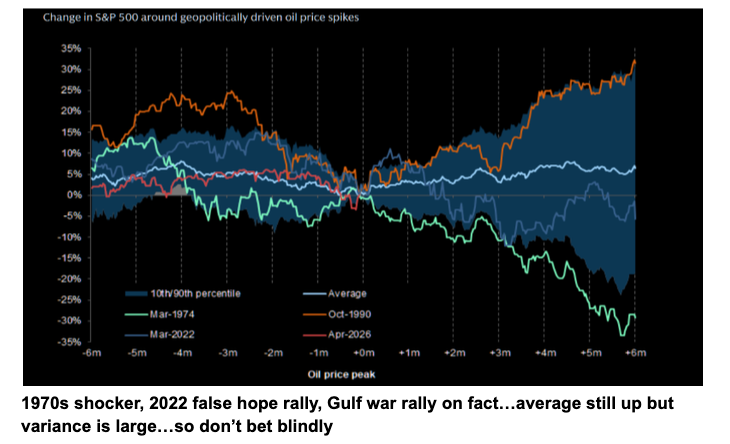

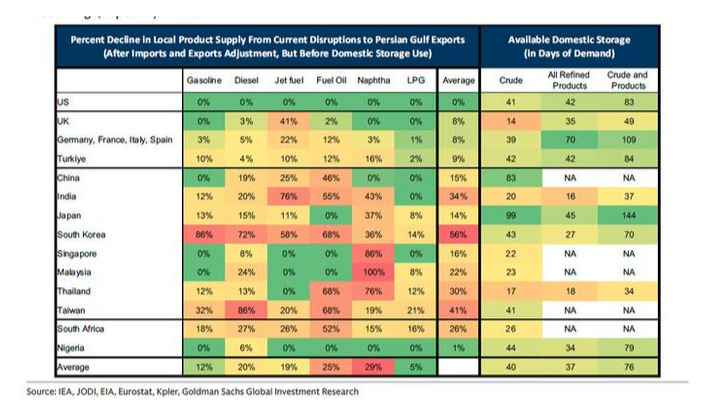

The macro narrative continues to be dominated by energy, with oil remaining the central driver across markets. The sharp move higher reflects ongoing supply constraints and disruption, feeding directly into inflation pressures and tightening financial conditions. This is no longer a contained commodity move, but a broader constraint impacting consumption, production, and policy flexibility.

The persistence of elevated energy prices is beginning to show through in second-order effects, particularly as higher costs filter into consumption and industrial activity. This creates a challenging backdrop where demand faces pressure while inflation remains elevated, reinforcing concerns around a stagflationary environment. The interaction between these forces continues to shape market expectations.

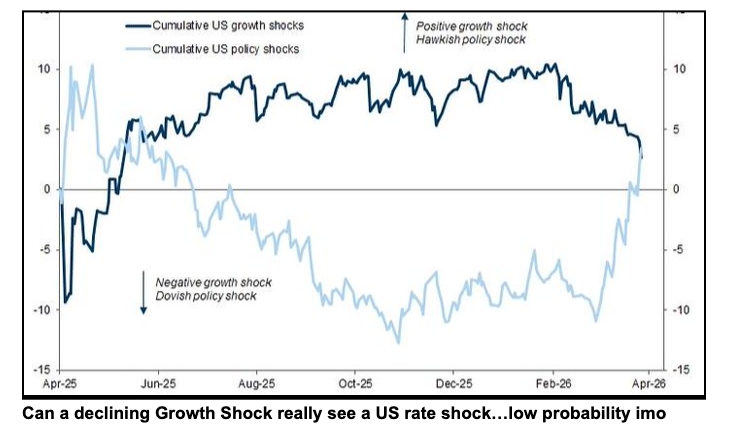

At the same time, central banks are navigating a difficult balance. Policymakers have signalled caution, particularly around tightening into what is increasingly viewed as a supply-driven shock rather than demand-led inflation. This limits the ability of policy to respond aggressively without risking further pressure on growth.

The result is a policy environment that remains reactive, leaving markets more sensitive to incoming data and external developments rather than guided by clear central bank direction.

Technical & Sentiment Breakdown: Supportive, but Increasingly Fragile

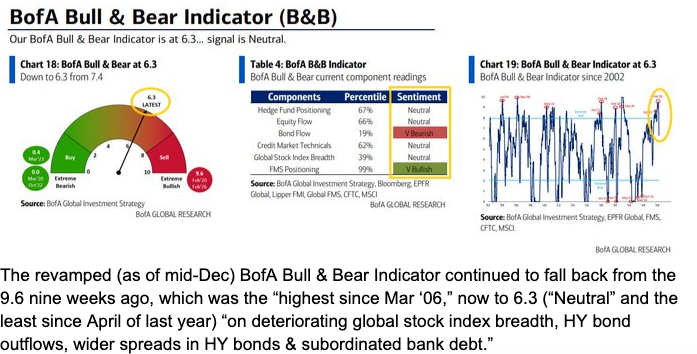

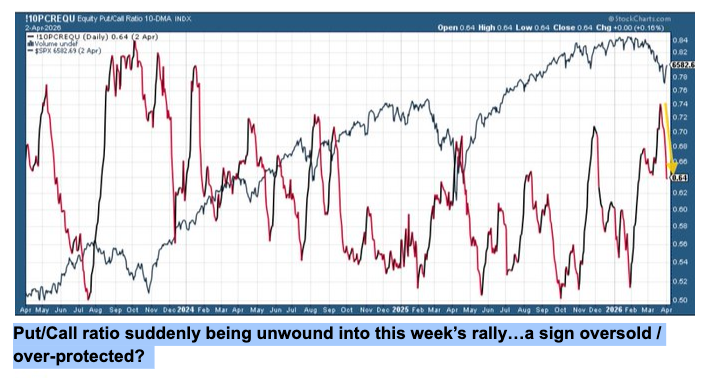

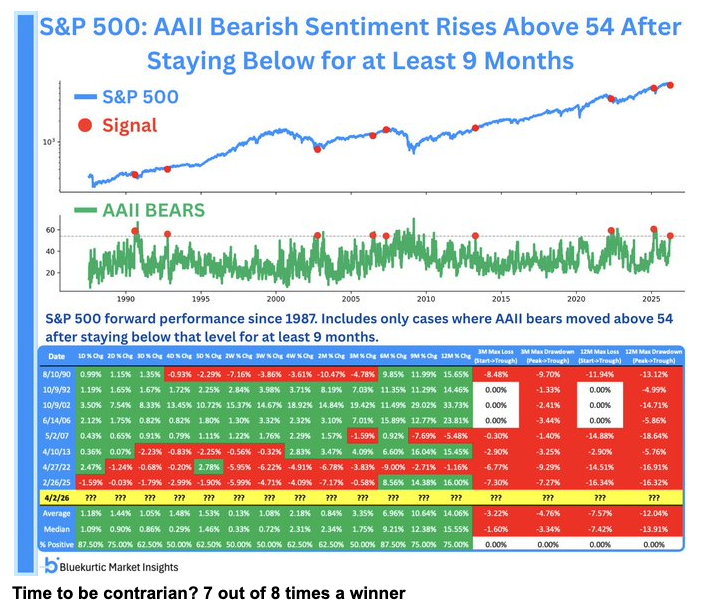

While the broader structure shows signs of stabilisation, sentiment and positioning suggest conditions remain stretched. The recent move higher has been driven more by positioning dynamics than by a shift in fundamentals, creating a setup where stability may not be durable. This introduces the potential for sharp moves in either direction, depending on how narratives evolve.

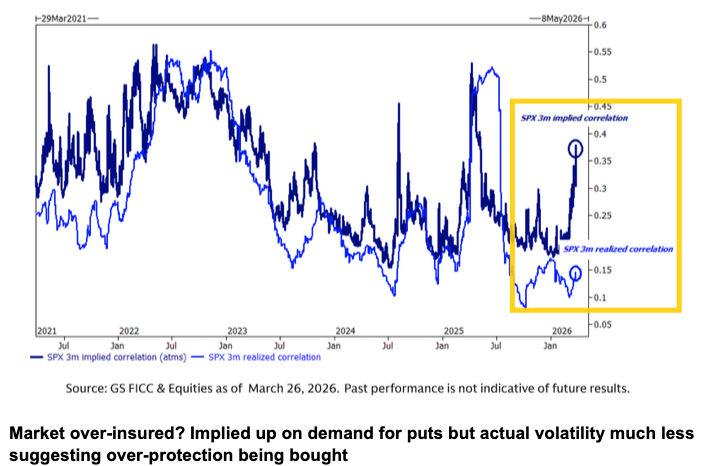

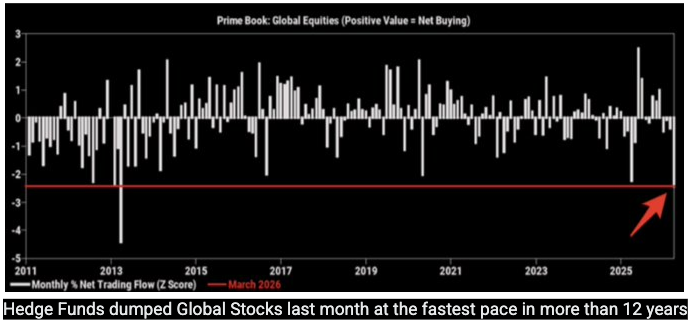

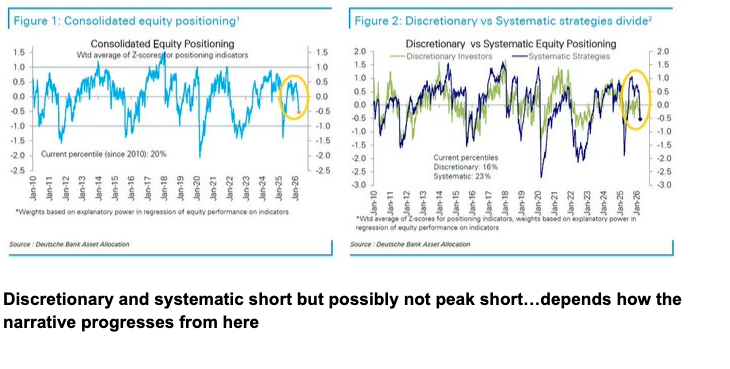

Positioning data highlights a market that is heavily hedged, with strong demand for downside protection. At the same time, realised volatility has not matched the level of protection being bought, suggesting an imbalance that can influence short-term price action. This type of setup often leads to reactive moves as hedges are adjusted.

Short positioning has also increased across both discretionary and systematic strategies, indicating a market that is already leaning defensive. This reflects a market already positioned defensively without new catalysts, while also increasing the potential for short-covering moves if sentiment shifts.

Sentiment has turned cautious but is not yet at extremes, leaving the market in a middle ground where downside risks remain, but positioning can still drive counter-trend strength. The combination of weak breadth and defensive positioning creates a fragile equilibrium rather than a stable trend.

Last Week’s Recap: Conflicting Signals Beneath Stable Headlines

The past week reflected a stabilisation in price action alongside continued macro uncertainty, with headline data often masking softer underlying trends. While markets attempted to find balance, underlying indicators suggested that the adjustment process is still ongoing rather than complete.

Key Highlights:

Macro:

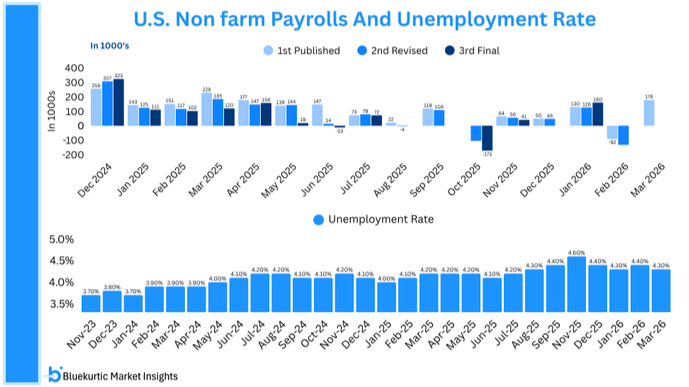

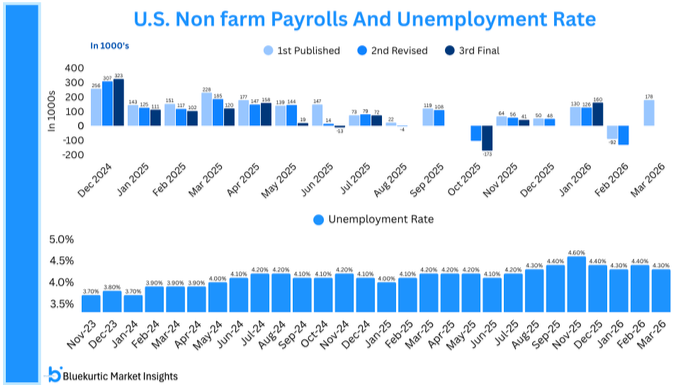

The latest jobs data delivered a strong headline print, but underlying components pointed to a more mixed picture. Differences between surveys and a decline in labour force participation suggest softer conditions beneath the surface, reinforcing the need to look beyond top-line strength.

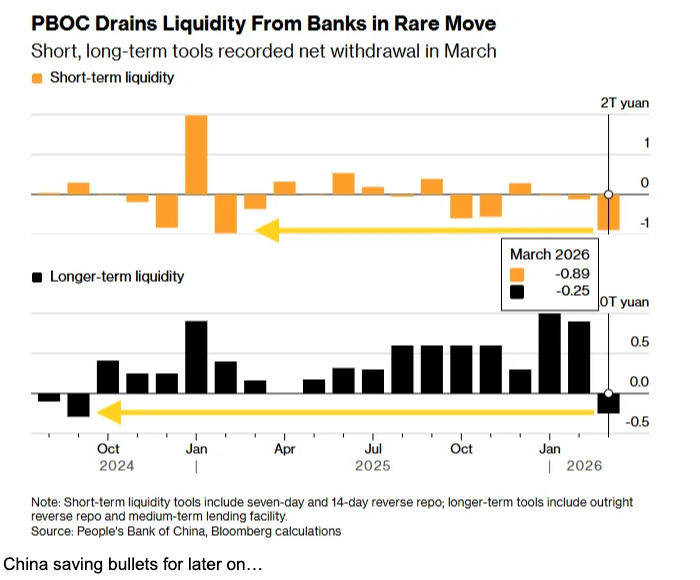

China:

Liquidity dynamics indicate a cautious stance, with flexibility being preserved rather than aggressively deployed. This reflects uncertainty around growth conditions and a preference to maintain optionality in the current environment.

Earnings:

Corporate expectations remain relatively stable, but valuation compression suggests markets are adjusting to macro risks rather than reacting to a deterioration in fundamentals.

Commodities:

Energy and refined product markets continue to reflect tight supply conditions, with disruptions forcing rerouting and increasing pricing pressure across key inputs. These dynamics highlight the ongoing influence of supply-side constraints.

Crypto:

Digital assets have shown relative resilience, with flows suggesting shifting liquidity dynamics rather than a clear macro-driven trend. The divergence reflects changing positioning rather than strong directional conviction.

Oil:

Oil remains central to the macro narrative, with supply constraints and geopolitical developments continuing to drive price action and influence broader market expectations.

The Week Ahead: Key Data and Market-Moving Signals

The week ahead is dense with macro catalysts, even without the geopolitical backdrop. Markets will be balancing growth, inflation, and policy signals alongside energy dynamics and bond market movements. With positioning already stretched and sensitivity to headlines elevated, incoming data is likely to have an amplified impact on price action.

Monday, April 6

- US: ISM Non-Manufacturing PMI, Prices, Employment

- US: CB Employment Trends Index

- IN: HSBC Manufacturing & Services PMI

- Global: Holiday-thinned liquidity across major regions (Easter, Ching Ming Festival)

- EU: Spain Unemployment Change

Tuesday, April 7

- US: Durable Goods Orders

- US: GDPNow Update

- US: Consumer Credit

- US: IBD/TIPP Economic Optimism

- US: NY Fed 1-Year Inflation Expectations

- US: EIA Short-Term Energy Outlook

- Global: Final Services & Composite PMIs (EU, UK, Japan, Australia)

- JP: Household Spending, Wage Data

- US: 3-Year Note Auction

Wednesday, April 8

- US: FOMC Meeting Minutes

- IN: Interest Rate Decision

- NZ: Interest Rate Decision + Press Conference

- US: Crude Oil Inventories

- US: MBA Mortgage Applications, Mortgage Rates

- EU: Retail Sales, PPI Data

- EU: Construction PMIs

- US: 10-Year Note Auction

Thursday, April 9

- US: PCE Inflation Data (Core + Headline)

- US: Q4 GDP (Final), GDP Price Index

- US: Jobless Claims (Initial & Continuing)

- US: Personal Spending, Income, Real Consumption

- US: Corporate Profits

- US: Wholesale Inventories & Trade Sales

- US: Fed Balance Sheet, Reserve Balances

- EU: German Industrial Production, Trade Balance

- JP: Household Confidence

- US: 30-Year Bond Auction

Friday, April 10

- US: CPI Inflation Data (Core + Headline)

- US: Michigan Consumer Sentiment, Current Conditions

- US: Michigan Inflation Expectations (1Y & 5Y)

- US: Real Earnings

- CA: Employment Data, Unemployment Rate

- CN: CPI & PPI Data

- JP: PPI Data

- KR: Interest Rate Decision

Markets are navigating a phase in which positioning dynamics and macro uncertainty interact in real time, creating a stable yet fragile environment. The shift away from aggressive de-risking has improved short-term stability, but the balance between positioning support and unresolved macro risks remains delicate.

Equities:

Markets have stabilised from oversold conditions, but participation remains narrow with large-cap leadership masking weaker breadth underneath. Price action continues to reflect a positioning-driven recovery, where rallies are supported by short covering rather than broad conviction.

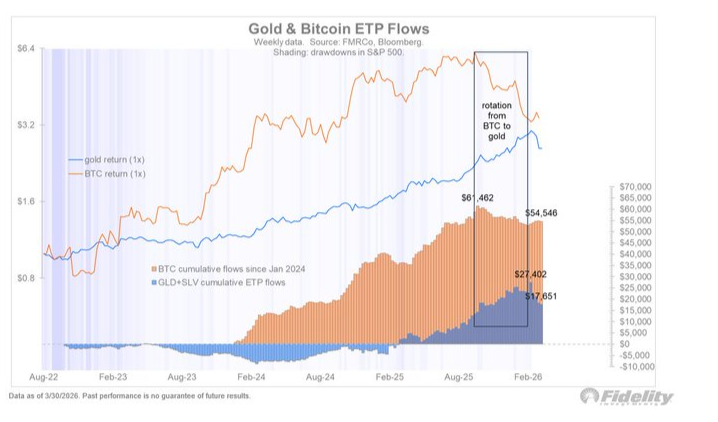

Gold & Silver:

Gold has not behaved in line with traditional geopolitical expectations, reflecting its role as a source of liquidity rather than a pure haven. Recent weakness suggests capital is being raised, even as the broader trend remains intact.

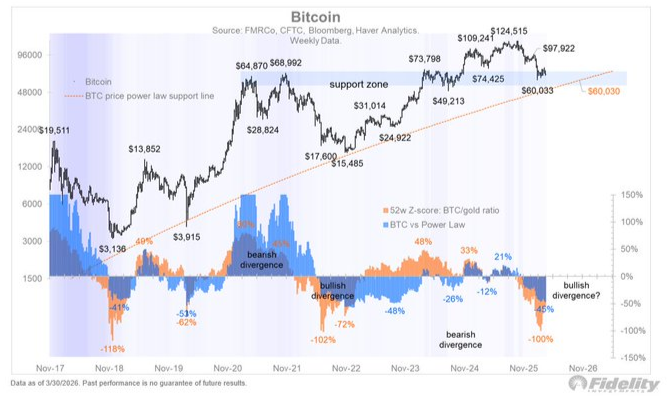

Crypto:

Crypto continues to reflect shifting liquidity dynamics, showing relative resilience compared to traditional assets. Price action appears driven more by flows than macro alignment, highlighting evolving rather than expanding participation.

Macro:

Energy remains the dominant driver, with elevated oil prices feeding into inflation pressures and weighing on growth expectations. At the same time, labour signals remain mixed and policy cautious, leaving markets reactive to data and geopolitical developments.

There are conditions for a counter-trend consolidation rally, with positioning stretched and markets already leaning defensive. That said, the environment remains headline-driven, with energy, rates, and geopolitics continuing to dictate direction. Trade carefully.