Peace Whispers, Tariff Tsunamis, and Gold’s Tug-of-War

Markets stormed into the second week of August with their strongest performance since June, powered by tech mega-caps, peace chatter between Washington and Moscow, and selective tariff exemptions. Beneath the euphoria, breadth remains thin, macro risks are mounting, and summer liquidity could amplify volatility in both directions.

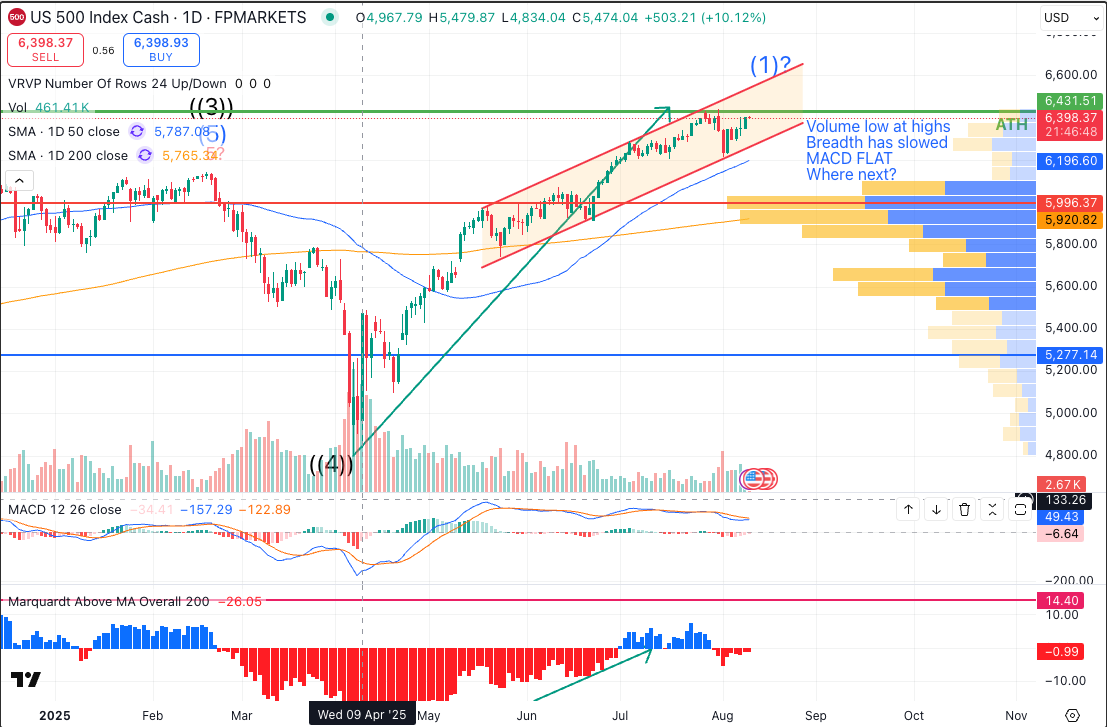

Market Overview – A Rally Running on Thin Ice

The Nasdaq 100 and the Magnificent Seven locked in fresh all-time highs, with Apple delivering its best week since 2020 — up 13.33% — after announcing a $100B US manufacturing plan to sidestep chip tariffs.

The S&P 500 approached 6,400, but momentum continues to diverge, with medium-term breadth flat near 50%.

Key Market Signals

- US 10-year yield rose seven basis points to 4.28%

- The dollar clung to its 50dma

- Oil slid on potential Russian supply returns

- Gold fluctuated within a volatile range

Macro & Policy Watch – Tariffs and Peace in the Same Breath

The US is reportedly working with Russia toward a territorial deal in Ukraine, with a Trump–Putin summit possible as early as next week.

At the same time, Trump unleashed aggressive tariffs:

- 100% on semiconductors

- 250% on pharmaceuticals

- Extra 25% on India for Russian oil imports

- Exemptions dangled for US-based producers

Treasury Secretary Bessent projected tariff revenues could exceed $300B annually.

The RBA is widely expected to cut rates by 25bps this week, while China’s CPI slipped back to 0%, raising the threat of exported deflation into the West — a setup that could support bonds in the short term.

From BoA’s Michael Hartnett

Best YTD Performers

- Russian ruble (+42%)

- Polish equities (+54%)

- Ukrainian bonds (+61%)

Peace Winners

- Japan

- China

- India (oil importers set for tariff relief)

Peace Losers

- Defence

- Tech

- Middle East markets

Dollar remains in a structural bear market; China stands as the standout “peak tariff” play.

Technical & Sentiment Breakdown – Melt-Up or Blow-Off?

Index price action is being driven by narrowing leadership and sentiment chasing. With 90% of S&P earnings reported, the market is leaning heavily toward a Q3/Q4 seasonal rally peak, but the technicals warn of exhaustion.

Gold Setup

Gold remains in a complex wave 5 structure, with buy support at 3240–3260 (GC 3300–3320) and resistance at 3400–3430 (GC 3480–3530).

A pullback could set up a sharp upside breakout into late Q3/Q4 — potentially in sync with a final equity high.

Last Week’s Recap – Tech Fireworks, Tariff Ripples, and Gold’s Standoff

Equities

Apple’s monster rally on tariff exemption hopes dominated headlines.

- Fannie Mae & Freddie Mac soared on IPO speculation valued at up to $500B

- Shopify (+22%) crushed earnings estimates

- Pfizer (+5%) raised guidance

- AMD slid on an EPS miss despite revenue growth

- Gold stalled at resistance as expected in the wave structure

Macro

Tariff news swung sentiment intraday, with exemptions boosting certain sectors while pharma and semiconductor names felt the pinch.

- China’s CPI flatlined, reinforcing deflation risks

- The dollar softened for a fifth straight day

- Oil’s breakdown reflected the peace premium unwinding

Commodities

- Gold tested its upper zone before fading

- Crude saw the biggest weekly loss since June

The Week Ahead – CPI, Central Banks, and Global Growth Data

A thin-volume week but loaded with market-moving catalysts. Tuesday’s US CPI and Friday’s global growth figures could set the tone heading into Jackson Hole.

Tuesday, August 12

- US: CPI (tariff inflation impact)

- China: CPI & PPI

- Australia: RBA Rate Decision (-25bps expected)

- UK: Employment & Earnings Data

- Germany: ZEW Economic Sentiment

- Eurozone: ZEW Economic Sentiment

- US: Federal Budget Balance

Wednesday, August 13

- New Zealand: Electronic Retail Sales (July)

- Japan: PPI (July)

- Australia: Wage Price Index (Q2)

- Germany: CPI

- Spain: CPI

- US: Mortgage Applications

- Oil: EIA Weekly Crude Inventory Data

- Auctions: Japan 5Y JGB (0.989% last), Germany 10Y Bund (2.620% last)

Thursday, August 14

- UK: GDP & Services Index

- Switzerland: PPI

- France: CPI

- Eurozone: GDP

- US: PPI

Friday, August 15

- Japan: GDP

- China: Retail Sales

- China: Industrial Production

- US: Retail Sales

- US: University of Michigan Consumer Sentiment (Prelim)

- US: Atlanta Fed GDPNow Q3 Estimate

Alpha Takeaway – Patience Before the Pop

This rally leg is nearer the end than the start. Peace headlines could squeeze markets to fresh highs, but thin breadth and macro divergences suggest chasing here is risky.

Gold’s consolidation is worth buying on weakness, and bonds could be the stealth winner if deflation pressure builds.

Our Stance

- Fade euphoric breakouts into resistance

- Buy gold dips in the buy zone for Q3/Q4 upside

- Size smaller in thin summer trade and prepare for outsized swings on data surprises