Jackson Hole, Inflation Whiplash, and Summer Seasonality

Markets enter the week at record highs but on shaky legs, with traders eyeing Jackson Hole for clarity. A 25bp cut in September is now the base case, though whispers of a “buy the rumour, sell the fact” fade linger. Meanwhile, geopolitics is back on the radar with Trump-Putin theatrics in Alaska, Ukraine guarantees in play, and oil slipping on renewed Russian flows. Beneath the calm, cracks in breadth, sentiment, and services inflation are worth watching.

Market Overview: Highs on Fumes, Cracks Beneath

The bulls still have control, but the structure looks increasingly fragile:

- SPX at all-time highs, but leadership is narrow—10 stocks driving 80% of gains

- Oil sold off as peace chatter allows Russian supply back

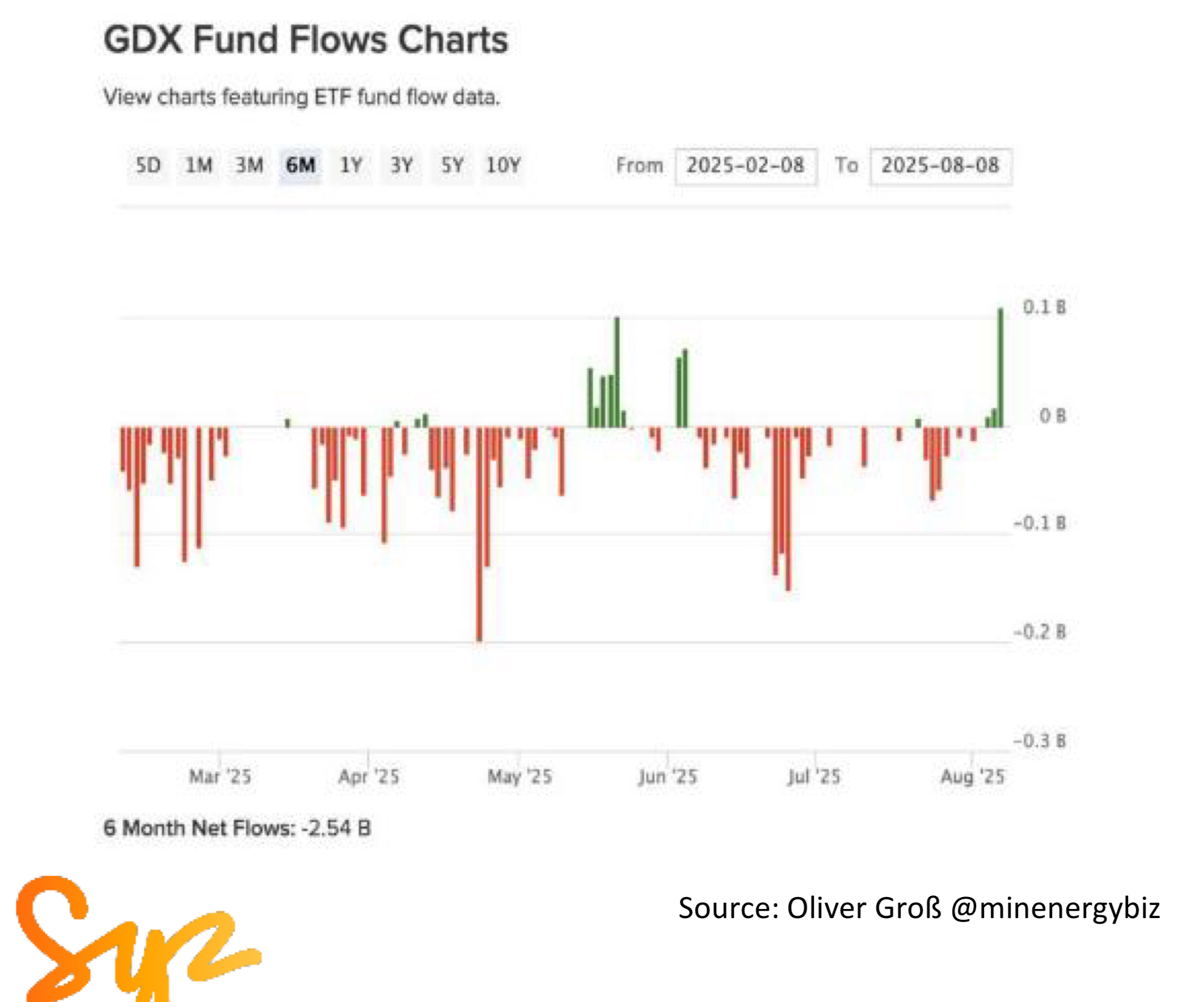

- Gold consolidating, but miners see inflows—a bullish tell

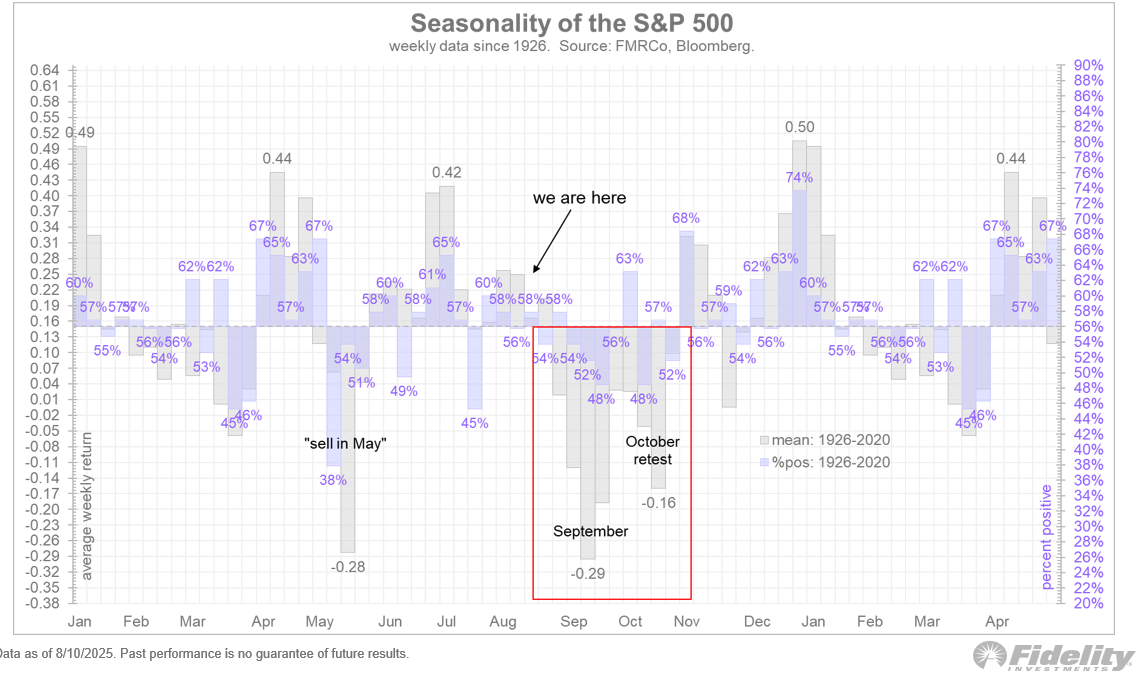

- Seasonality into late August and September historically brings weakness, especially in post-election years

Summer liquidity is thin, which means volatility can spike without much warning. Think cartoon physics: all looks fine—until everyone looks down.

Macro & Policy Watch: Powell in the Hole

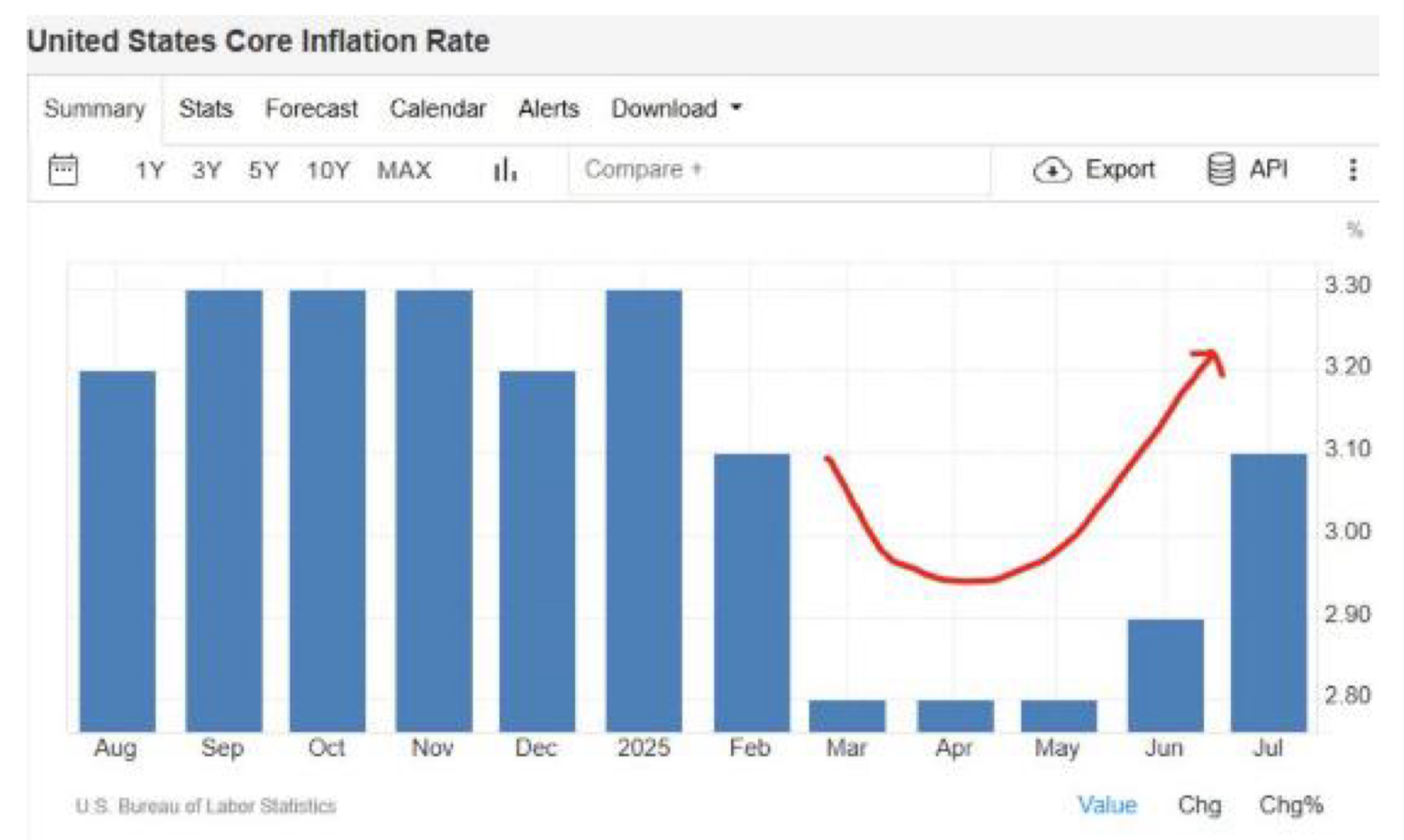

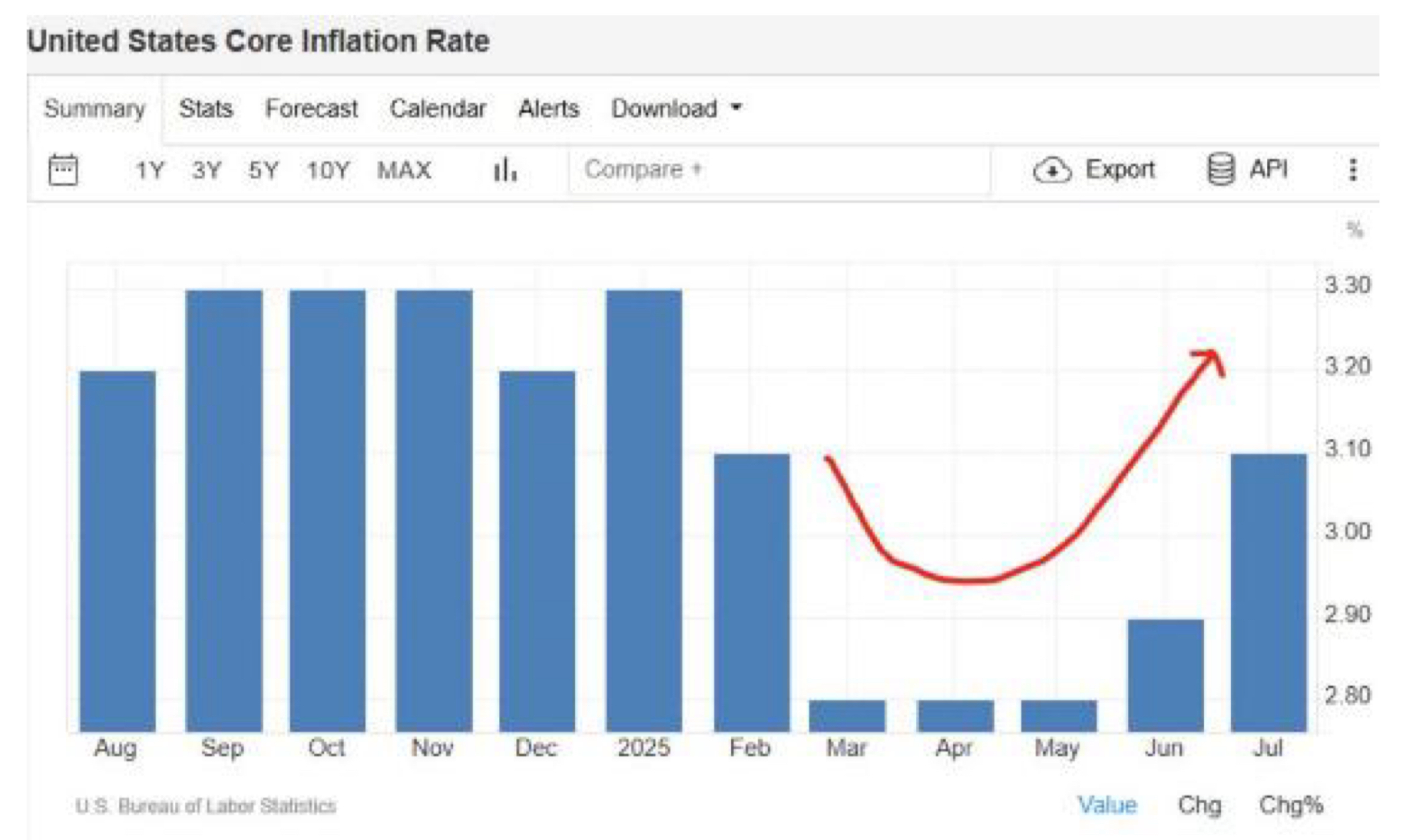

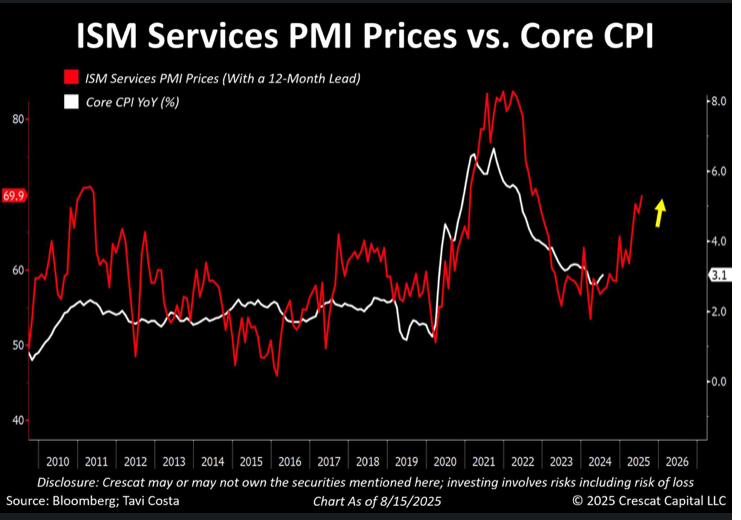

Inflation: The Services Sting

Last week’s US CPI/PPI mix was unsettling. Goods stayed tame, but services inflation roared back, raising stagflation whispers. ISM Services Prices Paid—a 12-month lead on Core CPI—is flashing red.

Global Data: Diverging Paths

- Japan beat GDP expectations, freeing the BoJ to stay hawkish if inflation holds

- UK GDP also beat, supporting a slow, steady BoE easing path

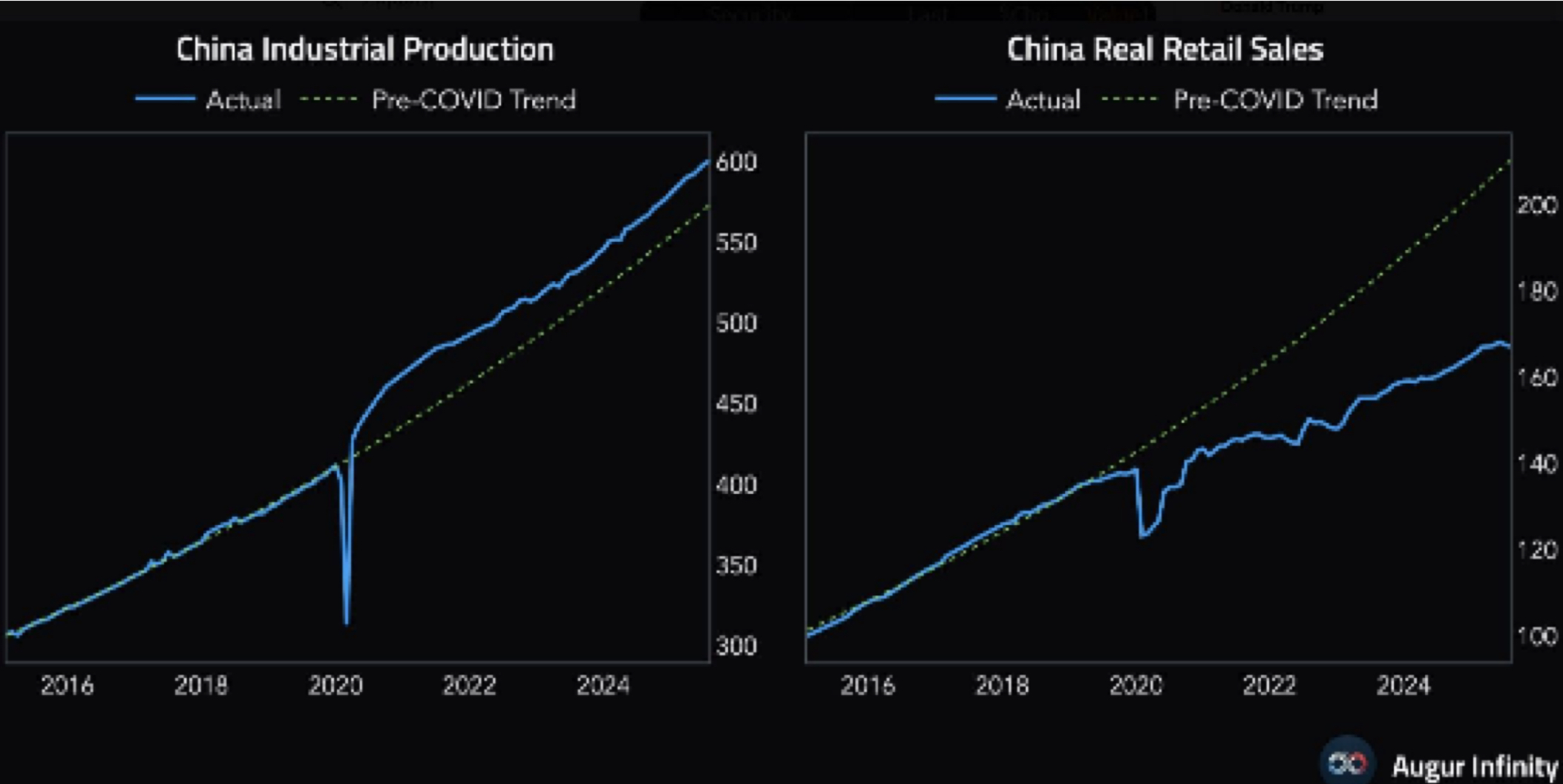

- China's retail sales slumped, and PPI deflation deepened. The fiscal “bazooka” can’t be far

US Consumers: Strong but Shaky

Retail sales were broad-based and solid, led by autos and online promos. Yet sentiment fell for the first time since April—and UoM credibility came under fire.

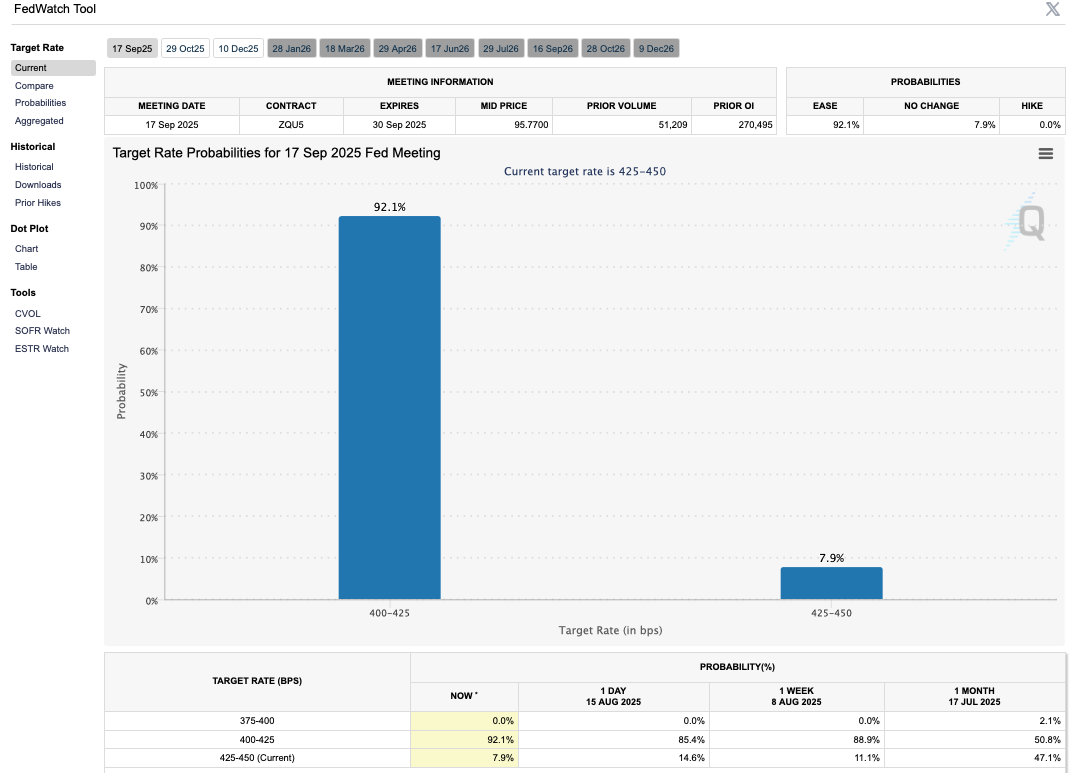

Rates: All Eyes on Jackson Hole

Fed cut odds remain stacked for September, but hotter PPI trimmed expectations from 100% to 90%. Talk of 50bps lingers, but 25bps is the base case.

Technical & Sentiment Breakdown: Fragile Setup

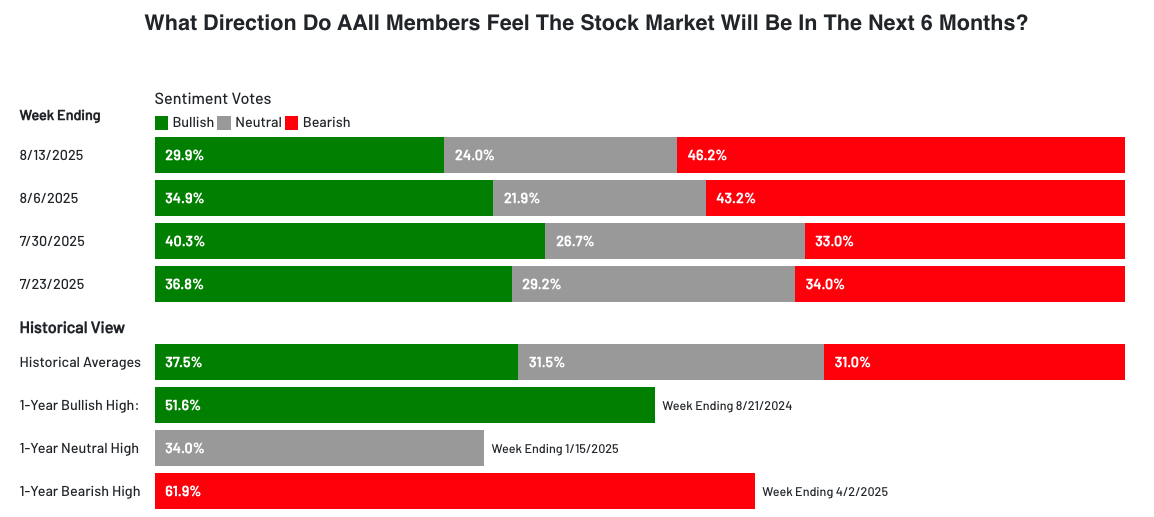

Sentiment Neutral, But Fragile

BofA’s bull-bear index sits neutral, while AAII shows bearishness creeping back in. Not panic levels, but enough to suggest fragility at highs.

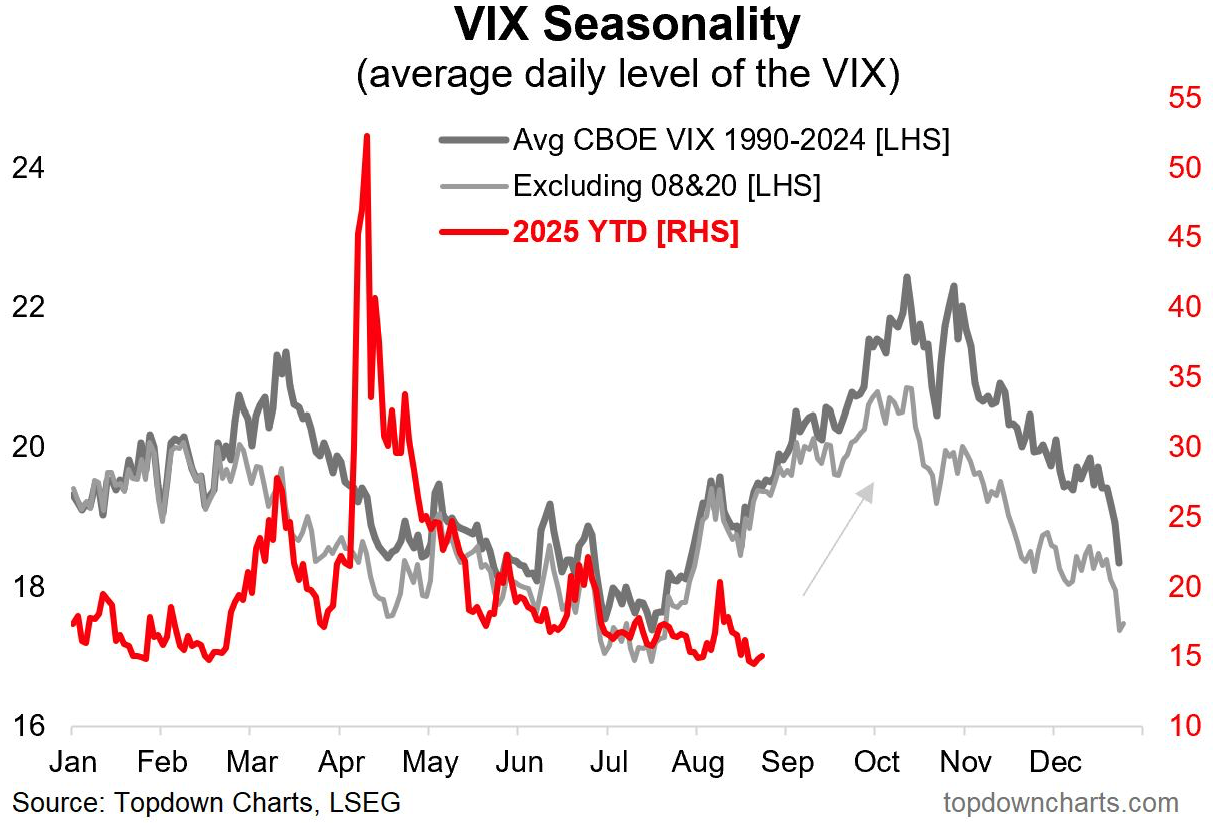

Volatility Seasonality

The VIX tends to rise into late Q3 and Q4—even excluding GFC and Covid extremes. Summer calm rarely lasts.

Earnings: A Rare Q2 Spurt

EPS growth in Q2 accelerated unusually fast, forcing underweights to chase. Analysts were caught off guard, turning a would-be earnings drag into a tailwind.

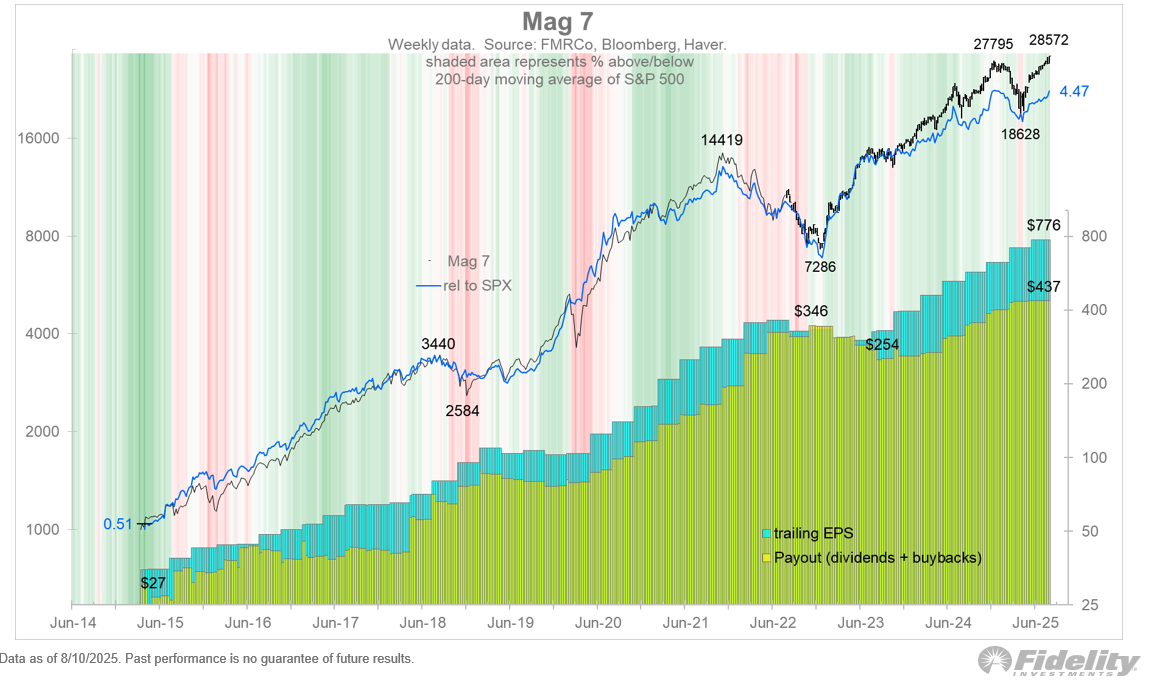

Narrow Leadership

The MAG7 remains the most crowded trade. Earnings still justify the flows, but watch credit spreads—first cracks will show there.

Gold vs. Oil Divergence

- Gold sits in a bullish consolidation triangle, with miners attracting inflows

- Oil drifts lower on Russian supply and inventory builds

This is late-cycle behaviour: narrow leadership, defensive flows into metals, and creeping volatility.

Last Week’s Recap: Inflation Sparks, Earnings Punch

Inflation

- US CPI showed an uptick led by services

- PPI surged on vegetables and services

- Tariff effects muted—for now

Retail Sales

- Stronger on autos and online

- Services spending sagged

Global Data

- UK GDP stronger than expected

- Japan back to growth

- China disappointed across the board

Fed Speak

- Hawks urging patience

- Doves open to cuts

- 50bps chatter flared, but odds remain stacked for 25bps

Earnings

- Applied Materials disappointed

- UnitedHealth surged on fresh inflows

Markets largely shrugged off the noise, grinding higher on liquidity and buy-the-dip psychology.

The Week Ahead: Day by Day Breakdown

Monday, August 18th

- NZD: Performance of Services Index 48.9 (up from 47.6)

- GBP: Rightmove HPI YoY -1.3% (vs +0.1% prior)

- CHF: Industrial Production

- EZ: Trade Balance

- CAD: Housing Starts (July)

- USD: NAHB Housing Market Index (Aug)

- Auctions: German 12M bill, US 3M & 6M bills

Tuesday, August 19th

- NZD: PPI

- EZ: Current Account

- USD: Building Permits (July), Housing Starts (July), Redbook, Atlanta GDPNow

- CAD: CPI (July)

- OIL: API weekly inventories

- Auctions: German 5Y Bobl

Wednesday, August 20th

- JPY: Machine Orders, Trade Balance

- CNY: Loan Prime Rate (expected unchanged)

- NZD: RBNZ Rate Statement (expected 25bp cut to 3%)

- GBP: CPI/RPI (July)

- GR: PPI (July)

- EZ: CPI (July final)

- USD: Mortgage data, FOMC minutes

- CAD: New HPI

- Auctions: German 30Y Bund, US 20Y Bond

Thursday, August 21st

- NZD: Trade Balance

- AUD: Manufacturing & Services PMI (Aug)

- Global: Flash PMIs (EZ, UK, US, Japan, India)

- CHF: Trade Balance

- USD: Jobless Claims, Philly Fed Index, Existing Home Sales, Fed Balance Sheet

- CAD: PPI

- EZ: Consumer Confidence (Aug)

- Auctions: US 4W Bill, 8W Bill, 30Y TIPS

Friday, August 22nd

- GBP: GfK Consumer Confidence (Aug), Retail Sales

- JPY: National CPI

- GER: GDP

- CAD: Retail Sales

- USD: Jackson Hole Symposium begins (key risk event)

Alpha Takeaway: Buy the Dip or Sell the Fact?

This market is walking on air: record highs, narrow leadership, and seasonal chop ahead. Jackson Hole may be Powell’s chance to thread the needle—but with services inflation back, tariffs biting, and political heat rising, the risk is the Fed underdelivers.

Short-Term

- Defensive rotation and higher vol likely

Medium-Term

- Earnings strength and liquidity still support the bull

Trade Setups

- Buy dips in quality equities

- Hedge with gold/silver on breakout watch

- Stay nimble on oil until supply politics clear

The market isn’t in bubble territory yet, but it is running on fumes. Don’t chase highs—keep cash ready for the dip.