Jobs Shock, Fed Firestorm & Gold on the Move

Markets stumbled hard into August as the macro floor gave way beneath a richly priced equity rally. With NFP revisions rattling the Fed and political pressure mounting, the stage is set for a volatile mid-month reversal—or one last squeeze into seasonal highs.

Market Overview: A Rally Interrupted by Reality

What started as a textbook grind-up turned into the worst week for equities since May 2023.

- S&P 500: -2.4%

- Nasdaq 100: -2.4%

- Dow Jones: -3.0%

- Russell 2K: -4.4%

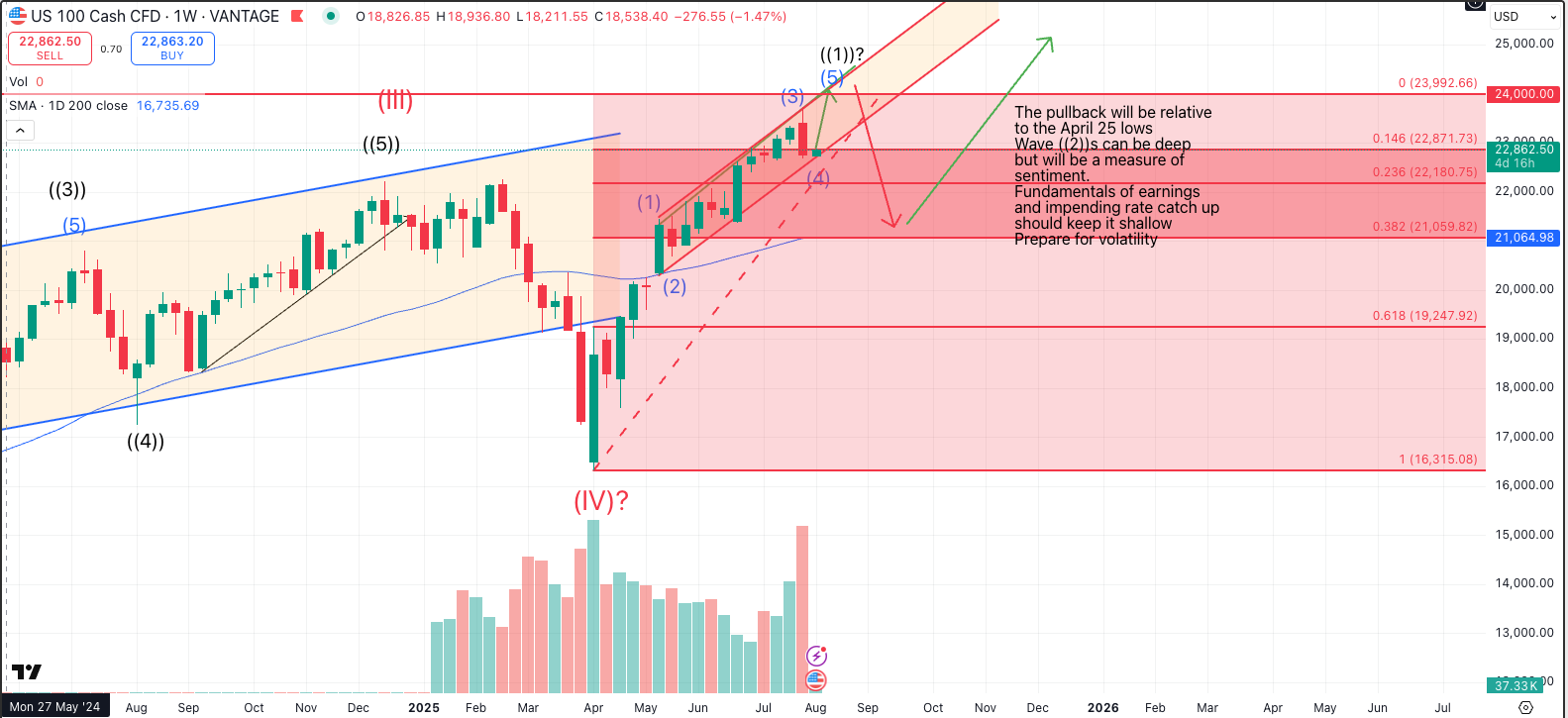

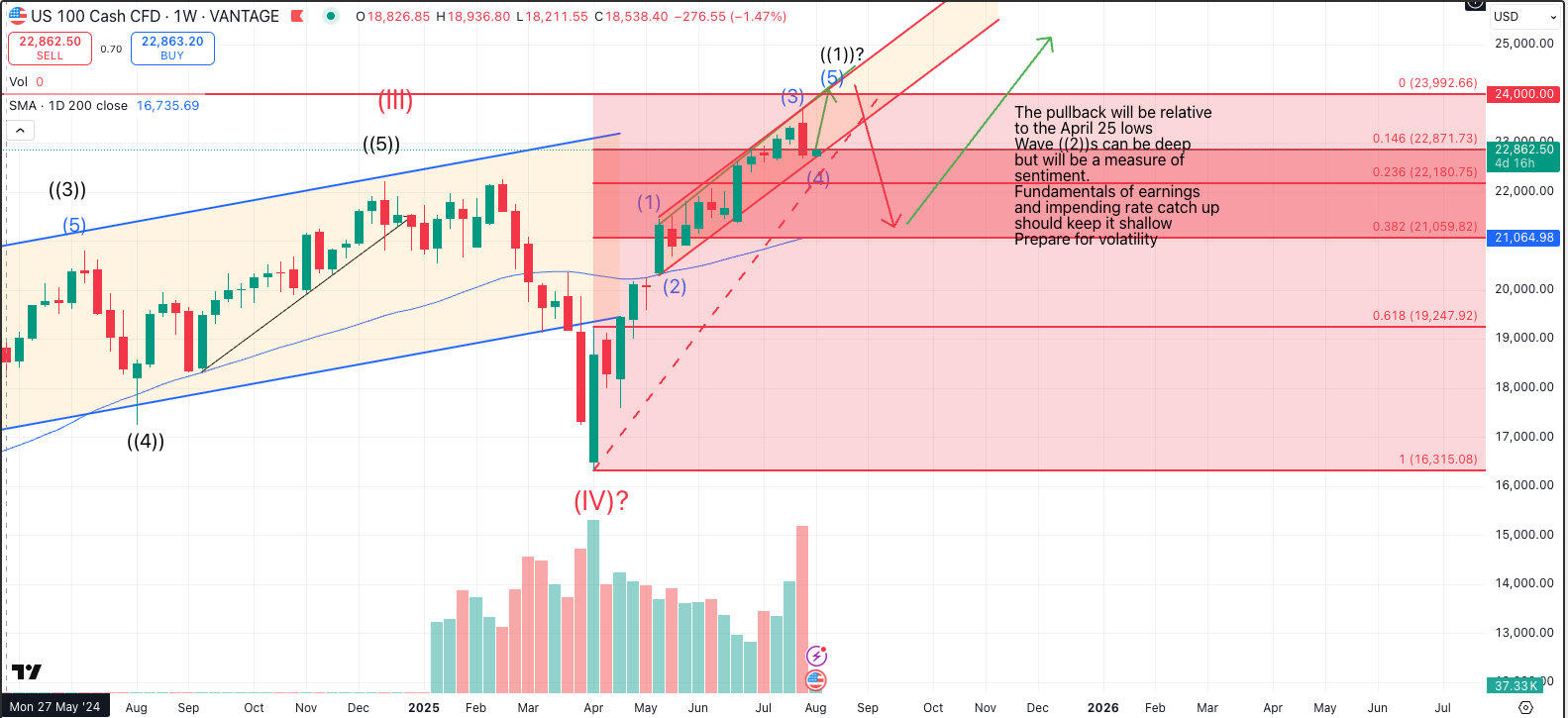

The tech-led advance hit resistance as the Nasdaq brushed the top of its rising channel. Last week’s correction aligns with our mid-August seasonal top scenario—likely a final leg higher remains before summer peaks.

But it's not just price exhaustion. Breadth is narrowing, volatility is reawakening, and macro support is fraying.

- VIX broke above 20

- Bond market volatility stayed oddly low—a telltale divergence

Cash levels remain high, which could support a bounce, but chasing here is risky.

Macro & Policy Watch: Fed in the Crosshairs, Jobs Collapse

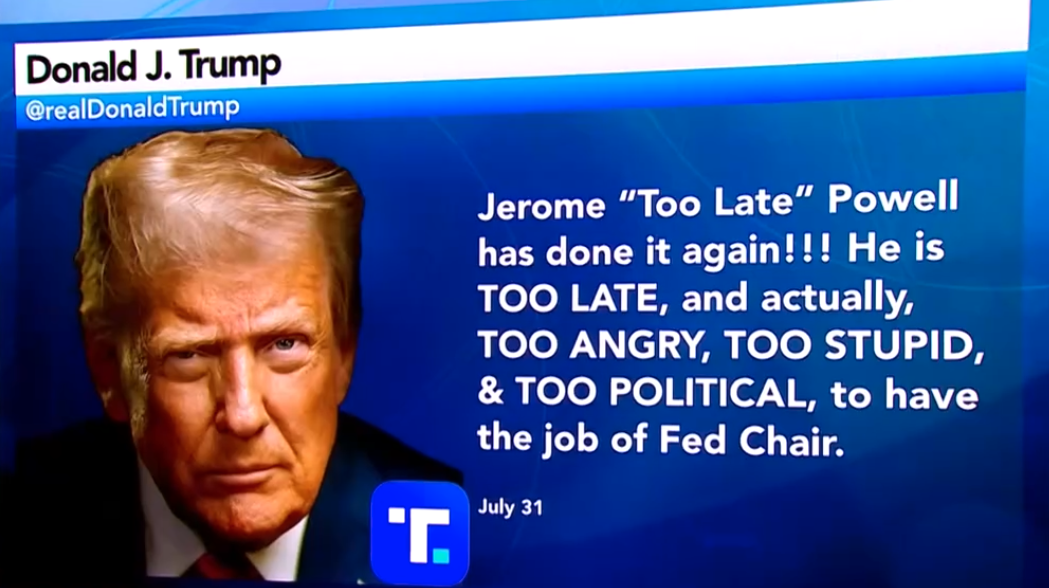

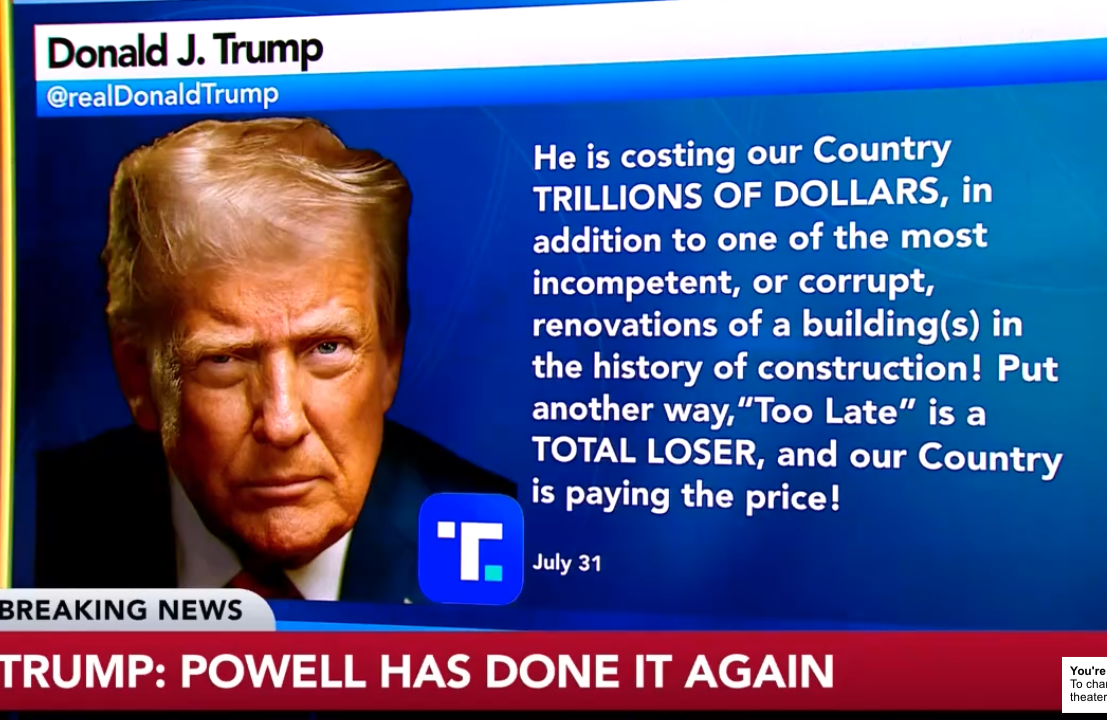

Powell Dodges, Trump Reloads

Last week’s FOMC meeting passed quietly, but the real fireworks came after.

- Fed Governor Kugler resigned, giving Trump a free slot to install a dovish voter

- Two dissenters (Waller & Bowman) openly opposed Powell, first time in decades

- Trump is now publicly pressuring Powell to resign, escalating the political war on Fed independence

The market got the message.

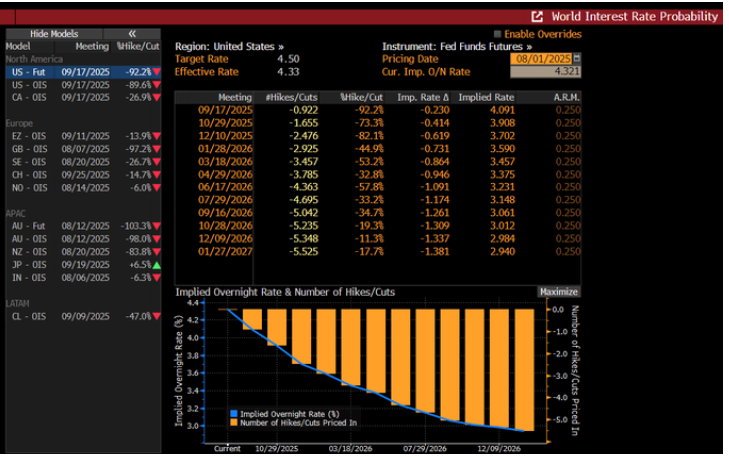

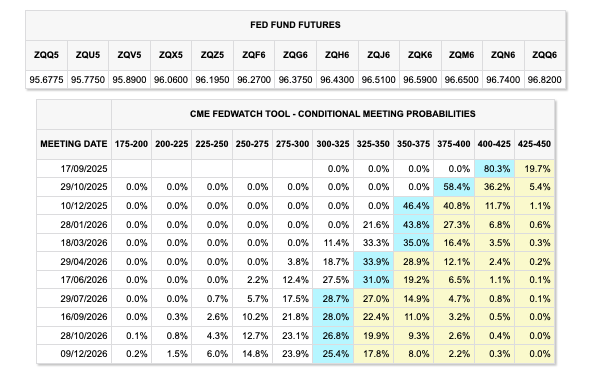

- Rate cut odds for September are now 92%, per Bloomberg’s WIRP and CME’s FedWatch tools

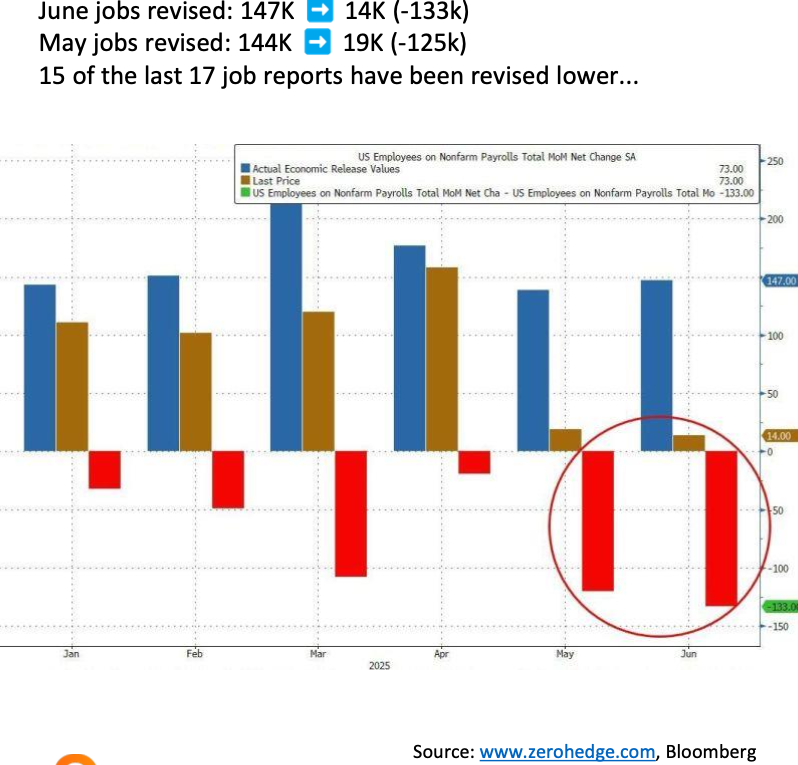

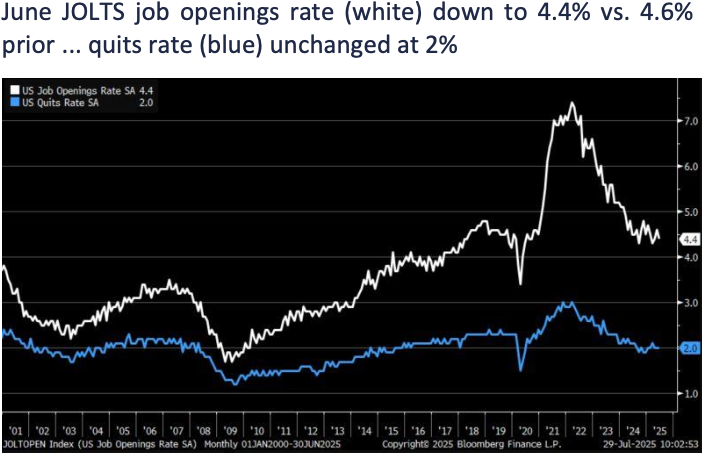

Jobs: The Dam Broke

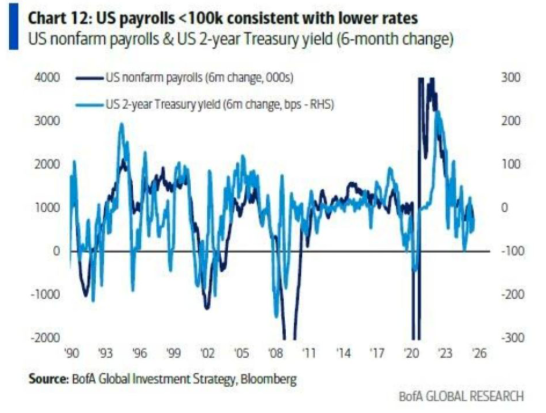

The July NFP print (73k) was a shock, but the bigger surprise was the massive downward revisions—258,000 jobs were erased, the worst revision since 1978.

Over the last 3 months, the economy has added just 35k jobs/month—a near stall. Hiring has collapsed.

This isn’t just weak data—it’s a political earthquake. Trump sacked BLS Chief Erika McEntarfer after the release, raising even more questions about data integrity and Fed independence.

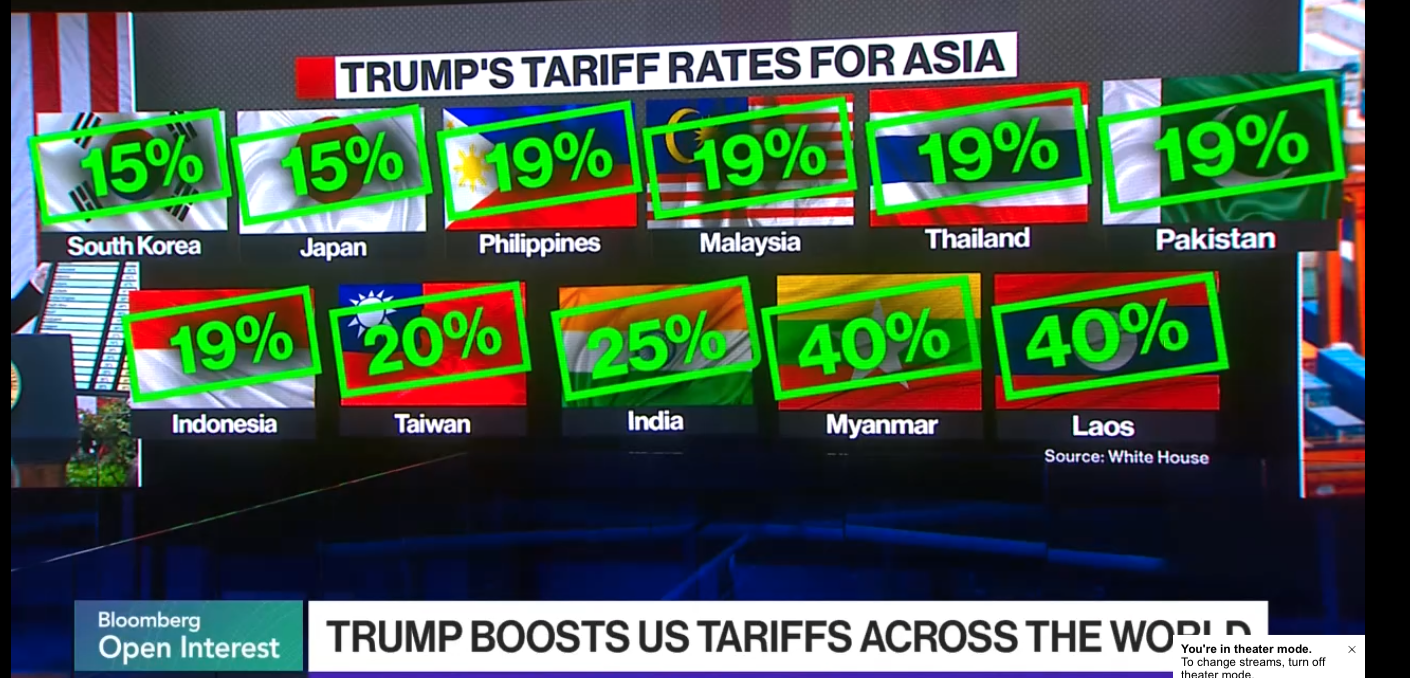

Tariffs: Weaponised Again

The average tariff rate was raised to 15.2%, with some countries like Switzerland hit with 39%. Trump also accelerated the de minimis threshold rule to Aug 29, 2025—four years early.

Expect ripple effects on inflation, margins, and consumer sentiment, especially in Q3.'

Technical & Sentiment Breakdown: A Fragile Setup

While equity indices remain in uptrends, the structure is deteriorating:

- SPX is grinding higher but stalling

- Nasdaq is stretched but not broken

- VIX has popped

- Semis are still leading, but risk appetite is showing signs of reversal

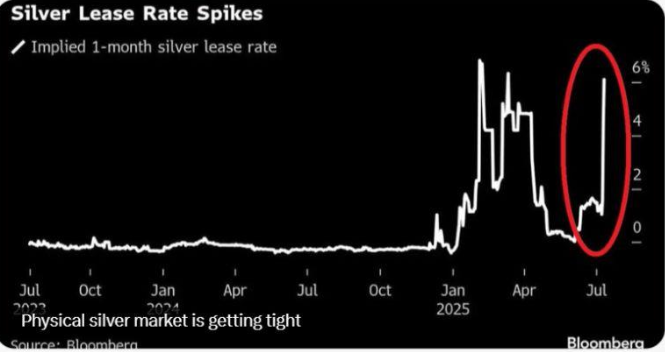

Meanwhile, gold and silver are quietly gaining steam. Rising geopolitical tensions, fiscal dominance, and Fed turmoil are powering up real assets.

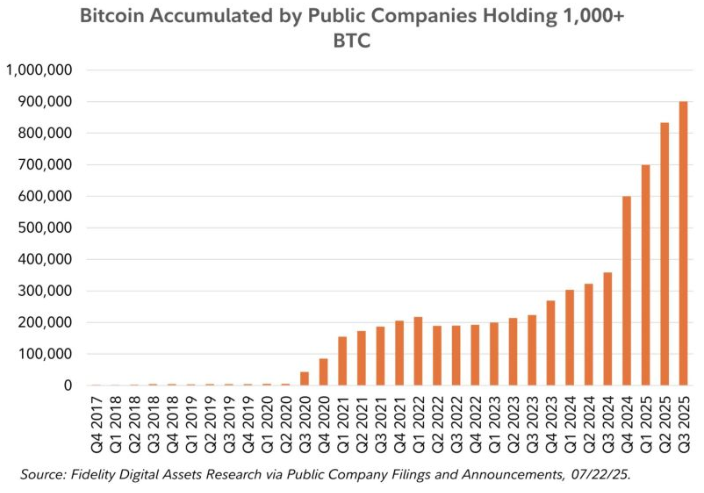

Crypto—especially BTC—also saw renewed inflows as macro hedges came back into focus.

This is classic late-cycle behaviour—speculative excess on one hand, safety rotation on the other.

Last Week’s Recap: Earnings Hold Up, Macro Doesn’t

Earnings: Strong Beats, Even in Tech

Despite the broader weakness, earnings were a bright spot:

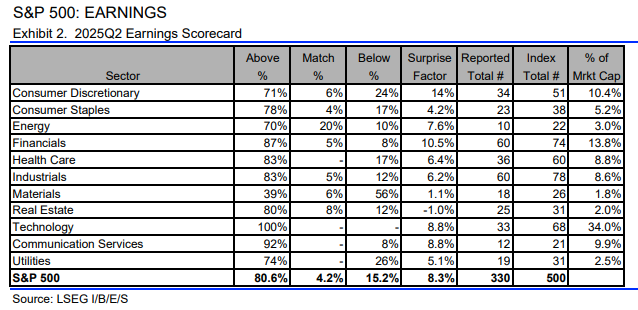

- 66% of SPX has reported

- 81% beat rate

- Q2 EPS growth revised to 11.2%, up from 5.8% forecast

Apple, Meta, Microsoft, and Amazon all posted strong results, although the latter stumbled on outlook. Apple is playing a longer AI game, while peers are going heavy on CapEx.

Meanwhile, Berkshire Hathaway posted a rare disappointment, writing down Kraft Heinz and posting a 59% drop in net income.

Macro Data: Warnings Were There

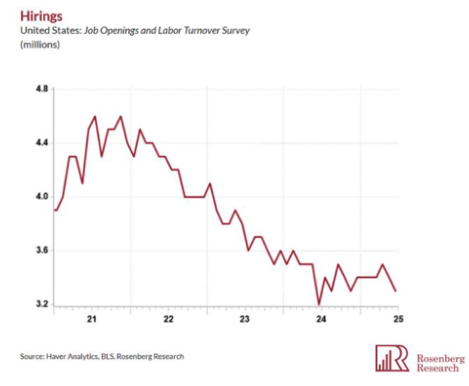

The JOLTS report previewed the NFP revisions collapse with a 261k hiring drop, the second-lowest since 2020. PCE remained sticky, but the composition showed offsetting forces—tariffed goods vs falling shelter costs.

The ISM manufacturing miss also signalled softening demand and suggests the Fed is behind the curve.

The Week Ahead: Fed Fallout, Global PMIs & UK Decision

Another heavy macro week lies ahead—Fed commentary, global PMIs, and UK rate decisions take the spotlight.

Monday, August 4

- UK (Scotland) Bank Holiday

- Canada Civic Holiday

- CHF CPI

- USD Durable Goods, Factory Orders

Tuesday, August 5

- Global Services PMIs (US, EZ, UK, CNY, JPY)

- USD ISM Services

- USD Atlanta GDPNow Q3 estimate

- USD Trade Balance

- Oil API Weekly Inventory

- Earnings: Pfizer, BP, CAT, AMD, SNAP, Rivian, Opendoor

Wednesday, August 6

- NZD Employment Data

- EZ Retail Sales

- USD Mortgage Applications

- Earnings: Uber, Shopify, Disney, McDonald’s, Duolingo, DraftKings

- Fed Speakers: Daly, Cook, Collins

Thursday, August 7

- BoE Rate Decision (expected hold at 4.25%)

- GBP Halifax HPI

- USD Jobless Claims

- USD Productivity & Unit Labour Costs

- USD Consumer Credit

- Earnings: Eli Lilly, ConocoPhillips, Sony, Pinterest, Twilios

- Central Bank Speakers: ECB Rehn, BOE Bailey, FOMC Bostic

Friday, August 8

- CAD Employment Data

- JPY Household Spending

- CHF Consumer Climate

- Earnings: Wendy’s, Terawulf

- Fed Speaker: Musalme

Alpha Takeaway: Prepping for the Mid-August Pivot

Markets are wobbling—but the bigger risk may still lie ahead. Beneath the surface, the late-cycle warning signs are flashing:

- Breadth is collapsing—7 stocks = 32% of SPX cap

- Job market revisions destroyed the “soft landing” story

- Fed independence is under attack—Powell vs Trump showdown looms

- Tariffs are back, and inflation risks may re-emerge

- Gold, silver, and BTC are quietly outperforming

Still, liquidity remains high, earnings are beating, and the rally could grind out one final leg into the August peak—unless the Fed breaks first.

Our Stance

- Stay long, high-quality, large caps, but tighten stops into strength

- Add BTC, gold, and silver on pullbacks—macro hedges are back in play

- Watch Wednesday–Friday closely: UK rate decision, ISM Services, and Fed speakers will steer the tone