Rates Push Back, AI Leadership Cracks, and Markets Confront the Cost of Capital

Market Overview: Price Resilience, Structural Friction

What initially looked like a clean post-Fed relief rally faded quickly as markets were forced to confront a familiar problem: rate cuts do not automatically mean easier financial conditions. While the Fed delivered the cut the market wanted, long-end yields moved the wrong way, tech leadership buckled, and credit markets once again proved quicker to react than equities.

Volatility stayed contained, and broader indices avoided disorderly selling, but the tone beneath the surface shifted meaningfully. AI winners faced their first serious credibility test, bond markets tightened financial conditions independently of policy, and flows — while still supportive — became far more selective. This was not panic, but it was a reminder that liquidity is no longer free.

Equities entered the week well-positioned heading into the Fed, with positioning light and downside hedges elevated. That setup initially worked. Markets absorbed the policy decision without stress, and dip buyers remained active.

However, strength proved fragile once leadership faltered. Friday’s sharp tech sell-off underscored how narrow the market’s tolerance has become for capital-intensive growth stories.

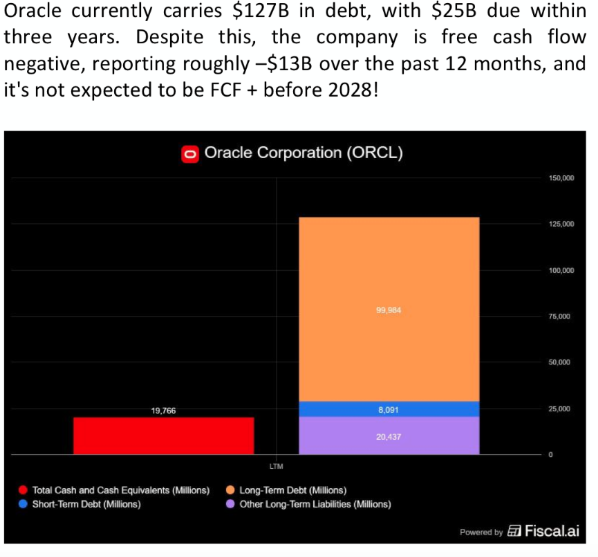

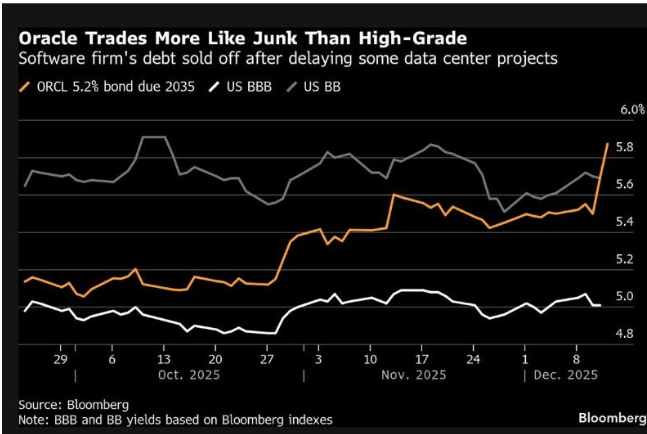

Oracle became the focal point of that reassessment. Credit markets had already been flagging concern, and equity investors were forced to catch up quickly as questions around cash flow durability and capex intensity resurfaced.

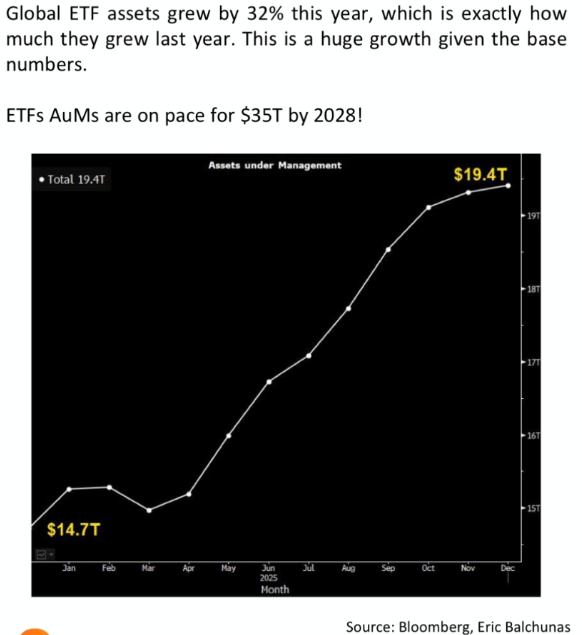

Flows remain supportive in aggregate, particularly through ETFs, but the character of buying has changed — less indiscriminate, more defensive.

The market is still being held together by flows — but the margin for narrative disappointment is shrinking.

Macro & Policy Watch: A Dovish Cut Meets a Hawkish Yield Curve

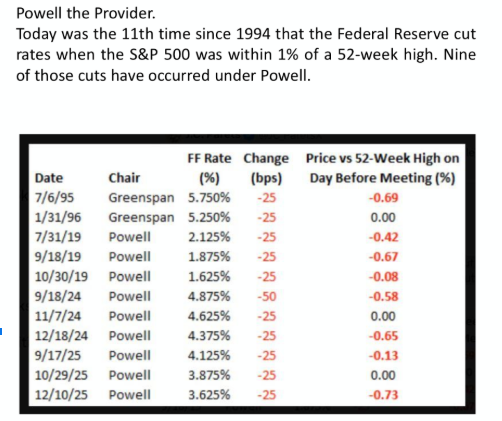

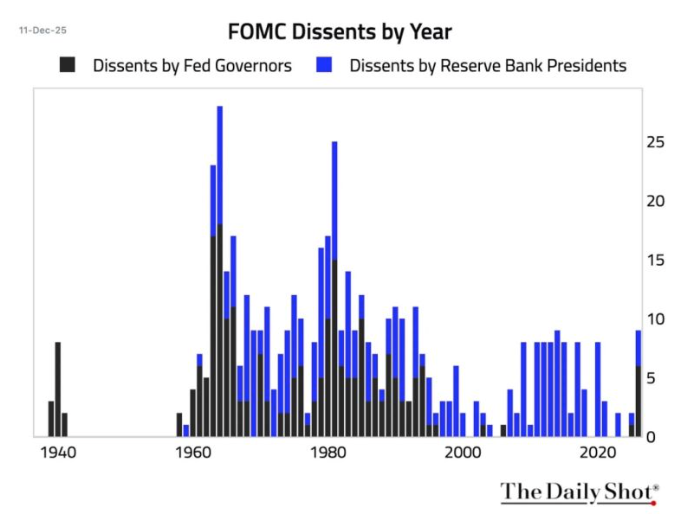

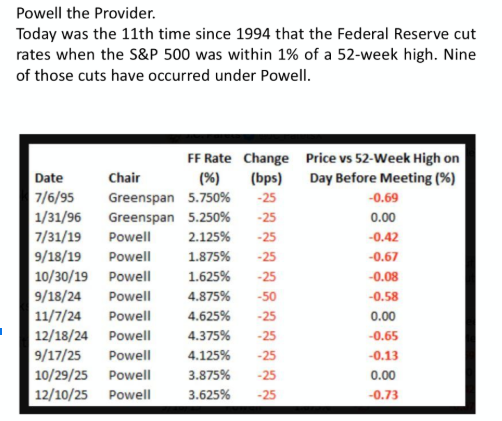

The Fed delivered the cut markets expected, but the internal story was more complex. Dissents widened, the hawk-dove balance shifted, and the message around future easing was noticeably less unified than headlines suggested.

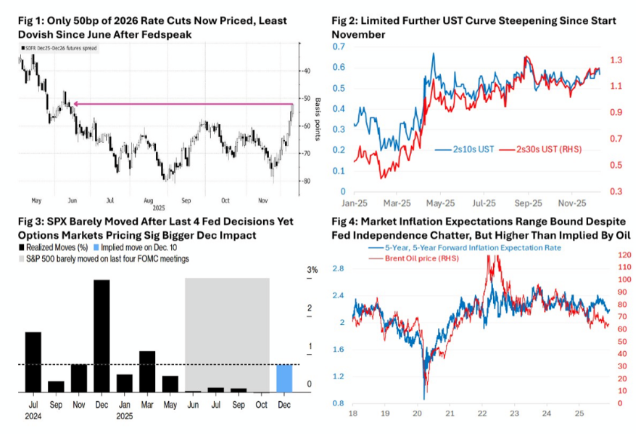

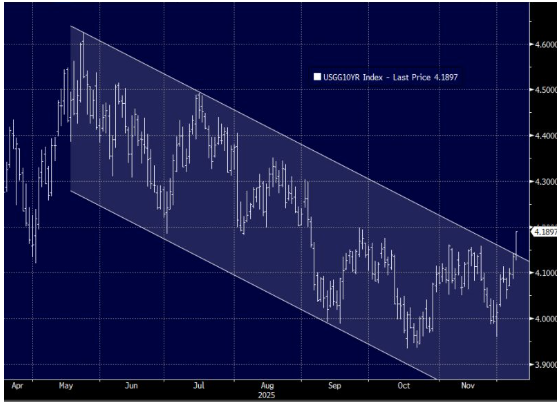

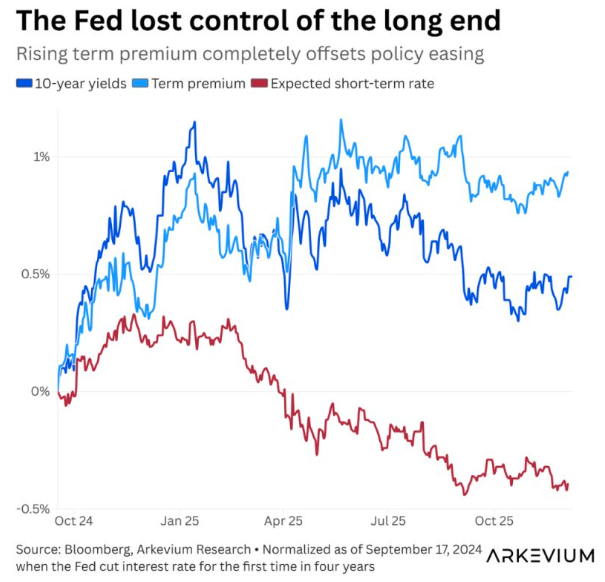

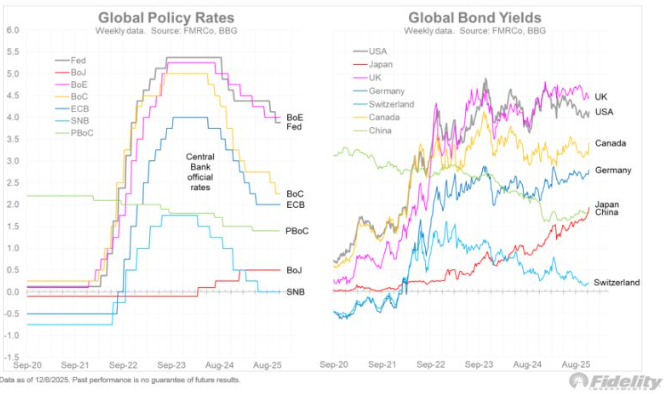

While the policy rate moved lower, long-end yields did not cooperate. Instead, Treasury yields pushed higher, tightening financial conditions at the very moment policymakers were attempting to ease them.

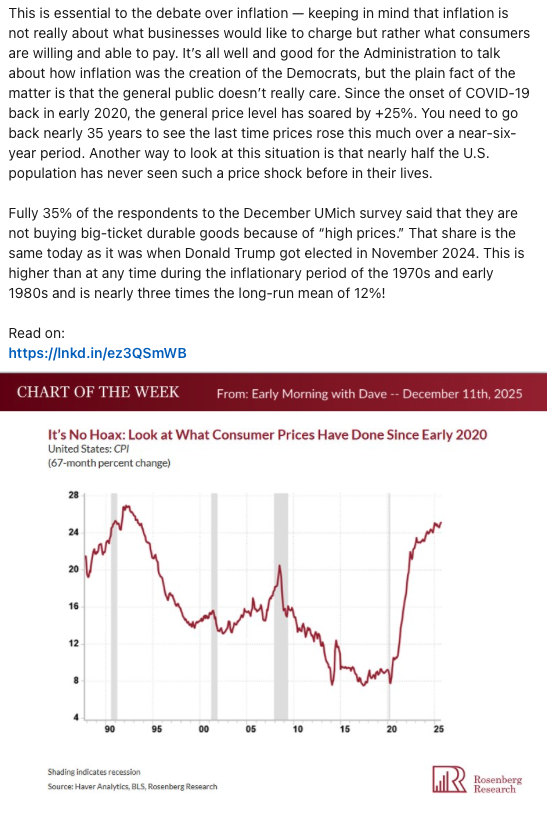

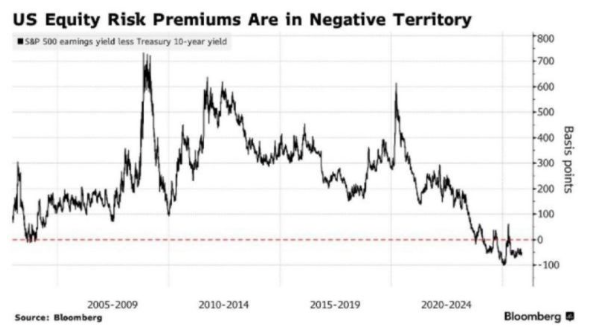

This disconnect matters. As Rosenberg highlighted, markets respond to price levels, not just inflation rates — and elevated borrowing costs continue to pressure duration-sensitive assets.

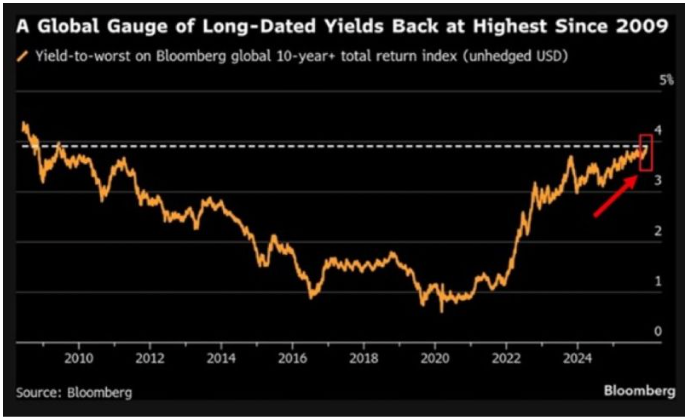

Globally, the pressure is not isolated. Bond markets across regions remain under strain, reinforcing the idea that fiscal supply and term premium — not policy rates — are driving the next phase.

Technical & Sentiment Breakdown: Support Holding, Leadership Fading

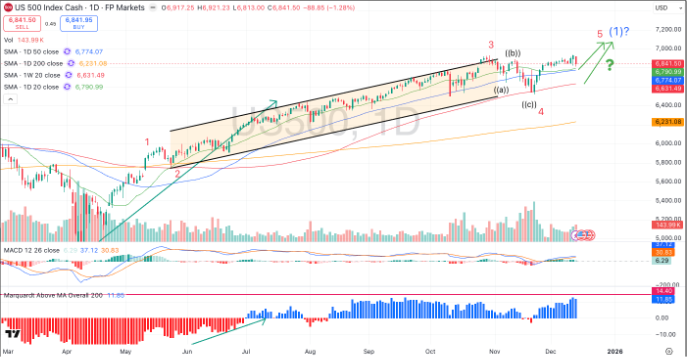

From a technical standpoint, broader indices remain intact, but leadership damage is evident.

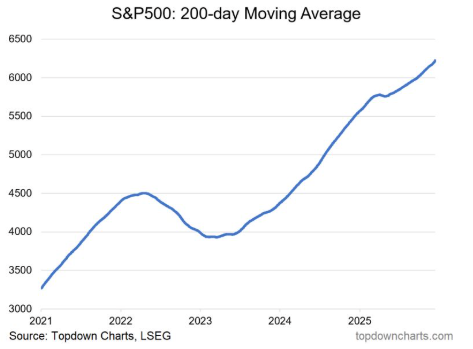

The S&P 500 continues to hold above key moving averages, though upside momentum has slowed as gamma dynamics flatten.

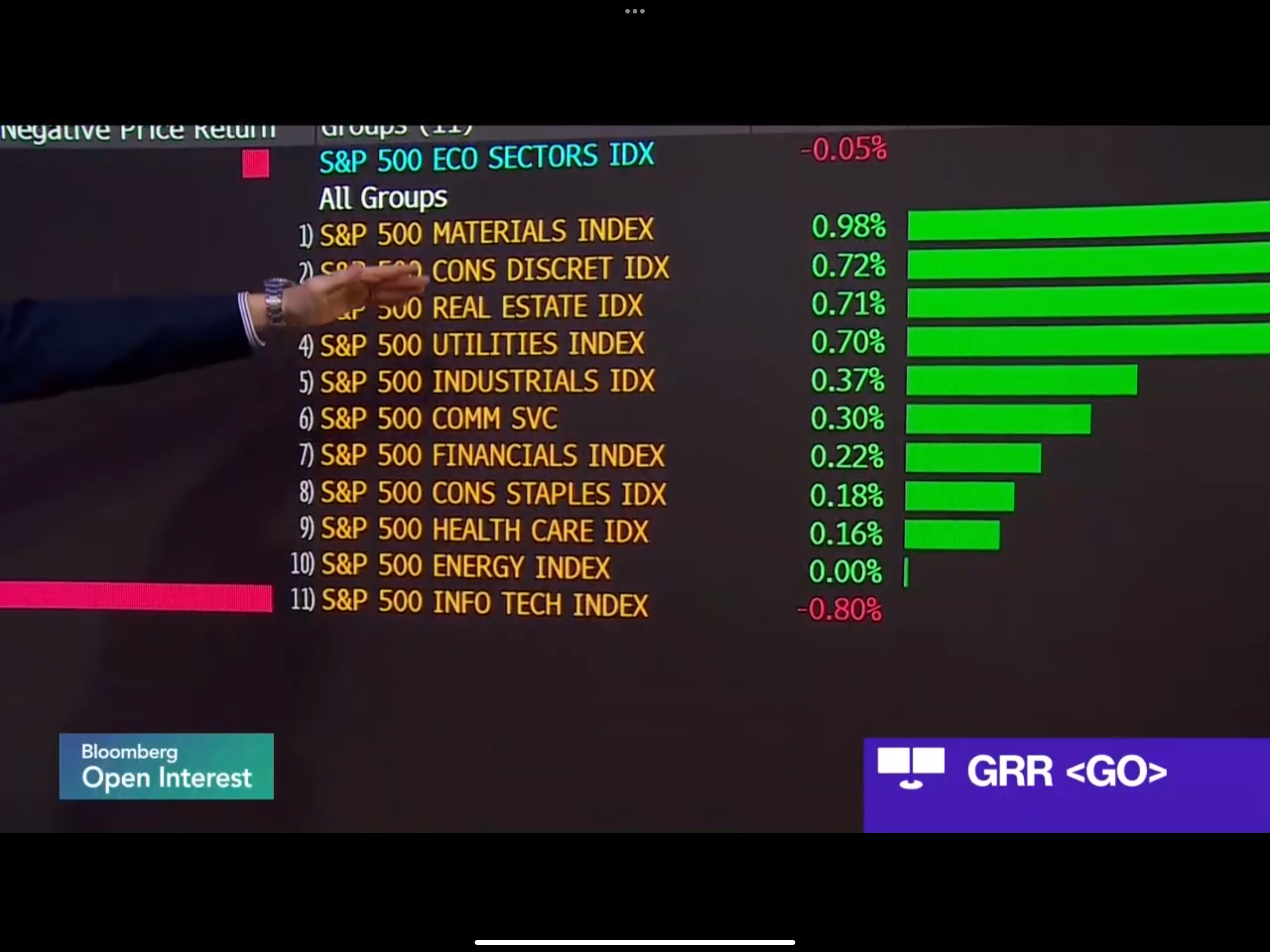

Nasdaq, however, closed the week on a weaker footing, slipping below key averages and confirming the rotation away from high-multiple tech.

Dow outperformance reflects this shift, with cyclicals and financials benefiting from curve steepening.

Sentiment indicators remain calm, but pockets of excess remain unresolved.

This is a market still supported by structure — but no longer forgiving of valuation or leverage.

Last Week’s Recap: Fed Relief, Yield Pushback, and AI Reality Checks

Markets began the week cautiously but stabilised by Friday as the Fed delivered its expected cut, and near-term downside risks eased. However, beneath the surface, rising long-end yields and cracks in AI leadership tempered enthusiasm and reinforced the market’s growing sensitivity to the cost of capital.

Key Highlights:

Macro:

The Fed delivered a rate cut as expected, but the reaction mattered more than the decision itself. While front-end rates eased, long-dated yields pushed higher, tightening financial conditions and undermining the traditional “cuts = risk-on” playbook. Dissents widened, highlighting an increasingly fractured policy backdrop.

Rates & Bonds:

Treasury yields broke higher across the curve, with the 10Y threatening a technical breakout. The Fed’s inability to control the long end reinforced concerns that fiscal supply and term premium are now driving conditions more than policy intent.

Equities & AI:

AI leadership suffered a sharp credibility test. Oracle sat at the centre of the repricing as concerns around capex intensity, delayed cash flow, and data-centre execution resurfaced. The late-week tech selloff confirmed that markets are no longer willing to fund growth stories on narrative alone.

Flows:

ETF inflows remained supportive, cushioning broader indices despite leadership damage. However, the character of buying shifted — more passive, less conviction-driven — leaving markets vulnerable to further yield pressure.

Commodities:

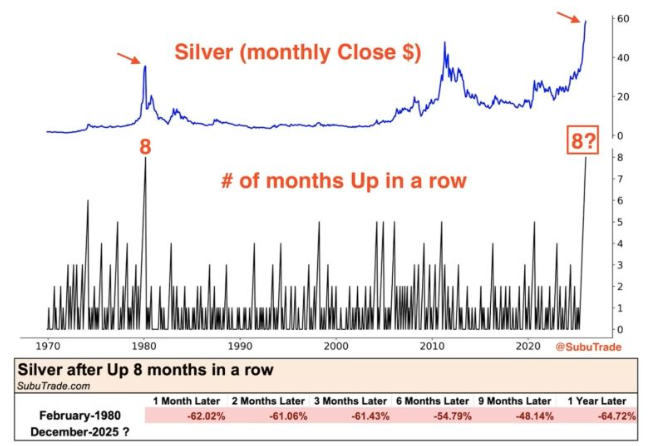

Gold likes the QE read but paused late in the week as yields rose, entering a wait-and-see phase ahead of clearer liquidity signals. Silver remained volatile following an outsized move, reflecting its sensitivity to shifts in financial conditions, but also higher on supply tightness and JP Morgan buying physical.

Crypto:

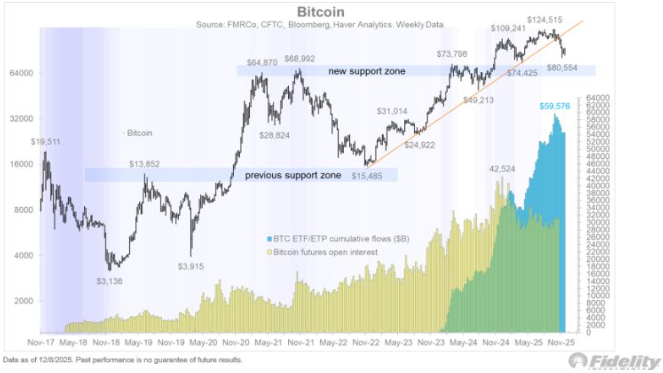

Bitcoin stabilised after recent volatility, with price holding key support zones. Liquidity conditions, rather than sentiment, remain the dominant driver.

The Week Ahead: Data Digestion, Central Banks, and Bond-Market Risk

A dense macro calendar closes out the final full trading week of the year. With the Fed decision now behind markets, focus shifts to inflation, labour-market follow-through, and a heavy slate of global central-bank decisions, all against the backdrop of tightening long-end yields and thinning year-end liquidity.

Monday, Dec 15

- Japan: Tankan Large Manufacturers & Services

- China: Industrial Production, Retail Sales

- China: Fixed Asset Investment, Unemployment Rate

- Eurozone: Industrial Production

- U.K.: Rightmove House Price Index

- U.S.: Empire State Manufacturing Index, NAHB Housing Market Index

Tuesday, Dec 16

- Australia: Manufacturing & Services PMIs

- Japan: Manufacturing & Services PMIs

- U.K.: Labour Market Report (Earnings, Unemployment, Claimant Count)

- Eurozone: ZEW Economic Sentiment

- U.S.: Retail Sales

- U.S.: ADP Employment

- U.S.: Nonfarm Payrolls (catch-up data)

Wednesday, Dec 17

- U.K.: CPI, PPI

- Germany: Ifo Business Climate

- Eurozone: CPI (Final), Wages, Labour Cost Index

- U.S.: MBA Mortgage Applications

- U.S.: Crude Oil Inventories

- U.S.: 20-Year Treasury Note Auction

Thursday, Dec 18

- U.K.: BoE Rate Decision, MPC Vote Split, Minutes, Bailey Speaks

- Eurozone: ECB Rate Decision, Press Conference

- Japan: BoJ Press Conference

- U.S.: Jobless Claims

- U.S.: Philly Fed Index

Friday, Dec 19

- Japan: CPI, BoJ Rate Decision

- U.K.: Retail Sales, GfK Consumer Confidence

- Eurozone: Business & Consumer Confidence

- U.S.: Core PCE, Personal Income & Spending

- U.S.: Michigan Sentiment

Alpha Takeaway: Policy Cut, Market Pushback

The Fed cut, but the message from markets was clear: easing policy is no longer enough. With term premiums rising and fiscal supply pressuring long rates, the bond market continues to dictate risk conditions.

Equities:

Broader indices remain supported by flows and structure, but leadership is narrowing fast. AI and high-duration names are no longer insulated from balance-sheet scrutiny. Stay selective and respect rotation risk.

Gold & Silver:

Gold remains structurally constructive but needs yields to stabilise. Silver’s higher beta keeps it volatile, attractive tactically, and dangerous emotionally.

Crypto:

Bitcoin continues to build a base, but upside remains liquidity-dependent. Stability is encouraging; confirmation is still required.

Macro:

The cut is done. What matters now is control, or lack thereof, over the long end. If yields continue to rise, financial conditions will tighten regardless of policy intent, capping upside into year-end.

“The bond market rules everybody, and with yields breaking higher, it is setting the limits on how far risk assets can run — regardless of rate cuts.”

Trade the structure. Respect the cost of capital. Stay nimble.