Flows Re-Ignite, Volatility Implodes, and Early Signs of a December Melt-Up

What looked like a painful end to November flipped sharply into strength as markets staged one of the most powerful rebound weeks of 2025. Forced selling, negative gamma, and AI panic all unwound at once, giving way to a flow-driven surge that caught most traders flat-footed. Despite crypto wobbling and thin holiday liquidity, equities found their footing as structural pressure turned supportive.

Still, the undertone isn’t entirely calm. Job cuts are accelerating, seasonal patterns point to early-week turbulence, and sentiment remains fragile underneath the relief rally. The market appears to be transitioning from “fear of further downside” to “fear of missing December’s upside.”

Market Overview: Flows Over Fear

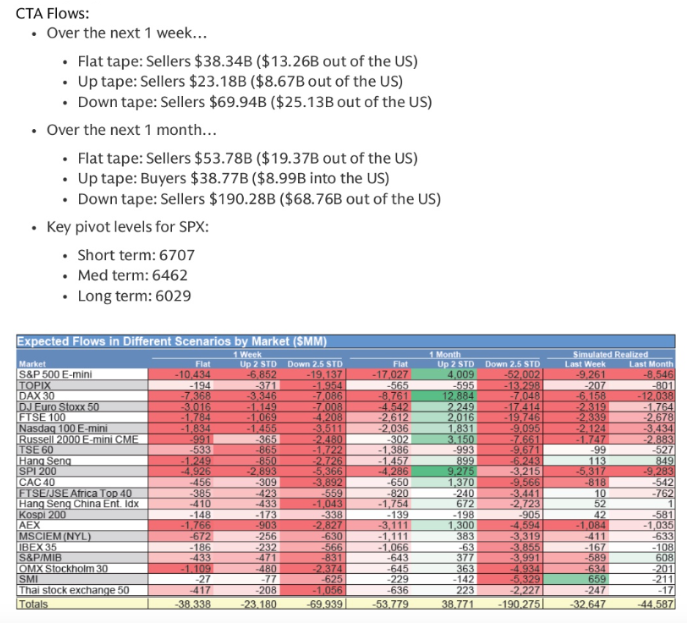

Last week’s rally was built almost entirely on positioning.

After spending most of November under pressure, the broad market ripped higher as dealer gamma flipped, hedge funds covered shorts, and month-end flows overwhelmed bearish narratives.

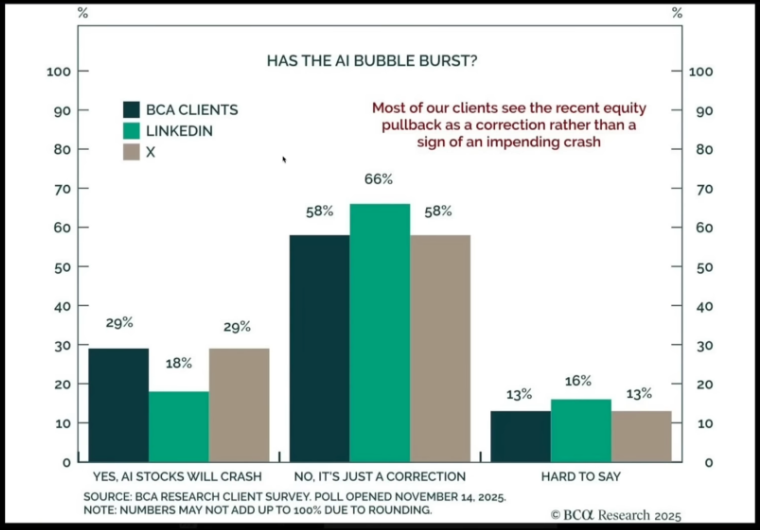

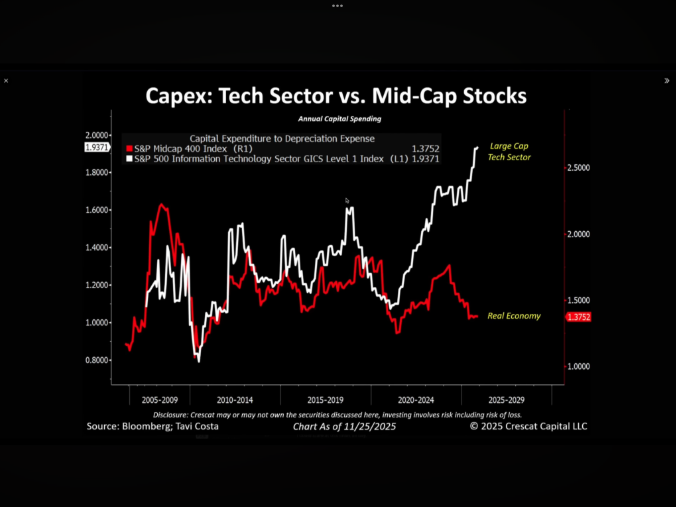

The AI panic that dominated early November eased as traders reassessed the actual risk behind shifting capex trends. Long-term investment cycles remain intact even as short-term uncertainty triggered sharp rotations.

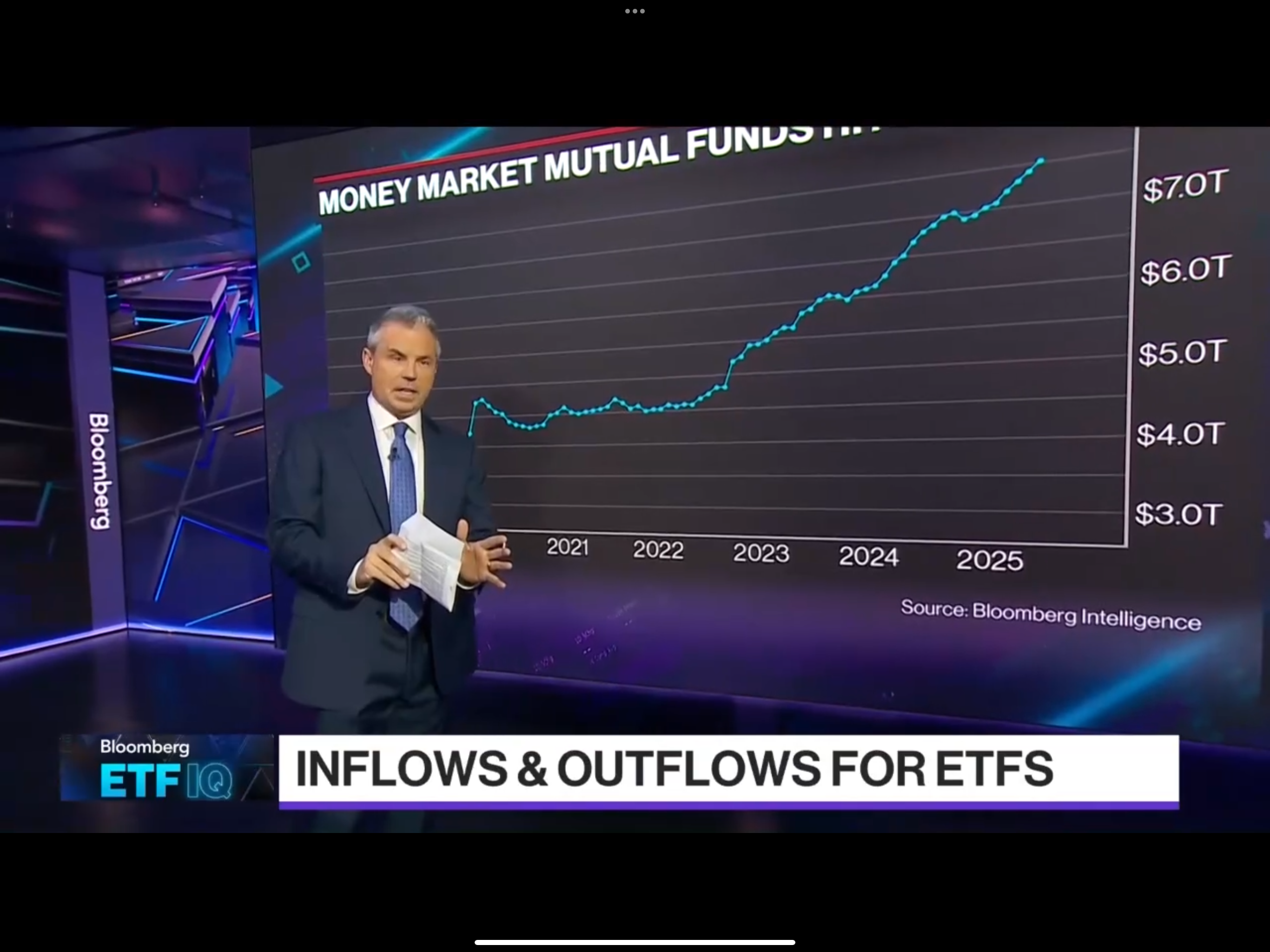

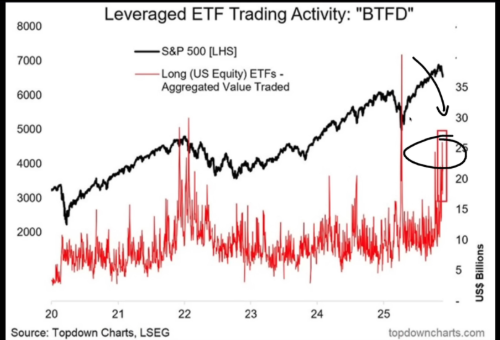

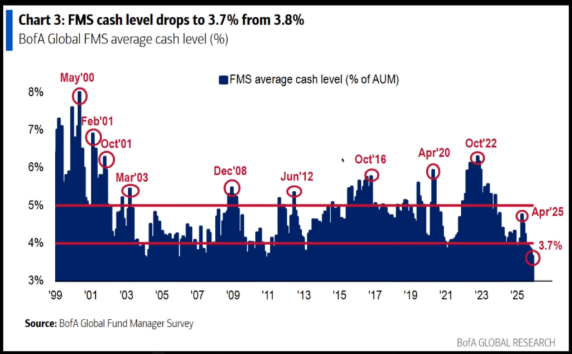

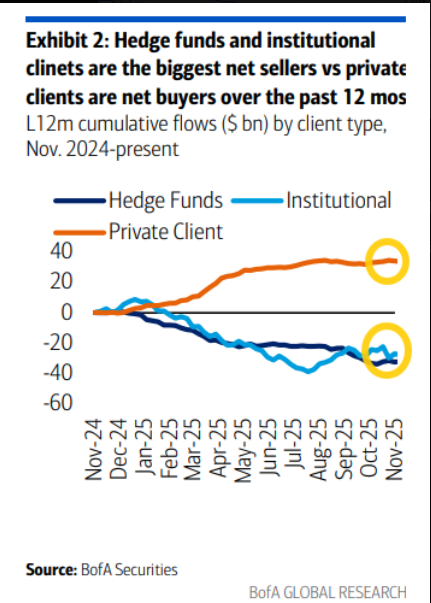

Flows confirmed the shift. Institutions and retail returned aggressively, while money parked in cash near record highs still represents potential dry powder.

The market wasn’t positioned for good news — so even mediocre news sparked an outsized reversal.

Macro & Policy Watch: Soft Labour, Global Easing, Seasonal Tension

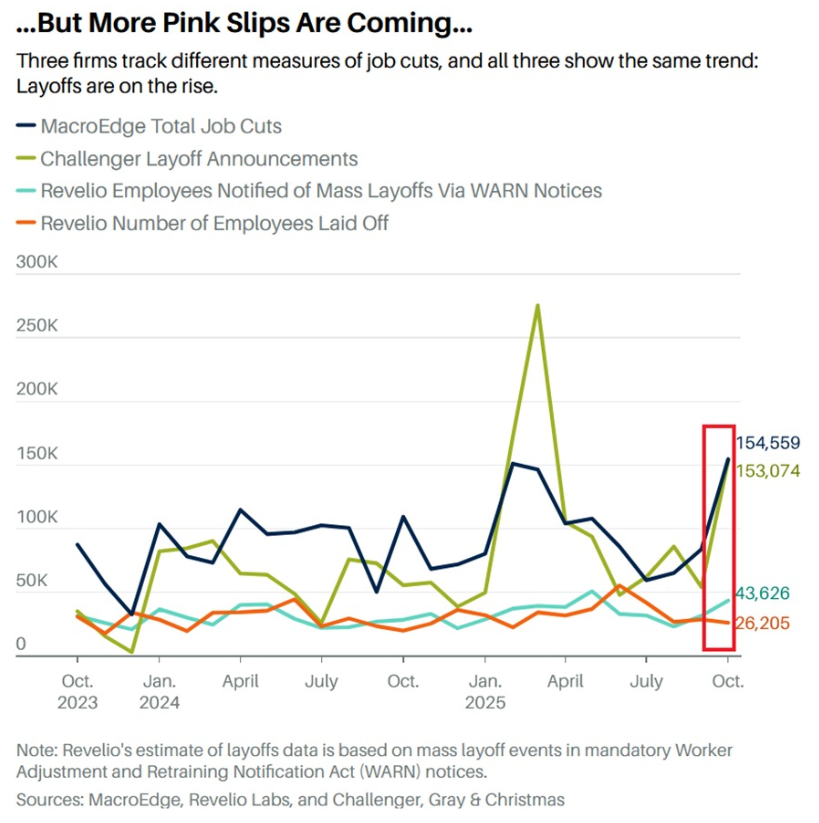

Recent alternative labour data highlighted a notable softening in conditions — something policymakers can’t ignore. Monthly job cuts, WARN notices, and Challenger layoffs all pushed higher, revealing stress beneath headline strength.

At the same time, global easing remains historically aggressive, with more than 300 rate cuts delivered in the last two years. This liquidity wave is now colliding with weakening fundamental data — a setup that often leads to choppy but upward-biased markets.

Seasonality complicates near-term flows.

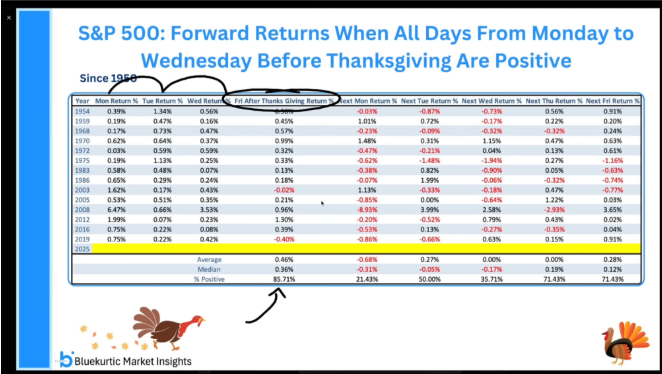

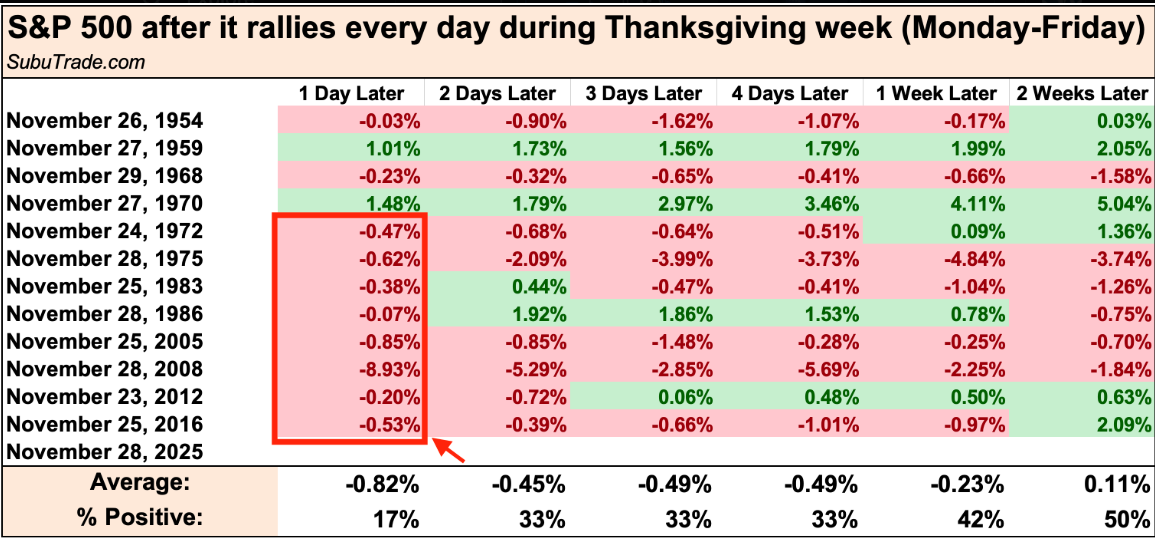

Thanksgiving week produced four straight green days — a pattern that often leads to Cyber Monday weakness, especially when Treasury settlements overlap.

Volatility remains crushed, with both short-dated and implied measures sitting near lows — a calm that feels increasingly disconnected from economic data.

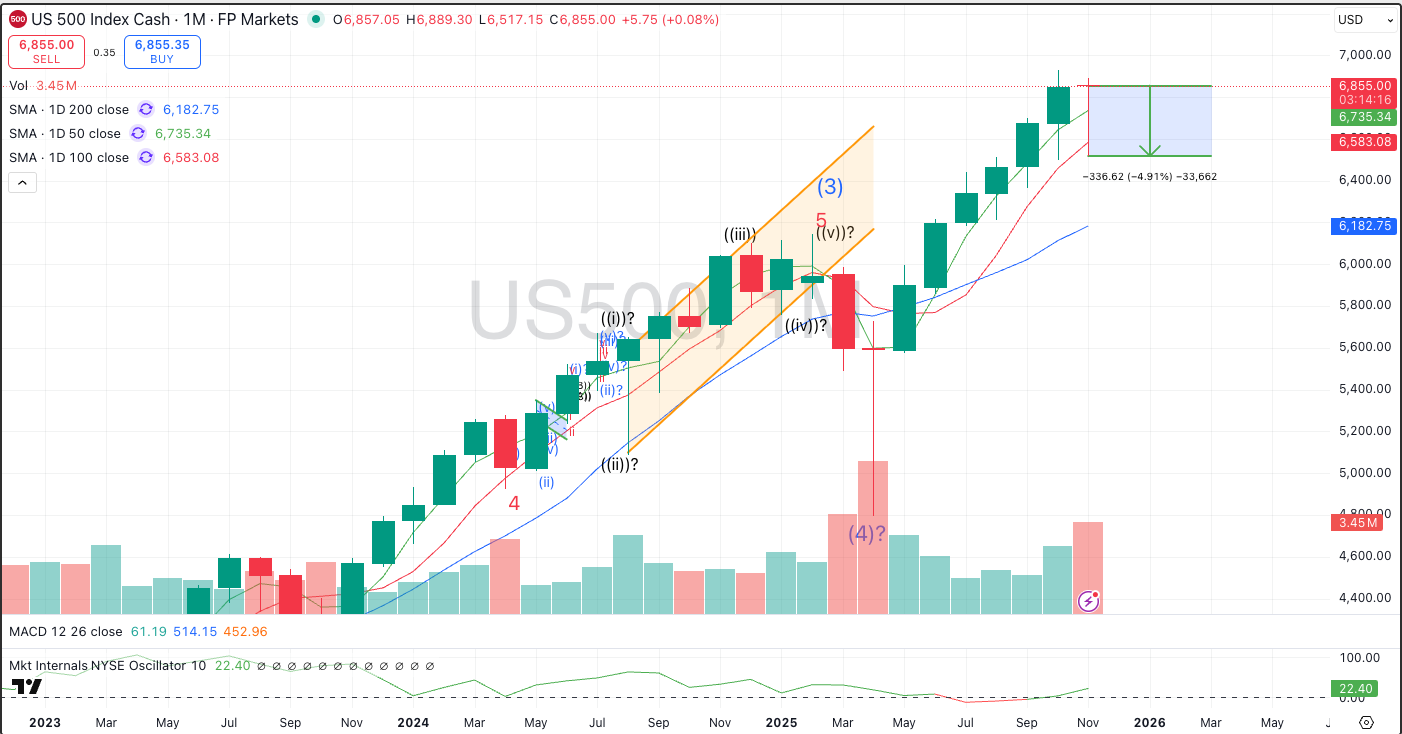

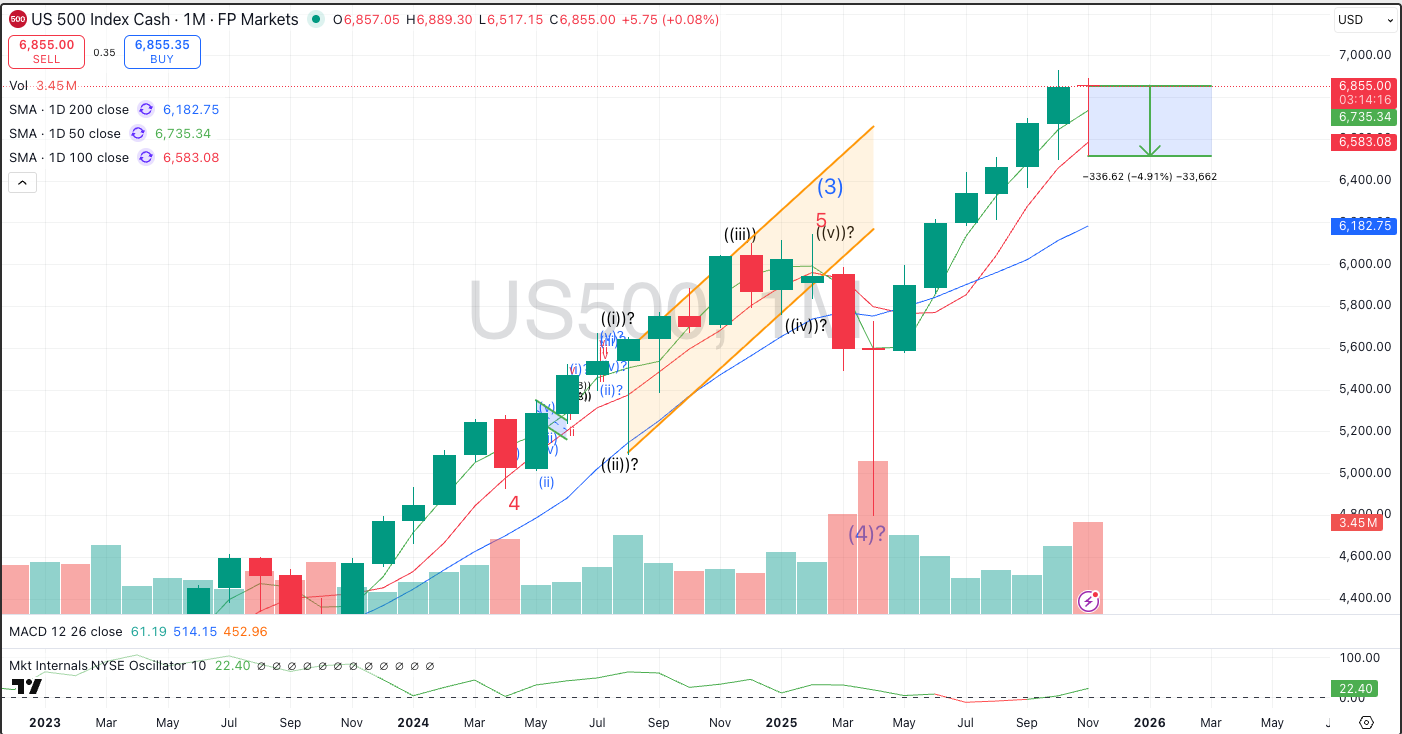

Technical & Sentiment Breakdown: Breadth Thrust, Gamma Shift, and Positioning Reset

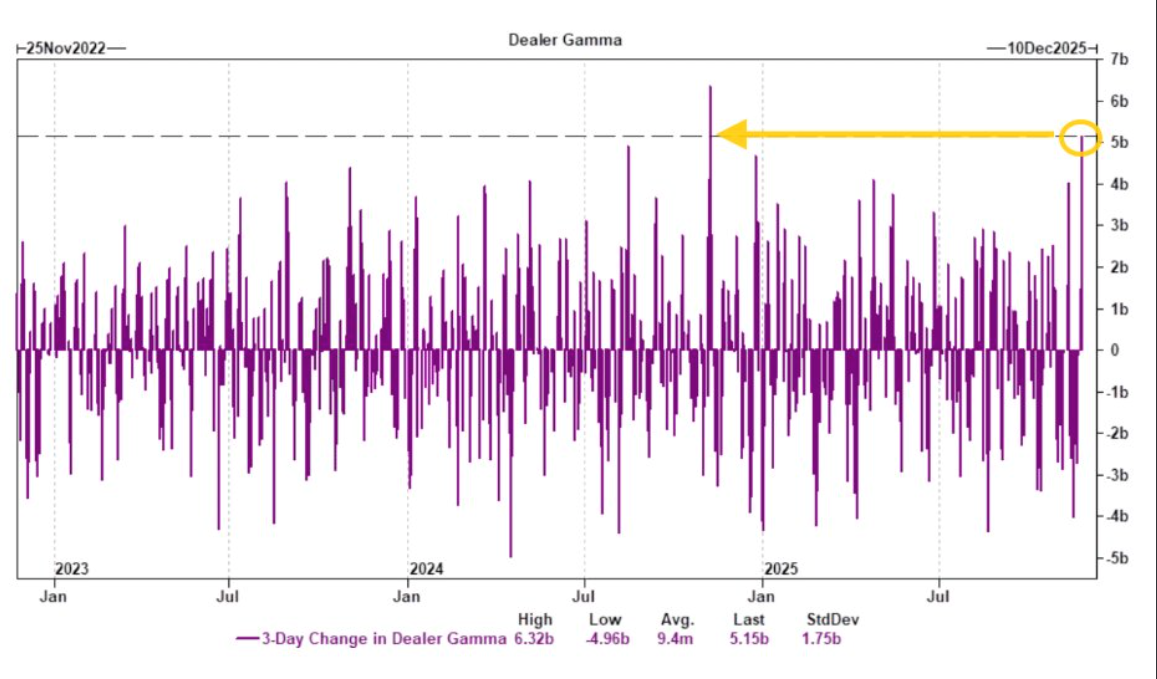

The most important technical development of the week was the structural shift in dealer positioning. Negative gamma that fueled November’s selling unwound into positive territory, stabilising intraday flows.

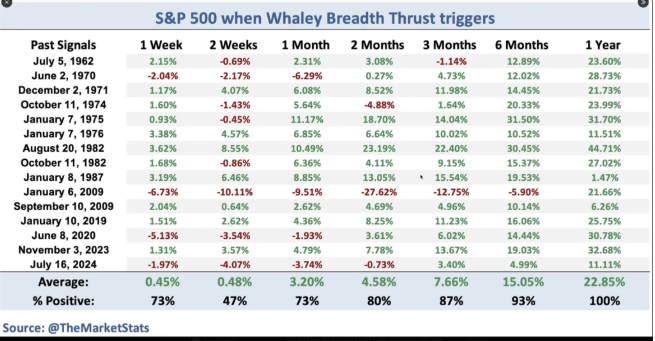

At the same time, a Whaley Breadth Thrust triggered — a rare technical signal that historically precedes strong multi-week and multi-month returns.

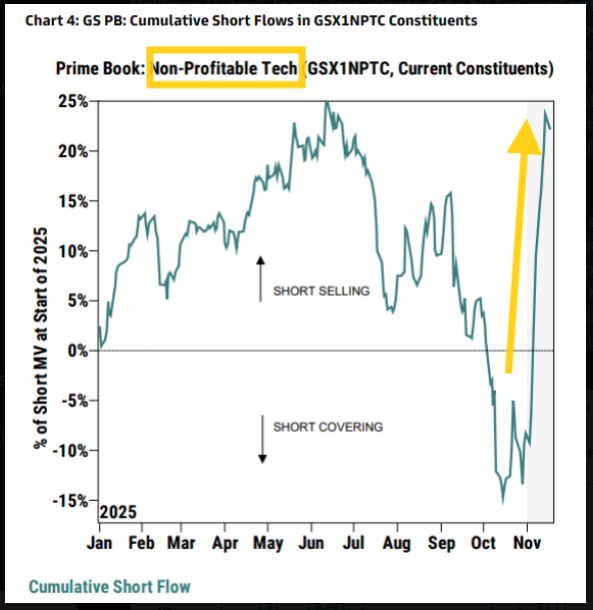

Positioning in unprofitable tech and the most-shorted baskets also showed signs of aggressive unwinds, adding to the upside momentum.

Leverage remains elevated but no longer at extremes, leaving room for further re-risking if momentum holds.

Forward return frameworks in the models remain constructive, with several upside scenarios opening if institutional supply fades and buyers return.

Sentiment has shifted off the lows, but it remains fragile enough that surprises can still produce sharp swings.

Last Week’s Recap: Volatility Crush, Positioning Reset, and Tech Relief

Markets started cautiously but reversed sharply on Friday as gamma flipped positive, Thanksgiving inflows hit, and labour-softening data supported expectations for an imminent policy cut. A crypto-driven wobble midweek didn’t derail the broader rebound, and flows turned decisively supportive for the first time in weeks.

Key Highlights

Macro:

Alternative labour data confirmed accelerating job cuts — Challenger layoffs, WARN notices, and monthly job cuts all surged. The softening backdrop strengthened the probability of an early policy cut as underlying labour momentum weakens.

Flows:

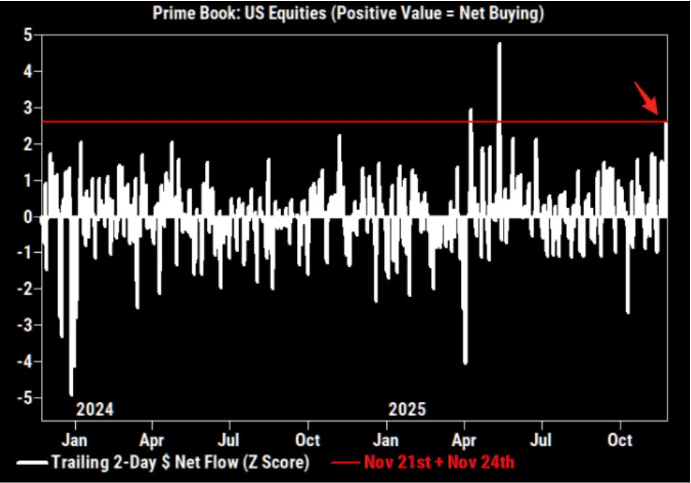

Hedge funds flipped aggressively, buying at the fastest pace since April, while retail outflows from mid-November marked a capitulation low that institutions quickly absorbed.

Tech & Positioning:

Unprofitable tech, one of the most shorted baskets through October–November, saw sharp short-covering as gamma turned positive and flows stabilised. Sentiment toward AI also stabilised after fears of capex displacement eased.

Commodities:

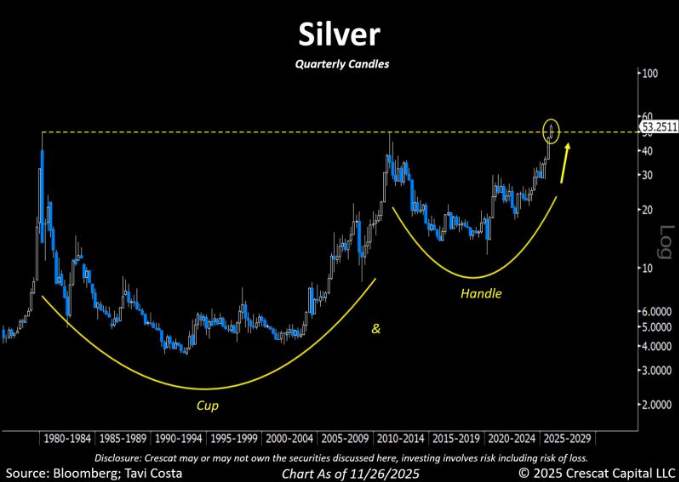

Gold pushed into breakout territory, while silver displayed classic late-cycle strength with physical tightness and multiple timeframe “cup and handle” structures intact.

Crypto:

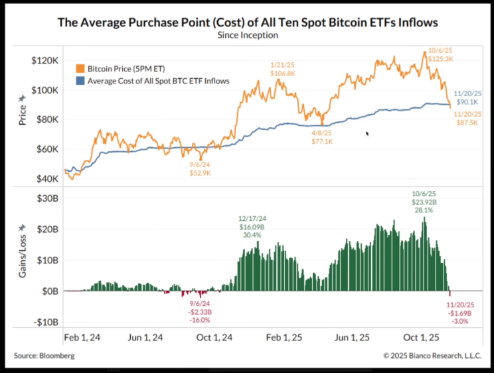

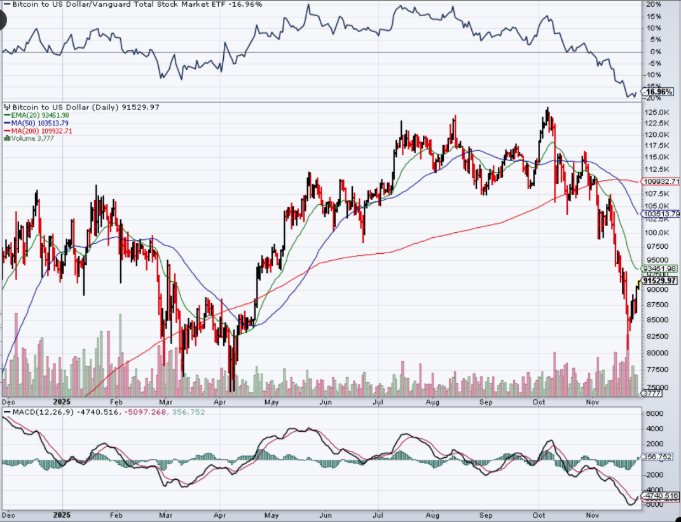

Bitcoin retraced from its V-shaped flush and bounced off ETF demand zones. MACD and RSI stabilised, suggesting bottoming behaviour at the tail end of a capitulation move.

Metals & Cyclicals:

Silver’s backwardation and long-term breakout structure continue to highlight tight supply dynamics, reinforcing the view of a multi-asset bottoming phase.

The Week Ahead: Data Cluster Meets Policy Silence

A dense macro calendar collides with policy blackout conditions, leaving markets driven purely by data and flows. With volatility crushed and positioning light, traders face a potentially choppy but opportunity-rich week.

Monday, Dec 1

Global Manufacturing PMIs

OPEC Meeting

U.S. ISM Manufacturing, Construction Spending

European Retail Sales

Treasury Bill Auctions

Tuesday, Dec 2

Terms of Trade (NZ)

European CPI (Flash)

U.S. JOLTS Job Openings

API Oil Stock Data

10-Year JGB Auction

Wednesday, Dec 3

Global Services PMIs

ADP Employment

ISM Non-Manufacturing

Mortgage Applications

Eurozone PPI

Thursday, Dec 4

Jobless Claims

European Construction PMIs

CAD Trade Balance

U.S. Challenger Job Cuts

Friday, Dec 5

CAD Employment

U.S. PCE Inflation

U.S. Consumer Sentiment

Factory Orders

Tokyo CPI Preview via Global Indicators

Alpha Takeaway: Flows Turned — Now the Test Begins

Liquidity, gamma, and seasonality all shifted bullishly last week, but the setup is still fragile. Labour softens, leverage remains elevated, and any disappointment in this week’s data could quickly challenge the rally. For now, flows dominate — but the window is narrow.

Equities:

Momentum turned constructive as gamma flipped positive. Breadth thrust signals support upside continuation, but any pullback must hold last week’s lows to keep dip-buyers engaged. Program flows favour grind-higher conditions if volatility remains suppressed.

Gold & Silver:

Gold’s breakout structure strengthens as yields soften. Silver continues to outperform late-cycle, with physical tightness and cup-and-handle formations supporting a higher-beta metals move into year-end.

Crypto:

Capitulation appears complete. ETF demand curves acted as support, and MACD crossovers signal early upside momentum. If global liquidity continues improving, crypto could see renewed flows sooner than expected.

Macro:

A policy cut remains increasingly likely as labour data deteriorates. The bigger question is the follow-through — if QT slows and liquidity recirculates, risk assets could stretch higher into December despite macro cracks.

Flows have clearly improved, but with leverage still elevated, the market will need to validate these gains rather than assume stability.