Seasonality Reappears, Disinflation Comforts, and Liquidity Does the Heavy Lifting

Market Overview: Flows Reassert as Seasonality Finds Its Timing

Markets finally found their footing last week after a hesitant start driven by delayed US data releases and a crowded central-bank calendar. Once those hurdles were cleared, price action stabilised and flows reasserted themselves, allowing equities to lean back into year-end seasonality. The rally did not come from fresh macro optimism, but from the removal of uncertainty and the steady bid from positioning and liquidity.

This was not a breakout week — but it was an important one. Inflation data moved in the right direction, labour markets cooled without collapsing, and risk assets were given room to breathe. At the same time, sentiment indicators and flow concentration are becoming harder to ignore, suggesting that while the tape remains supportive, the margin for error is shrinking as we look toward 2026.

Equities spent the early part of the week chopping sideways as markets worked through US catch-up data and multiple central-bank decisions. Once those passed, price action improved meaningfully. Options expiry removed a layer of negative hedging, and market-makers appeared to rebalance risk into year-end rather than press shorts.

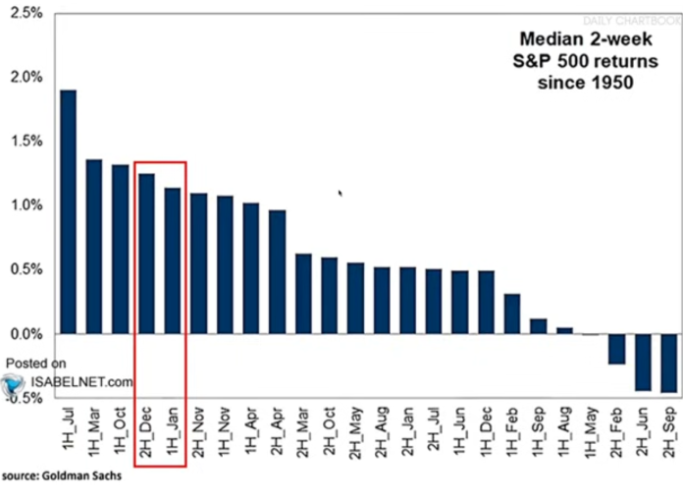

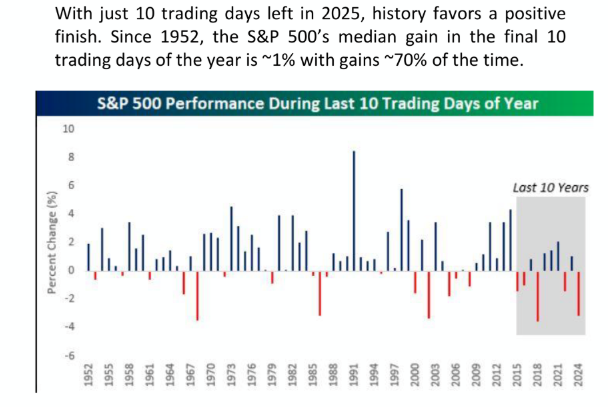

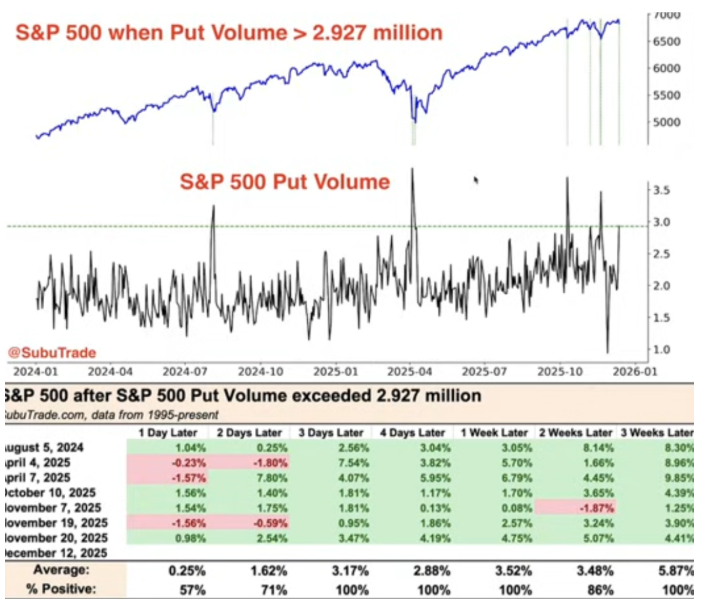

Seasonality is now firmly back in play, with equities entering historically strong periods for performance.

That said, the PDF also highlights that not all Santa rallies are smooth. Late-year strength has, in the past, given way to sharper pullbacks when positioning becomes crowded or liquidity thins too quickly.

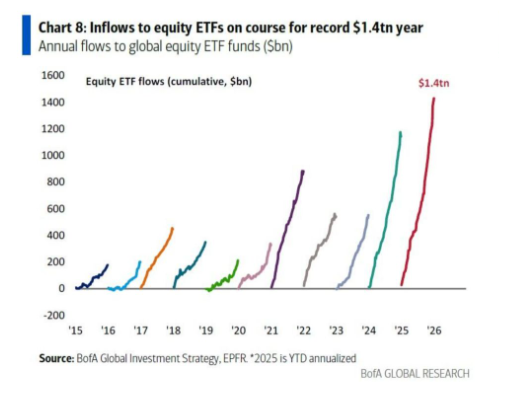

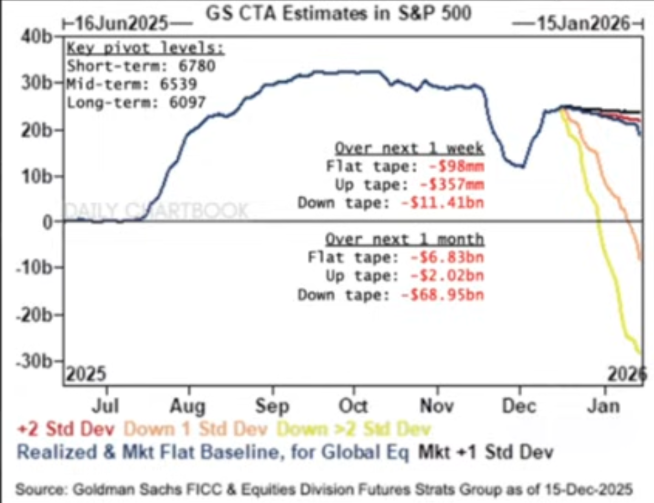

Flows remain the dominant driver. Bank of America data shows one of the largest weekly inflows into equities on record, led overwhelmingly by US stocks and passive vehicles.

Importantly, this is occurring alongside record balances still parked in money-market funds, suggesting redeployment of cash rather than outright speculation. Hedge funds, however, remain persistent sellers on downside moves, reinforcing the idea that this is a flow-driven grind rather than a conviction-led surge.

Macro & Policy Watch: Disinflation Helps, Fiscal Reality Lingers

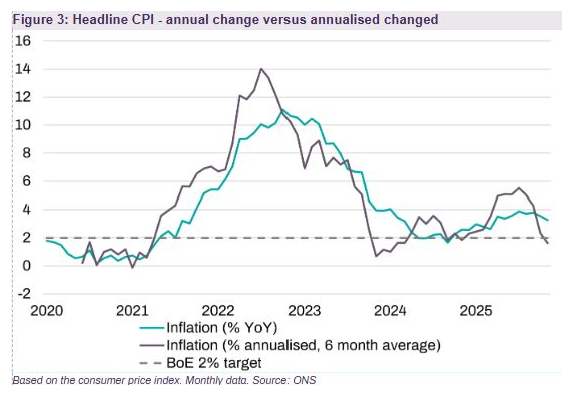

Inflation data continues to move in a favourable direction, particularly when viewed through a smoothed lens. The six-month trend in headline US CPI shows clear disinflationary momentum.

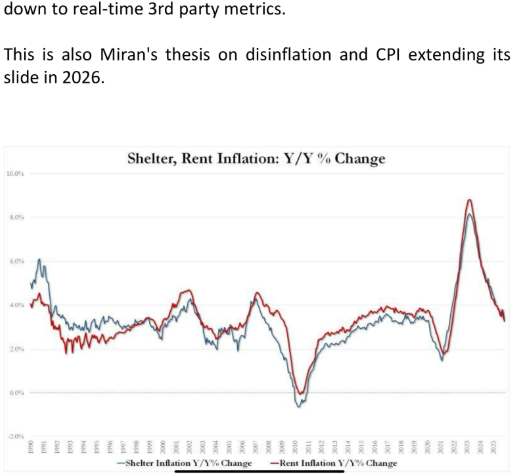

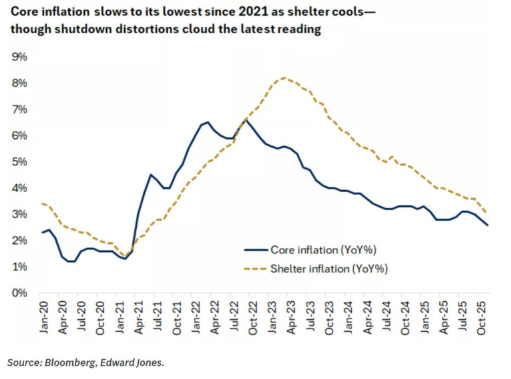

A major driver remains shelter inflation. The PDF repeatedly stresses that the shelter’s statistical lag — combined with its outsized weight in CPI — exaggerated inflation on the way up and is now accelerating the decline.

This supports the near-term easing narrative and helps explain why markets are increasingly comfortable with the idea of lower policy rates. However, the rate picture is complicated by fiscal dynamics. Planned 2026 fiscal programmes continue to pressure the long end of the curve, keeping upward bias in yields even as inflation cools.

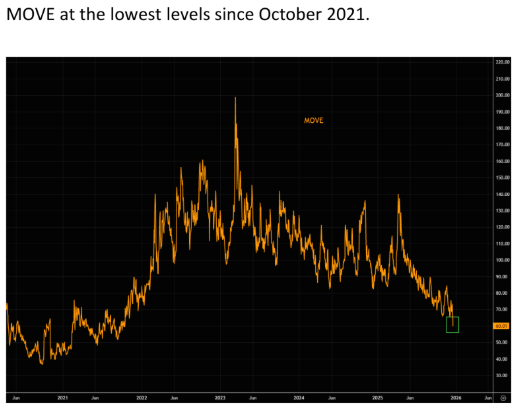

Bond volatility remains unusually subdued, with the MOVE index back near 2021 lows.

The analyst framing is clear: reserve-management operations and quiet balance-sheet support are becoming more important than policy rhetoric. Disinflation helps risk assets for now — but fiscal dominance will shape the next phase.

Technical & Sentiment Breakdown: Support Holding, Leadership Crowding

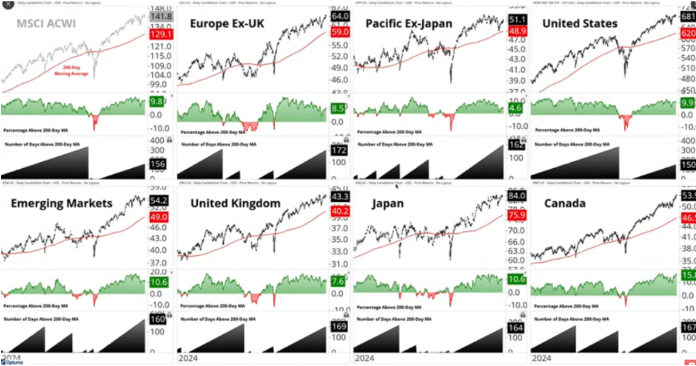

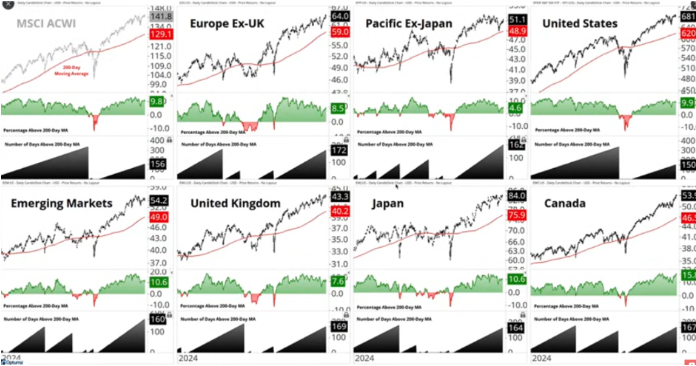

From a technical standpoint, broader indices remain intact, with long-term trends holding and recent consolidation occurring near highs rather than breaking lower. Price action continues to reflect resilience, but it is increasingly uniform across indices, suggesting stability without strong internal momentum.

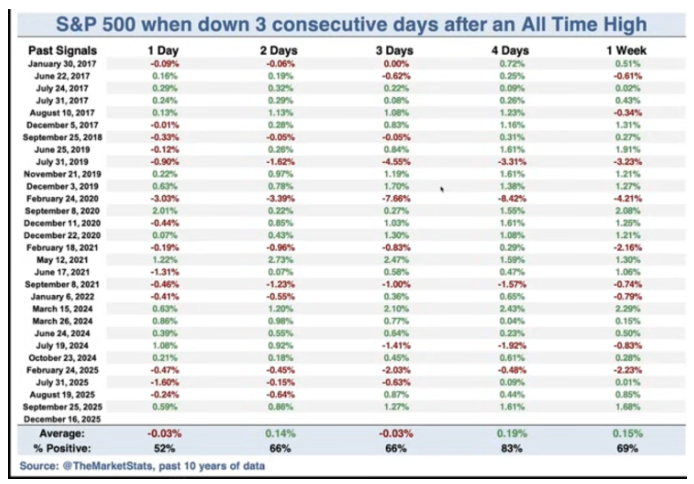

Momentum has moderated meaningfully. The market appears to be transitioning from an explosive advance into a slower, grind-higher phase — still upwardly biased, but far more sensitive to disappointment as marginal buyers become selective.

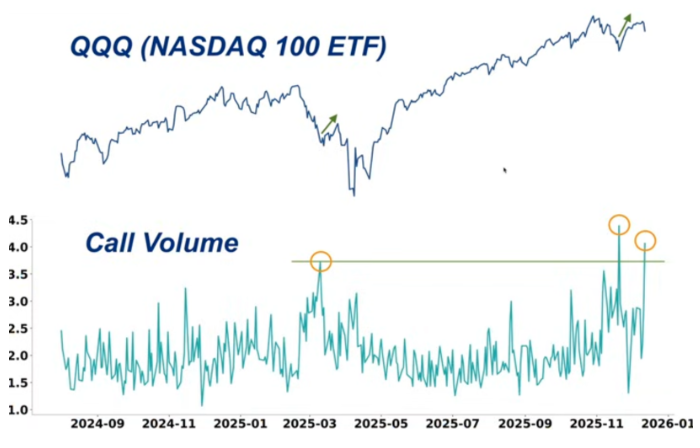

Leadership dynamics remain critical. Options data shows renewed call buying in tech-heavy indices, signalling continued appetite for upside exposure. At the same time, downside protection in the S&P has become elevated enough to act as a short-term contrarian tailwind, suggesting hedging demand may be peaking rather than accelerating.

Rotation beneath the surface continues. Broader participation is helping stabilise indices, but leadership concentration and crowding risks remain evident beneath the headline strength.

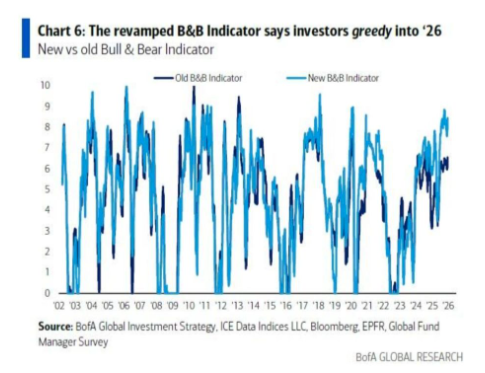

Sentiment, however, is no longer benign. Bank of America’s risk indicators have pushed into elevated territory, a condition historically associated with choppier forward returns rather than clean upside continuation.

This is a market still supported by structure — but increasingly unforgiving of crowded positioning and sentiment excess.

Last Week’s Recap: Data Catch-Up, Central Banks, and Flow Relief

Markets began the week cautiously as investors worked through delayed US data and a heavy slate of central-bank decisions, but stabilised into Friday as inflation prints softened, tech fears eased, and year-end flows reasserted themselves.

Key Highlights:

Macro:

US inflation data continued to move in the right direction, with shelter components finally reflecting real-world rental declines. The lagged nature of shelter inflation and its heavy CPI weighting — dragged headline prints lower, reinforcing the disinflation narrative and easing pressure on risk assets.

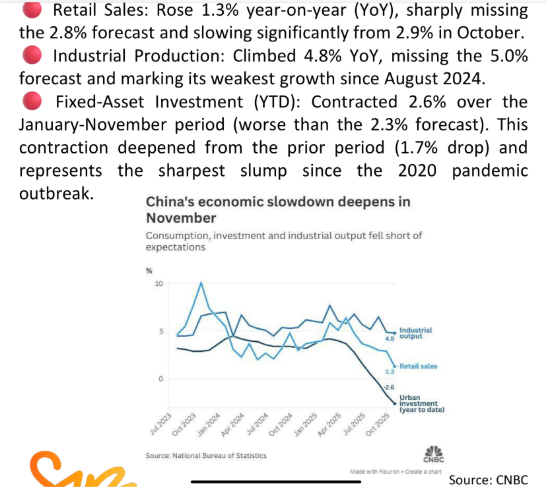

China:

Chinese data remained soft, with retail sales and domestic demand underscoring the fragility of the consumer. Fixed asset investment continues to disappoint, and while policy support is being delivered, it remains targeted and slow to gain traction.

Earnings:

Tech sentiment stabilised following Micron’s update, which helped soothe concerns around near-term demand and capital-expenditure visibility. While earnings season is thinning into year-end, leadership reassurance proved important in restoring confidence.

Commodities:

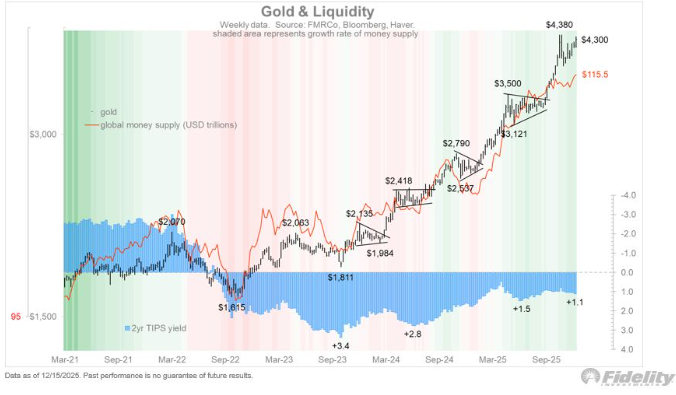

Precious metals continued to push higher, with gold, silver, and platinum extending gains as liquidity expectations and debasement narratives stayed firmly in place.

Crypto:

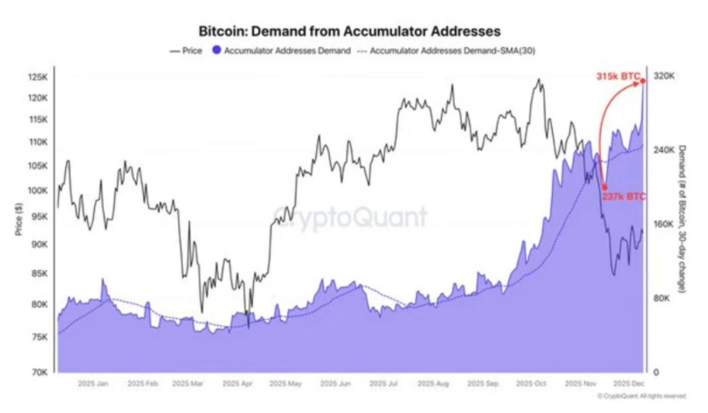

Volatility earlier in the week looked increasingly like a positioning shakeout. Flows stabilised into the end of the week, with signs that larger participants were accumulating rather than distributing.

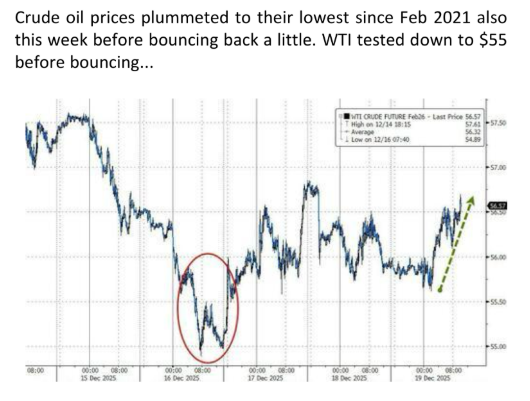

Oil:

Energy prices remained capped, with sentiment still leaning bearish. Positioning looks vulnerable; however, should supply dynamics tighten or broader reflation narratives regain momentum.

The Week Ahead: Holiday Liquidity, GDP Focus, and Inflation Follow-Through

This is a shortened holiday week with thinning liquidity, increasing the risk that even routine data surprises produce outsized market reactions. With major central-bank decisions behind us, focus shifts to US growth confirmation, inflation follow-through, and Japan inflation signals, all against a quieter but more fragile year-end tape.

Monday, Dec 22

- CNY: One-Year & Five-Year Loan Prime Rate (LPR)

- GBP: Q3 GDP (Final), Current Account

- USD: Core PCE (MoM, YoY)

- USD: Personal Income & Personal Spending

- USD: Dallas Fed PCE

Tuesday, Dec 23

- JPY: Core CPI (YoY)

- USD: GDP (Q3), Core PCE Prices (Q3), Corporate Profits

- USD: Atlanta Fed GDPNow (Q4 – first estimate)

- USD: Consumer Confidence

Wednesday, Dec 24 (Markets Close Early)

- USD: Initial & Continuing Jobless Claims

- USD: Crude Oil Inventories

- USD: Mortgage Applications

Thursday, Dec 25 (Christmas Day – Markets Closed)

- JPY: Tokyo CPI (Headline, Core)

- JPY: CPI ex-Food & Energy

- JPY: Unemployment Rate

- JPY: Industrial Production (MoM)

- JPY: Retail Sales (YoY)

Friday, Dec 26 (Boxing Day – US Markets Open)

- USD: Thin liquidity — focus on flows and positioning

Alpha Takeaway: Supportive Tape — But Crowding Is the Risk

Markets are benefiting from a rare alignment of disinflation relief, seasonal tailwinds, and powerful passive flows. That combination is supporting risk assets into year-end — but it is also compressing forward returns and raising sensitivity to positioning extremes.

Equities:

The structure remains constructive, with indices holding key trends and flows that provide support. However, sentiment is stretched, and upside is increasingly dependent on rotation rather than broad multiple expansion.

Gold & Silver:

The structural case remains intact as liquidity expectations and debasement themes persist. Pullbacks appear more corrective than terminal, although near-term consolidation would be healthy following recent gains.

Crypto:

Stabilisation is encouraging following recent volatility. Any renewed upside remains tied to liquidity conditions and broader risk appetite rather than idiosyncratic catalysts.

Macro:

Disinflation is easing pressure on policy, but fiscal dynamics and bond-market behaviour will increasingly dictate conditions in 2026. Real rates — not just rate cuts — remain the key variable.

Flows are still carrying the market — but crowded trades unwind quietly before they unwind violently. Participate, but stay nimble.