Physical Stress Surfaces, Liquidity Carries the Tape, and Markets Drift Into Year-End

Market Overview: Structure Holds as Flows Do the Heavy Lifting

Markets moved through the final full trading week of the year with little urgency but plenty of signals. Liquidity remained thin, conviction was limited, and yet price action held together far better than sceptics expected. This was not driven by fresh optimism or new macro clarity, but by structure, positioning, and the continued absence of forced selling.

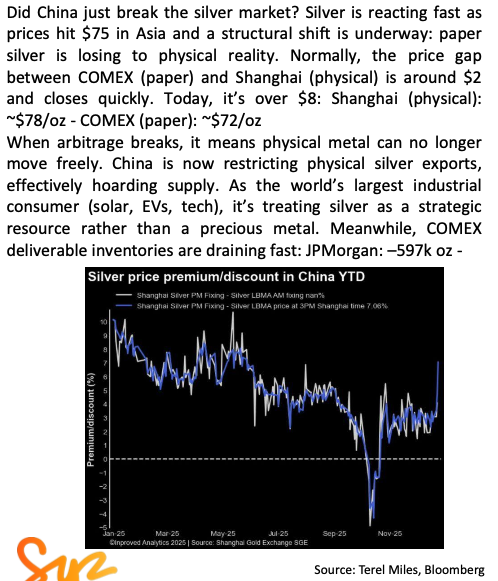

Beneath the surface, however, pressure is quietly building. Physical markets—particularly in metals—are flashing stress signals that paper systems cannot indefinitely smooth over. Stress in physical markets suggests increasing tension between paper pricing and real-world settlement as the year closes.

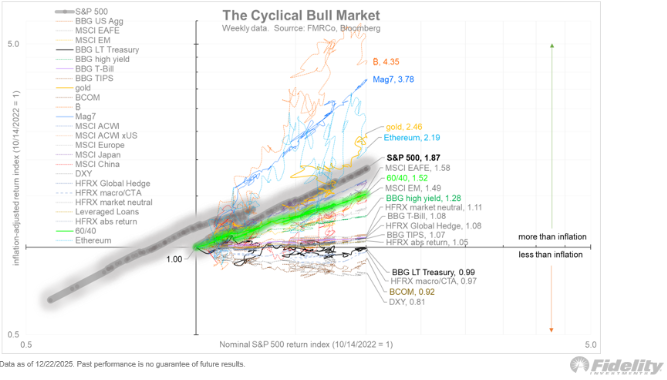

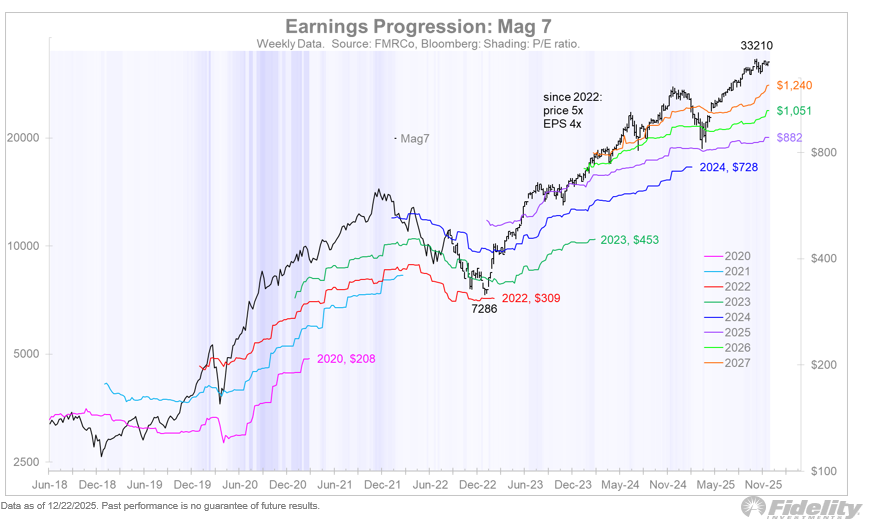

Equities continue to grind higher into year-end, supported by a structural rather than an enthusiastic backdrop. The rally from the October 2022 lows remains intact, and this cycle has been driven by earnings growth rather than indiscriminate multiple expansion.

That distinction matters. As long as earnings continue to justify prices, equity indices will continue to attract flows. Breadth has improved meaningfully, with a healthy proportion of stocks trading above short- and medium-term moving averages.

However, longer-term breadth remains less convincing. The percentage of stocks above the 100- and 150-day averages has not yet confirmed a decisive breakout, reinforcing the idea that this is persistence rather than acceleration.

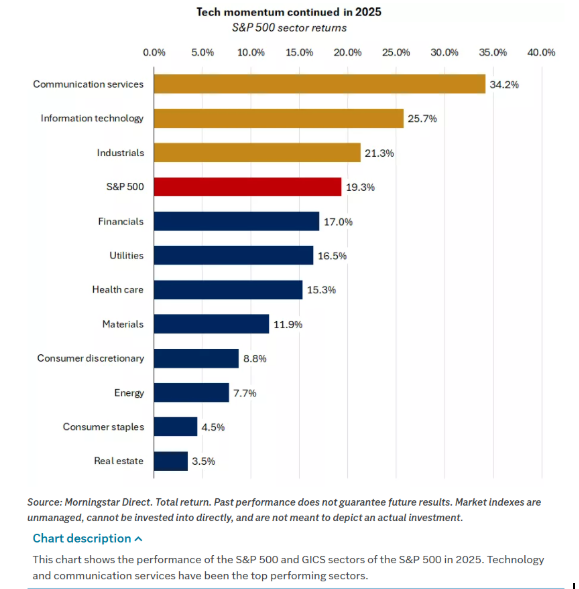

Rotation continues to play an important role. The Dow's leading relative performance suggests ongoing interest in health care, financials, and energy rather than a narrow, growth-only rally.

Play momentum, not laggards. This is not the phase of the cycle where mean-reversion trades are being rewarded.

Macro & Policy Watch: Liquidity Is Plentiful, Growth Is Not

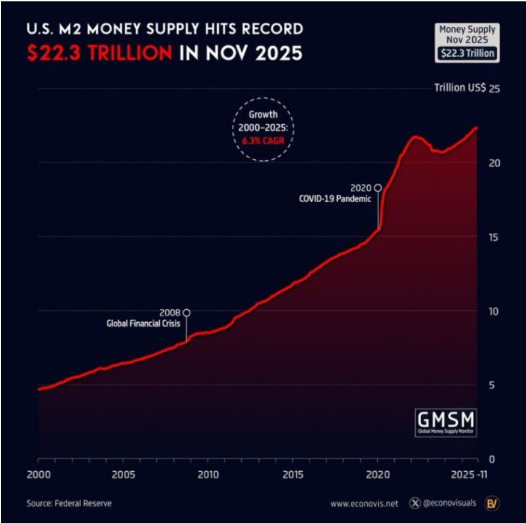

Macro conditions remain defined by contradiction. Liquidity is abundant—globally and persistently—but it is not translating cleanly into productive growth. Money supply continues to expand far faster than GDP, implying dilution rather than expansion.

Crucially, this does not automatically mean financial conditions are expansionary. Much of this liquidity appears to be hoarded, recycled, or used defensively rather than deployed into growth-enhancing investment.

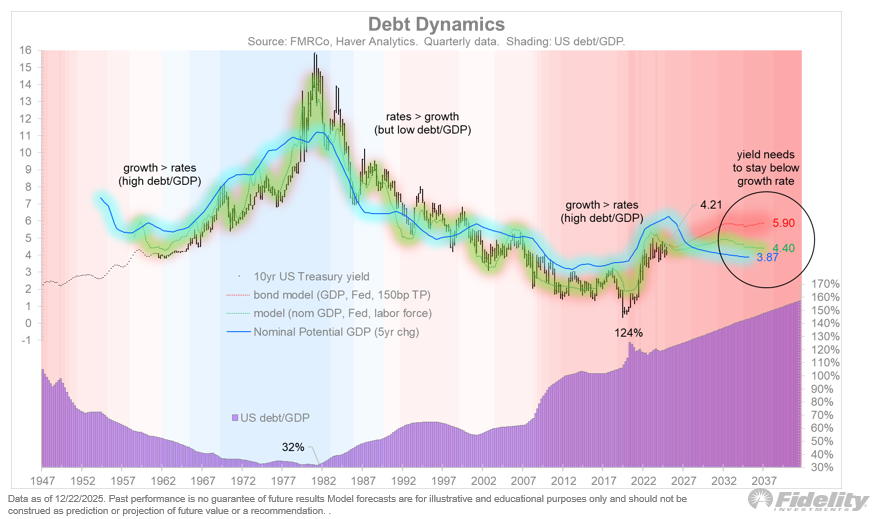

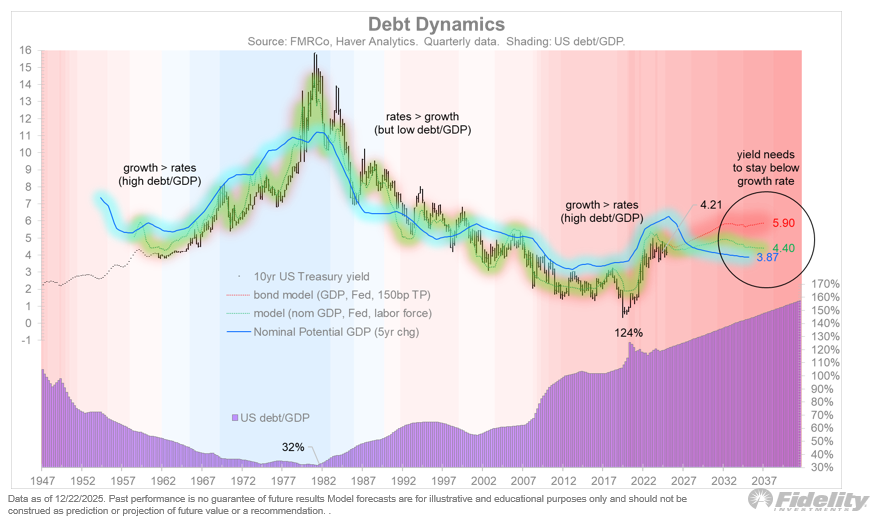

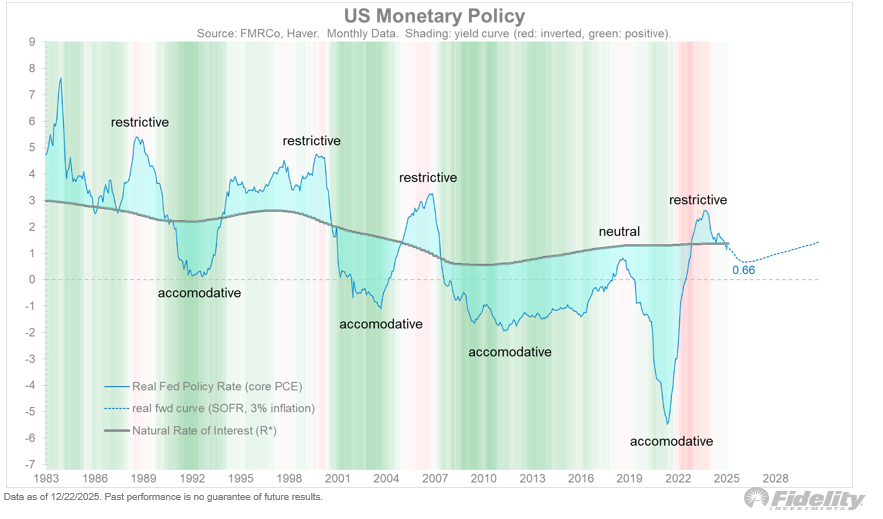

Governments themselves are losing purchasing power, reinforcing why markets are bidding up scarce and real assets. Rates sit close to neutral, but history suggests neutrality rarely lasts long. When long-dated yields sit above nominal growth—particularly with elevated debt levels—stress eventually shows up in servicing costs and policy pressure.

Looking ahead, the debate is less about rate cuts already delivered and more about whether yields can be controlled without reigniting inflation. That tension will define 2026.

Technical & Sentiment Breakdown: Supportive, but Increasingly Fragile

From a technical standpoint, the structure remains intact. Pullbacks have been shallow, consolidation has occurred near highs, and broader trends have not broken. However, momentum has slowed, and price action feels more sensitive to disappointment.

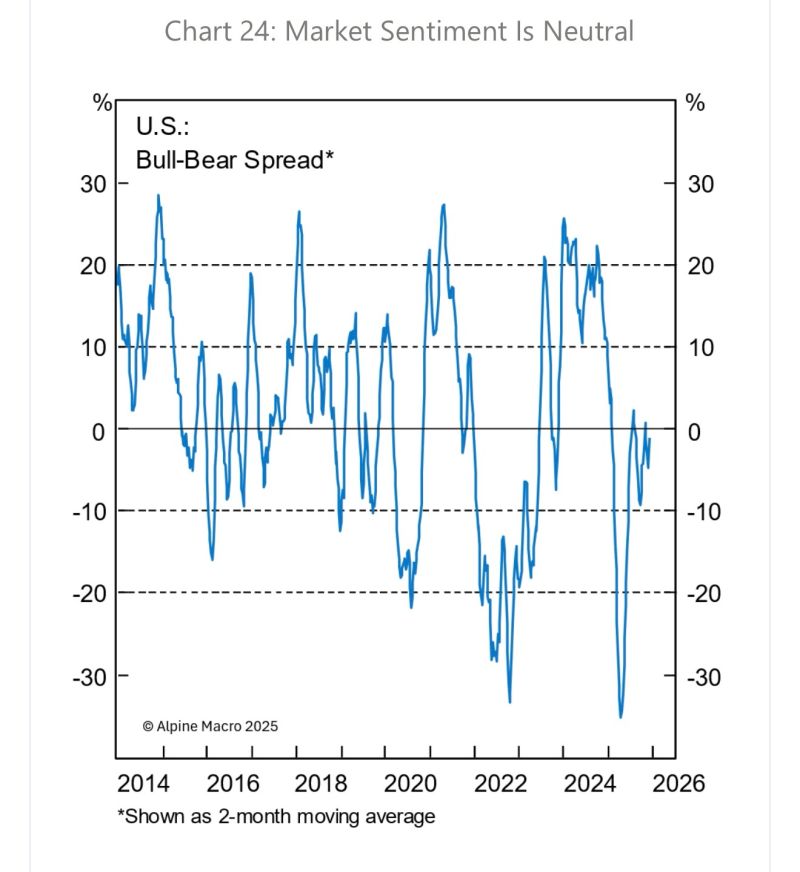

Sentiment captures that unease. Indicators sit close to neutral—neither pessimistic enough to trigger capitulation nor complacent enough to justify aggressive risk-taking.

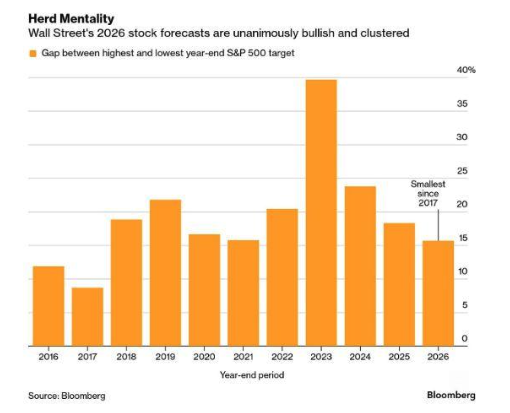

Groupthink is becoming more evident. Expectations cluster around “smaller upside, but still upside,” a condition that often masks the potential for sharper swings in both directions.

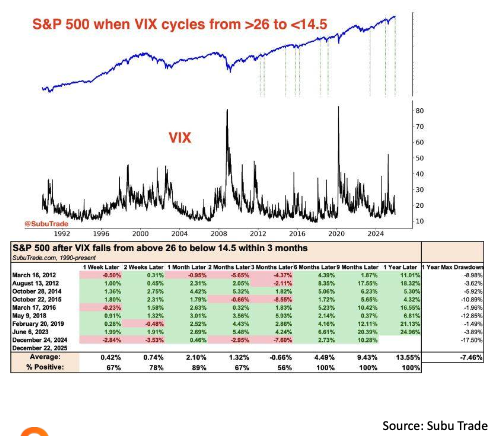

Volatility remains suppressed, which historically supports equity drift, but timing matters. Low volatility into year-end often delays adjustment rather than eliminating it.

Positioning and sentiment conditions suggest asymmetric outcomes around disappointment rather than broad upside expansion.

Last Week’s Recap: Liquidity Stress, Metals Signal, and Growth Reality

Markets started the week quietly but firmed into the close as structural flows dominated thin liquidity. With limited headline data, underlying stresses became more visible.

Key Highlights:

Macro:

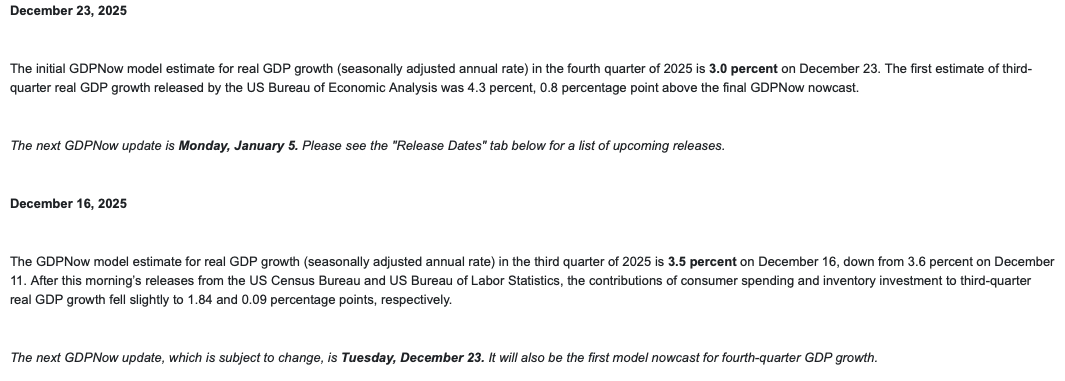

US GDP surprised to the upside, but this strength largely reflects backwards-looking data. Shutdown distortions are expected to weigh on Q4 estimates, with forward growth already softening. Housing data continues to show how aggregates mask sharp divergences beneath the surface.

China:

Physical demand from China remains a central theme, particularly in commodities. Silver demand continues to bypass Western paper markets, reinforcing the divergence between Shanghai pricing and COMEX structures.

Earnings:

Earnings remain the backbone of the equity rally. The post-October 2022 advance has been earnings-led, and until that changes, equities are likely to retain structural support.

Commodities:

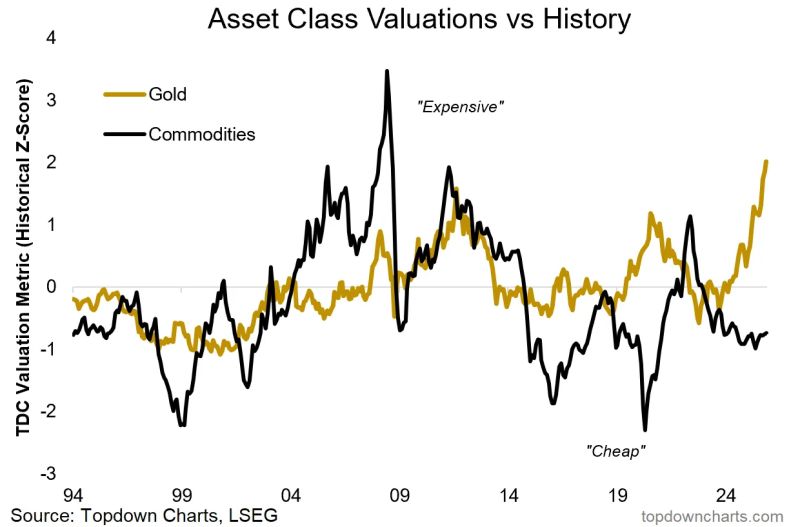

Gold continues to act like a zero-coupon bond in a world where long-dated fixed income no longer offers safety. Silver stood out as physical stress intensified, with backwardation and delivery premiums signalling distrust of paper settlement.

Crypto:

Crypto volatility increasingly resembles a positioning shakeout rather than a trend reversal. Consolidation has tested conviction, but belief in the asset class is being challenged rather than abandoned.

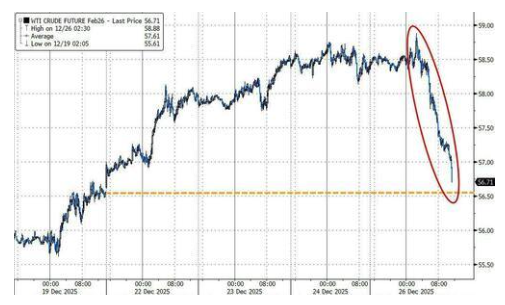

Oil:

Energy remains capped by sentiment, but growing geopolitical optionality is becoming harder to ignore. With positioning negative, it would not take much to trigger a reflexive move higher.

The Week Ahead: Holiday Liquidity and Key Macro Signals

The final week of the year remains dominated by holiday conditions and thin liquidity. With US equity markets largely quiet and many global venues closed or operating on reduced hours, price action is likely to be driven more by flows and funding dynamics than by headline data. Still, a handful of macro releases and central-bank communications could matter, particularly where they intersect with liquidity, housing, and inflation expectations.

Monday, December 29

- U.S.: Pending Home Sales (MoM, Nov)

- U.S.: Dallas Fed Manufacturing Index

- U.S.: Crude Oil Inventories

- Japan: BoJ Summary of Opinions

Tuesday, December 30

- Eurozone: Core CPI (Dec)

- Spain: CPI (Dec), Retail Sales (Nov)

- U.S.: House Price Index (Oct)

- U.S.: FOMC Meeting Minutes

Wednesday, December 31

- China: Manufacturing & Non-Manufacturing PMI (Dec)

- U.S.: Initial & Continuing Jobless Claims

- U.S.: Chicago PMI (Dec)

- Global: Multiple market holidays and early closes

Thursday, January 1

- Global: New Year’s Day — major markets closed

Friday, January 2

- U.S.: S&P Global Manufacturing PMI (Dec)

- Eurozone: Final Manufacturing PMIs

- U.K.: Nationwide House Price Index

- U.S.: Fed Balance Sheet & Reserve Balances

Alpha Takeaway: A Grind Higher, With Cracks Beneath

Markets are ending the year supported, but uneasy. Liquidity and structure are carrying risk assets, yet trust in paper systems is being quietly tested.

Equities:

Structure remains constructive, and earnings continue to do the heavy lifting. Upside persists, but it is increasingly selective rather than broad-based.

Gold & Silver:

Gold continues to benefit from falling trust in long-dated bonds. Silver’s move is more structural, driven by physical scarcity and delivery stress rather than speculative froth.

Crypto:

Belief is being tested, not broken. Consolidation may persist, but volatility is likely before clarity emerges.

Macro:

Liquidity is abundant, but growth is lagging. Debt dynamics, yield control, and fiscal reality—not policy soundbites—will shape conditions in 2026.

This still feels like a grind higher—until it doesn’t. Flows decide direction, but crowded trades unwind quietly before they unwind violently. Participate, but stay nimble.