Liquidity Stabilises, Macro Signals Split, and Markets Brace for a Defining Fed Week

What started as another shaky December stretch — weighed down by crypto volatility, liquidity distortions, and geopolitical rumblings — ended with markets showing notable resilience. Forced liquidations faded, Treasury settlement pressures eased, and flow dynamics turned supportive again. Despite softening in smaller-business labour data and mixed macro signals, equities clawed back higher as volatility collapsed and positioning normalised.

Yet, beneath the surface, the market tone remains fragile. The LEI/CEI recession signal has slipped into levels historically associated with downturns, the crypto structure remains unstable, and global policy paths have begun to diverge. With a pivotal FOMC week approaching, traders find themselves balancing early-December chop against rising seasonal tailwinds — particularly the long-observed post–Day 11 Santa impulse.

Market Overview: Stabilisation Through Flows, Not Fundamentals

The stabilisation last week came almost entirely from flows rather than macro improvement. Crypto was hit hardest, pressured by structural liquidity issues and regulatory developments in China, while concerns around the JPY carry trade resurfaced after Japanese long-end yields climbed on potential BOJ tightening signals.

Still, equities held firm. Breadth improved meaningfully, with more SPX components trading above key moving averages — a welcome reversal after November’s grind lower.

Institutional and retail flows also returned, even as hedge funds remained hesitant. This divergence has become a defining feature of late-2025 trading: cautious hedge funds versus opportunistic retail/institutional inflows.

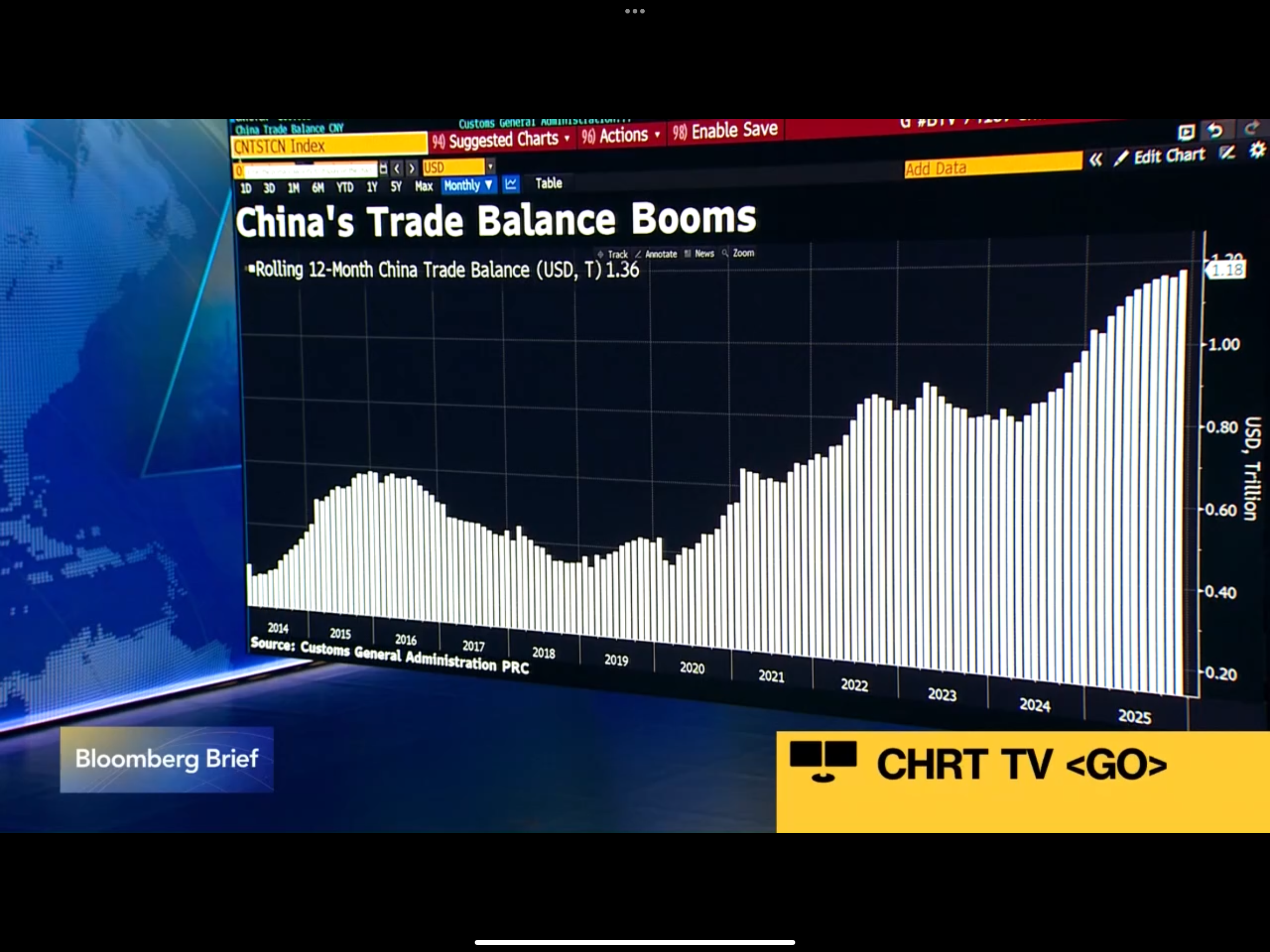

Meanwhile, China posted a record trade surplus, an early sign that global deflationary forces may intensify into 2026. This spillover helped ease input-cost pressures and offered a mild boost to global risk sentiment.

The week’s message was simple: the market isn’t celebrating macro improvement — it’s stabilising because positioning reset and flows turned supportive.

Macro & Policy Watch: Flat Labour, Recession Signals, and Global Policy Divergence

Labour Market: Weak Under the Surface, But Not Collapsing

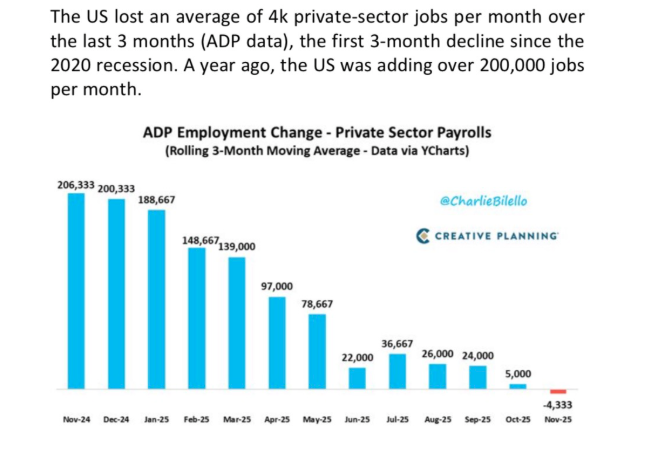

ADP data suggests continued softening, especially among smaller firms. The trend supports the analyst’s view that labour is weakening gradually rather than cyclically breaking down.

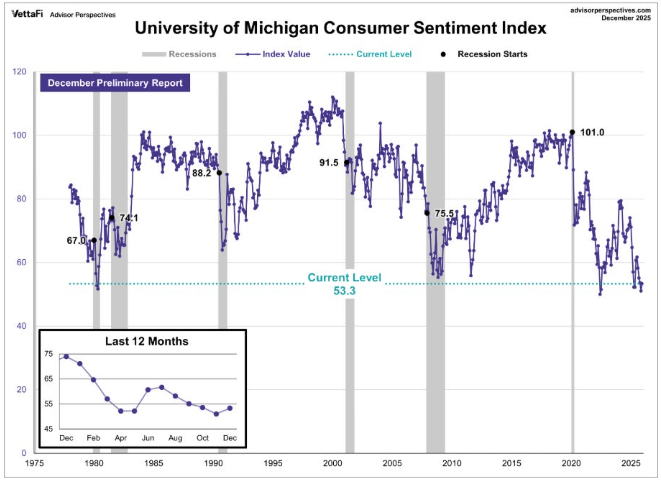

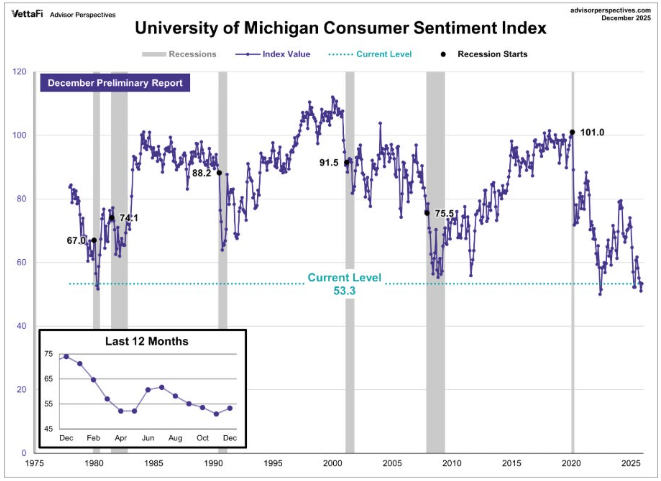

At the same time, consumer sentiment indicators show signs of bottoming rather than deteriorating.

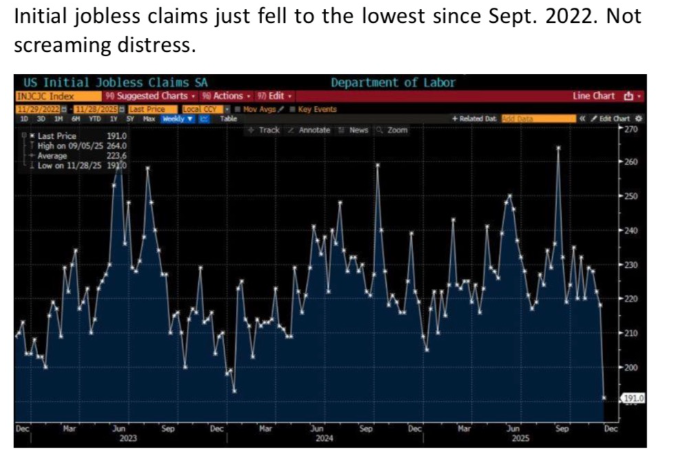

Initial jobless claims moved lower — the best levels since 2022 — contradicting recession-imminent narratives driven by online commentary.

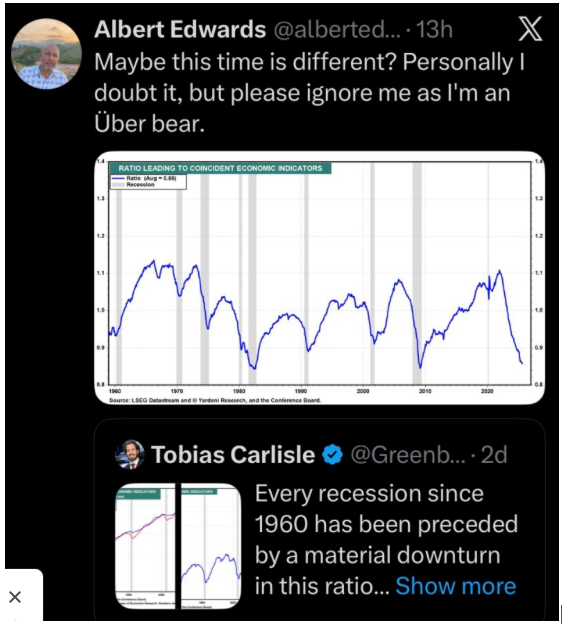

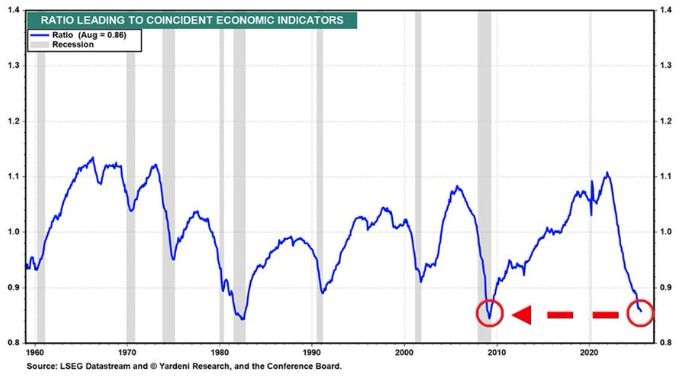

The LEI/CEI Warning

One of the strongest recession indicators flashed again: the LEI/CEI ratio fell to 0.86, entering a zone historically linked with recessions going back six decades.

This has now become one of the key macro charts the analyst is watching into early 2026.

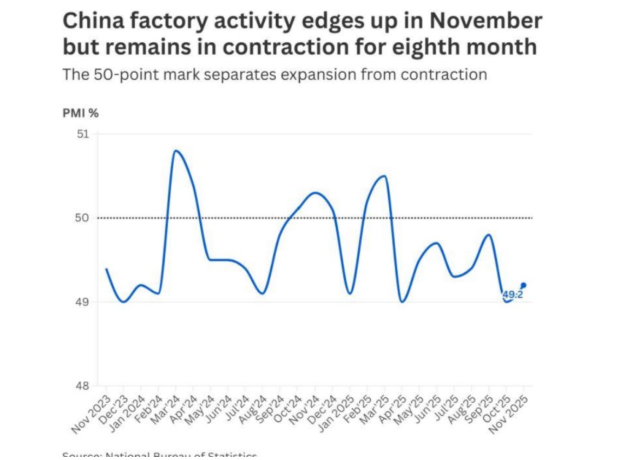

China’s Complex Bottom

China’s factory activity shows tentative signs of firming — a potential early-cycle stabilisation.

Combined with deflationary export momentum from its record surplus, China becomes a quiet macro wildcard — both a support for global disinflation and a potential driver of industrial sentiment.

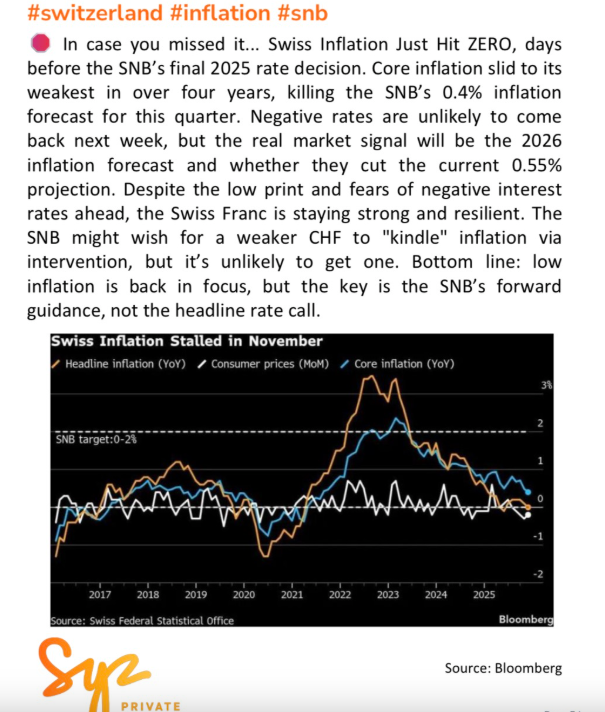

Europe Turns Hawkish

The ECB signalled a surprisingly hawkish stance, noting that future moves could include rate hikes, even as Switzerland posted near-zero inflation — the lowest in years.

The result is a global macro landscape dominated by contradictions ahead of the FOMC.

Technical & Sentiment Breakdown: Pre-Santa Chop Meets Flow Support

Technical conditions improved meaningfully, though they remain short-term choppy.

Broad-market internals strengthened as cyclicals, tech, and defensives all participated in the rebound. SPX positioning models showed a gradual shift back toward neutral-bullish territory.

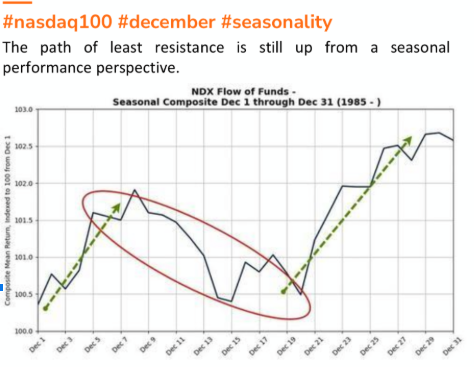

Nasdaq 100 enters one of its best seasonal windows of the year — the mid-December momentum phase.

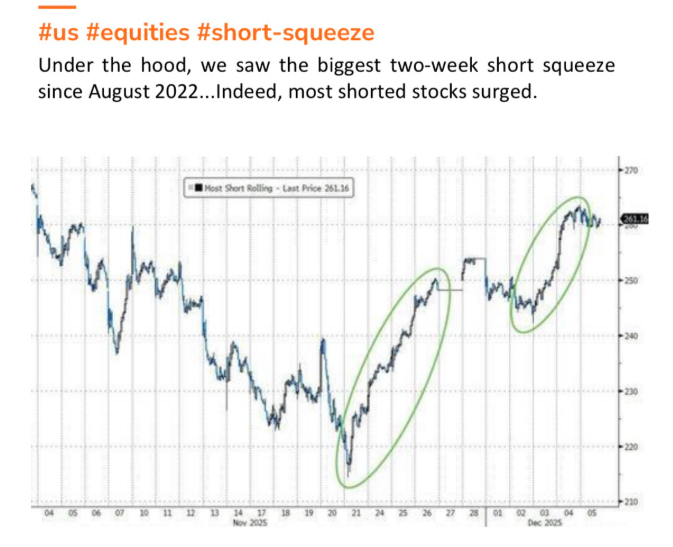

Short-interest baskets bounced as covering accelerated, signalling improved risk appetite across weaker pockets of the market.

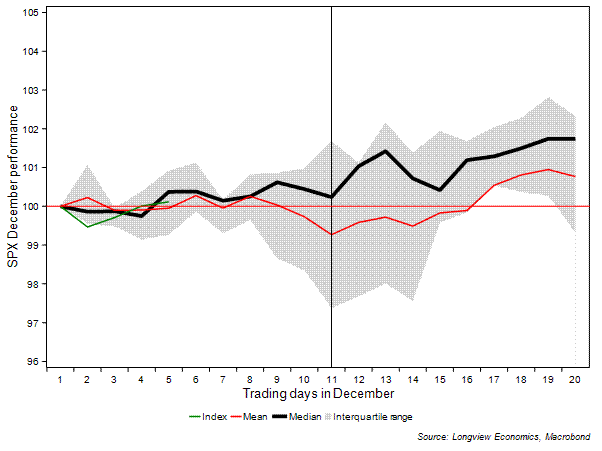

Seasonality models continue to highlight Day 11 of December as the key inflexion point for historically reliable upside follow-through.

The analyst’s view: the next few days may remain noisy, but the broader structure ahead of mid-December looks supportive.

Last Week’s Recap: Labour Softness, Crypto Stress, and Internal Stabilisation

Markets kicked off on unstable footing as crypto liquidations, Treasury settlement pressures, and mixed macro data dragged risk lower. But as the week progressed, flows stabilised, volatility collapsed, and improving internals helped equities regain their footing into Friday.

Key Highlights

Macro:

Labour remained soft beneath the surface, with ADP signalling continued slowing among smaller firms. Sentiment indicators showed tentative signs of bottoming, while jobless claims surprised by dropping to their lowest since 2022.

China:

Factory activity displayed early signs of improvement, while the record trade surplus reinforced China’s growing deflationary impact on global markets.

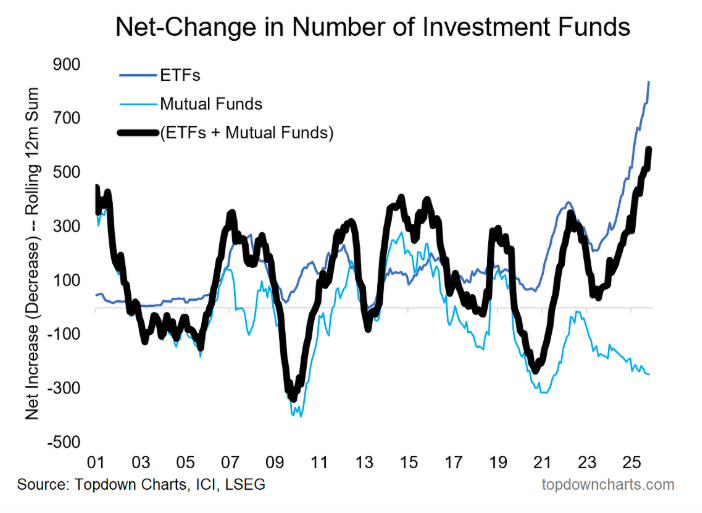

Flows:

Positioning improved as retail and ETFs absorbed supply. Institutional flows stabilised, while hedge funds remained cautious but no longer aggressively risk-off.

Commodities:

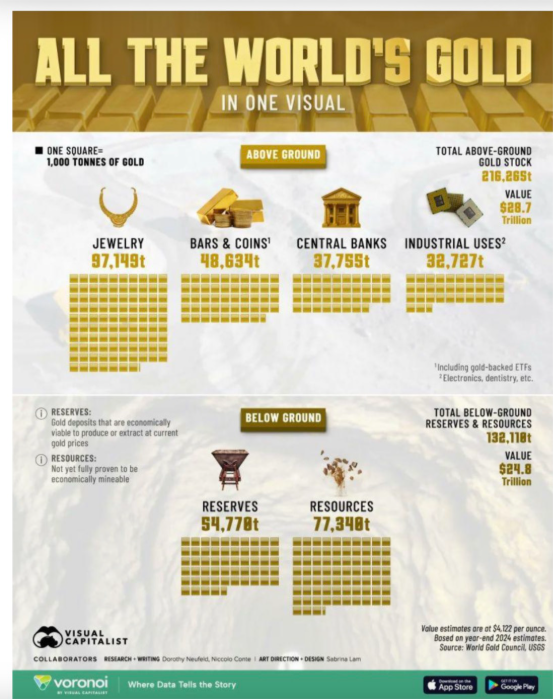

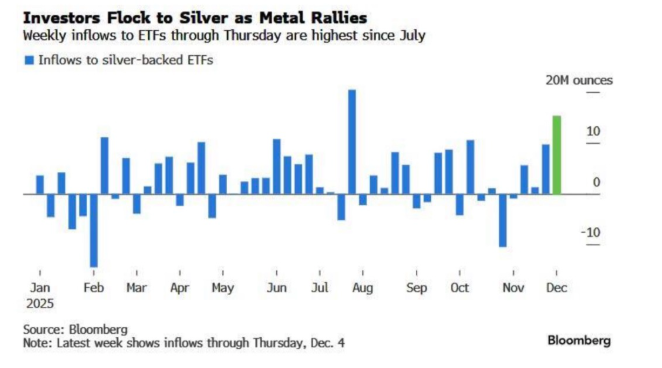

Gold’s structural bullish setup remains intact, supported by constrained supply dynamics. Silver continued to reflect tight conditions across physical markets.

Crypto:

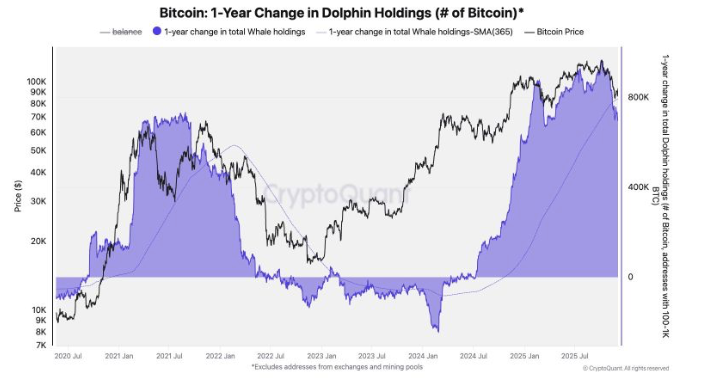

Bitcoin faced another wave of structural volatility as “dolphin” wallets (100–1,000 BTC) sharply reduced accumulation — a key behavioural shift among mid-sized holders. Liquidity issues, not fraud, were behind the move.

The Week Ahead: FOMC, Inflation, and a High-Stakes Policy Cluster

A heavyweight macro calendar collides with one of the most pivotal policy weeks of Q4. With volatility suppressed and positioning light, traders face a window where data surprises and policy tone could quickly reprice risk assets.

Monday, Dec 8

Japan: GDP, Wages

China: Trade Balance, Exports

Germany: Industrial Production

Switzerland: SECO Consumer Climate

U.S.: Treasury Bill Auctions

Tuesday, Dec 9

RBA Rate Decision

Eurozone & German Trade Data

NFIB Small Business Optimism

U.S. JOLTS Job Openings

API Oil Stock Data

10-Year U.S. Note Auction

Wednesday, Dec 10

U.S. CPI

FOMC Rate Decision, SEP, Dot Plot

BoC Rate Decision

Crude Oil Inventories

U.S. Federal Budget Balance

Thursday, Dec 11

SNB Rate Decision

Eurogroup Meeting

U.S. Jobless Claims

Canada: Trade Balance

OPEC / IEA Monthly Reports

Friday, Dec 12

Global PMIs (U.S., EU, Japan, China)

U.K.: GDP

Eurozone: CPI for major regions

China: M2, TSF, Loan Growth

Alpha Takeaway: Mixed Into the Fed — Seasonal Momentum After Day 11

The market enters the week positioned for chop, but with improving internals and strong seasonality looming. Flows have stabilised, rate expectations soften the macro backdrop, and the Santa window opens soon — but recession signals and geopolitical fragility still loom large.

Equities:

Momentum remains constructive as internals strengthen and volatility stays suppressed. Seasonal tailwinds grow stronger after the 11th trading day of December, but any hawkish surprise from the Fed could quickly challenge upside follow-through.

Gold & Silver:

Gold’s structural bull case remains supported by tight supply and falling yields. Silver’s higher beta keeps it attractive tactically, though it remains sensitive to liquidity swings.

Crypto:

Structural liquidity issues persist, with reduced accumulation among key mid-tier holders. Upside depends on broader risk appetite and whether liquidity channels open post-FOMC.

Macro:

The LEI/CEI recession signal demands attention, even as labour holds stable and inflation cools. If QT guidance softens and yields remain capped, risk assets could extend gains into year-end — but the window is narrow and highly path-dependent.

“Expect chop into the Fed — but once the calendar clears and seasonality turns on, the path of least resistance becomes higher. The window is narrow, but the opportunity is real.”