AI Anxiety Meets Earnings Resilience, Rotation Beneath the Surface

Markets move into the back half of February, navigating a complex mix of strong earnings momentum and heightened uncertainty around AI-driven disruption. Price action has reflected a period of reassessment rather than outright deterioration, with sharp swings and leadership shifts highlighting how positioning is being recalibrated across sectors.

Liquidity remains supportive, yet participation reveals signs of caution. Defensive rotations, sensitivity to macro releases, and difficulty sustaining moves at key levels point to underlying stress even as the broader equity structure holds together.

Market Overview: Rotation and Repricing Without Structural Breakdown

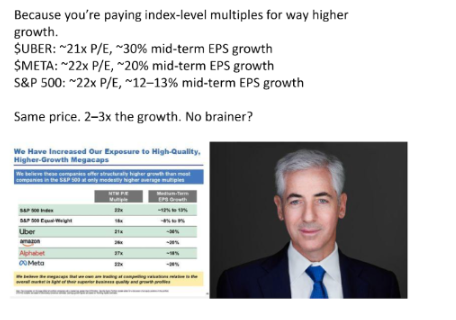

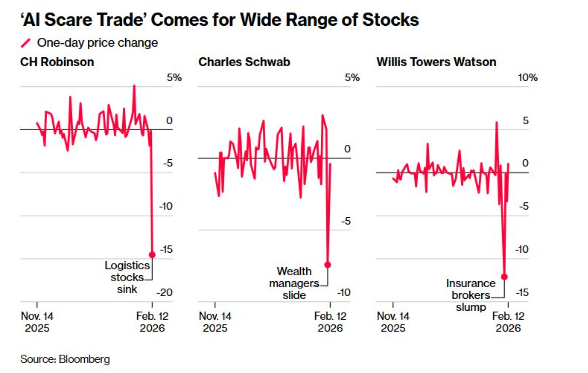

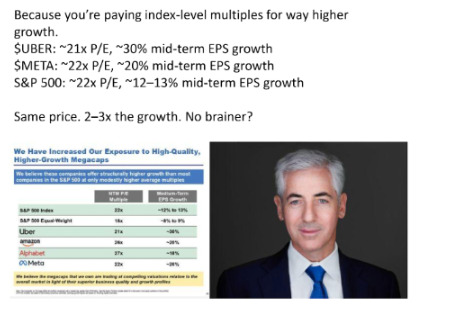

Equity markets have experienced notable multiple compression even as earnings continue to advance, reflecting a repricing of expectations rather than a deterioration in fundamentals. AI-related fears have driven broad sector anxiety, contributing to unwinds in momentum trades and increased dispersion across industries.

Flows into defensive sectors alongside continued strength in growth expectations highlight a market balancing caution with opportunity. The environment suggests that buying high-growth companies at market-level multiples may present opportunities as rotations settle.

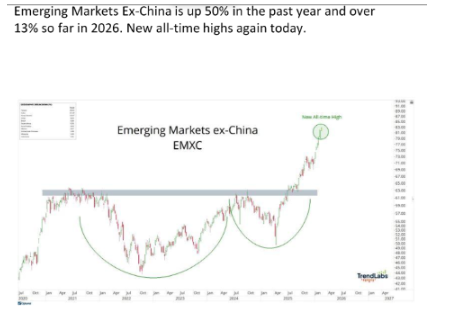

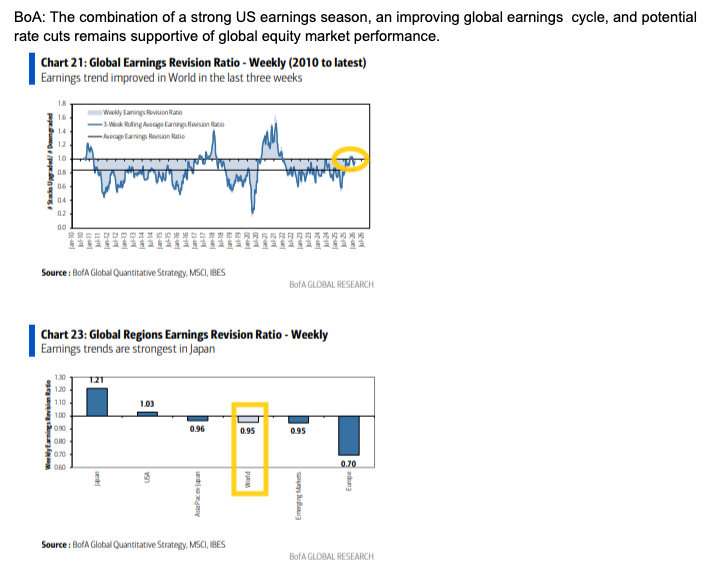

Flows toward non-US equities continue to reverse prior concentration, supported by expectations of fiscal loosening across major economies. This shift underscores a broader participation dynamic rather than a narrow leadership environment.

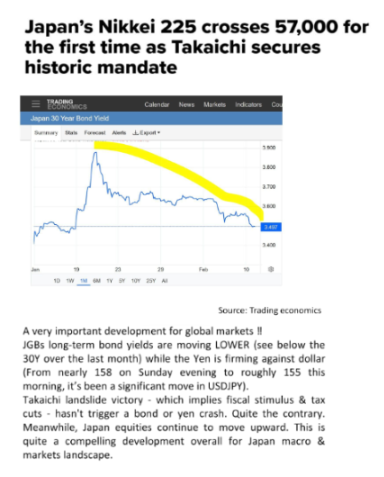

Japan remains a focal point as a supportive mix of policy direction, currency dynamics, and investor demand attracts both domestic and foreign capital.

Macro & Policy Watch: Liquidity, Inflation Signals, and Global Drivers

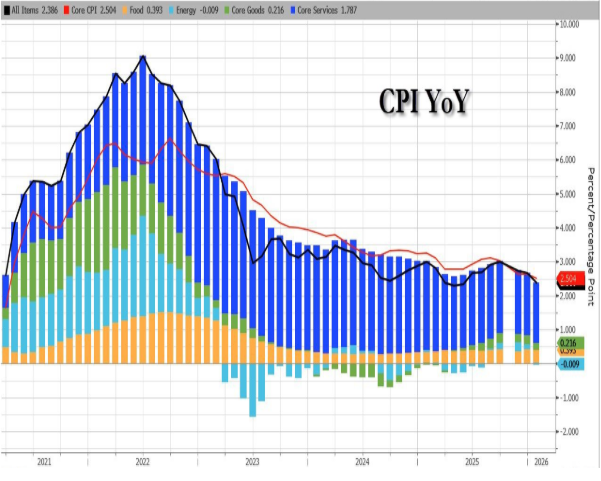

Cross-asset price action reflected the interaction between softer inflation prints and evolving expectations around policy support. Inflation readings came in cooler across headline measures, reinforcing the view that price pressures are moderating and allowing markets to lean toward expectations of easing conditions without signalling a shift in growth fundamentals.

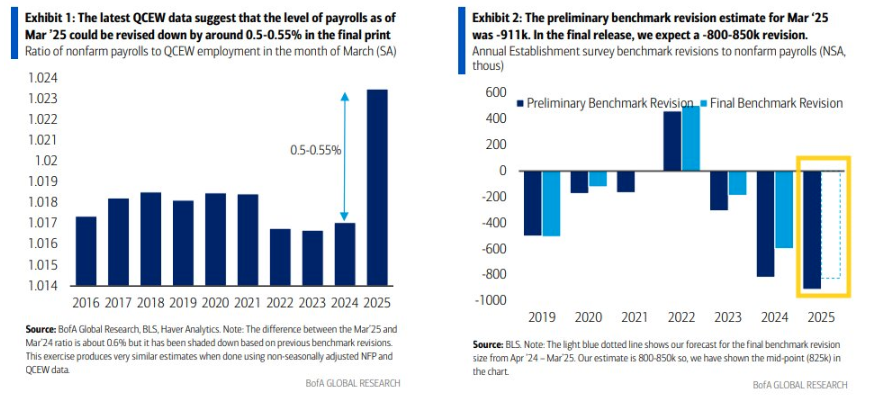

Labour market developments showed signs of slowing momentum without deterioration, with revisions highlighting how expectations continue to adjust as the breakeven pace of job growth declines. Growth tracking estimates have edged lower but continue to indicate expansion, reinforcing a cooling rather than contractionary backdrop.

Rates markets responded with yields trending lower, providing a supportive anchor for risk assets even as volatility persisted across equities. The move reflects expectations of easing financial conditions and reinforces the role of rates as a key transmission channel for broader market sentiment.

Global policy dynamics remained in focus, with fiscal support expectations and ongoing capital expenditure — particularly around technology — underpinning the broader macro environment. International flows and policy developments, including Japan’s supportive mix of demand and currency dynamics, continued to attract attention across asset classes.

Technical & Sentiment Breakdown: Consolidation with Reactive Positioning

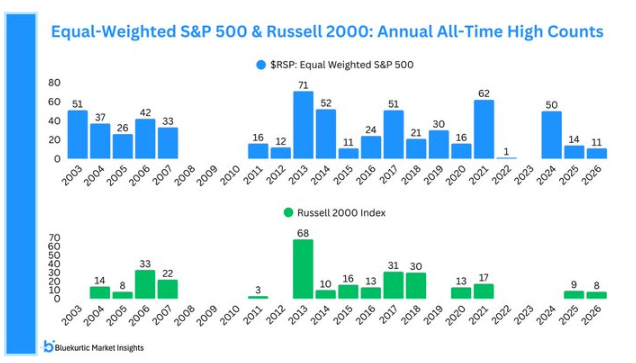

Headline indices remained within broader ranges as repeated tests of key levels reflected a market consolidating after strong gains. Difficulty sustaining moves above resistance underscored how positioning remains tactical, with participants reacting quickly to shifts in momentum.

Leadership rotation persisted as large technology names consolidated while other areas of the market attracted flows, reinforcing a broadening dynamic beneath stable headline indices. Dispersion across sectors remained elevated as investors adjusted exposures.

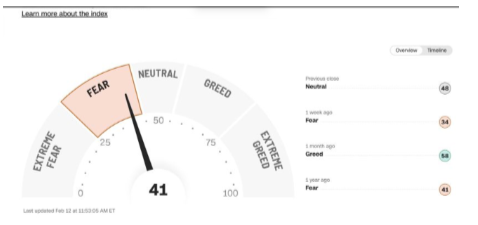

Sentiment indicators pointed to rising caution, with rapid swings between overbought and oversold conditions highlighting reactive positioning. Episodes where supportive developments failed to generate follow-through reflected fragile conviction across participants.

Breadth remained constructive in parts of the market, suggesting participation beyond narrow leadership even as volatility persisted. Range-bound behaviour reinforced the importance of monitoring positioning shifts as markets digested prior gains.

Last Week’s Recap: Cooling Inflation and Positioning Adjustments

Recent developments reinforced the theme of easing inflation alongside resilient growth, while cross-asset movements reflected ongoing repositioning rather than structural change.

Key Highlights

Macro

Inflation readings came in softer, reinforcing expectations of moderating price pressures and supportive financial conditions.

China

Seasonal dynamics and ongoing developments in China continued to influence global flows and sentiment.

Earnings

Corporate earnings remained strong, with a high proportion of companies exceeding expectations and forward estimates continuing to rise.

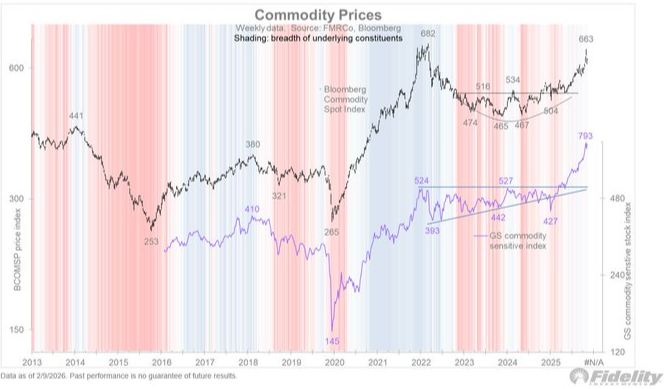

Commodities

Precious metals and broader commodity markets remained influenced by supply dynamics, geopolitical considerations, and positioning shifts.

Crypto

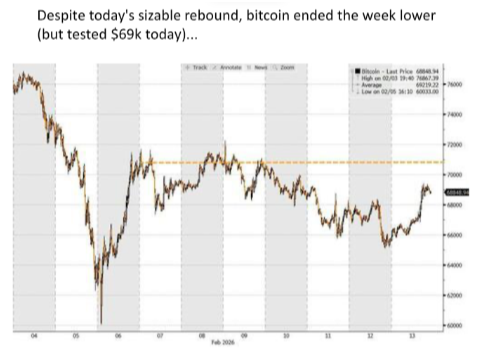

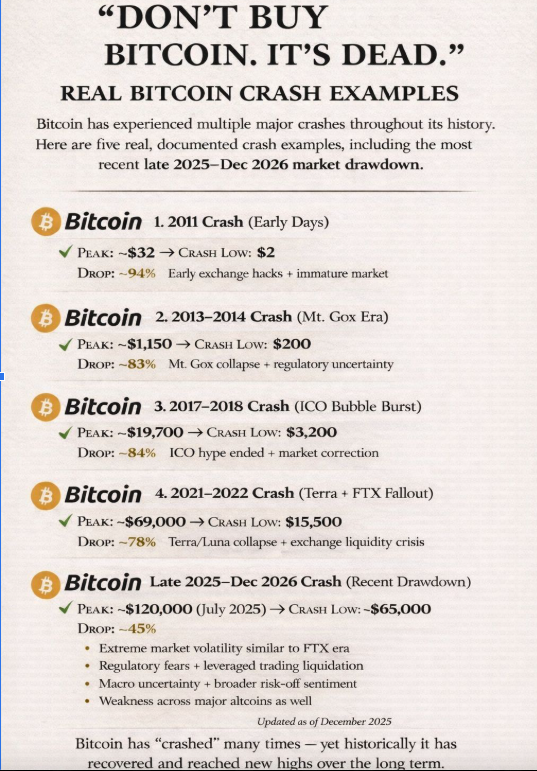

Digital assets experienced volatility but continued to show signs of stabilisation amid shifting correlations and positioning dynamics.

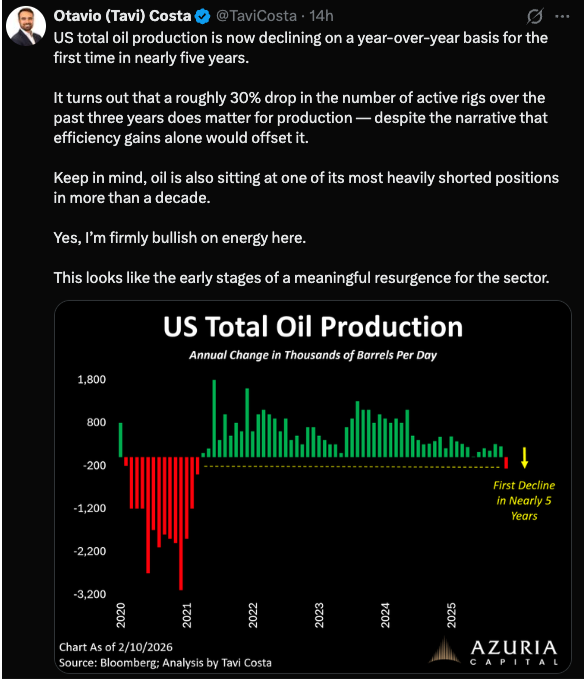

Oil

Energy markets remained sensitive to geopolitical developments and supply considerations, with price action reflecting fluctuating risk premiums.

The Week Ahead: Key Data and Market-Moving Signals

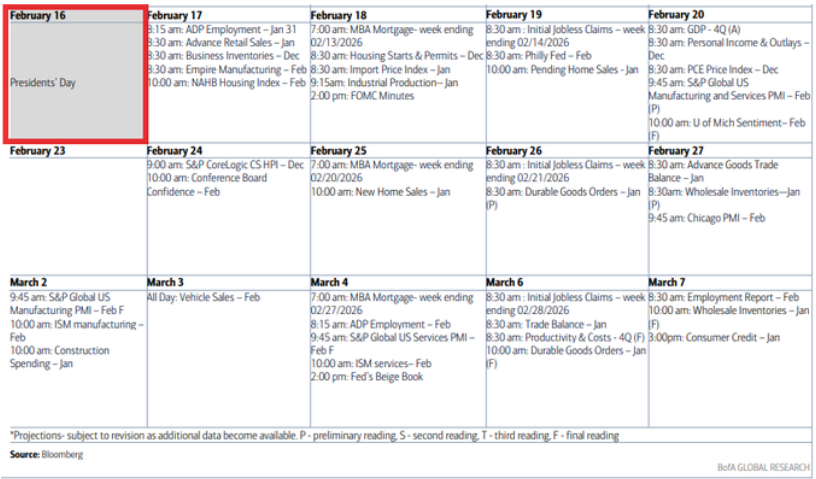

The week starts with a US holiday and China’s Lunar New Year, keeping volumes lighter, before attention turns to FOMC minutes, housing and durable goods, Q4 GDP, and Friday’s PCE, alongside global CPI updates, the RBNZ decision, trade data, and PMIs.

Monday, February 16

- US: Washington’s Birthday holiday

- Global: China Lunar New Year

- Japan: Q4 GDP (QoQ, YoY, components)

- Canada: CPI (headline, core measures)

- Europe: Industrial production

- UK: Rightmove house prices

- ECB Eurogroup meetings / Fed & ECB speakers

Tuesday, February 17

- UK: Employment data, unemployment rate, earnings

- Germany / Eurozone: CPI and ZEW sentiment

- US: Empire manufacturing index, NAHB housing index

- Canada: CPI details and wholesale sales

- Japan: Trade balance, exports, imports

- RBA minutes / Fed speakers

Wednesday, February 18

- RBNZ: Rate decision and press conference

- UK: CPI and inflation measures

- Europe: French CPI

- US: Durable goods orders

- US: Housing starts and building permits

- US: Industrial production and capacity utilisation

- US: FOMC minutes

Thursday, February 19

- US: Initial jobless claims

- US: Trade balance and goods trade

- US: Philadelphia Fed manufacturing index

- US: Wholesale inventories and pending home sales

- Japan: National CPI

- ECB bulletin / Fed speakers

- US: 30-Year TIPS auction

Friday, February 20

- US: Core PCE and PCE inflation

- US: GDP (Q4 advance) and GDP price index

- US: Personal income and spending

- US: PMIs (manufacturing, services, composite)

- US: Michigan consumer sentiment

- UK: Retail sales

- Eurozone / Germany / France: PMIs

- China: Loan Prime Rate

- CFTC positioning across major asset classes

Alpha Takeaway: Consolidation Within a Constructive Backdrop

Markets appear to be navigating a phase of consolidation as strong earnings momentum, easing inflation pressures, and positioning resets interact with ongoing uncertainty around leadership and valuation adjustments.

Equities

Earnings resilience, continued capital expenditure, and improving breadth support the underlying structure even as leadership rotates away from crowded areas and momentum moderates amid multiple compressions.

Gold & Silver

Precious metals remain supported by macro uncertainty, supply considerations, and shifting inflation expectations, with positioning reflecting both defensive demand and sensitivity to rates.

Crypto

Volatility reflects positioning adjustments and shifting correlations, with price action suggesting a period of consolidation as markets weigh risk sentiment and potential recovery dynamics.

Macro

Moderating inflation, lower yields, expectations of policy support, and ongoing fiscal and liquidity dynamics continue to frame the broader environment despite near-term volatility.

The current phase reflects repricing rather than deterioration, with markets adjusting to shifts in leadership and sentiment. Careful monitoring of flows and macro signals remains essential as the next directional move develops.

Excerpt:

Markets remain in a constructive consolidation, supported by earnings resilience, easing inflation and improving breadth, though leadership rotation and AI-driven repricing are raising sensitivity beneath the surface. With positioning adjusting rather than breaking down, the focus remains on whether supportive liquidity and macro signals can sustain the next directional move.