Liquidity Breaks the Calm, Positioning Gets Exposed

Markets enter the week having just experienced their sharpest reminder this year that stability built on leverage and crowded positioning is inherently fragile. What began as routine consolidation quickly morphed into a disorderly repricing across metals, volatility products, and selected risk assets, with spillovers felt well beyond their original source.

The shift in tone was abrupt, but not random. Participation remained high, yet conviction thinned rapidly once volatility expanded. The events of last week were not driven by deteriorating growth data or an earnings collapse, but by liquidity sensitivity finally asserting itself beneath extended trends.

Market Overview: Structure Intact, but No Longer Forgiving

Equity structure remains intact, but the internal message has clearly changed. Markets are no longer advancing on broad momentum. Instead, price action reflects selective participation, increasing dispersion, and a growing intolerance for leverage and crowding.

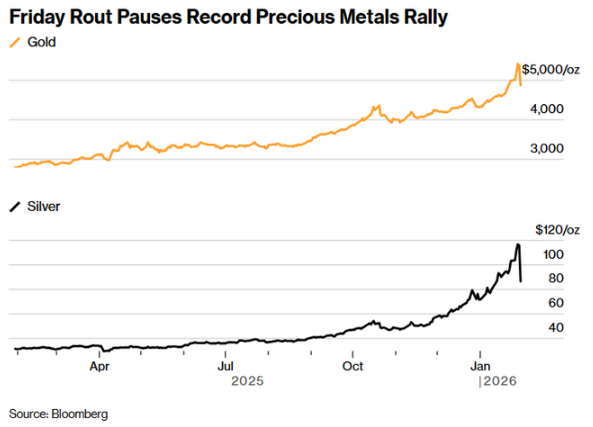

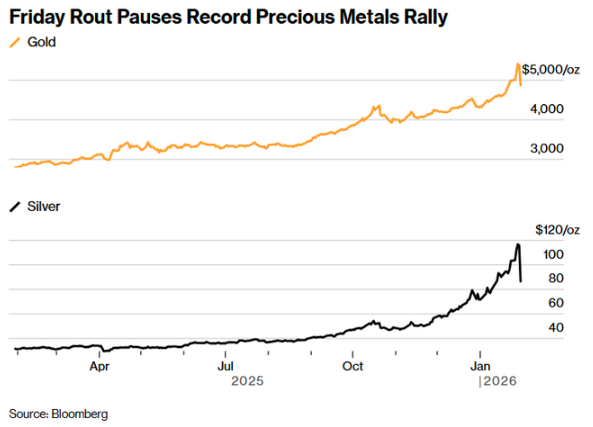

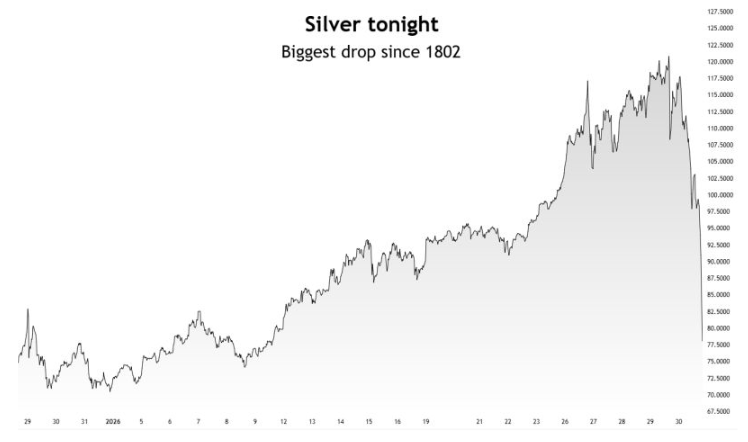

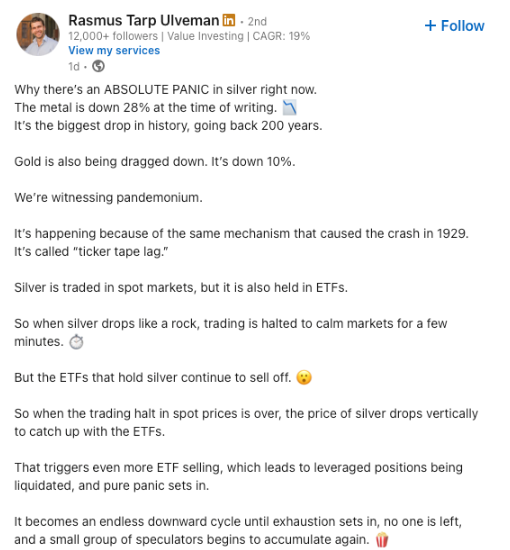

The most important development was the violent repricing in precious metals, which acted as the initial stress point. Extreme volatility readings in gold and silver were followed by forced selling, triggering a cascade that rippled through systematic positioning and broader risk exposure. This was not a growth shock — it was a liquidity event.

Despite the scale of the move, equities absorbed the shock without structural damage. Headline indices remained resilient, reinforcing that this episode reflected a tightening of risk tolerance rather than a wholesale exit from equities. However, the ease with which markets had been advancing has clearly diminished.

Macro & Policy Watch: Liquidity, Not Rates, Drives Price Action

Policy narratives last week were quickly absorbed into a broader liquidity framework. Market reaction was less about changes to rate expectations and more about uncertainty around balance sheet support and the perceived durability of accommodation.

The focus shifted toward whether liquidity conditions would remain as supportive as markets had assumed. This reframing mattered most for assets that had benefited from sustained inflows and leverage, leaving them vulnerable once confidence wavered.

Geopolitical developments added background noise, but their market impact remained secondary. The dominant transmission channel into price action was liquidity sensitivity rather than headline risk. This distinction is critical: it explains why the sharpest moves occurred in assets with the most extended positioning rather than those most exposed to geopolitical narratives.

Technical & Sentiment Breakdown: Supportive, but Increasingly Fragile

From a technical perspective, markets remain in an uptrend, but momentum has slowed materially. Recent price action reflects consolidation rather than continuation, with volatility expanding from historically compressed levels.

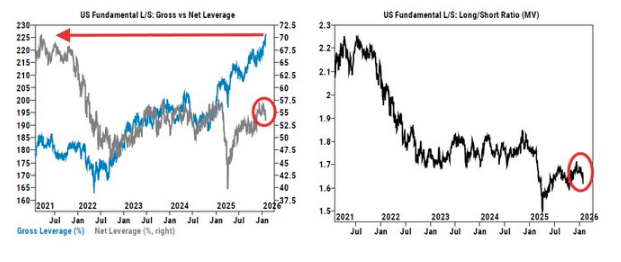

Sentiment indicators show a clear reset underway. Gross leverage across hedge funds and systematic strategies remains elevated, but net leverage has declined sharply, indicating that risk reduction is occurring through trimming rather than outright liquidation.

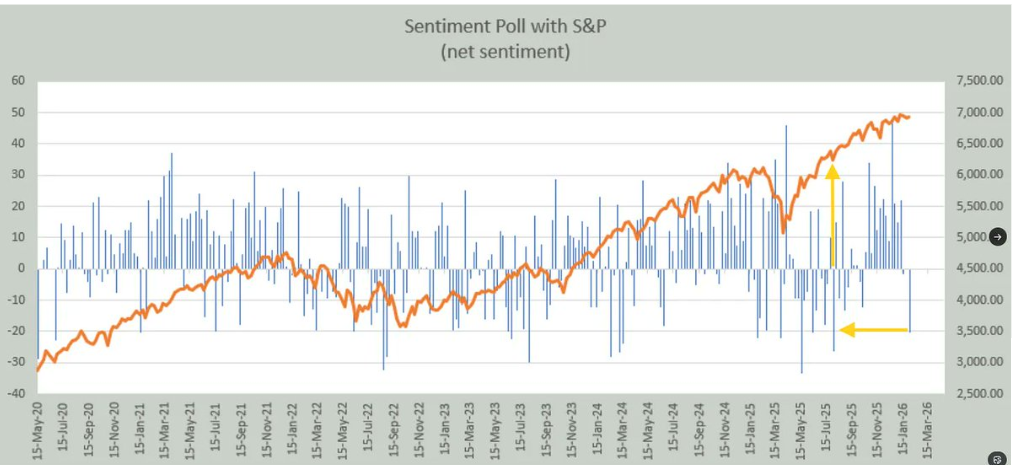

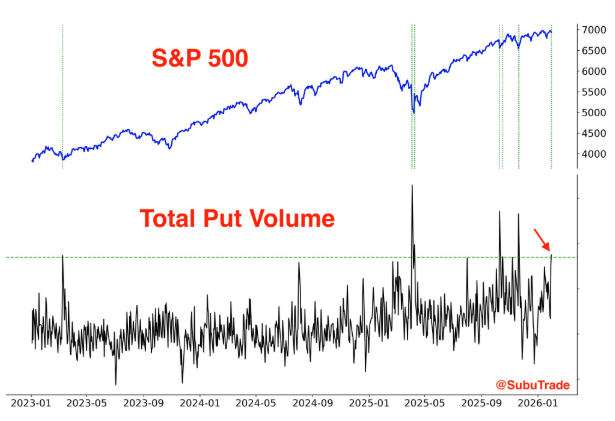

Options markets reinforced this message. Put volume spiked late in the week, suggesting a delayed but meaningful increase in demand for protection. This shift marks a transition from complacency to caution, even as headline indices remain near highs.

Last Week’s Recap: Liquidity Shock, Positioning Reset

Last week served as a case study in how volatility emerges when leverage and liquidity collide.

Key Highlights:

Macro:

Macro data itself was not the catalyst. Price action was driven by volatility extremes and forced deleveraging rather than new economic information. Services inflation pressures remained evident, while shelter components continued their gradual decline, with lagged effects still feeding into broader inflation measures.

China:

China-related signals remained mixed. Regional growth pressures and deflationary dynamics persisted, reinforcing concerns around demand and limiting the global growth impulse.

Earnings:

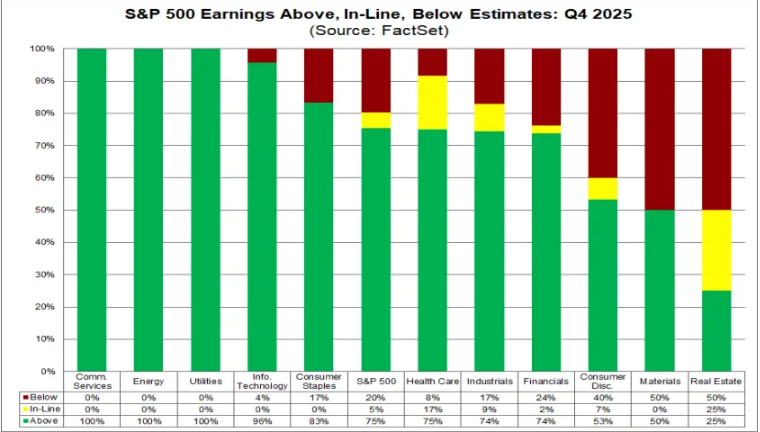

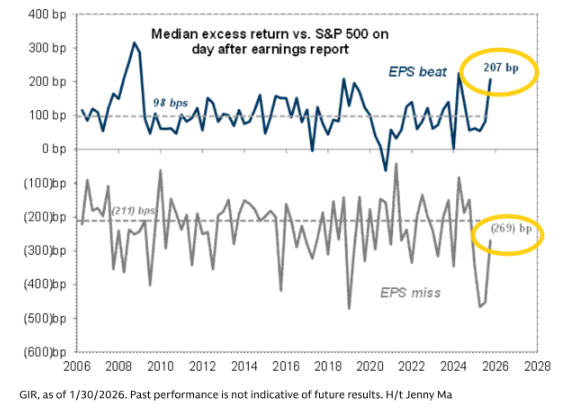

Early earnings results remained broadly constructive. Beats continued to outnumber misses, though dispersion increased and tolerance for disappointment narrowed, particularly in sectors sensitive to rates and liquidity.

Commodities:

Precious metals experienced one of the most extreme repricings in the dataset. Silver collapsed following ETF dislocations and forced selling, while gold retraced sharply after an extended advance, unwinding excess momentum rather than invalidating the broader structural drivers.

Crypto:

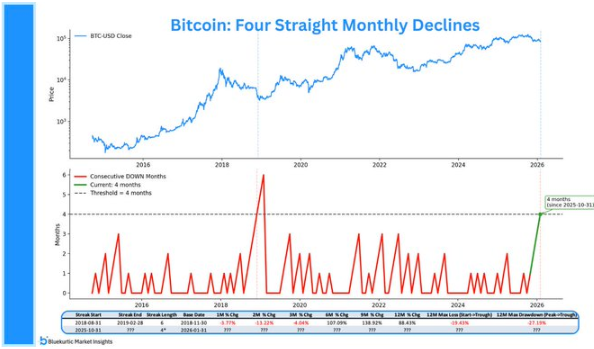

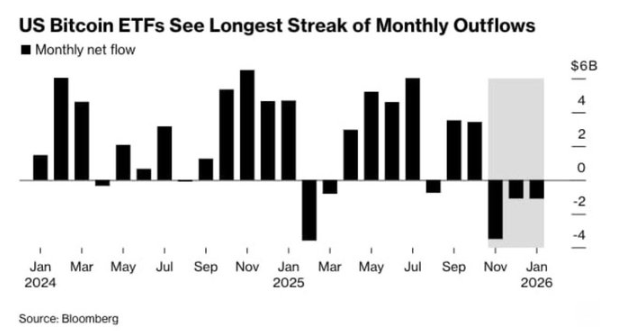

Crypto assets remained under pressure. Bitcoin extended a multi-month decline, while ETF flows continued to unwind. Price action reflects ongoing deleveraging rather than renewed accumulation.

Oil:

Oil prices remained range-bound. Supply considerations and geopolitical risk were offset by softer demand signals, particularly from China, resulting in consolidation rather than directional follow-through.

The Week Ahead: Key Data and Market-Moving Signals

The coming week is heavily focused on the US labour market, with a dense run of employment indicators leading into Friday’s payrolls report. With markets already sensitive to liquidity and positioning, these releases, alongside scheduled Federal Reserve commentary, carry increased potential to influence rate expectations, volatility, and risk sentiment.

Monday, February 2

- US: S&P Global US Manufacturing PMI (Jan, final)

- US: ISM Manufacturing (Jan)

- US: Bostic speaks at the Atlanta Rotary Club

Tuesday, February 3

- US: JOLTS Job Openings (Dec)

- US: Wards Total Vehicle Sales (Jan)

- US: Barkin speaks on the US economy

- US: Bowman in moderated conversation

Wednesday, February 4

- US: MBA Mortgage Applications

- US: ADP Employment Change (Jan)

- US: S&P Global US Services PMI (Jan, final)

- US: ISM Services Index (Jan)

Thursday, February 5

- US: Initial Jobless Claims

- US: Bostic speaks with the Dean of Clark Atlanta University

Friday, February 6

- US: Change in Nonfarm Payrolls (Jan)

- US: Change in Private Payrolls (Jan)

- US: Average Weekly Earnings MoM (Jan)

- US: Average Weekly Hours (Jan)

- US: Unemployment Rate (Jan)

- US: Labour Force Participation Rate (Jan)

- US: University of Michigan Sentiment (Feb, preliminary)

- US: Consumer Credit (Dec)

Alpha Takeaway: Structure Intact, Tolerance for Risk Narrows

Markets remain structurally supported, but last week exposed how sensitive positioning has become as volatility expands and liquidity tightens. Selectivity continues to matter more than broad exposure, particularly where crowding has built up.

Equities:

Equity structure remains intact, but leadership is narrow. Gross exposure is high while net leverage has declined, pointing to rotation and trimming rather than broad de-risking. Consolidation remains the dominant pattern, increasing the importance of positioning and timing.

Gold & Silver:

Precious metals saw a sharp reset driven by volatility extremes, ETF dislocations, and forced selling. The broader framework remains intact, but near-term price action is dominated by positioning repair, keeping volatility elevated.

Crypto:

Crypto continues to lag, with price action reflecting ongoing deleveraging rather than accumulation. Persistent declines and ETF outflows suggest conviction remains uneven and liquidity-sensitive.

Macro:

Liquidity expectations are now the primary macro driver. Market sensitivity last week reflected balance sheet and liquidity concerns rather than growth deterioration, increasing reactivity to shocks.

The environment remains sensitive to positioning. Stability now depends more on how leverage and liquidity adjust than on continued momentum.