Grinding Through Uncertainty, Liquidity Cross-Currents and Rotation Define the Tape

Markets move into the latter part of February with price action continuing to grind higher despite persistent concerns about downside risks. The environment reflects a classic “wall of worry,” where institutional long buying and retail participation coexist with speculative flows leaning the other way, creating conditions where weaker positioning can be squeezed as markets advance.

Liquidity remains a key driver beneath the surface. Funding needs in the bond market, ongoing geopolitical developments, and major earnings catalysts are shaping short-term flows, while sector rotation — particularly across technology, commodities, and defensives — highlights an environment where the broader structure remains intact even as underlying dynamics evolve.

Market Overview: Constructive Structure with Ongoing Rotation

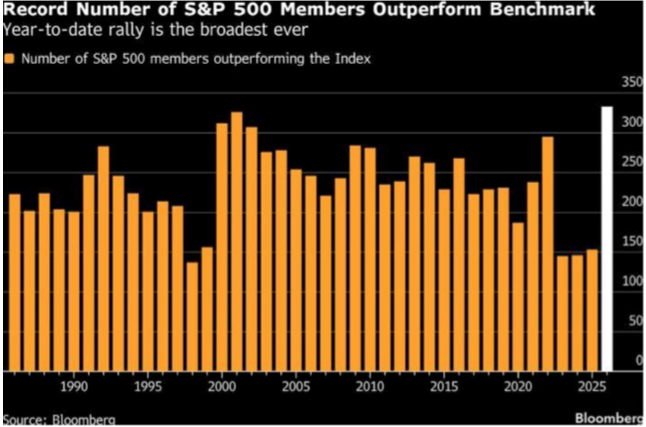

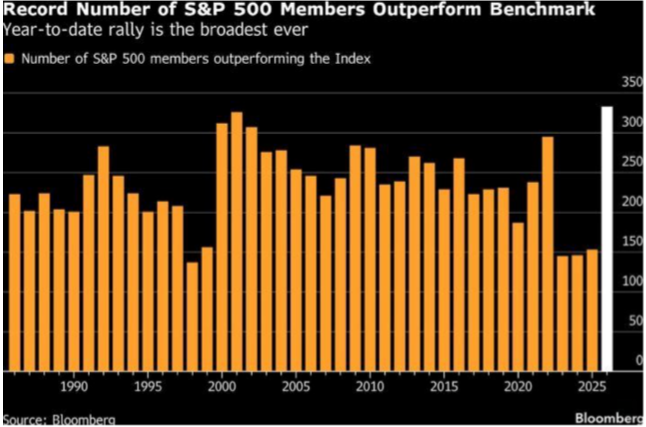

Equity markets continue to show resilience, with participation broad enough to support the advance even as leadership rotates across sectors. Price action suggests that markets are absorbing headline risks, including policy developments and geopolitical noise, without losing structural footing.

Institutional buying alongside retail activity has created a backdrop where short positioning risks being squeezed, reinforcing the constructive tone. At the same time, there is evidence of defensive flows emerging as seasonal tendencies and macro uncertainties encourage a degree of caution.

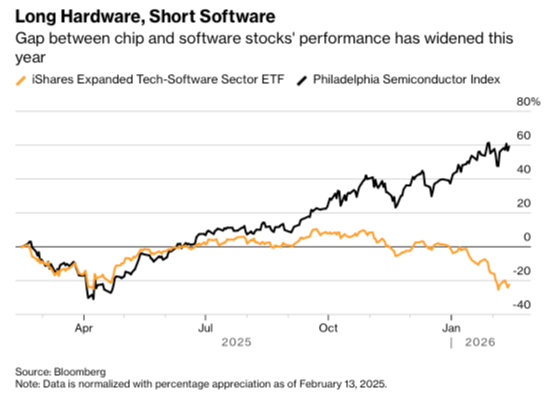

Rotation within the AI ecosystem remains a defining theme. While enthusiasm around artificial intelligence persists, flows are increasingly differentiating between areas seen as structural beneficiaries — such as semiconductors, infrastructure, and energy inputs — and segments facing questions around long-term disruption.

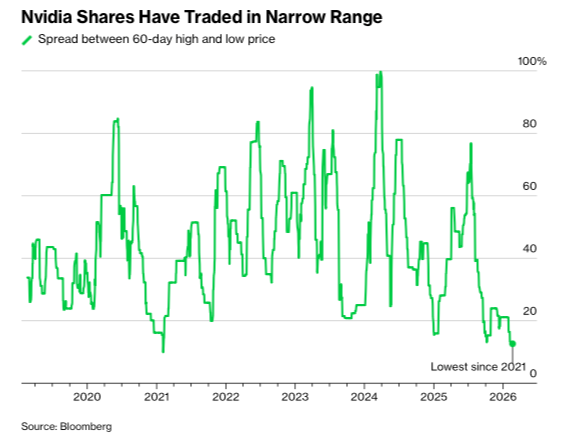

NVIDIA sits at the centre of this dynamic, with expectations around earnings and guidance acting as a key catalyst not just for the stock but for broader market sentiment and dispersion across large-cap technology.

Global equity benchmarks continue to reflect strength, with new highs in broad indices reinforcing the idea that the overall structure remains constructive despite tactical volatility.

Macro & Policy Watch: Liquidity Drains, Policy Signals, and Mixed Data

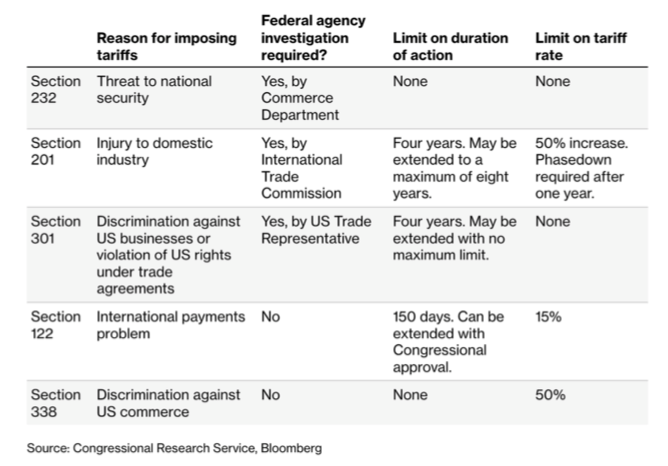

Policy developments around tariffs have reintroduced uncertainty, with legal rulings and alternative mechanisms shaping expectations around trade policy. The key issue is less the immediate outcome and more the potential for prolonged uncertainty to influence corporate planning and earnings outlooks.

Liquidity dynamics are particularly important this week, with significant funding needs tied to bond market settlements historically associated with softer equity sessions. These flows coincide with major earnings events, reinforcing the importance of monitoring cross-asset interactions.

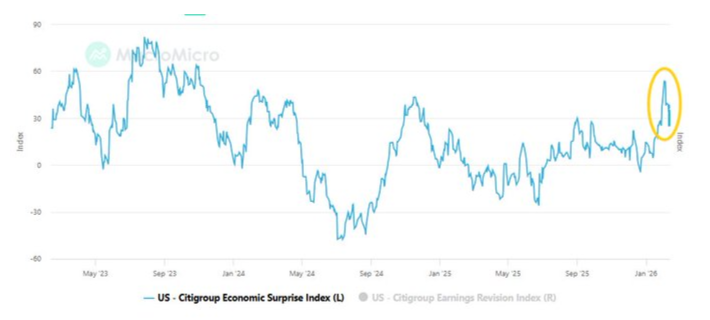

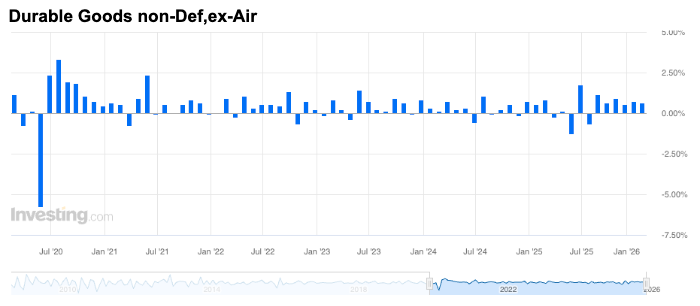

Economic data have presented a mixed picture. Surprise indices have turned negative, reflecting softer headline momentum, yet underlying components such as business investment measures suggest pockets of resilience beneath the surface.

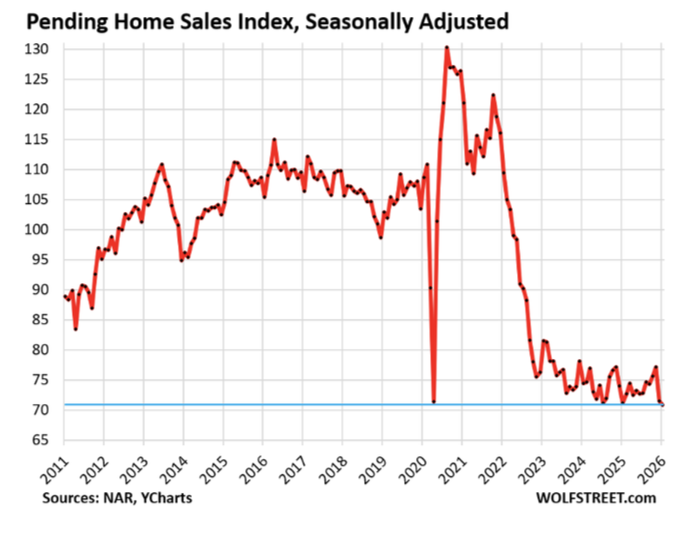

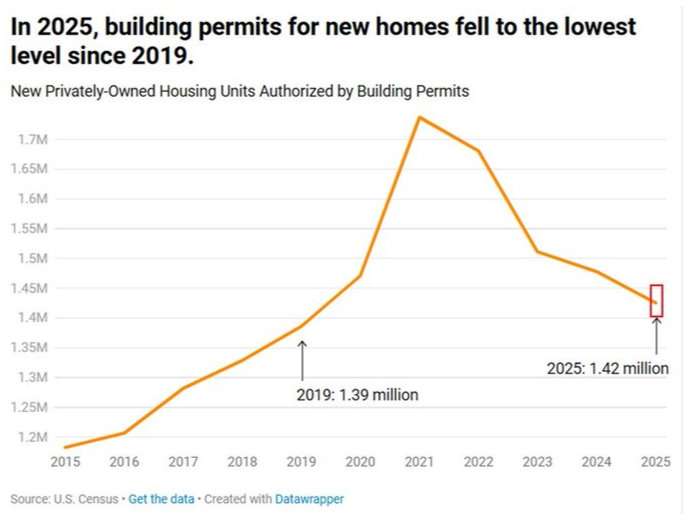

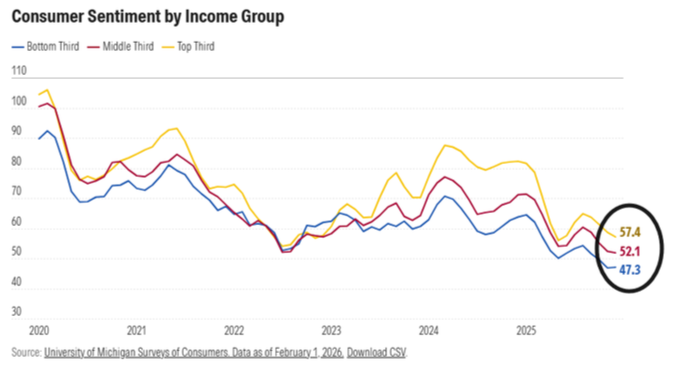

Housing indicators and consumer sentiment point to uneven momentum, consistent with a gradual rather than synchronised expansion. Slippage in pending sales and permits alongside softer sentiment readings highlight areas of cooling without signalling broad deterioration.

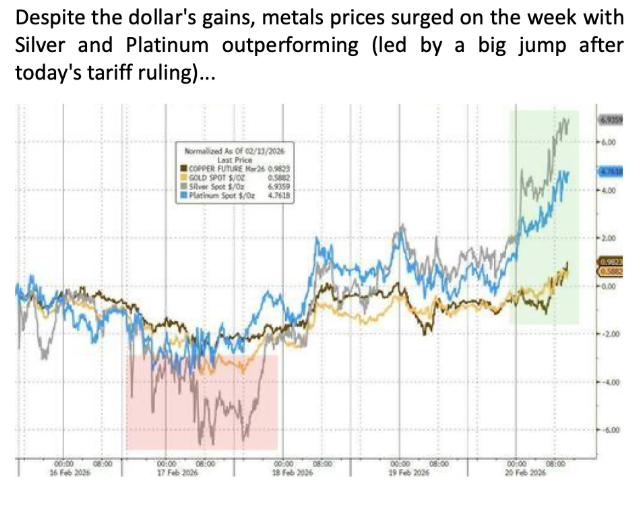

Geopolitical developments continue to influence commodities, with oil and gold responding to military posturing and supply dynamics, though historical patterns suggest such spikes often fade over time.

Technical & Sentiment Breakdown: Consolidation with Strong Internals

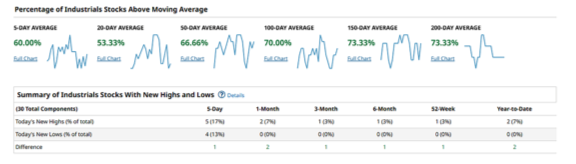

Market internals remain supportive even as headline indices face challenges holding near-term moving averages. This combination — firm breadth alongside episodic momentum stalls — reflects a market advancing while continuously testing conviction.

The NASDAQ shows signs of testing momentum, with key moving averages acting as important reference points as investors assess whether recent consolidation represents a pause within an uptrend or a broader shift in leadership.

Sentiment indicators highlight elevated positioning around key catalysts, including options activity suggesting heightened focus on directional risk. At the same time, volatility measures imply that markets may be pricing less risk than recent price behaviour might suggest.

Flows and positioning data point to confusion among investors, with surveys showing optimism on earnings alongside concerns around overinvestment and crowded trades. This mix reinforces the view that markets are navigating competing narratives rather than a single dominant theme.

Last Week’s Recap: Liquidity Signals and Cross-Asset Adjustments

Recent developments reflected a combination of earnings reactions, policy headlines, and evolving positioning across asset classes, reinforcing the theme of resilience alongside underlying caution.

Key Highlights

Macro

Data releases showed softer surprise readings while underlying indicators suggested continued activity. Policy discussions and liquidity considerations remained central to market interpretation as investors assessed the implications for growth and rates.

China

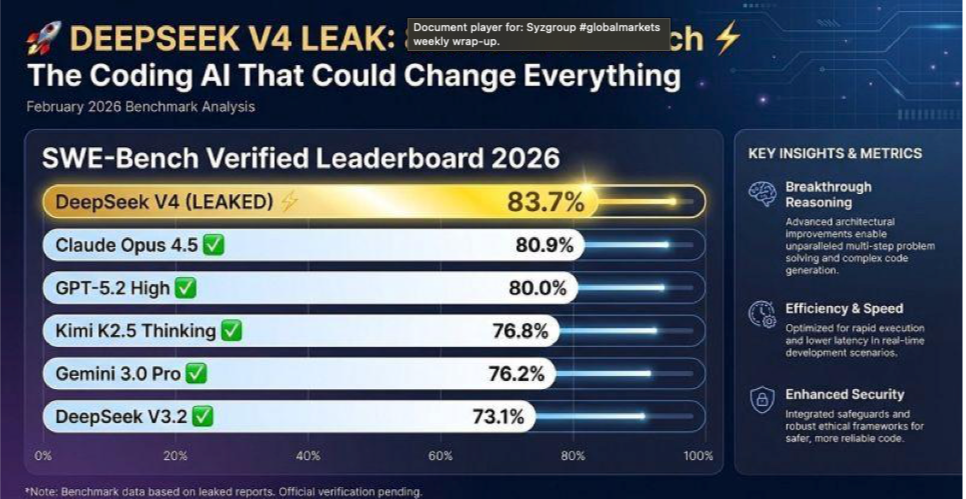

Developments around new AI initiatives and competitive dynamics within technology drew attention, highlighting potential shifts in global innovation and cost structures that could influence sentiment.

Earnings

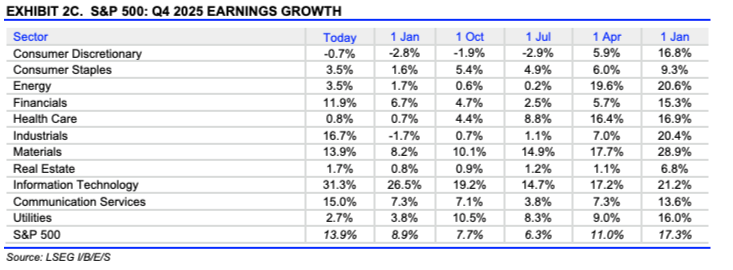

Corporate results broadly exceeded expectations, with a significant proportion of companies reporting above estimates and forward growth expectations remaining constructive even as markets focused closely on guidance.

Commodities

Gold continued to show strength amid uncertainty and positioning dynamics, while broader commodity behaviour reflected geopolitical developments and supply considerations, reinforcing the role of real assets within portfolio allocations.

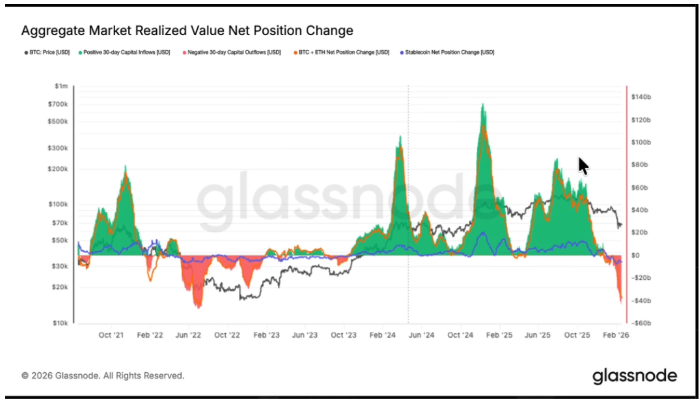

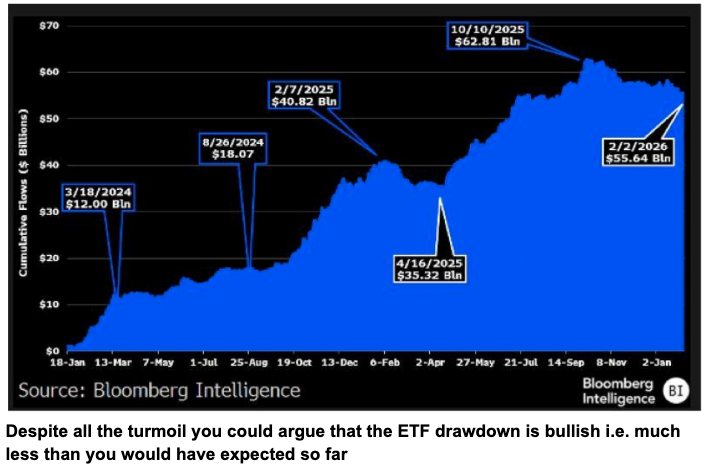

Crypto

Digital assets saw positioning adjustments and ongoing debate around flows, with market participants assessing whether recent moves represent consolidation within a broader trend or continued volatility driven by sentiment shifts.

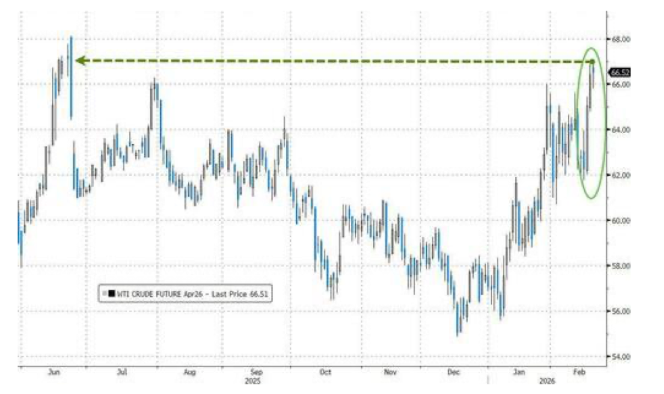

Oil

Energy markets remained sensitive to geopolitical developments and inventory dynamics, with price action reflecting fluctuating risk premia and the interaction between supply concerns and macro expectations.

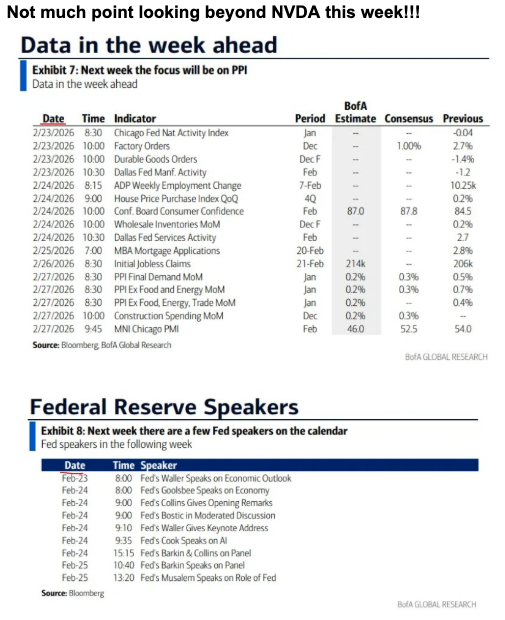

The Week Ahead: Key Data and Market-Moving Signals

The week is centred on NVIDIA earnings, which effectively act as the primary macro catalyst given their influence across AI, large-cap technology, and broader risk sentiment. Liquidity will remain an important theme as multiple bond auctions and settlement flows keep funding conditions in focus. The State of the Union address introduces potential policy headline risk, while PPI later in the week will be closely watched for signals on inflation pressures.

Monday, February 23

- Global: China Lunar New Year holiday (liquidity impact)

- Germany: Ifo business climate index and expectations

- Italy: CPI releases

- US: Chicago Fed national activity index

- US: Factory orders and durable goods data

- US: Dallas Fed manufacturing index

- France: Treasury bill auctions

- US: 3-month and 6-month bill auctions

- Central bank speakers: Fed, ECB, BoE

Tuesday, February 24

- China: FDI data

- UK: CBI distributive trades survey

- US: House price indices

- US: Consumer confidence

- US: Richmond Fed manufacturing index

- US: Wholesale inventories and trade sales

- US: Money supply data

- US: API crude oil inventories

- US: 2-year note auction

- US: State of the Union address

- Multiple Fed speakers

Wednesday, February 25

- Australia: CPI releases

- Germany: GDP and consumer climate

- Eurozone: Inflation readings

- US: Mortgage applications

- Canada: Manufacturing sales

- US: 5-year note auction

- Corporate: NVIDIA earnings

- Central bank speakers and policy events

Thursday, February 26

- New Zealand: Business confidence

- Australia: Capital expenditure

- Eurozone: Money supply and credit data

- US: Initial and continuing jobless claims

- US: Kansas City Fed indices

- Japan: Tokyo CPI

- US: 7-year note auction

- Central bank speakers

Friday, February 27

- UK: Consumer confidence

- Eurozone: Inflation prints

- Germany: CPI

- US: PPI and core PPI

- Canada: GDP

- US: Chicago PMI

- US: Construction spending

Alpha Takeaway: Constructive Trend with Competing Narratives

Markets continue to advance within a constructive framework as supportive participation interacts with policy uncertainty and mixed economic signals, reinforcing a backdrop where progress and caution coexist.

Equities

Broad participation and institutional flows support the structure, though leadership rotation and sensitivity to catalysts highlight the importance of monitoring positioning and technical levels.

Gold & Silver

Precious metals remain supported by uncertainty and positioning dynamics, reflecting their role as a hedge amid evolving macro narratives.

Crypto

Positioning reflects cautious engagement as markets balance volatility with shifting correlations across asset classes.

Macro

Liquidity dynamics, policy developments, and mixed data continue to frame expectations, reinforcing a balanced environment rather than a clear directional shift.

Markets appear to be navigating a phase where resilience persists alongside ongoing reassessment of risks. Careful monitoring of flows, sentiment, and policy developments remains essential as the next phase unfolds.