Setting the Stage: Markets on Edge Ahead of a Big Week

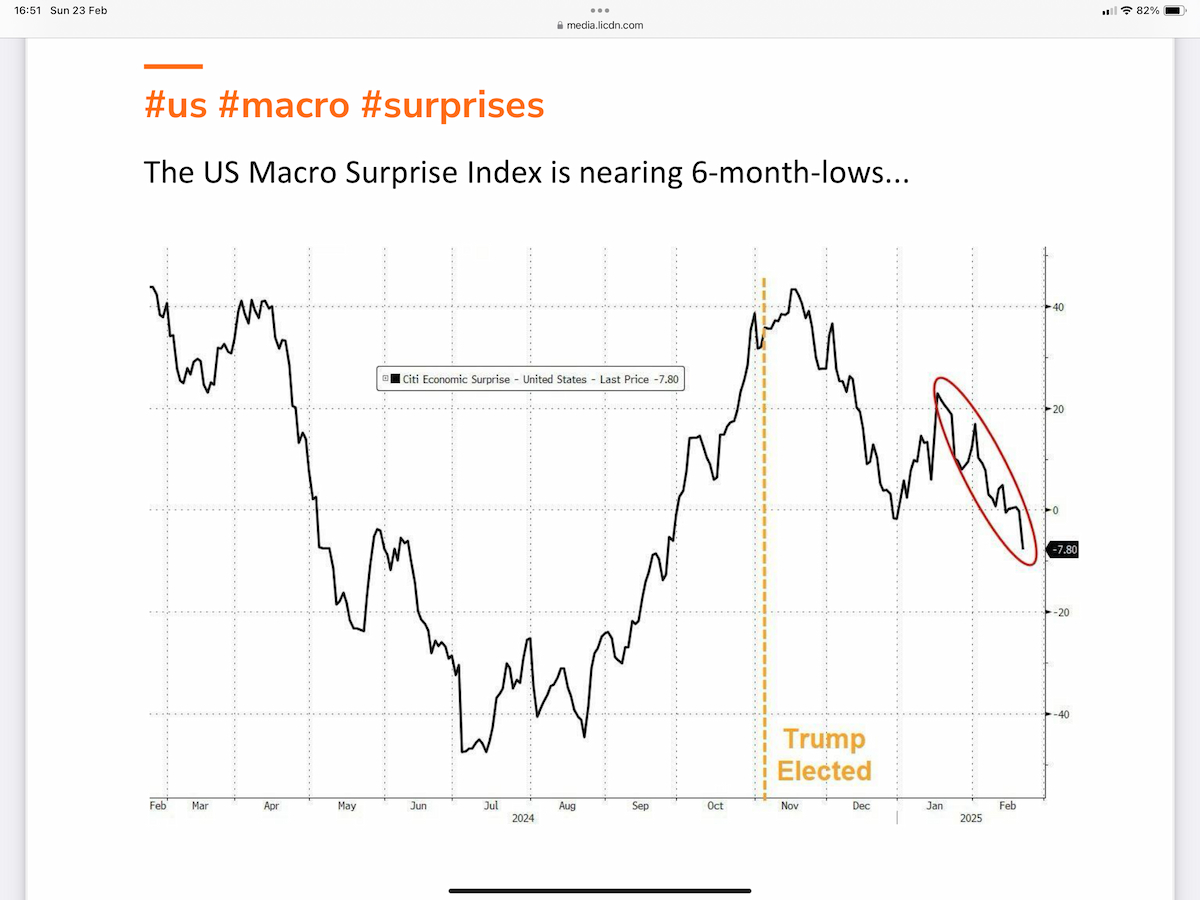

Volatility is creeping back in, and traders are gearing up for what could be a pivotal week. After retail sales disappointed and Walmart confirmed a bleak 2025 outlook, sentiment took a hit. Friday’s Michigan Consumer Sentiment collapse, alongside weak global PMIs, tipped the scales toward risk-off. The broader macro environment remains uncertain, with geopolitical tensions simmering under the surface and bond market volatility suggesting an impending shift in risk appetite.

Bond volatility is stirring, with MOVE and VIX ticking up, watch for Put/Call parity nearing 1. Meanwhile, geopolitical risks remain in the background, though Ukraine's push for a European peace envoy and OPEC+ supply maneuvers could quickly shift the narrative. Energy markets are closely watching developments in uranium supply talks, particularly between the US and Australia, which could impact nuclear power investments.

Key Market Themes

1. Bond Volatility & Yields: Buckle Up

Scott Bessent’s strategy of short-term bill financing persists, but the Trump team is eyeing longer-term yield normalization. Despite headline noise, bond volatility wasn’t initially breaking out, until Friday changed the game. US 10Y yields are erratic, dangerously flirting with slower growth pricing, which is causing concern about a potential economic slowdown. Stagflation chatter is picking up, adding to uncertainty over how central banks will respond.

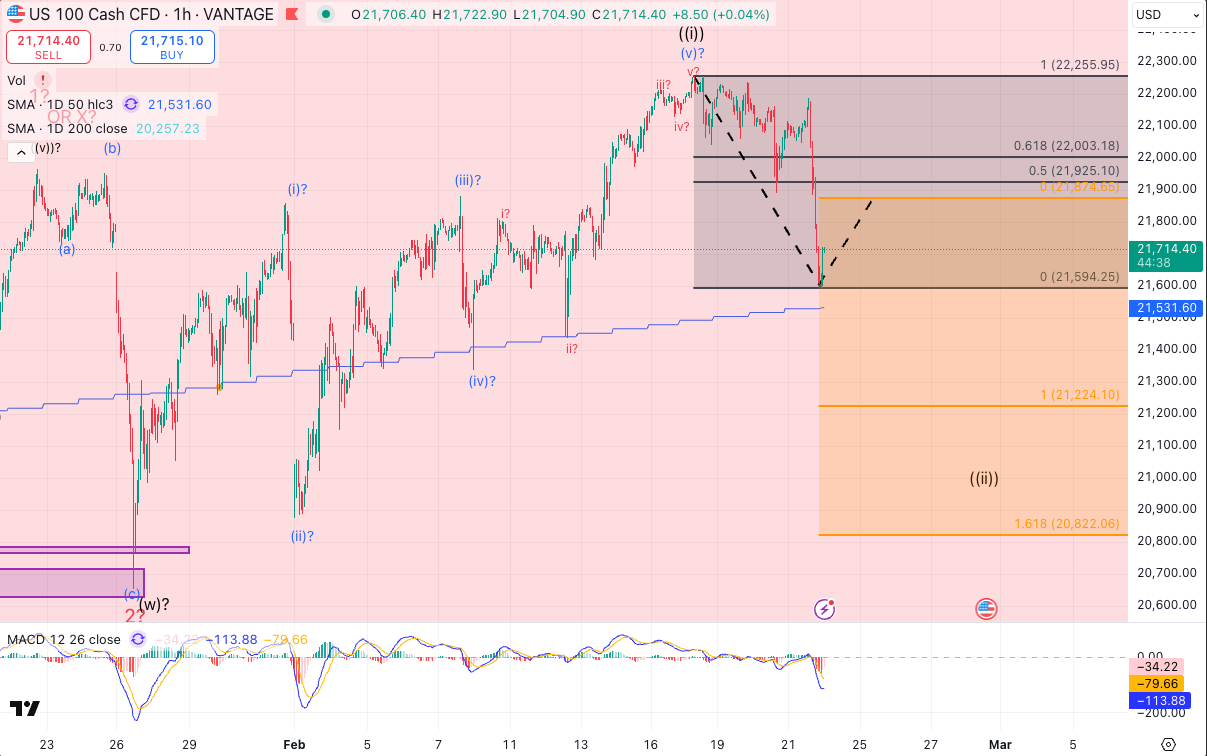

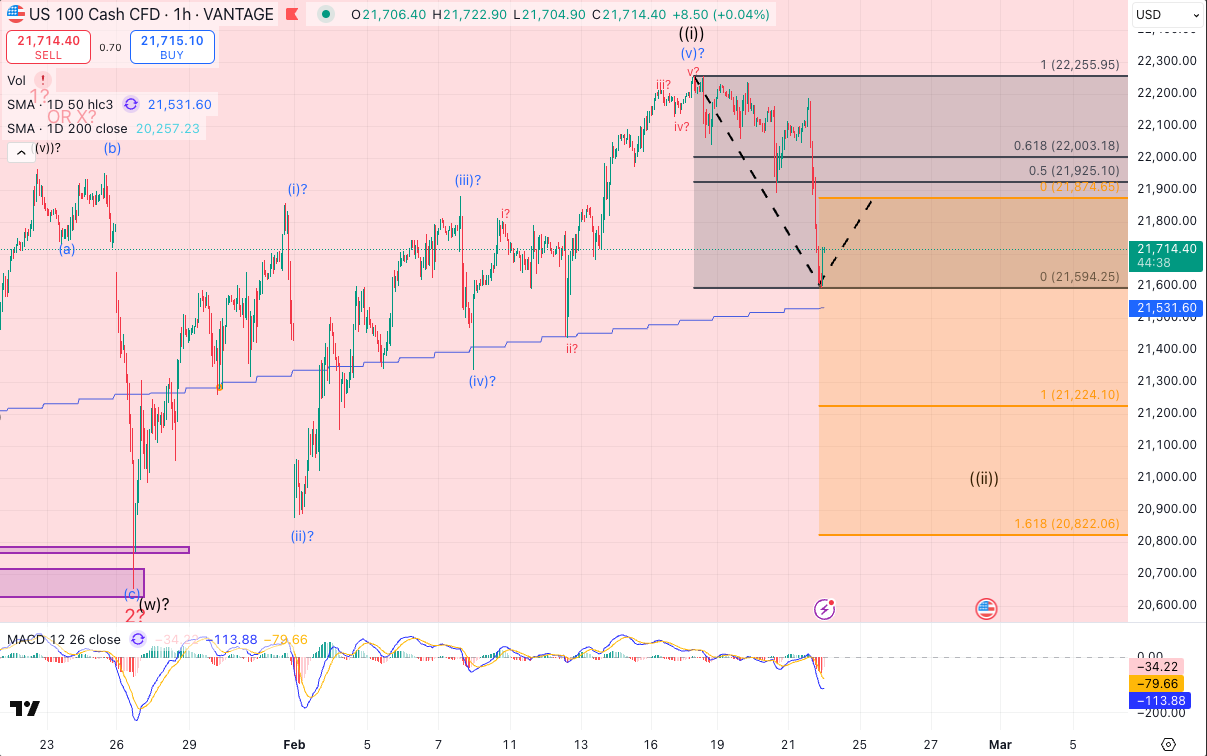

2. Equities: Fence-Sitting Mode

Equity market rotations are widening, 50% of sectors up vs. just 25% in recent years, but without a real selloff yet. The Russell 2000 is breaking down, putting markets on a knife edge. A final push higher is possible, but a selloff looms large. With Nvidia’s earnings (Wednesday) and CB Consumer Confidence (Tuesday) on deck, traders should prepare for a sharp directional move. The broader tech sector remains under pressure, especially with China’s continued focus on semiconductor competition and AI advancements.

3. China Tech & Global Investment Flows

China’s tech sector is outperforming, but valuations remain depressed compared to US peers. Investment flows are shifting, though it’s too early to call it a structural move away from US markets. Tariff concerns remain a wildcard, with March deadlines approaching for key trade policies that could impact global supply chains. The weaker yuan is also playing a role in attracting capital to Chinese markets, as investors seek higher relative growth rates.

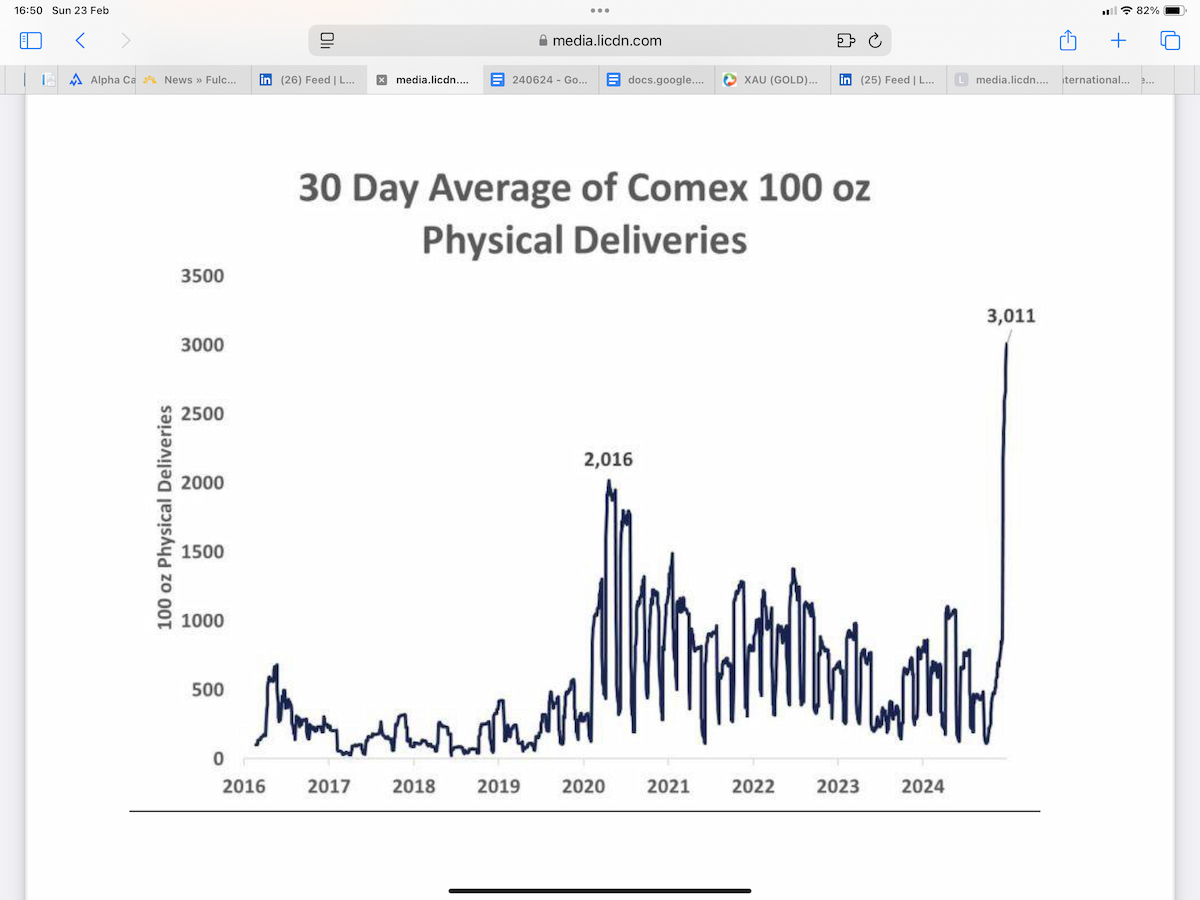

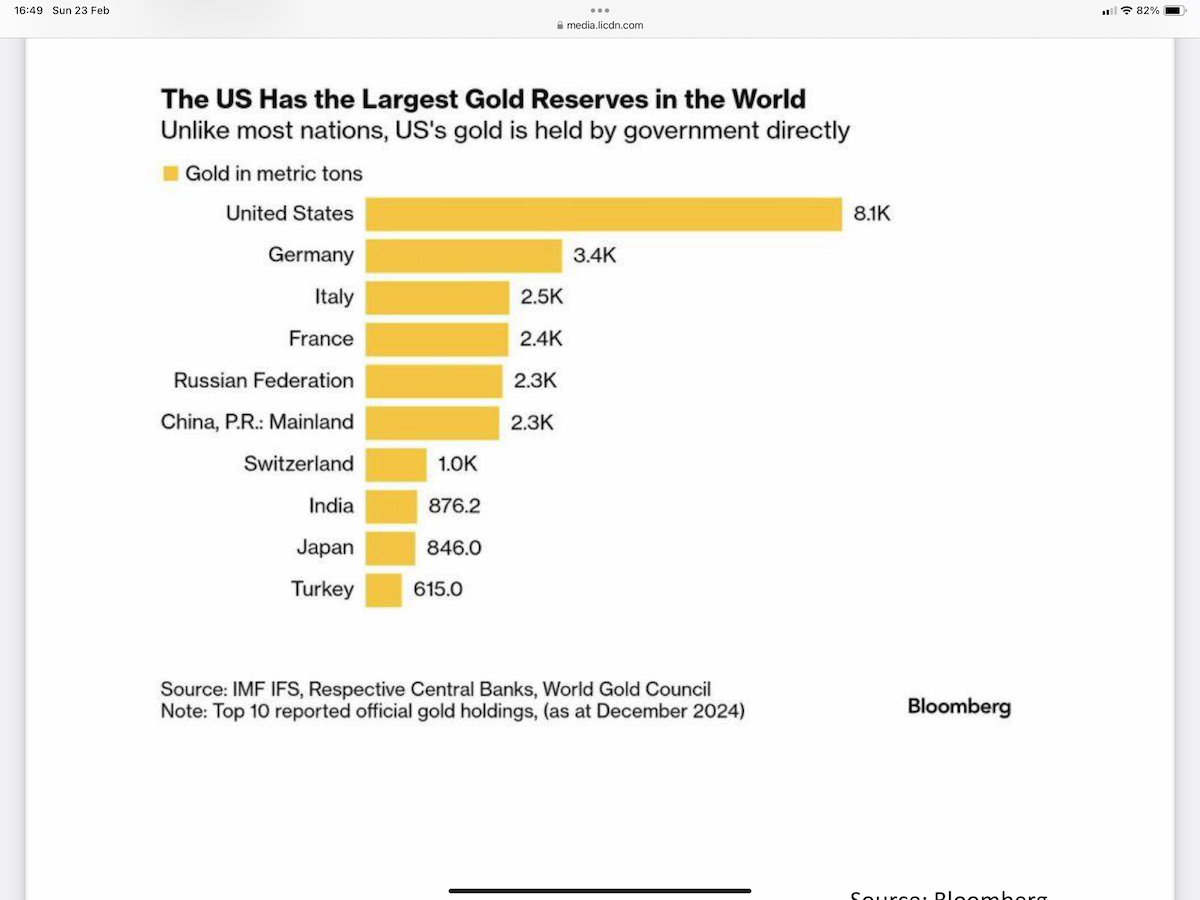

4. Gold: ATHs & Market Dislocations

Gold has hit new all-time highs, fueled by physical delivery demands and central bank buying. Futures spreads are flashing warning signals of arbitrage opportunities driven by shortages. With the March-April tariff decision looming, gold’s role as a safe haven remains solid, but price action could be volatile if supply chain pressures ease. The widening spread between futures and spot prices suggests continued stress in the market, with delivery constraints adding fuel to the rally.

Technical & Sentiment Analysis

Bond Markets

Volatility is finally showing signs of life, confirming Friday’s breakout. The lack of clarity on Fed policy remains a major overhang.

Equities

Sentiment is at a coin flip, market structure suggests either a final push higher or a fast drop. Increased hedging activity among institutional players suggests caution.

Commodities

Oil traders skeptical on OPEC+ supply delays; gold remains bid on geopolitical tensions and delivery constraints.

Last Week’s Recap: Key Events & Earnings

Bond Markets

Volatility is finally showing signs of life, confirming Friday’s breakout. The lack of clarity on Fed policy remains a major overhang.

Equities

Sentiment is at a coin flip, market structure suggests either a final push higher or a fast drop. Increased hedging activity among institutional players suggests caution.

Commodities

Oil traders skeptical on OPEC+ supply delays; gold remains bid on geopolitical tensions and delivery constraints.

The Week Ahead: Key Market Events

Tuesday

CB Consumer Confidence, Can it recover after the Michigan collapse?

Wednesday

Nvidia Earnings: A potential market mover, especially after recent weakness. AI-related spending will be a key focal point.

Thursday

US GDP Q4 (2nd read) & Durable Goods, Key data on economic momentum. Industrial production figures will provide insight into manufacturing resilience.

Friday

PCE Inflation Data, The Fed’s preferred inflation gauge, critical for rate expectations. The Fed’s next move could be influenced by this data point.

Actionable Takeaways

- Volatility is back. Traders should watch VIX and MOVE; bond volatility is now in play, and liquidity remains thin.

- Equity markets are at an inflection point. Nvidia earnings could determine short-term direction, with semiconductors and AI stocks under scrutiny.

- Gold is flashing warning signs. Physical delivery stress and futures spreads suggest ongoing market dislocations, but speculative flows could exaggerate moves.

- Watch the Consumer. Confidence data is shaky, and Friday’s PCE will be critical for rate expectations. Wage growth data could provide additional clues.

Key Trades to Watch

- Long volatility. MOVE & VIX positioning suggests a breakout setup. Consider structured option plays.

- Short Russell 2000. Small caps breaking down could be the first real sign of equity weakness. Look for key support levels.

- Gold spreads. Dislocations present arbitrage opportunities, but the risk of mean reversion remains.

- Watch bond market reaction to PCE. A stronger-than-expected print could push yields higher, impacting risk assets.

Markets are primed for a pivotal week, stay sharp and position accordingly.