Rotation Intensifies, Volatility Returns

Markets enter the new week after a sharp reminder that leadership transitions are rarely quiet. What began as a continued rotation away from richly valued technology has evolved into a broader repricing of positioning, volatility, and cross-asset conviction. Systematic flows are driving price action while sector dispersion has widened across indices.

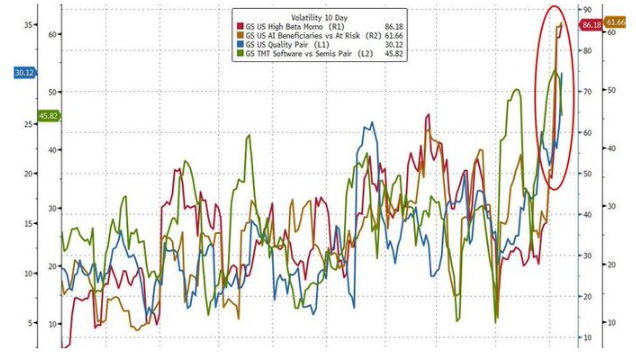

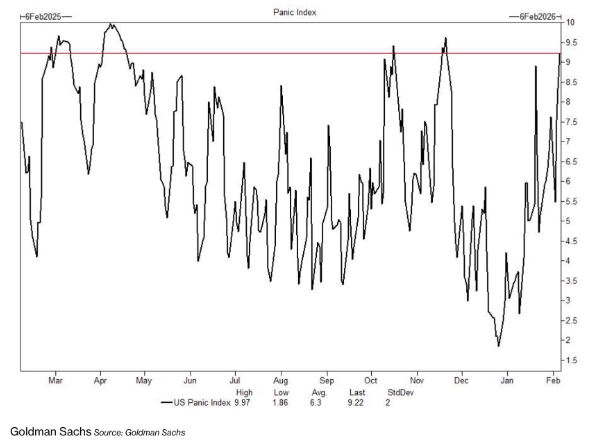

Short-gamma positioning has amplified recent price swings. Systematic selling pressure, short-gamma positioning, and elevated margin constraints have amplified swings, even as headline indices remain structurally supported. Recent volatility expanded alongside positioning resets in crowded trades.

Market Overview: Rotation Without Structural Damage

Equity structure remains intact while sector leadership has shifted. Technology multiples compressed as industrial and value sectors stabilised, resulting in wider performance dispersion without a breakdown in headline indices. The Dow’s breakout occurred alongside this internal rotation, reflecting divergence in sector performance rather than broad risk reduction.

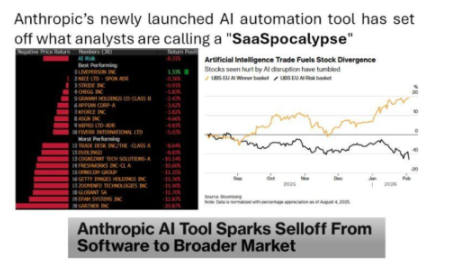

Pressure inside software and AI-linked names coincided with multiple compressions relative to other sectors. Earnings expectations remained comparatively stable while price performance diverged, reinforcing that recent moves reflect valuation adjustment rather than earnings deterioration. Sector dispersion increased, consistent with a market trading on rotation rather than synchronised momentum.

Volatility expanded alongside short-gamma positioning, increasing sensitivity to directional price swings. Relief rallies followed the volatility reset without altering the broader index structure, indicating that positioning adjustments — rather than structural breakdown — defined the week’s movement.

Recent price action reflects sector rotation and positioning-driven dispersion while headline index structure remains intact. Leadership divergence widened, consistent with an environment shaped by valuation resets and flow dynamics.

Macro & Policy Watch: Politics, Liquidity, and Rate Sensitivity

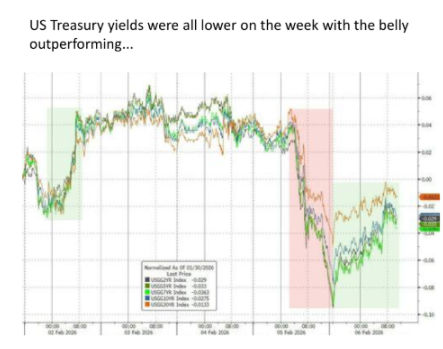

Cross-asset price action coincided with shifts in yields and currency markets during the week. Bond yields moved higher alongside broader asset volatility, reflecting rate-sensitive positioning rather than changes in earnings structure. Rate-sensitive assets reacted to these yield movements without altering the overall index structure.

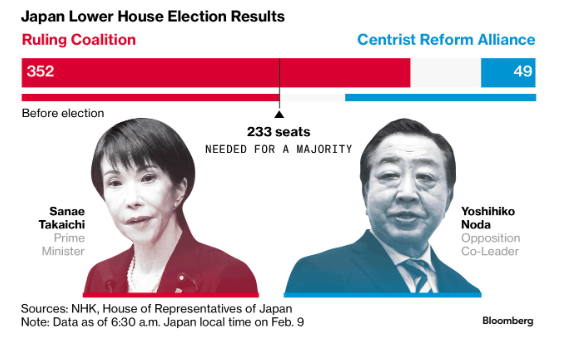

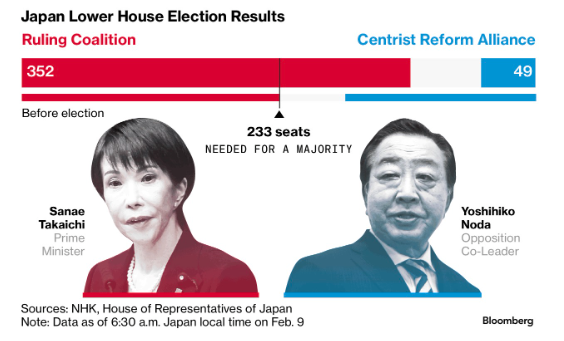

Japan’s election outcome was followed by equity strength, higher yields, and currency volatility. Portions of that initial move retraced later in the week, leaving cross-asset pricing aligned with positioning adjustments rather than a persistent directional shift. The sequence reflects how political developments coincided with rate and currency sensitivity across markets.

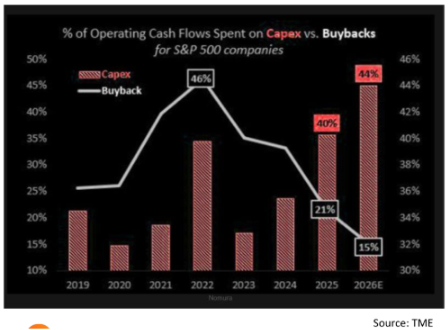

Corporate capital allocation trends showed elevated capital expenditure relative to shareholder returns. The technology sector multiples adjusted alongside this shift while earnings expectations remained comparatively stable, reinforcing that valuation dispersion occurred independently of earnings deterioration.

Commodity markets reflected positioning and liquidity adjustments during the repricing phase. Metals and resource-linked assets traded with elevated volatility consistent with cross-asset flow activity rather than a breakdown in underlying structure.

Technical & Sentiment Breakdown: Supportive, but Increasingly Fragile

Headline indices remained within broader uptrends while internal performance diverged. Sector dispersion widened alongside changes in positioning, reflecting uneven participation across industries rather than synchronised index momentum.

Systematic positioning influenced directional price swings as short-gamma exposure increased volatility sensitivity. Volatility-linked flows accelerated during the repricing phase, followed by relief rallies consistent with positioning resets rather than structural trend changes.

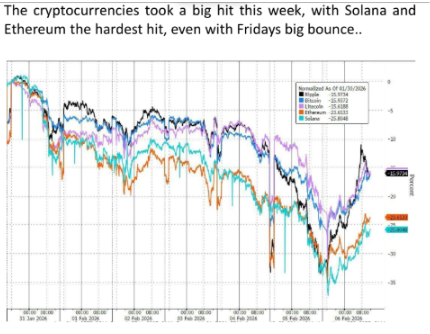

Crypto and metals experienced liquidation phases followed by stabilisation, aligning with cross-asset positioning adjustments. Price action reflected flow-driven unwinds rather than earnings or structural deterioration.

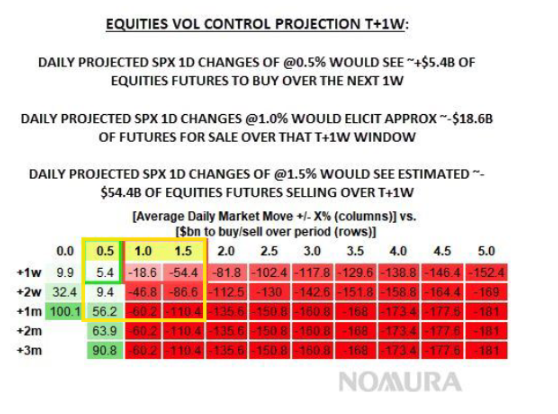

Volatility control activity and positioning flows remained active after the reset, reinforcing that recent movement was driven by mechanical exposure adjustments rather than directional trend continuation.

Last Week’s Recap: Rotation Shock, Volatility Reset

Last week illustrated how quickly positioning and liquidity conditions can reshape leadership without breaking the broader market structure.

Key Highlights

Macro

Bond yields pushed higher amid fiscal and political sensitivity, tightening financial conditions at the margin. Markets interpreted this less as growth deterioration and more as liquidity friction, reinforcing volatility across risk assets.

China

Seasonal demand shifts around the Lunar holiday appeared to influence metals flows, particularly copper, highlighting how regional activity changes can ripple into global commodity pricing.

Earnings

Forward expectations for major growth sectors remained broadly stable despite price volatility. The disconnect between earnings resilience and multiple compression underscores that valuation adjustment, not earnings collapse, is driving performance dispersion.

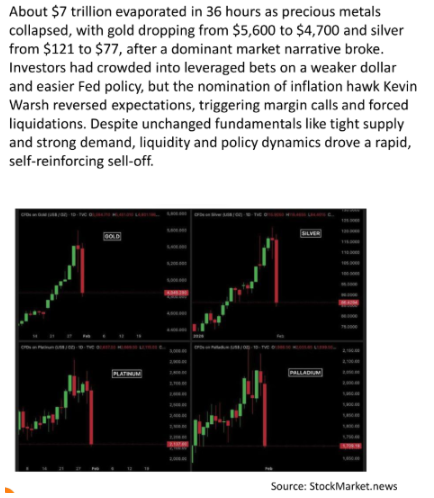

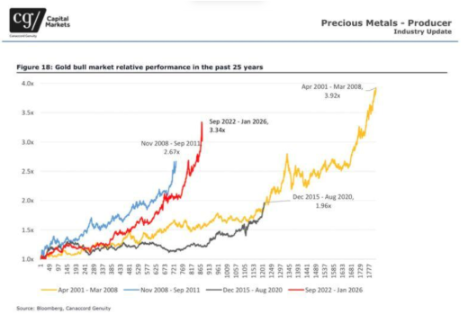

Commodities

Gold and silver volatility reflected physical market dynamics colliding with futures positioning and margin pressures. The pricing disconnect between regional trading venues reinforced liquidity sensitivity.

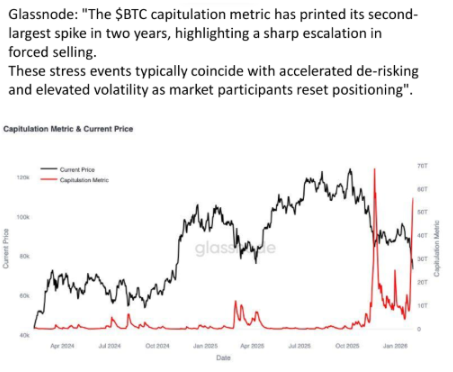

Crypto

Crypto experienced a broad liquidation phase consistent with deleveraging and sentiment washout. Stabilisation late in the week suggests forced selling rather than structural abandonment.

Oil

Energy markets remained range-bound as supply commentary and geopolitical considerations balanced demand concerns, reinforcing consolidation rather than directional conviction.

The Week Ahead: Key Data and Market-Moving Signals

This week clusters labour market releases, inflation data, consumer activity, and central bank communication, a mix that directly shapes rate expectations and liquidity conditions. With positioning already sensitive, the concentration of macro catalysts increases the probability of volatility bursts rather than isolated reactions.

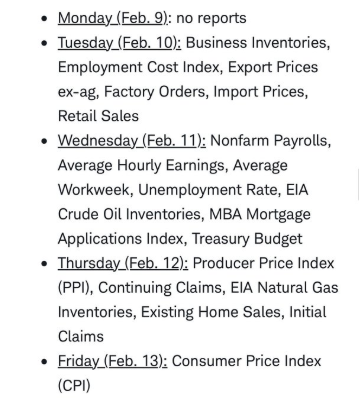

Monday, February 9

- Japan: Economy Watchers Current Index

- Eurozone: Sentix Investor Confidence

- US: CB Employment Trends Index

- ECB: Lagarde speaks

- Fed: Waller speaks

- US: Treasury Bill Auctions

Tuesday, February 10

- US: Retail Sales

- US: Core Retail Sales

- US: Employment Cost Index

- US: ADP Employment

- Fed: Logan speaks

- US: 3-Year Treasury Auction

Wednesday, February 11

- China: CPI

- China: PPI

- US: Nonfarm Payrolls

- US: Unemployment Rate

- US: Average Hourly Earnings

- Fed: Bowman speaks

- Earnings: Cisco Systems

- US: 10-Year Treasury Auction

Thursday, February 12

- UK: GDP (Monthly & Quarterly)

- US: Initial Jobless Claims

- US: Existing Home Sales

- ECB: Cipollone speaks

- Earnings: Alibaba

Friday, February 13

- US: CPI

- US: Core CPI

- Eurozone: GDP

- Eurozone: CPI

- BoE: Pill speaks

Alpha Takeaway: Rotation Continues, Discipline Matters

Markets remain structurally supported, but leadership transition and volatility dynamics are redefining participation. Liquidity sensitivity, not macro collapse, is driving the tape.

Equities

Rotation away from concentrated growth toward industrial and value exposures continues. Structure holds, but volatility favours selective positioning over broad beta.

Gold & Silver

Metals remain volatile amid physical demand signals and futures positioning adjustments. Pricing swings reflect liquidity dynamics more than structural trend change.

Crypto

Liquidation appears driven by positioning washout. Stabilisation suggests a tactical reset phase rather than renewed momentum.

Macro

Rate pressure, political developments, and systematic flows are shaping near-term price action. Liquidity conditions remain the dominant transmission channel.

The market is not breaking; it is repricing participation. Elevated volatility is a reminder that structural support does not eliminate tactical risk, and disciplined exposure matters most when flows drive the narrative.