Breadth Expands, Growth Persists, Volatility Remains Dormant

Markets continue to lean on structure rather than momentum as the year settles into its first full trading rhythm. The past week reinforced a tone of stability, with participation quietly improving beneath the surface even as headline indices paused rather than pushed higher. Liquidity remains available, and once again, the absence of forced selling proved more influential than any individual data point.

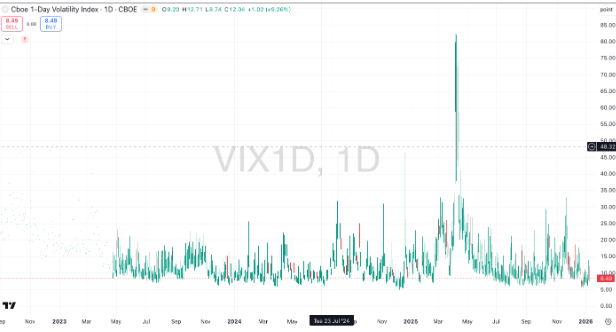

At the same time, calm should not be mistaken for conviction. Volatility remains compressed across asset classes, sentiment has improved from late-year caution, and expectations are beginning to rise. This creates a constructive but delicate backdrop—one where markets are increasingly sensitive to disappointment rather than insulated from it.

Market Overview: Rotation Over Acceleration

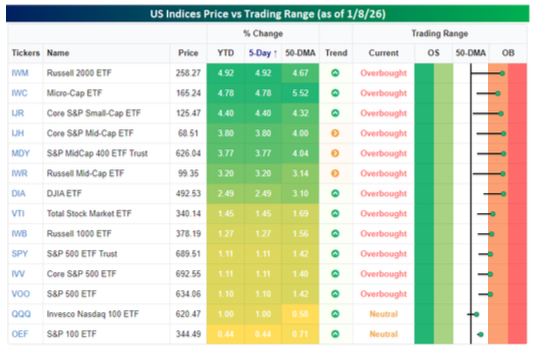

Equity markets remain supported, with trend structure intact and internal participation broadening. This has not been a momentum-driven surge or a valuation-led expansion. Instead, the market is redistributing leadership, rotating away from narrow concentration and toward smaller caps and equal-weight exposure.

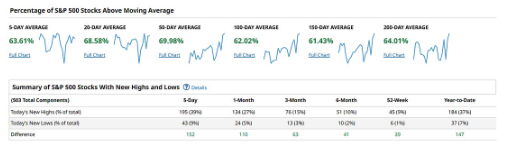

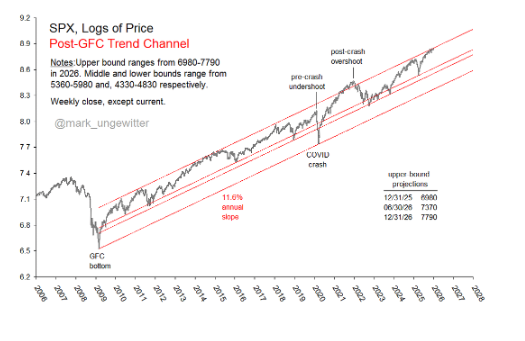

This shift suggests engagement is widening rather than intensifying. The S&P 500 continues to trade comfortably above its longer-term moving averages, reinforcing the view that the broader trend remains functional even as upside momentum moderates.

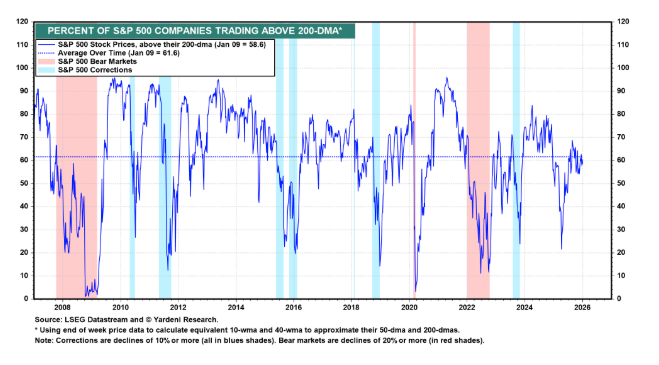

Breadth data adds weight to this interpretation. A growing share of constituents remain above short-, medium-, and long-term averages, indicating that price action is being supported by participation across the index rather than carried by a shrinking group of leaders.

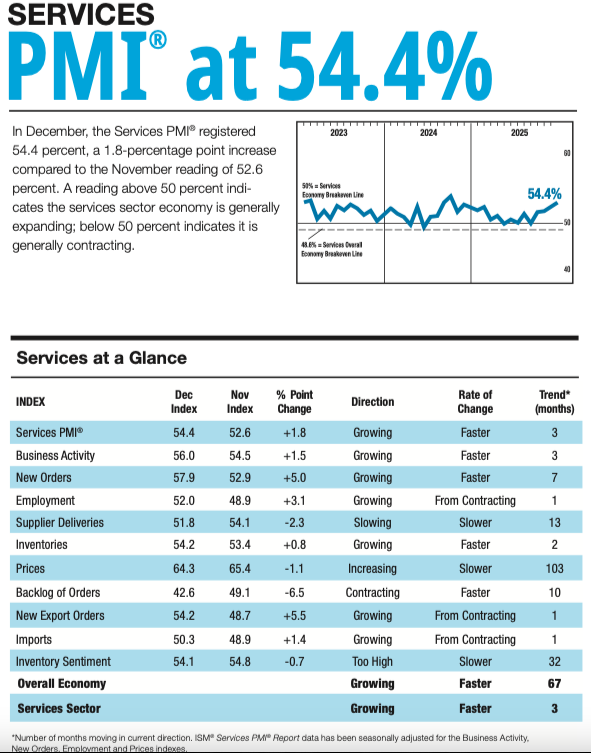

At the macro level, growth continues to provide the underlying cushion. Services activity remains the dominant driver, offsetting softness elsewhere and keeping real-time growth estimates elevated.

Macro & Policy Watch: Growth Holds as Policy Stays Active

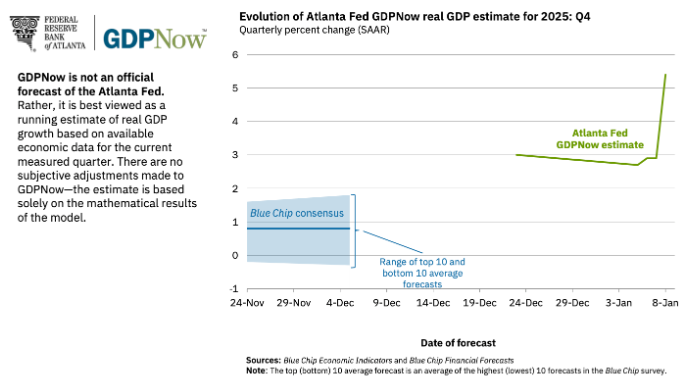

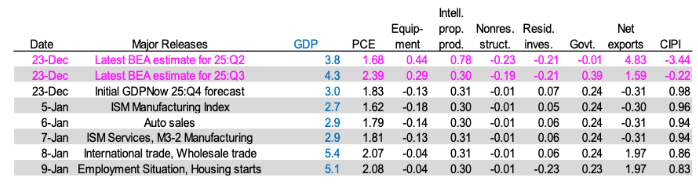

Macro data over the week reinforced resilience rather than reacceleration. Real-time GDP tracking moved sharply higher, driven primarily by services and consumption, even as housing-related investment remained a drag on the overall picture.

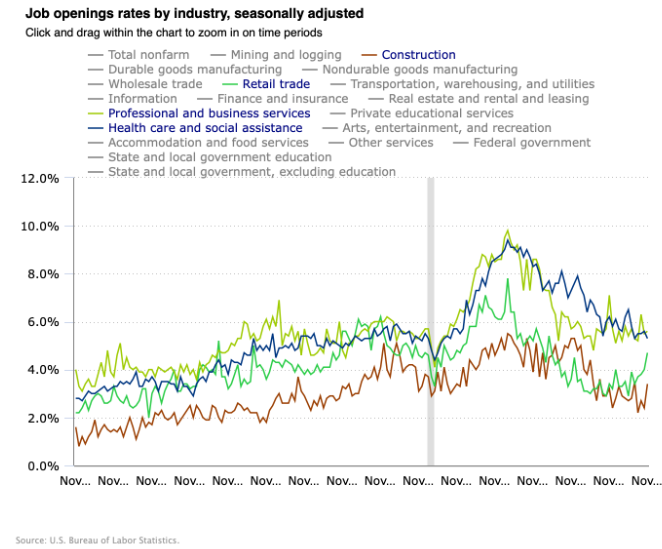

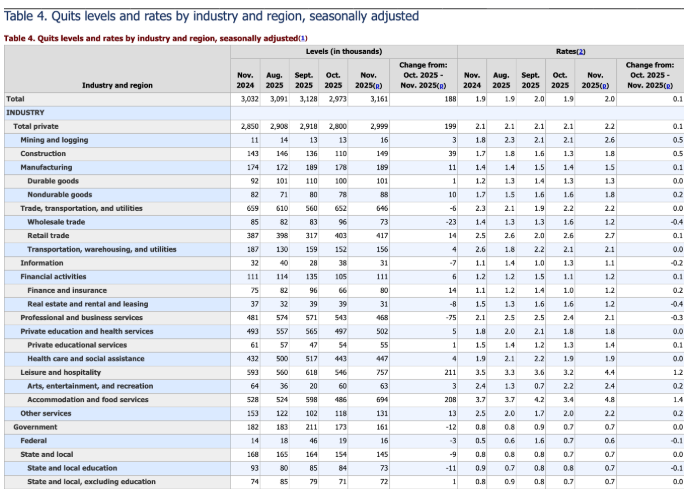

The labour market continues to reflect adjustment rather than deterioration. Job openings declined, but layoffs remained contained, while quits increased—suggesting mobility and churn rather than stress or contraction.

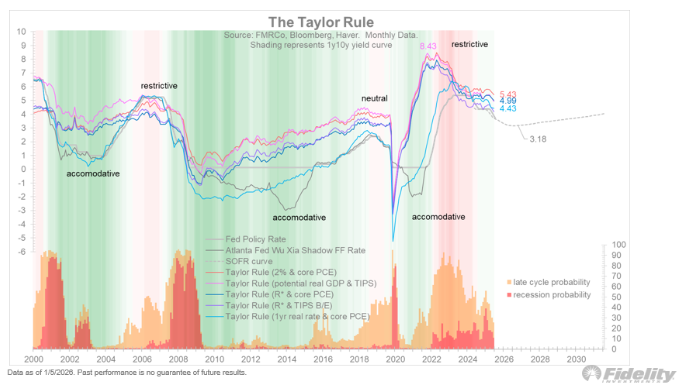

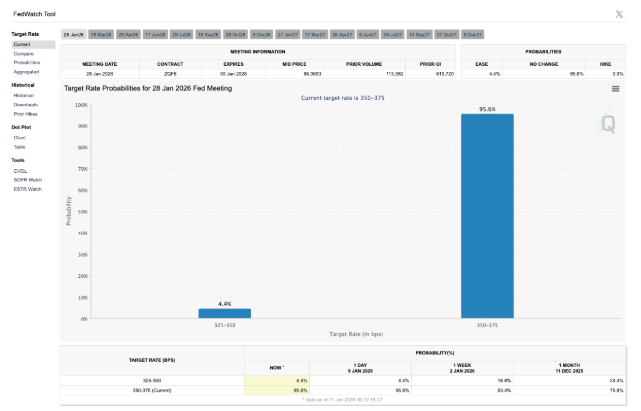

Policy framing remains broadly accommodative. Rate expectations continue to align with rules-based frameworks, pointing toward lower policy settings over time, even as near-term cuts are repriced out of the immediate horizon.

Alongside growth and rates, resources remain a recurring macro anchor. Control of supply chains, energy flows, and strategic commodities continues to intersect with inflation dynamics and broader policy considerations.

Technical & Sentiment Breakdown: Supportive, but Increasingly Fragile

From a technical perspective, the structure remains intact. Major indices continue to respect trend channels and key moving averages, with pullbacks remaining contained and corrective rather than impulsive.

Momentum, however, has slowed meaningfully. This is visible not through breakdowns, but through consolidation near highs and increasing dispersion beneath the index surface. Leadership churn has replaced directional thrust.

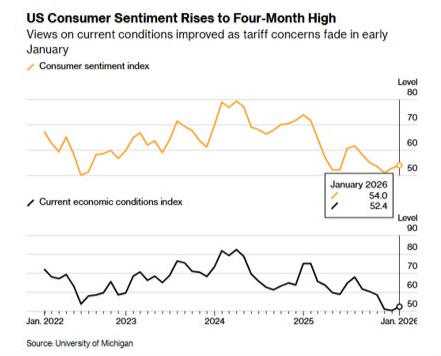

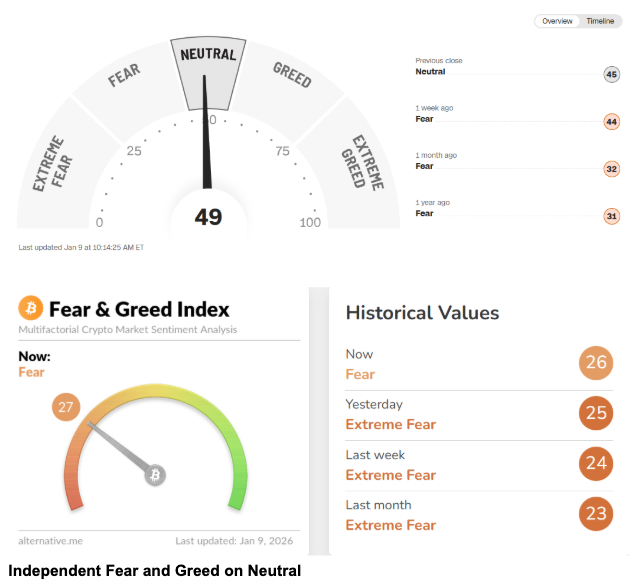

Sentiment reflects this balance. Indicators have improved from late-year caution but remain closer to neutral than exuberant. Historically, this zone tends to leave markets more reactive to shocks than resilient to them.

Volatility remains deeply suppressed across both equity and rates markets. While this has supported drift and carry strategies, dispersion suggests that risk is being stored internally rather than expressed outright.

Last Week’s Recap: Growth Holds, Volatility Stays Compressed

Markets moved through the week with little visible stress, even as participation improved and expectations edged higher. Data generally supported growth, while positioning and flows continued to matter more than conviction. Beneath the calm, however, several familiar fault lines remained unresolved.

Key Highlights:

Macro:

Growth data surprised positively, led by services activity and real-time GDP tracking. Housing and manufacturing remained uneven, but the absence of forced selling or rate stress allowed equities to maintain structure. Liquidity continued to cushion downside rather than accelerate upside.

China:

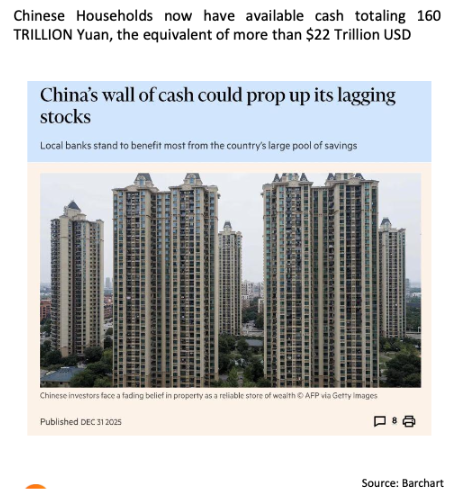

China remained relevant primarily through commodity and trade channels rather than headline macro releases. Demand dynamics continued to influence metals and industrial inputs, reinforcing China’s role as a marginal driver rather than a directional catalyst.

Earnings:

Earnings remained the underlying anchor for equities. Profit trends continued to support market structure, even as leadership rotated and valuation dispersion widened beneath the surface.

Commodities:

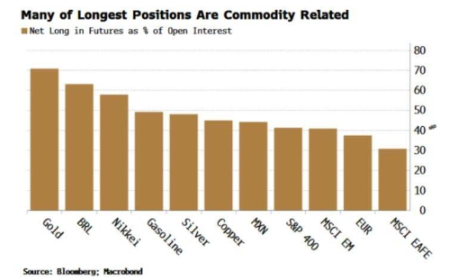

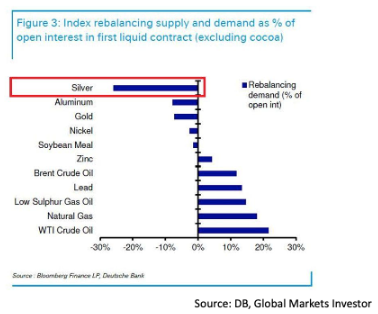

Hard assets continued to attract attention, supported by flow dynamics and re-weighting effects. Price action remained constructive, but positioning suggests sensitivity to sentiment shifts rather than speculative excess.

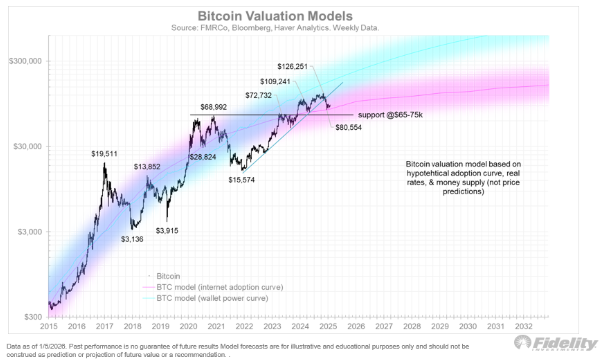

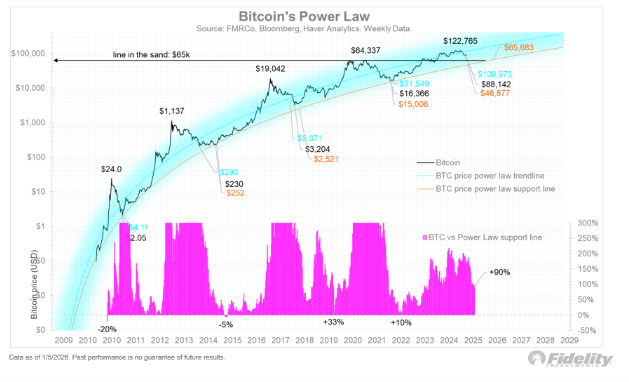

Crypto:

The crypto price action resembled consolidation rather than a reversal. Valuation support held, but positioning remained heavy, keeping conviction contained and volatility muted.

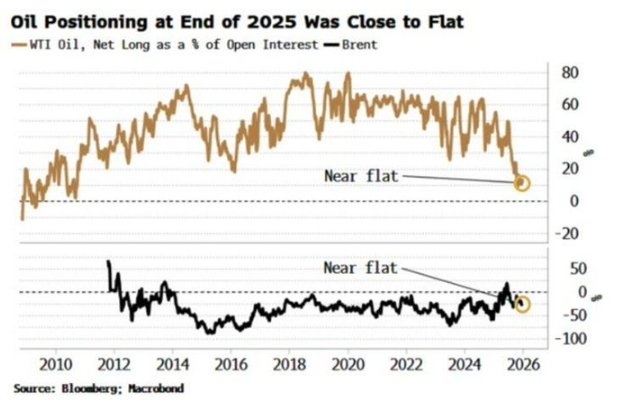

Oil:

Energy markets remained capped by sentiment despite ongoing geopolitical relevance. Positioning stayed relatively negative, leaving oil responsive to flow changes rather than fundamentals alone.

The Week Ahead: Key Data and Market-Moving Signals

With liquidity largely restored, the coming week brings a dense and globally relevant run of macro data. U.S. CPI on Tuesday and PPI on Wednesday sit firmly at the centre of the calendar, while UK GDP, bank earnings, and Asia-Pacific data feature prominently across growth, inflation, and activity trends. With positioning elevated and volatility compressed, how markets react to confirmation or disappointment may matter more than the releases themselves.

Monday, January 12

- Japan: Market Holiday (Coming of Age Day)

- Europe: Sentix Investor Confidence

- Europe: German Current Account

- US: Employment Trends Index

- US: Treasury Auctions (3Y, 10Y)

Tuesday, January 13

- New Zealand: Business Confidence, Capacity Utilisation

- Australia: Consumer Sentiment

- Japan: Current Account, Bank Lending

- UK: BRC Retail Sales

- US: CPI (Headline & Core)

- US: Real Earnings

- US: NFIB Small Business Optimism

- US: JPMorgan Earnings

Wednesday, January 14

- China: Trade Balance, Exports, Imports

- China: Credit Data (Loans, TSF, M2)

- Japan: Machine Tool Orders

- US: PPI (Headline & Core)

- US: Retail Sales

- US: Existing Home Sales

- US: Crude Oil Inventories

- US: Bank of America, Wells Fargo, Citi Earnings

- US: Supreme Court Opinion on Tariffs (Tentative)

Thursday, January 15

- Japan: PPI

- South Korea: Rate Decision

- UK: GDP, Industrial & Manufacturing Production

- Eurozone: CPI (France, Spain, Italy)

- US: Jobless Claims

- US: Regional Manufacturing Surveys

- US: BlackRock, Morgan Stanley, Goldman Sachs Earnings

Friday, January 16

- New Zealand: PMI

- Europe: German & Italian CPI

- US: Industrial Production

- US: Capacity Utilisation

- US: NAHB Housing Market Index

Alpha Takeaway: Constructive Structure, Rising Sensitivity

Markets remain supported, but not comfortable. Structure and liquidity continue to do the heavy lifting for risk assets, while confidence in prevailing narratives is being tested rather than reinforced. Price action remains orderly, but the margin for error is narrowing as expectations rise.

Equities:

Broadening participation continues to support the trend, but leadership rotation suggests upside is becoming increasingly selective rather than broad-based. This remains a market that rewards positioning and patience rather than indiscriminate exposure.

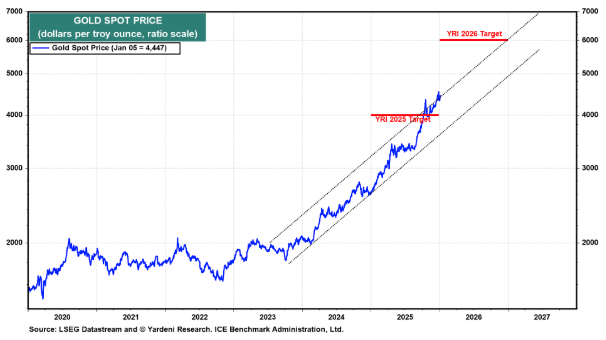

Gold & Silver:

Hard assets remain supported by structural and flow-driven dynamics. While positioning may introduce near-term volatility, the underlying bid remains intact, particularly as confidence in long-duration assets remains uneven.

Crypto:

Price action continues to resemble consolidation rather than reversal. Valuation support is present, but conviction remains uneven, suggesting the market is still working through positioning rather than attracting fresh directional flow.

Macro:

Growth remains resilient, policy remains active, and volatility remains compressed. This combination continues to favour engagement, but also leaves markets increasingly sensitive to disappointment when expectations are elevated.

This still feels like a grind higher—until it doesn’t. Flows decide direction, but crowded trades tend to unwind quietly before they unwind abruptly.