Geopolitics Re-Emerges, Growth Holds, Complacency Builds Quietly

Markets opened the week under a cloud of political and geopolitical headlines, yet price action remained notably contained. Early defensive flows emerged, but they failed to translate into sustained stress across rates or equities. Liquidity continued to circulate, volatility stayed compressed, and participation remained broadly intact beneath headline indices that largely moved sideways.

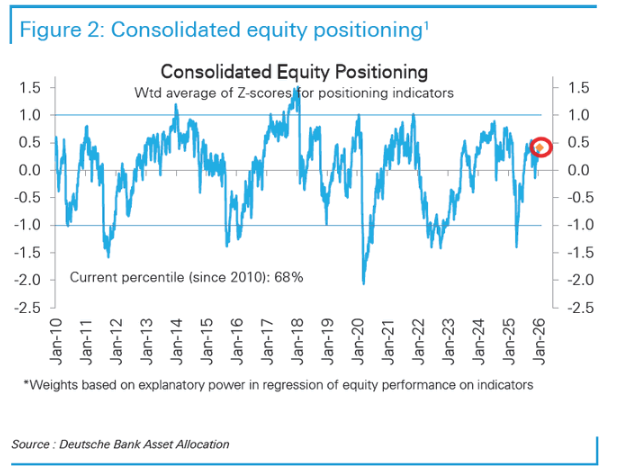

That calm, however, should not be mistaken for comfort. Positioning remains extended in places, hedging is thin, and expectations have adjusted higher even as headline risk has increased. The backdrop remains constructive, but increasingly sensitive—one where stability depends more on the absence of shocks than on fresh conviction.

Market Overview: Rotation, Not Retreat

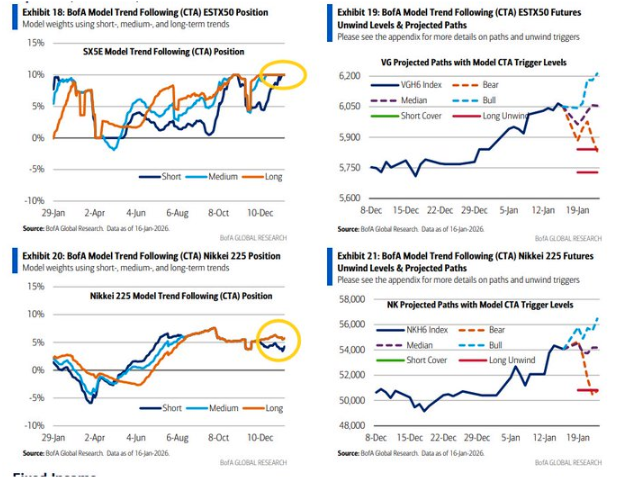

Equity structure remains intact, supported by participation rather than acceleration. The market is not pushing higher through momentum; instead, leadership continues to rotate. Selling pressure has been visible in concentrated areas, while equal-weight and smaller-cap exposure has absorbed flows more effectively.

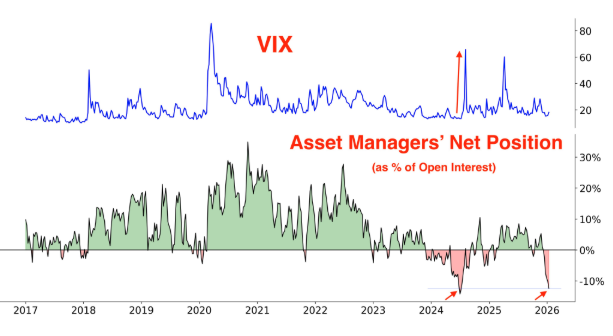

This redistribution of leadership reinforces the view that engagement is broadening rather than intensifying. Importantly, this has occurred without material deterioration in overall positioning. Hedge fund activity points to caution, not capitulation, reinforcing the idea that risk is being managed rather than exited.

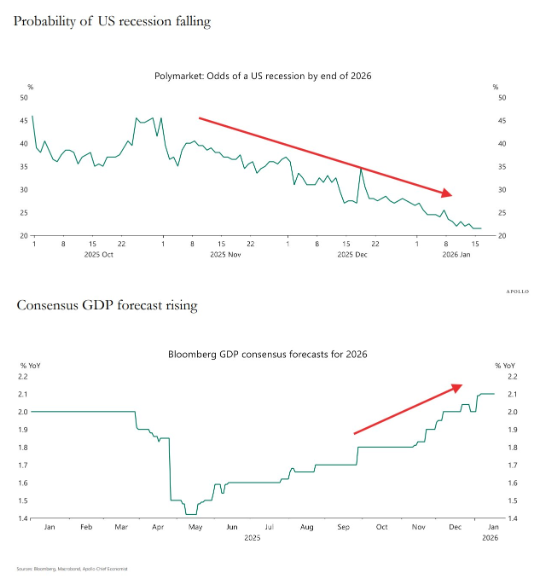

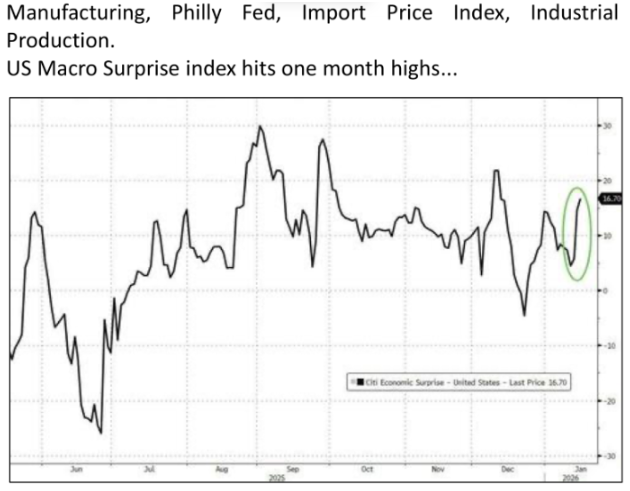

At the macro level, growth continues to underpin this structure. Surprise indices remain positive, and recession probabilities have moved lower, helping cushion equity markets even as geopolitical noise increases

Macro & Policy Watch: Politics Loud, Markets Measured

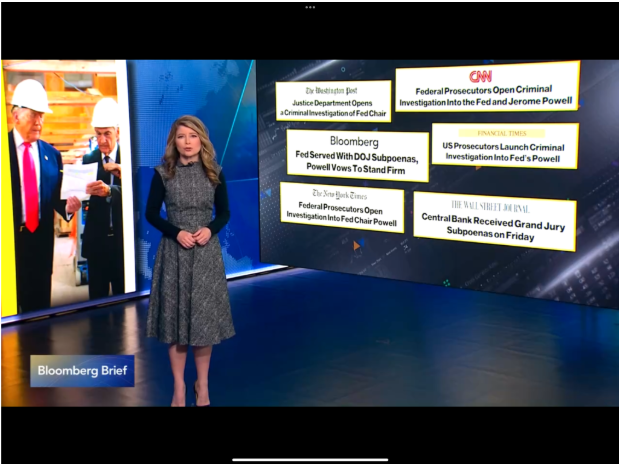

Policy and geopolitics dominated the narrative, but markets remained disciplined in their response. Political pressure surrounding central bank independence generated significant attention, yet yields moved only marginally. Global central bank support helped stabilise expectations and contain spillover risk.

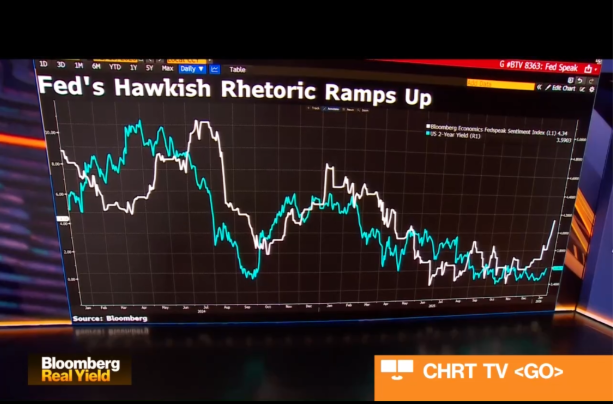

Rates continue to reflect this restraint. Despite hawkish policy rhetoric, the front end has yet to reprice fully, highlighting the gap between commentary and market conviction.

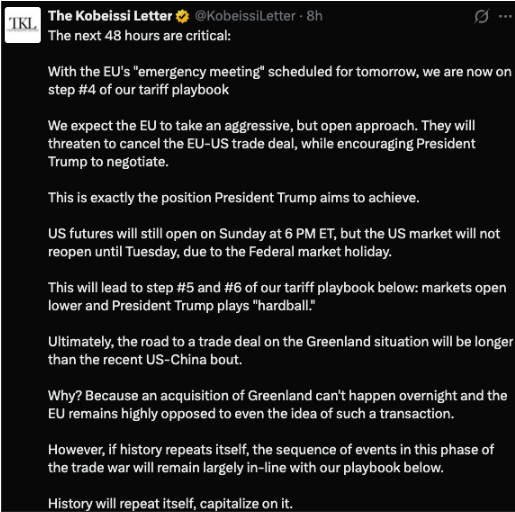

On the geopolitical front, tariff threats and strategic manoeuvring followed a familiar escalation pattern. Price action suggests these episodes were treated as episodic, reinforcing the market’s tendency to view such developments as conditional.

Technical & Sentiment Breakdown: Supportive, but Increasingly Fragile

From a technical perspective, trend structure remains functional. Major indices continue to hold key levels, and pullbacks have been corrective rather than impulsive. However, momentum has slowed, and dispersion beneath the surface has increased.

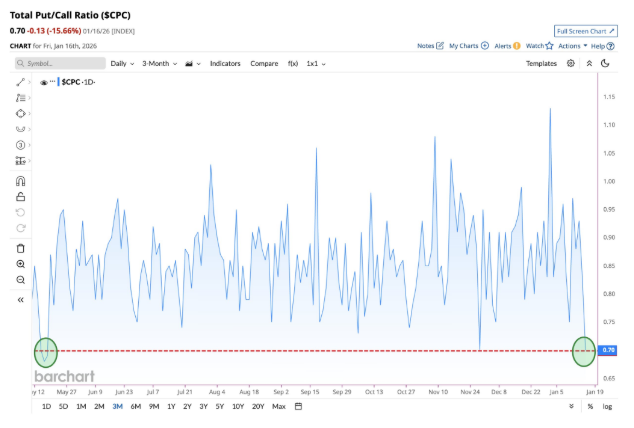

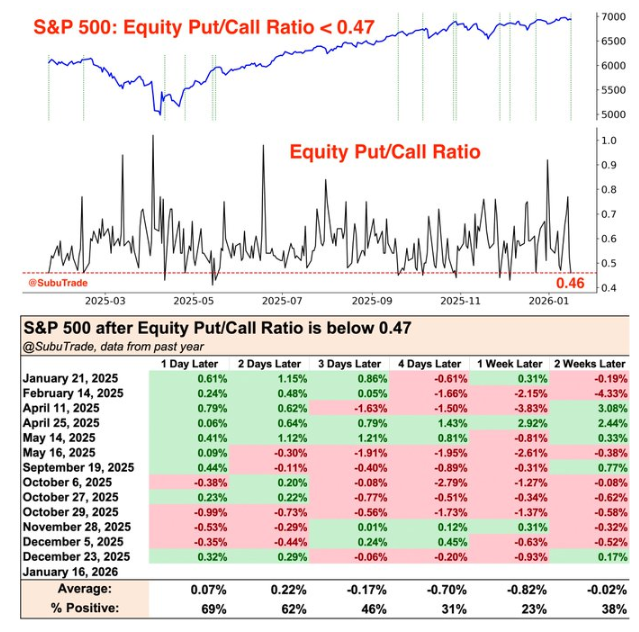

Sentiment indicators point to rising confidence, but protection remains limited. Put-call ratios are low, and volatility is suppressed across both equity and rates markets—conditions that support carry but reduce resilience to surprise.

Volatility measures remain calm, yet this calm sits alongside elevated geopolitical risk, increasing the likelihood that any shock could travel further than expected.

Overall positioning remains bullish but not extreme, reinforcing the idea that complacency—not excess—is the more immediate vulnerability.

Last Week’s Recap: Stability Holds, Fault Lines Remain

Markets navigated the week with little visible stress despite a heavy headline load. Data generally reinforced growth resilience, while flows and positioning continued to matter more than outright conviction. Beneath the surface, familiar pressure points remained unresolved.

Key Highlights:

Macro:

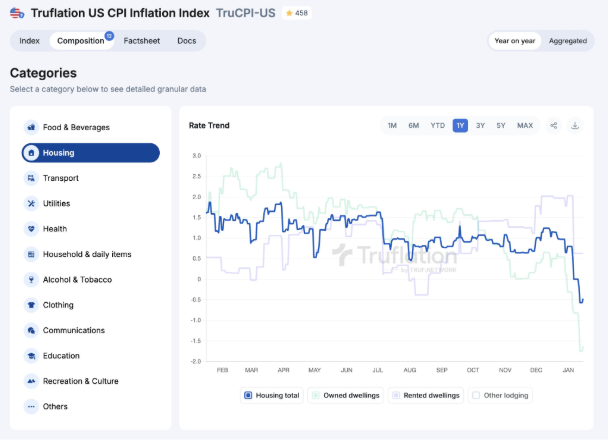

Inflation data remained benign, with headline releases failing to generate renewed rate stress. Alternative inflation measures reinforced the view that price pressures remain contained for now.

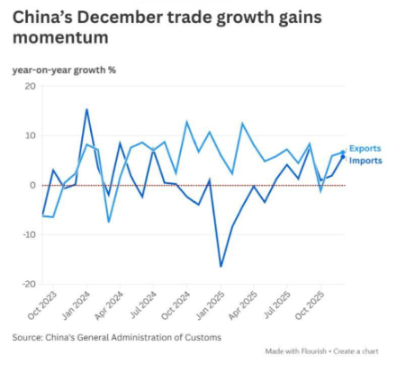

China:

Trade dynamics remained supportive, with external demand adjusting rather than contracting. China’s influence continued to operate more through commodities and trade channels than through headline macro shifts.

Earnings:

Early earnings confirmed a low-bar environment. Financials struggled to deliver positive surprises despite solid absolute results, keeping leadership concentrated elsewhere.

Commodities:

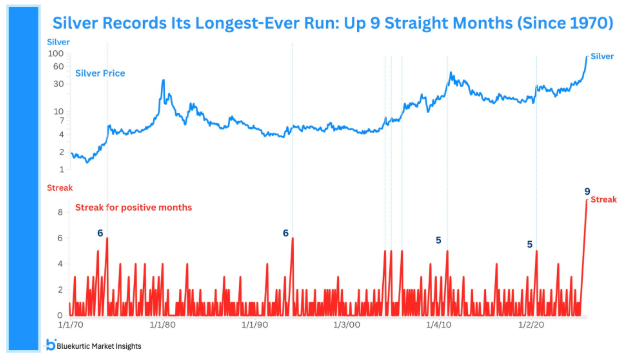

Precious metals remained well supported amid geopolitical uncertainty. Price action stayed constructive, though positioning suggests sensitivity to sentiment shifts rather than speculative excess.

Crypto:

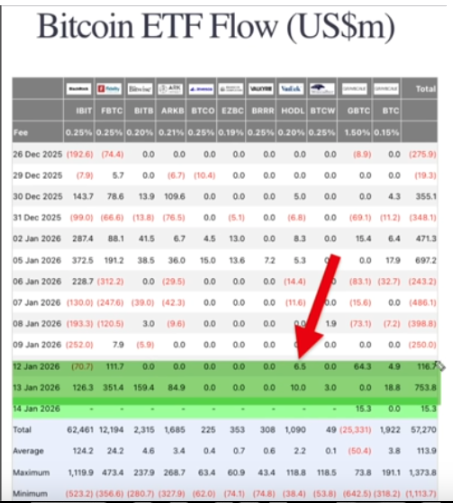

Digital assets stabilised following prior selling pressure. Flow dynamics suggest sellers have eased, though overhead supply remains a consideration.

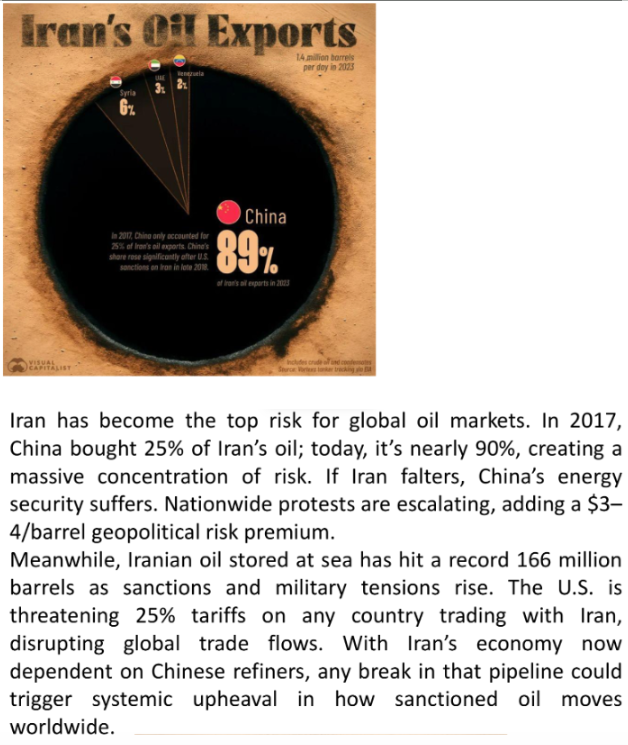

Oil:

Energy markets continued to react to geopolitical headlines, with price action driven more by risk premia than by underlying supply dynamics.

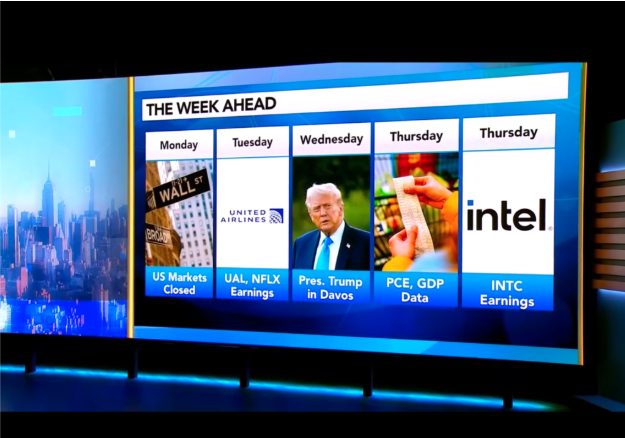

The Week Ahead: Key Data and Market-Moving Signals

With U.S. cash markets closed on Monday, early direction is set by futures and a heavy overseas data slate. The focus then shifts to China’s activity dump, UK inflation, U.S. growth and PCE, Japan policy, and global PMIs, with Davos headlines running in the background throughout the week.

Monday, January 19

- US: Market Holiday (Martin Luther King Jr. Day)

- China: GDP (Q4 YoY & QoQ)

- China: Retail Sales

- China: Industrial Production

- China: Fixed Asset Investment

- China: NBS Press Conference

- Eurozone: CPI (Headline & Core)

- Global: World Economic Forum (Davos)

Tuesday, January 20

- China: Loan Prime Rate (1Y, 5Y)

- Eurozone: ZEW Economic Sentiment (Germany, Eurozone)

- US: Treasury Bill Auctions (3M, 6M, 52W)

Wednesday, January 21

- UK: CPI (Headline & Core)

- UK: PPI, RPI

- US: Construction Spending

- US: Pending Home Sales

- US: MBA Mortgage Applications

- US: Atlanta Fed GDPNow

- US: 20-Year Treasury Auction

- US: President Speaks

- Global: World Economic Forum (Davos)

Thursday, January 22

- US: GDP Revision (Q3)

- US: PCE Prices (Headline & Core)

- US: Personal Income & Spending

- US: Jobless Claims

- US: Corporate Profits

- US: Crude Oil Inventories

- US: 10-Year TIPS Auction

- Eurozone: ECB Monetary Policy Account

- Australia: Employment

- New Zealand: CPI

Friday, January 23

- Japan: BOJ Policy Decision

- Japan: CPI

- Japan: BOJ Press Conference

- Global: Flash PMIs (US, Eurozone, UK, Japan)

- US: Michigan Consumer Sentiment & Inflation Expectations

Alpha Takeaway: Constructive Structure, Narrowing Margin for Error

Markets remain supported, with structure holding as volatility stays compressed and positioning remains elevated. Growth continues to cushion risk assets, while hedging remains limited.

Equities:

Rotation continues to dominate. Broad participation supports the trend, but leadership remains selective, favouring positioning over indiscriminate exposure. Trump’s Greenland push has created a risk off start to the week which sits in a seasonally weak period in mid-term presidential market years. Look to build longs into deeper pullbacks.

Gold & Silver:

Precious metals remain underpinned by geopolitical and macro uncertainty. While extended positioning may introduce near-term volatility, the underlying bid remains intact.

Crypto:

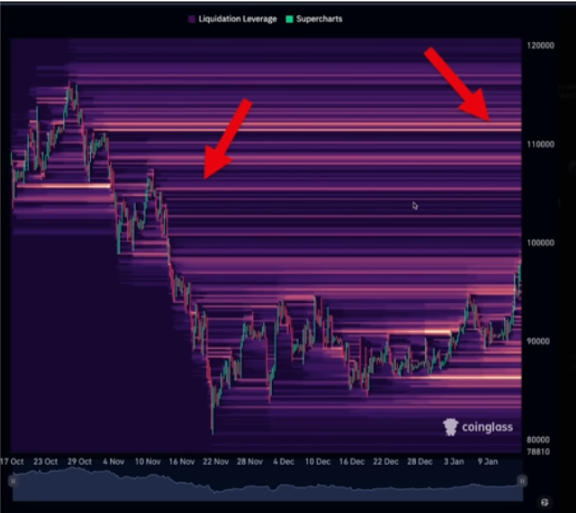

Price action suggests consolidation rather than reversal. Support has held, but conviction remains uneven as the market works through positioning.

Macro:

Growth resilience, contained inflation pressures, and active policy continue to define the backdrop. This mix supports engagement but leaves markets more reactive when expectations rise.

The structure remains constructive, but the tolerance for surprise is narrowing. Calm conditions persist—yet they rest on increasingly thin protection.