Growth Still Leads, Rotation Deepens, Volatility Lurks

Markets enter the week with a familiar tone: constructive, but increasingly selective. Despite a steady flow of geopolitical, policy, and rates-related headlines, price action has remained broadly contained. Drawdowns have been shallow, rebounds have been orderly, and liquidity continues to circulate rather than retreat.

That stability, however, masks a more nuanced internal picture. Positioning has shifted, leadership has rotated, and hedging remains uneven. Expectations have adjusted higher while protection has not kept pace, leaving markets more sensitive to surprises even as the broader growth narrative remains intact.

Market Overview: Rotation Without Capitulation

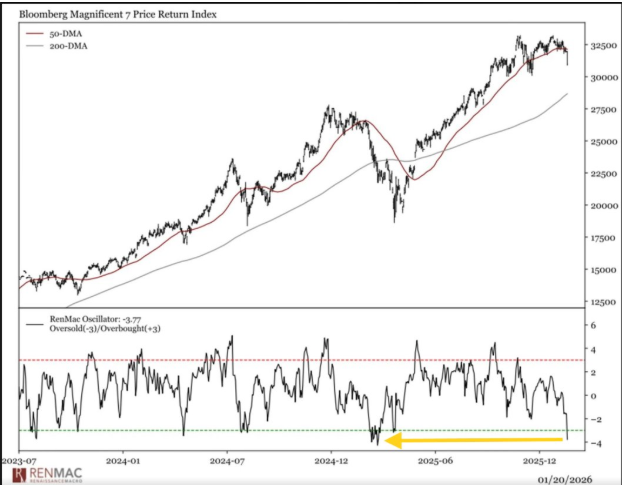

Equity structure remains intact, but progress is no longer driven by uniform momentum. Leadership rotation continues to define tape action, with selling pressure concentrated in crowded mega-cap exposures while broader participation absorbs flows more effectively. This has kept headline indices range-bound rather than broken.

Importantly, this redistribution of leadership reflects reallocation, not exit. Institutional selling has been visible, particularly in high-weight names, yet there is little evidence of broad de-risking. The lack of aggressive downside hedging reinforces that risk is being managed rather than abandoned.

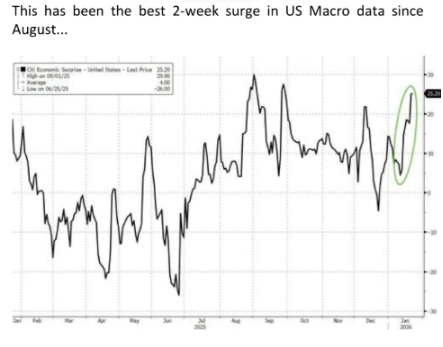

Growth remains the primary anchor underpinning this structure. US economic data continues to surprise positively, supporting earnings expectations and cushioning equities against episodic volatility driven by headlines rather than fundamentals.

Macro & Policy Watch: Loud Headlines, Measured Response

Geopolitics has reasserted itself as a persistent source of noise. Greenland-related tensions and Arctic security considerations have drawn attention, but market reactions suggest these developments are being treated as conditional rather than systemic risks.

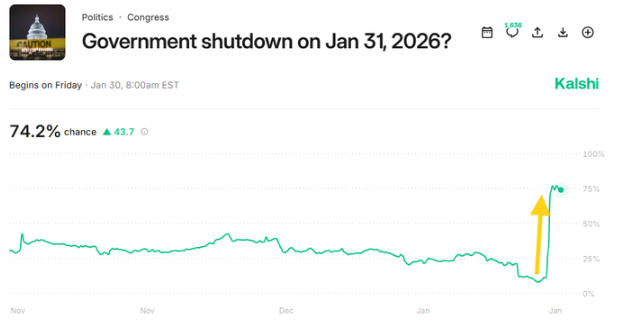

Domestically, renewed government shutdown concerns briefly lifted volatility and downside protection. However, the response across rates and equities remained contained, reinforcing the view that policy risk is being acknowledged but not fully priced.

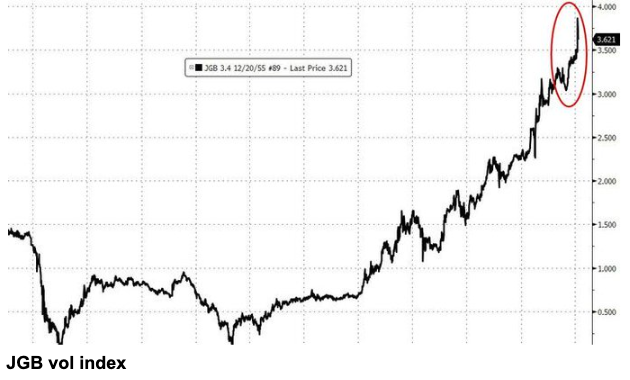

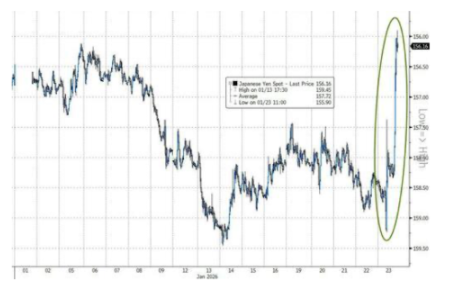

Japan continues to sit at the centre of global macro sensitivity. Rising JGB yields and increased volatility have revived carry trade concerns, with FX markets reacting quickly to both policy rhetoric and intervention risk. These dynamics keep global rates and currency markets on alert.

Technical & Sentiment Breakdown: Supportive, but Increasingly Fragile

From a technical perspective, trend structure remains functional. Major indices continue to hold key levels, and recent pullbacks have been corrective rather than impulsive. However, momentum has slowed, and dispersion beneath the surface has increased.

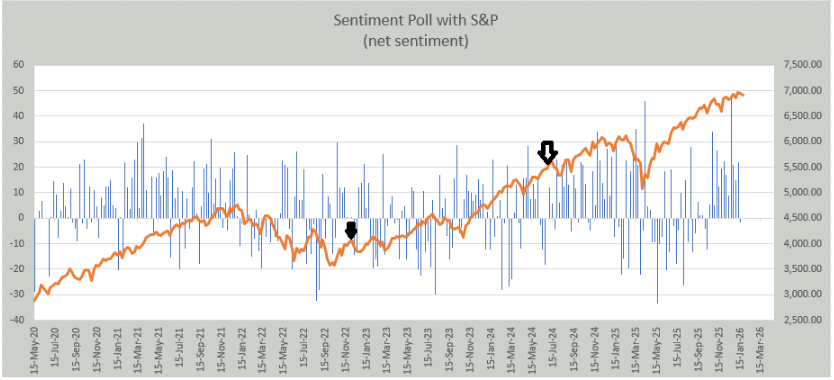

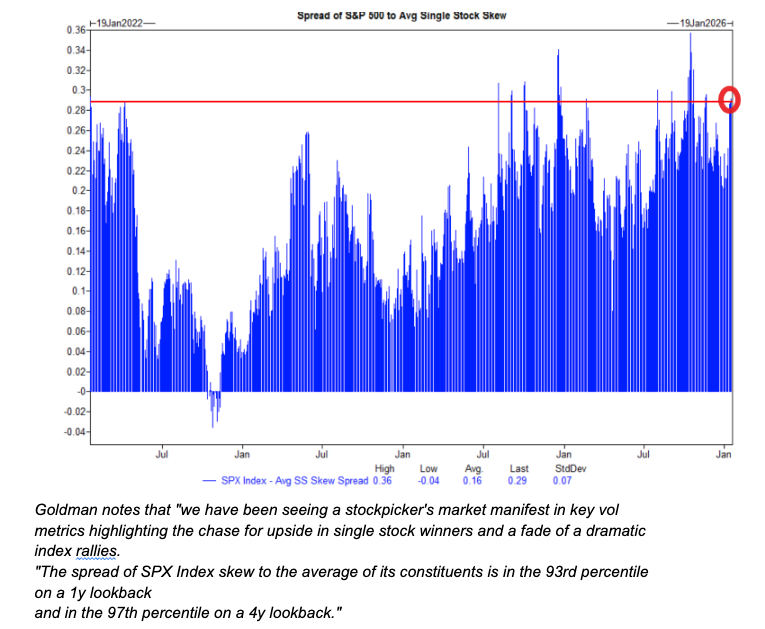

Sentiment data highlights a growing imbalance. Confidence remains elevated in single-stock opportunities, while demand for index-level protection has increased. This reflects a market that is optimistic in parts but cautious in aggregate, raising sensitivity to earnings outcomes and macro surprises.

Volatility remains compressed overall, yet this calm sits alongside elevated geopolitical and policy risk. Short gamma dynamics suggest that any unexpected shock could result in sharper, faster moves than recent price action implies, increasing intraday risk even as trends hold.

Last Week’s Recap: Growth Holds, Cross-Currents Build

Markets navigated last week with resilience, absorbing geopolitical shocks and policy noise without material structural damage. Data, flows, and positioning continued to matter more than headlines, even as familiar pressure points remained unresolved.

Key Highlights:

Macro:

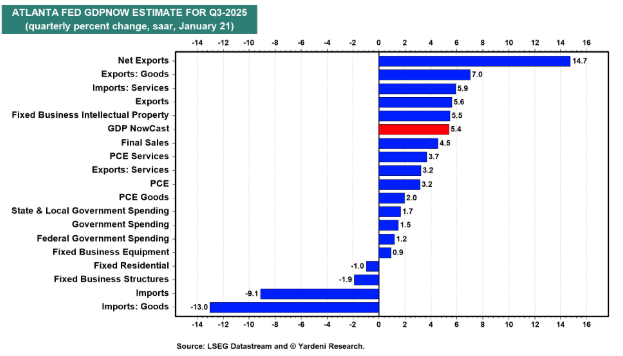

US growth data remained constructive. GDP tracking, consumption trends, and corporate profitability reinforced the broader growth narrative, while economic surprise indicators continued to move higher, helping anchor risk assets.

China:

Chinese data remained mixed. While headline growth targets were met, underlying consumption weakness and subdued imports highlighted ongoing structural challenges, limiting the global growth impulse and reinforcing regional divergence.

Earnings:

Early earnings results were broadly consistent with historical patterns, with a healthy proportion of beats but clear sector dispersion. Financials lagged expectations in places, while attention increasingly turns to large-cap technology for confirmation of broader market strength.

Commodities:

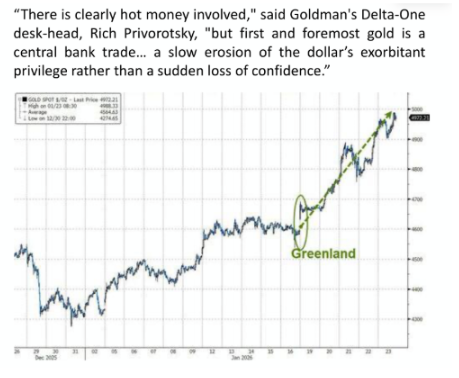

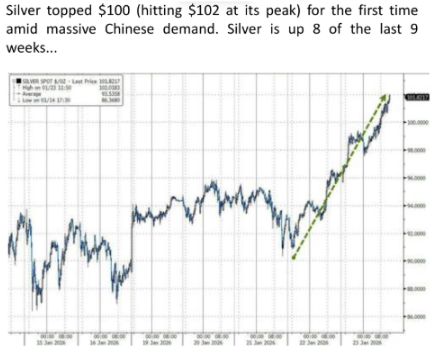

Precious metals continued to attract strong inflows. Gold benefited from debasement concerns and institutional demand, while silver’s strength reflected a combination of industrial demand and speculative interest.

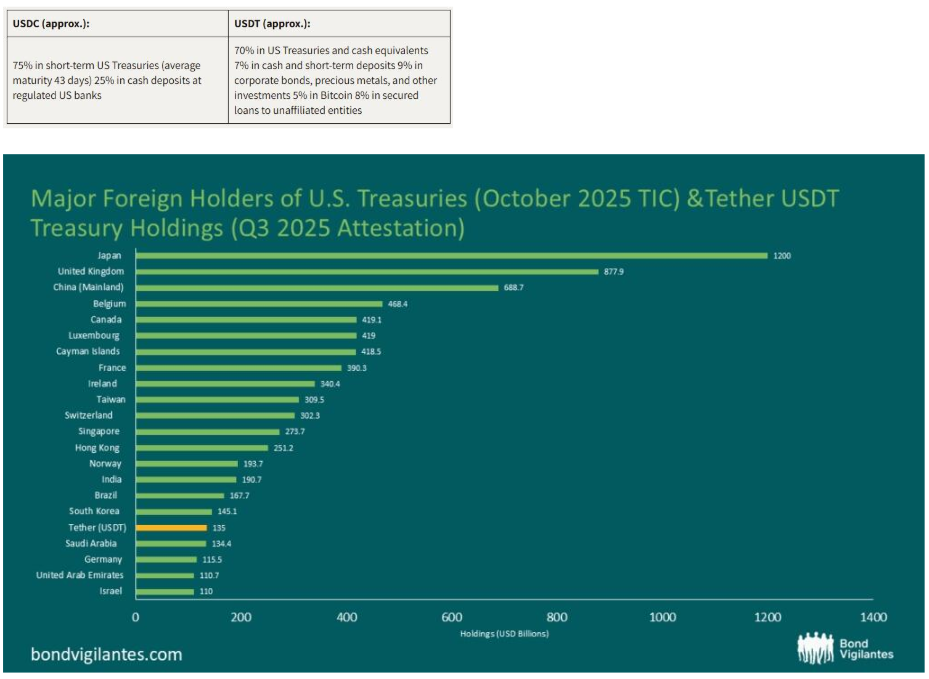

Crypto:

Crypto assets continued to underperform relative to hard assets. Price action reflects sensitivity to US-centric political dynamics and competition from traditional stores of value rather than renewed speculative excess.

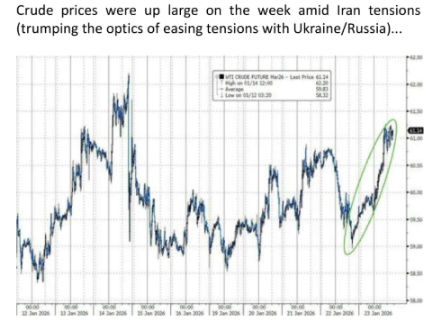

Oil:

Oil prices remained supported by geopolitical risk and supply considerations. However, price action suggested consolidation rather than acceleration, with risk premia fluctuating alongside headlines.

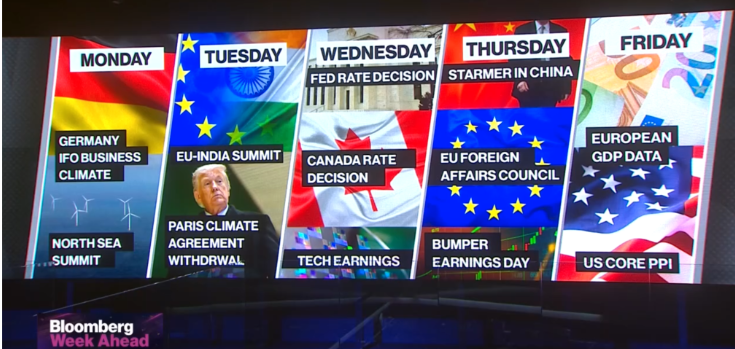

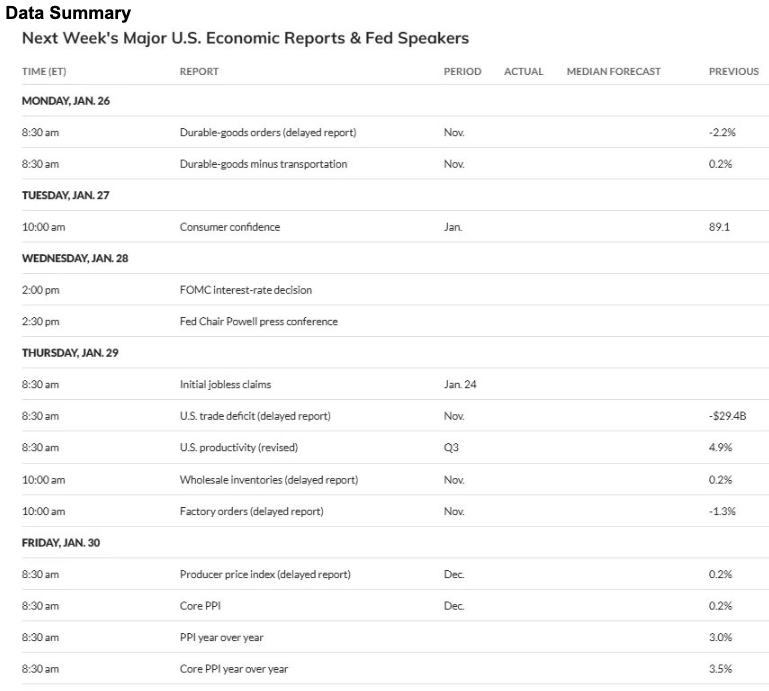

The Week Ahead: Key Data and Market-Moving Signals

This week is unusually dense, with a heavy concentration of earnings, central bank decisions, inflation data, and auctions. With positioning already sensitive, the breadth of scheduled risk raises the probability of volatility clustering rather than isolated reactions.

Monday, January 26

Japan: Coincident Indicator, Leading Index

Eurozone: German Ifo Business Climate, Expectations, Current Assessment

US: Durable Goods Orders, Core Durable Goods

US: Chicago Fed National Activity Index

US: Atlanta Fed GDPNow Update

US: Treasury Bill Auctions (3M, 6M)

Tuesday, January 27

Japan: BoJ Core CPI, Monetary Policy Meeting Minutes

China: Industrial Profits

US: Consumer Confidence

US: House Price Indices

US: Richmond Fed Manufacturing & Services

US: M2 Money Supply

US: API Crude Oil Inventories

US: 5-Year Treasury Auction

Earnings: UnitedHealth, General Motors, UPS, Boeing, American Airlines

Wednesday, January 28

Australia: CPI (Quarterly & Monthly Indicators)

US: MBA Mortgage Applications

Canada: Bank of Canada Rate Decision, Monetary Policy Report, Press Conference

US: Federal Reserve Rate Decision, Statement & Press Conference

US: Crude Oil Inventories

US: 7-Year Treasury Auction

Japan: Foreign Bond & Equity Flows

Earnings: Microsoft, Tesla, AT&T, Starbucks

Thursday, January 29

Japan: Tokyo CPI, Unemployment Rate, Industrial Production

Eurozone: Business & Consumer Surveys, Money Supply, Loans Data

US: Jobless Claims

US: Trade Balance

US: Factory Orders

US: Atlanta Fed GDPNow Update

US: Federal Reserve Balance Sheet

Earnings: Apple, Mastercard, Caterpillar, Lockheed Martin

Friday, January 30

Japan: Retail Sales, Housing Starts

Eurozone: GDP (Germany, France, Italy, Euro Area)

Eurozone: CPI (Germany, Spain)

UK: Mortgage Approvals, Credit Data

Canada: GDP

US: PPI (Headline & Core), Chicago PMI

US: Michigan Consumer Sentiment

China: Manufacturing & Services PMIs

Earnings: Chevron, Exxon, American Express

Alpha Takeaway: Constructive Structure, Narrowing Margin for Error

Markets remain supported by growth and liquidity, but positioning has become more sensitive as volatility stays compressed and protection remains limited. The environment continues to reward selectivity over broad exposure.

Equities:

Rotation continues to dominate equity performance. Broad participation supports the overall structure, but leadership remains selective, increasing the importance of positioning and timing.

Gold & Silver:

Precious metals remain underpinned by geopolitical and macro uncertainty. While positioning may introduce near-term volatility, underlying demand remains resilient.

Crypto:

Crypto continues to lag hard assets, reflecting uneven conviction and sensitivity to political and policy narratives rather than a breakdown in structure.

Macro:

Growth resilience and contained inflation pressures continue to define the backdrop, even as geopolitical and policy risks increase the market’s reactivity to surprises.

The structure remains constructive, but tolerance for shocks is narrowing. Calm conditions persist, yet they rest on increasingly thin protection.