Markets grind higher despite tariff shocks, weakening breadth, and rising political risk

All eyes now shift to CPI, earnings, and Trump’s Aug 1 “TACO” deadline. Here's your full macro breakdown, technical setups, and tactical trading guide.

Market Overview: SPX at Highs, but Cracks Are Forming Beneath

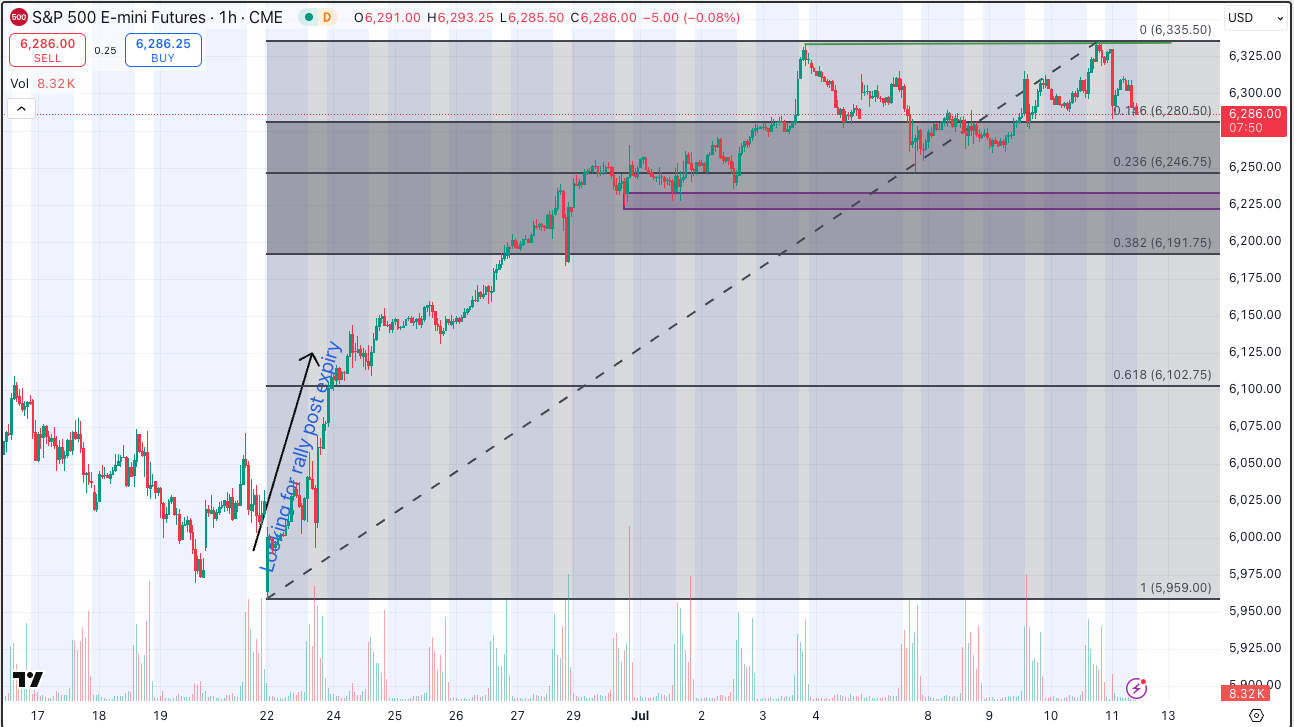

The S&P 500 hit a fresh ATH last Thursday but closed the week 0.33% lower at 6,259.75. While price action remains orderly, internals suggest we’re on thinner ice than many realise.

- 5-day breadth dropped sharply: 65.8% → 50.39%

- Net new highs collapsed: +178 to -87

- 200dma participation crawls up, but 50dma stagnates

- Nasdaq 100 down slightly (-0.21%), but propped up by mega-caps

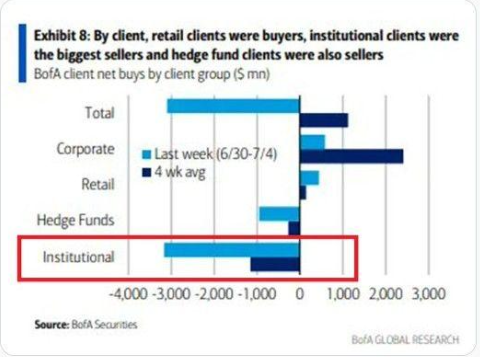

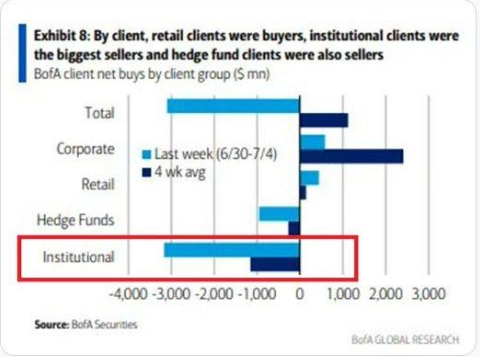

- Retail buying peaked by July 4th while pros continue fading

Energy surged +3% on geopolitical catalysts and defence-led inflows. Semis and infrastructure also stayed firm, with NVIDIA achieving the first $4T valuation.

This isn’t a breakdown yet—but it’s not a breakout either. Traders are rotating, not chasing.

Macro & Policy Watch: CPI Flashpoint, Tariff Poker, and the Powell Pressure Cooker

CPI: Calm Surface, Hidden Risk

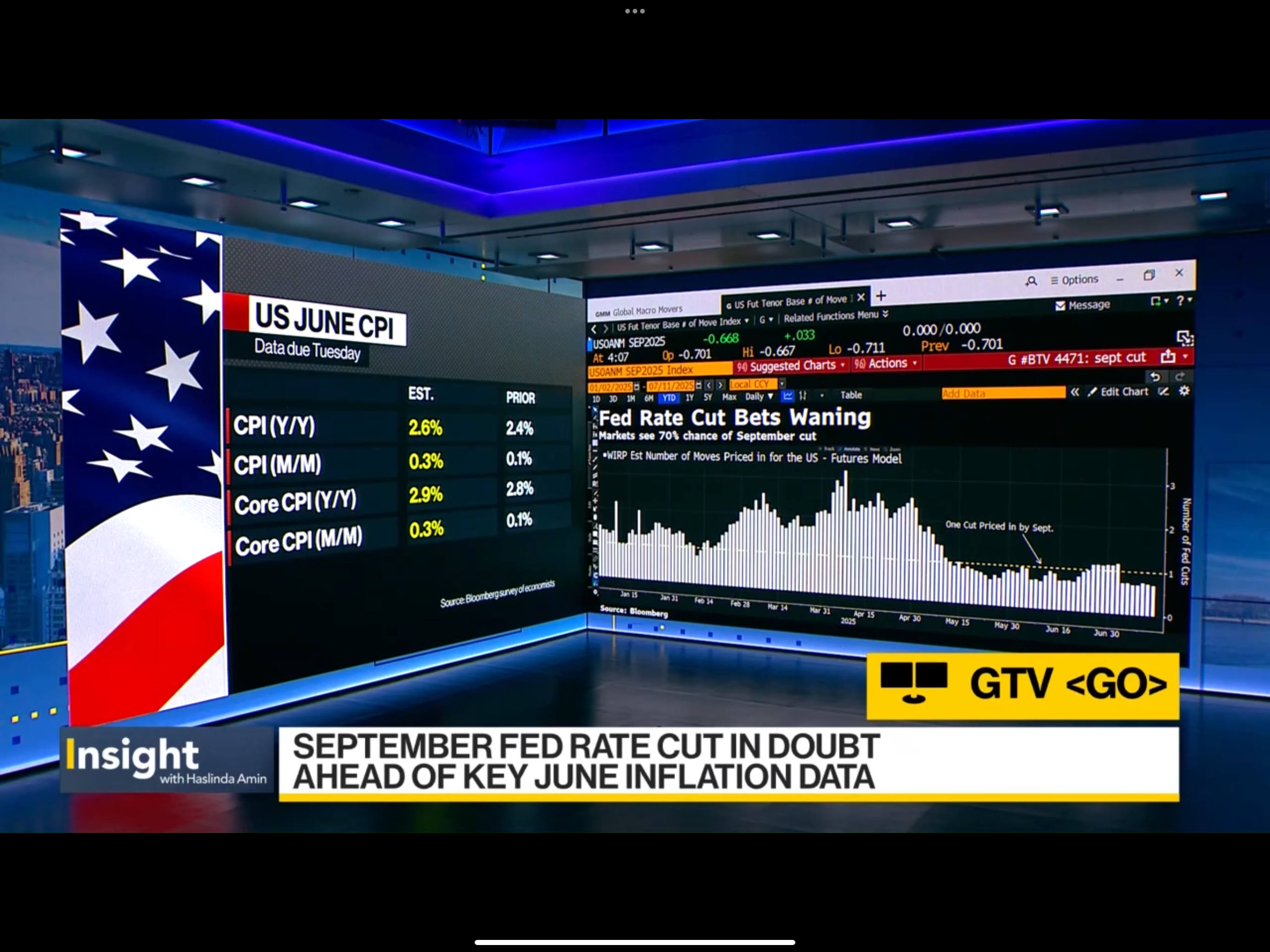

Tuesday’s CPI will offer the first real signal of tariff spillover into consumer prices. Bloomberg projects a soft print, but under the hood, there are offsetting forces.

Firming:

- Appliances

- Furniture

Weak:

- Airfares

- Used cars

- Shelter

Result: Likely benign headline, but a higher miss risk.

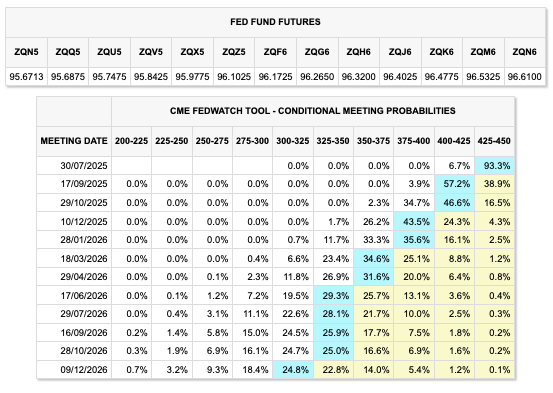

Markets expect CPI to land close to May's levels. But a beat could erase rate cut hopes and drive a repricing of September odds.

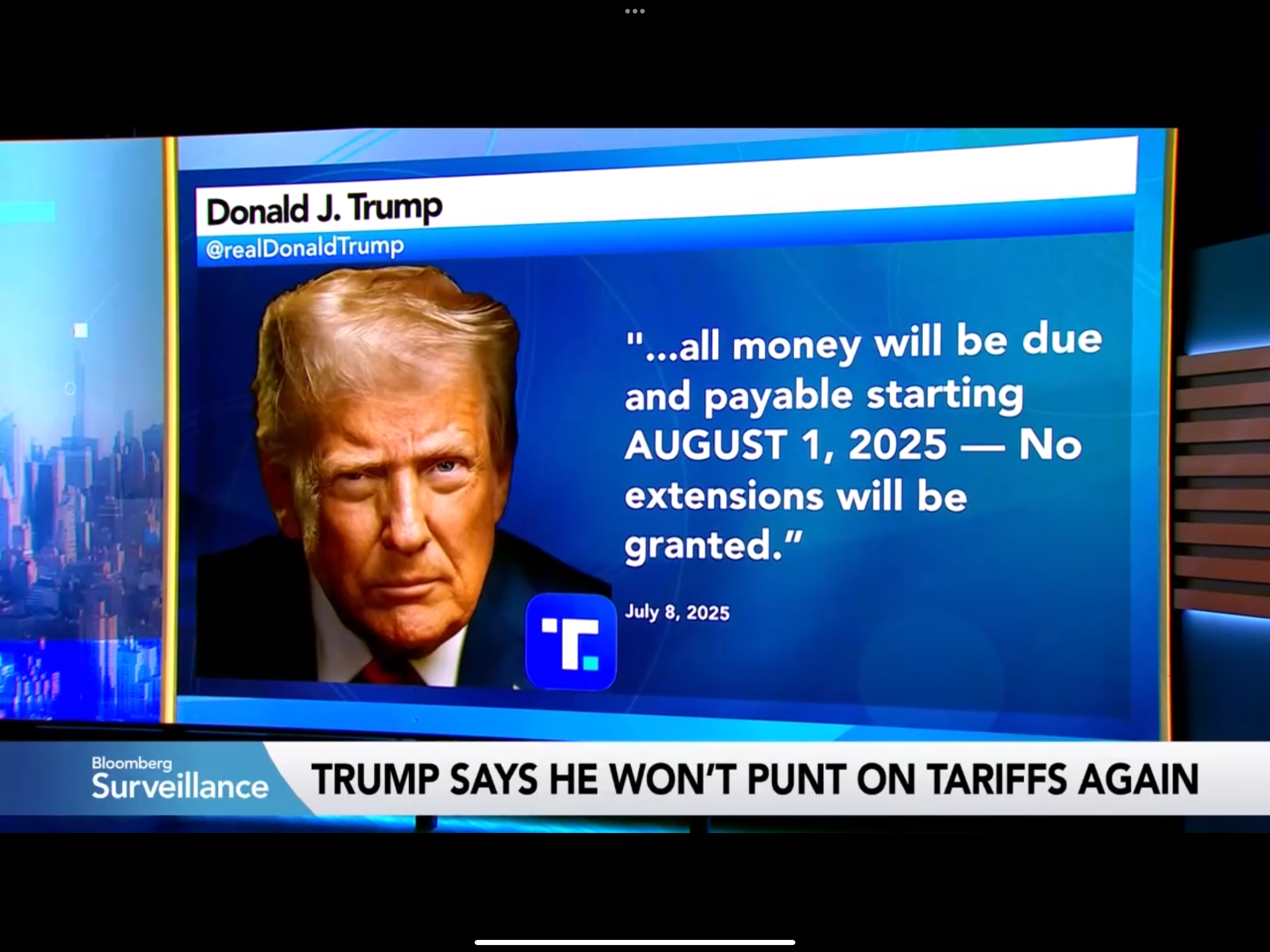

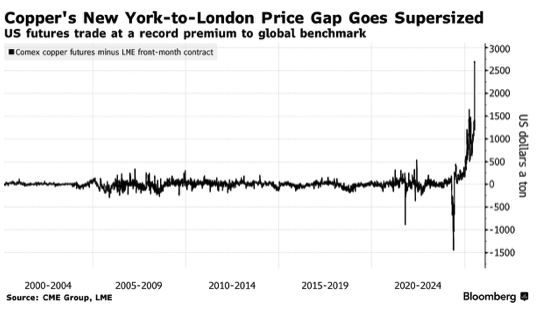

Tariffs: Aug 1st = TACO Deadline

Trump delayed his counter-tariff move to Aug 1st, marking a tactical pause in trade escalation. But the copper tariff (50%) is already impacting supply chains, and a proposed 200% pharma tariff hangs over Q3 like a sword.

Expect

- Positioning skews into Aug 1st

- Copper and pharma volatility to rise

- Global supply arbitrage (Hawaii/PR stockpiling) accelerating

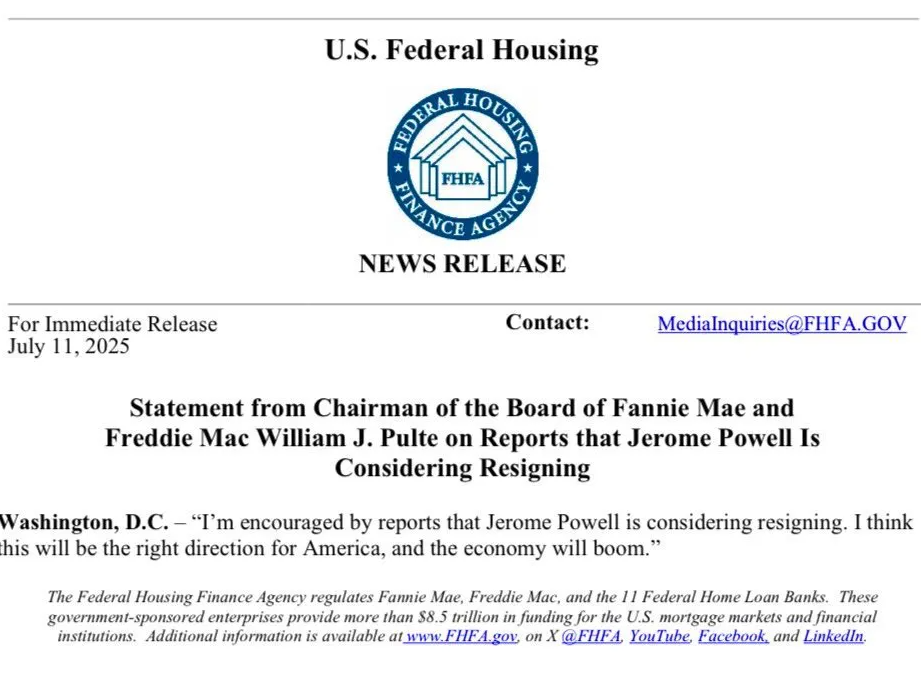

Powell: Independence Under Fire

Behind the scenes, chatter of Powell being pushed out returned. Whether realistic or not, it reveals the growing politicisation of monetary policy. A divided Fed and persistent political noise will weigh on confidence in H2.

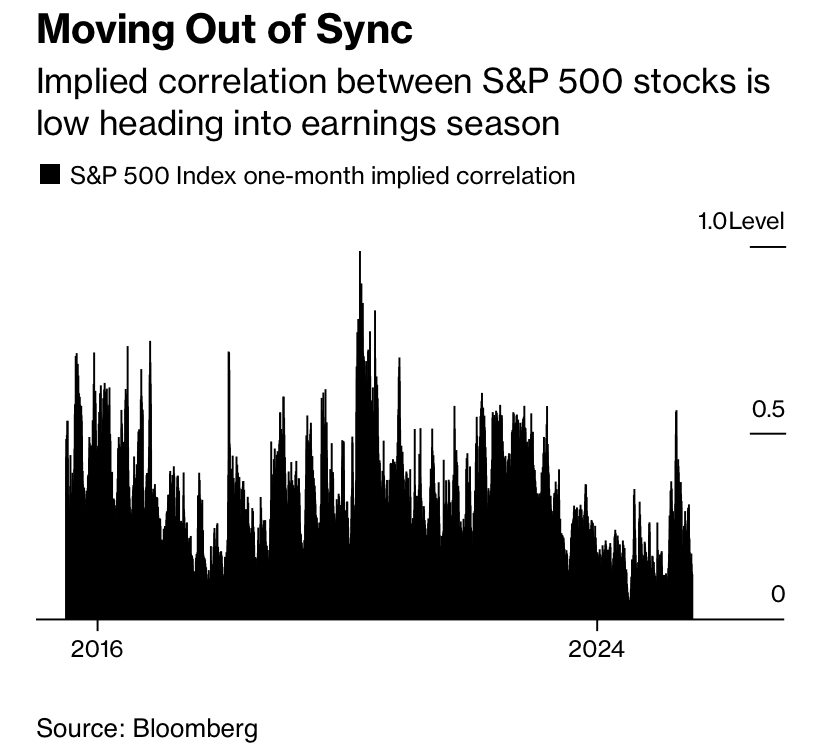

Technical & Sentiment Breakdown: Rotation, Mega-Cap Risk, and Sentiment Divergence

SPX – Breadth Breaks Down

The index is still near highs, but the internals tell a different story:

- Distribution rising in the lower index half

- 50dma breakouts stalled

- Momentum cools even as price stays elevated

Nasdaq – Mega-Caps Holding the Dam

Only 43.56% of Nasdaq 100 names are above their 5-day average, down from 79.2%. Yet the index held steady, thanks to the top 5 stocks propping it up. If those falter, expect a swift flush.

Crypto – Liquidity Tsunami

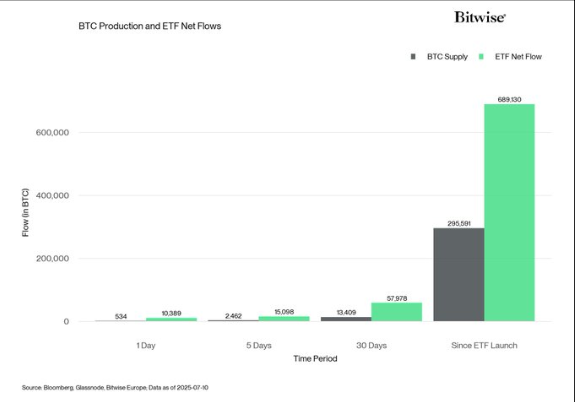

Bitcoin ripped through $120K after ETF flows overwhelmed daily supply. With U.S. institutions absorbing 10,389 BTC vs a daily supply of just 534, this is liquidity capture on steroids.

- Total crypto cap at $4T

- Institutional and Treasury flows are accelerating

- “Crypto Week” designation in Congress adds tailwind

Last Week’s Recap: Earnings Beats, Energy Surge, and Trade Shockers

Markets were macro-light but tariff-heavy last week.

- SPX hit ATHs but faded late week

- Defence names surged: Red Cat +25%, Kratos +11%, AeroVironment +10%

- Gold held 50dma support amid safe-haven demand

- Delta reinstated guidance (+13%), but United looms this week

- Crypto surged as ETF buying and M2 tailwinds aligned

- Retail sales held, but underlying consumption softened

- Brazil hit hard by copper tariffs; Real dropped, global stocks reacted

This wasn’t a quiet week—it was the calm before a potential policy storm.

The Week Ahead: CPI, China Data, and Earnings Roulette

This week is macro-loaded and earnings-heavy—Tuesday is the new Super Thursday.

Monday, July 14

- CNY Trade Balance, NZ Services Index

- CHF PPI, JPY Industrial Production

- Fed, ECB, and BOE speakers

Tuesday, July 15

- US CPI (June)

- JPM, CITI, WFC, BLK, STT earnings

- CNY GDP, Retail Sales, HPI, Unemployment

- German & EZ ZEW Surveys

- Spain & Canada CPI

- OPEC monthly report, API oil data

Wednesday, July 16

- GBP CPI, EZ Trade, US PPI, Beige Book

- Earnings: BoA, GS, ASML, UAL, Alcoa

Thursday, July 17

- US Retail Sales, Claims, Philly Fed

- Netflix, TSMC earnings

- AUD Employment, JPY Trade

- EZ CPI Final

Friday, July 18

- US Housing Starts, Michigan Sentiment

- AMEX, Charles Schwab earnings

- GER PPI, EZ Trade

Alpha Takeaway: Market Is Calm—But That’s the Risk

We are in a complacency pocket. But it’s a thin one.

- CPI surprise could unwind bullish bets

- Breadth deterioration warns of fragility

- Crypto and gold suggest macro stress is still alive

- Retail still buying dips—pros remain defensive

- Powell, tariffs, and China headlines are all unresolved

Our Playbook

- Stay long SPX above 6200, but tighten stops into CPI

- Add to crypto on dips, but trail aggressively

- Watch defensive sectors and gold—Q3 risk-off trade may emerge fast

- Earnings will matter more than usual: margins vs headline beats