Gridlock in Japan, Melt-Up Momentum, and a Tariff Countdown into Earnings

Markets continue their summer rally despite rising political dysfunction, tariff deadlines, and bubbling risk sentiment. As over 100 S&P companies prepare to report, traders are leaning into liquidity and narrative certainty. However, cracks beneath the surface—breadth divergences, retail-driven flows, and policy instability—suggest that volatility could return quickly.

Market Overview: A Calm Surface, Cracks Beneath

The bulls are still in control—for now. U.S. indices continue to grind higher, supported by strong Q2 earnings, high cash levels, and a surprising absence of volatility. But under the hood, the structure is weakening:

- Japan’s ruling coalition has lost both houses of government but refuses to step down, injecting fresh global uncertainty

- Trump doubled down on his15–20% EU tariff demand, locking in August 1 as a hard deadline

- The Fed is now in blackout ahead of the July 30 FOMC, offering no reassurance as markets press higher

- Retail flows dominate while macro internals start to deteriorate

Meanwhile, cash levels remain elevated, offering dip-buying fuel. However, with SPX having rallied strongly, participation thinning, and AI mania peaking, traders should exercise caution not to chase late-stage price action blindly.

Macro & Policy Watch: Tariff Certainty, Fiscal Stress, and Dollar Deterioration

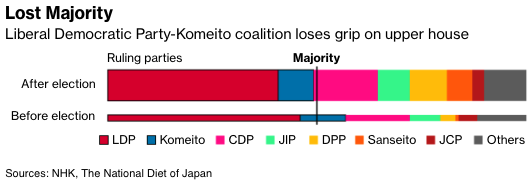

Japan’s Political Breakdown = Fiscal Creep Risk

Markets expected a loss, but Ishiba’s coalition losing both houses and refusing to resign is a problem. The concern is that, to regain credibility, the government may resort to spending increases or tax cuts, thereby risking fiscal credibility. Japanese assets could wobble further if investor confidence erodes.

Trump’s August 1 Deadline is Set in Stone

According to FT leaks, the White House is demanding a 15–20% tariff on all EU goods. Trump’s not bluffing—August 1 is now the line in the sand. While markets dislike the numbers, they love certainty. This gives risk assets breathing room to consolidate—unless the situation deteriorates.

Debt, Dollar & QE-by-Stealth

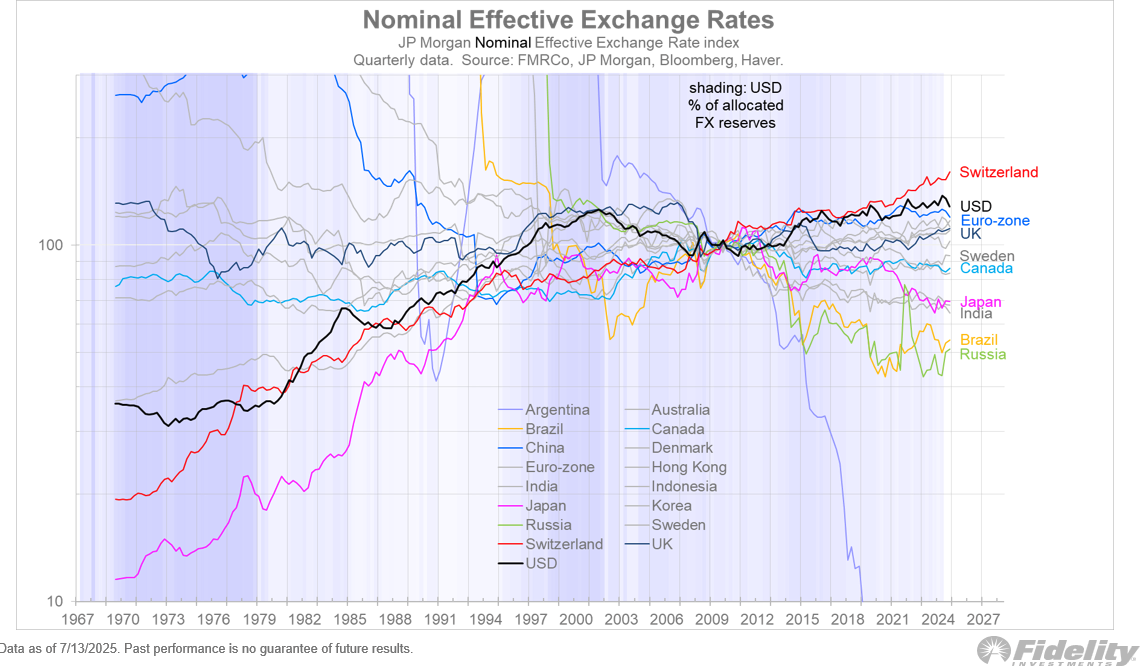

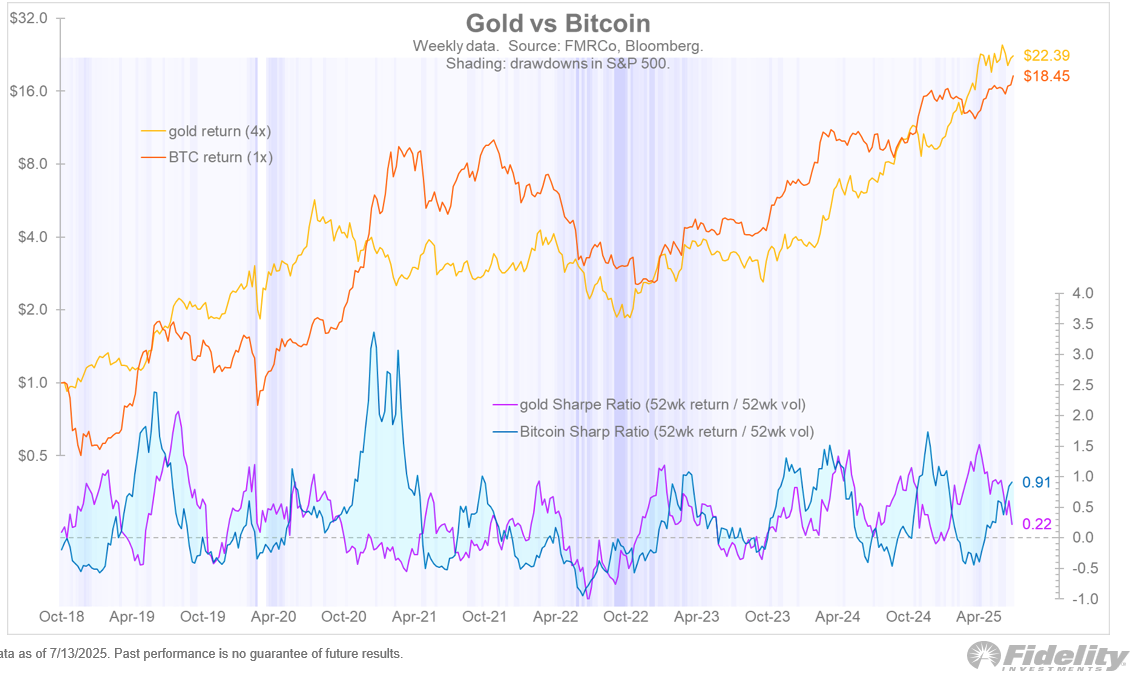

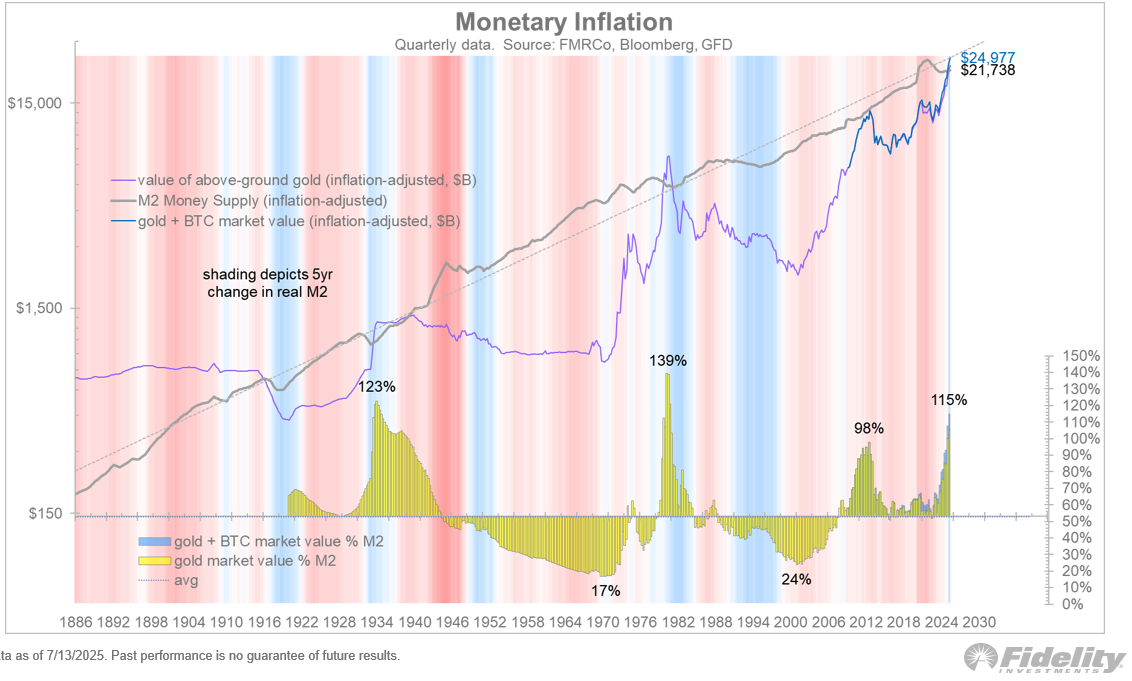

With massive Treasury issuance looming, the Fed may be forced into buying government debt again. This is quiet QE, and it won’t go unnoticed—especially by gold, silver, and Bitcoin. The dollar remains expensive, with JPM’s effective dollar index still near cycle highs.

Fiat scepticism is building. The market sees through the math, and protection assets are responding.

Technical & Sentiment Breakdown: Divergences Signal Late-Stage Behaviour

The uptrend remains intact—but it’s increasingly narrow and speculative.

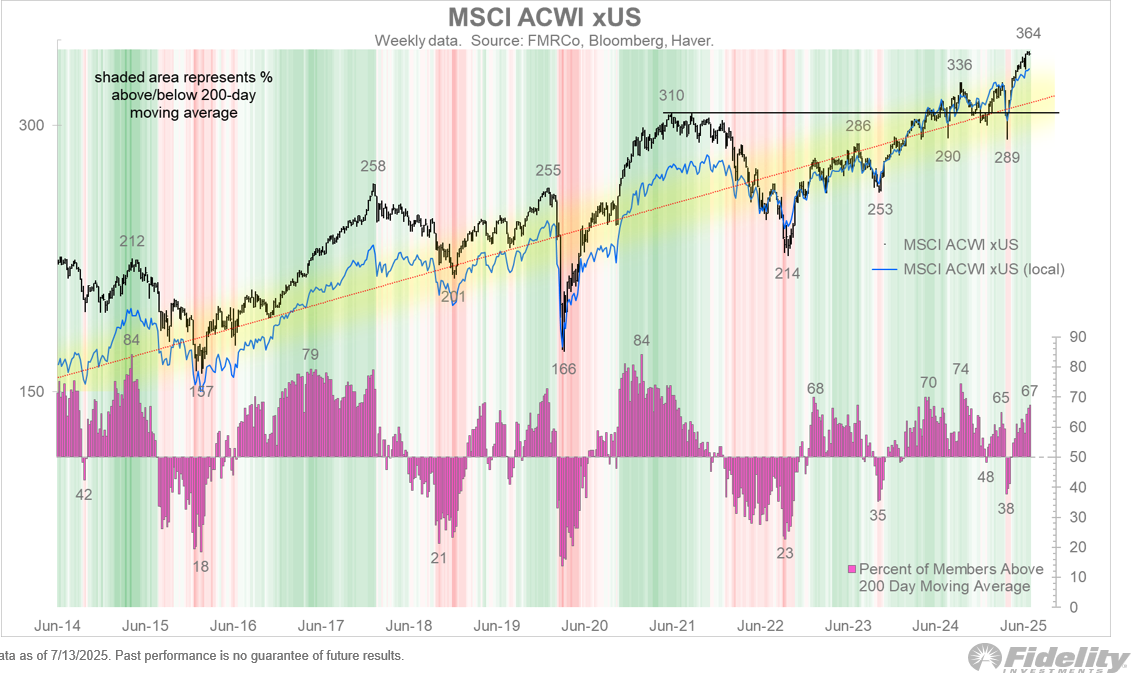

- ACWI internals are diverging from price

- Non-profitable tech stocks have staged a wild V-shaped rebound

- Large caps are masking weakness under the surface

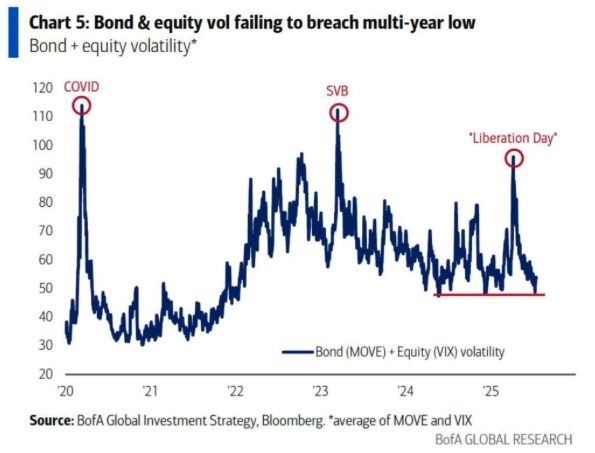

- Volatility metrics (VIX, MOVE) are flat despite mounting macro risks

AI continues to drive flows into speculative growth, pulling capital away from real economy sectors. With global equity valuations pushing against GDP ratios, the risk of mean reversion increases.

Retail is driving the bus. That means we’re in a short gamma environment where dealers chase upside to manage exposure—until they don’t.

Last Week’s Recap: Cooling CPI, Hot Earnings, and Fed Uncertainty

Inflation: Soft Enough to Support Dovish Case

U.S. data last week showed a modest inflation pulse:

- CPI-PPI spread suggested improving margins and weaker cost pressures

- The Philly Fed index jumped unexpectedly, crushing residual recession fears

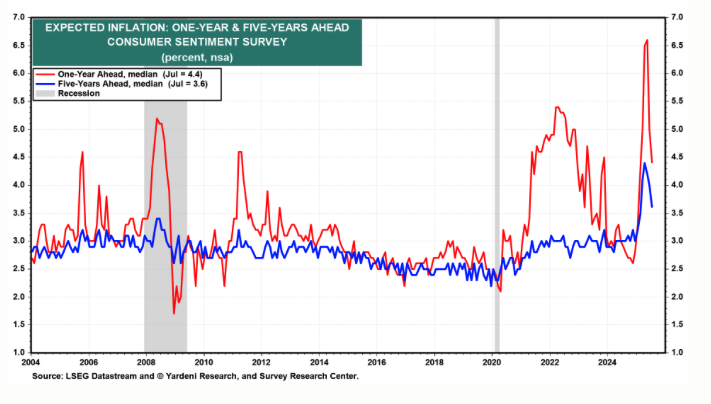

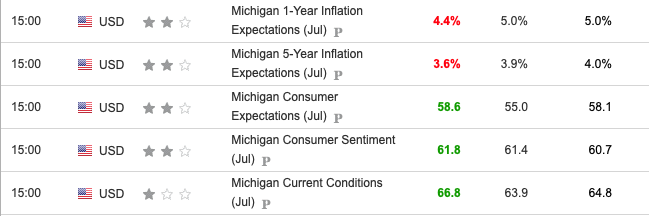

- University of Michigan survey showed inflation expectations falling and consumer confidence rising

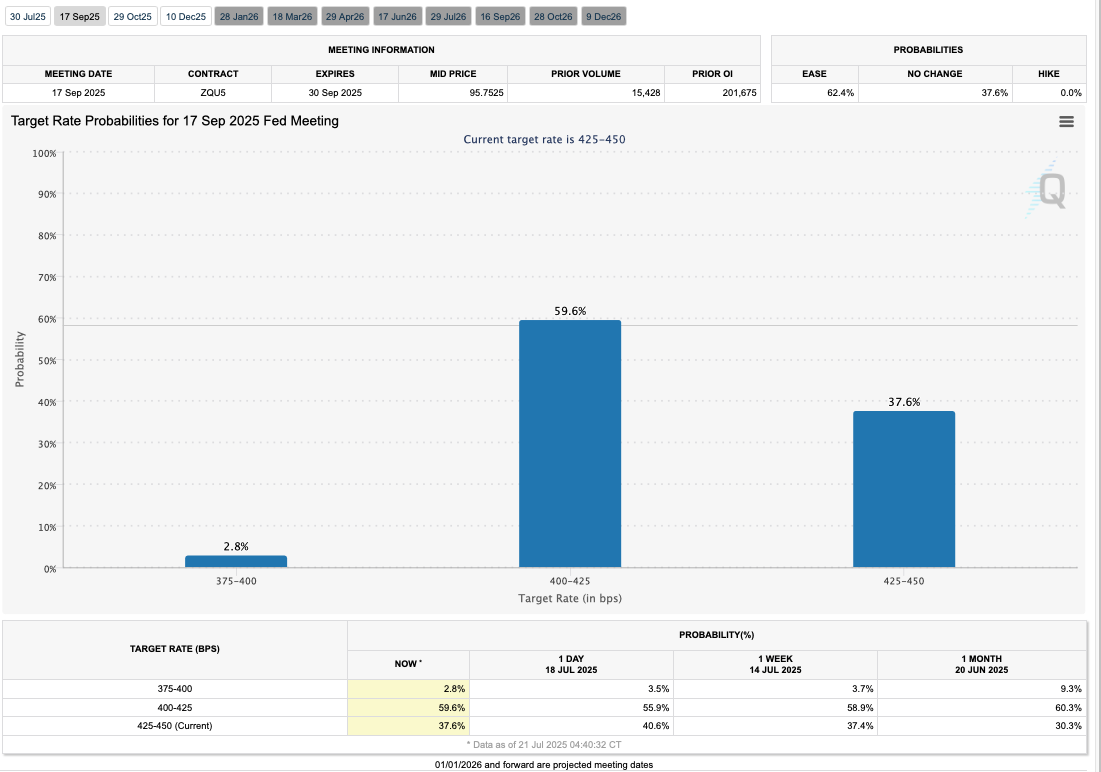

The Fed enters its blackout window split on what’s next:

- Waller argued for a July cut

- Daly and Kugler see a restrictive policy holding

- Goolsbee flagged tariff-driven inflation as a new headwind

All eyes now turn to the July 30 FOMC.

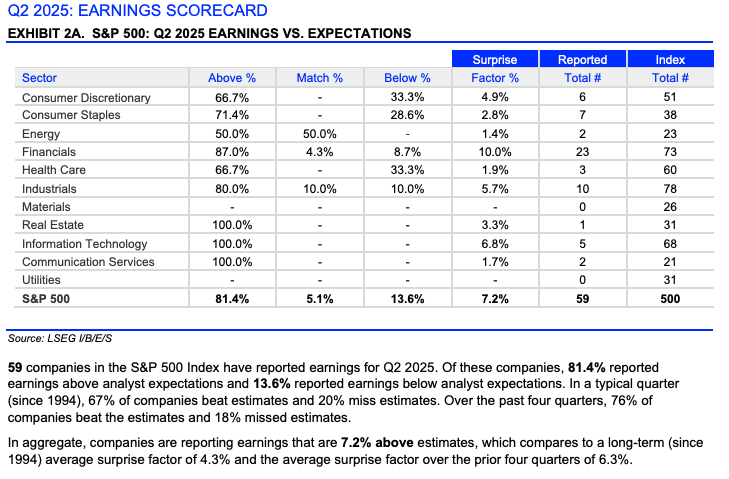

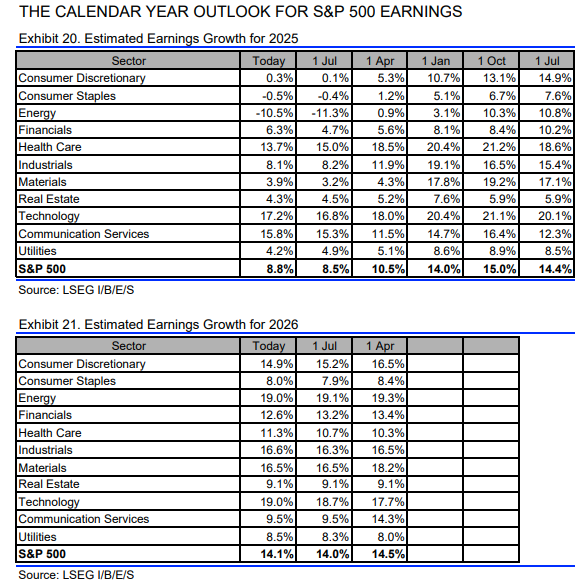

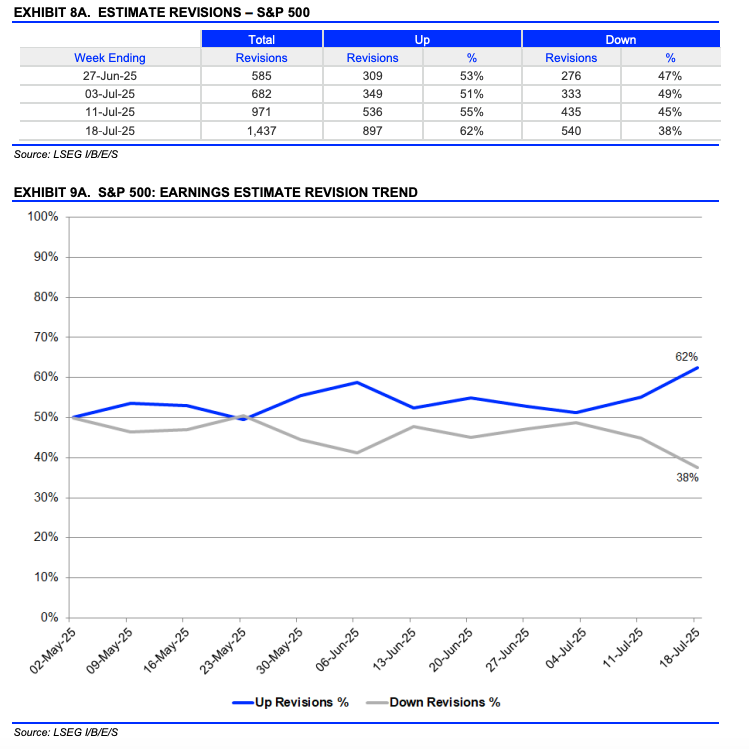

Earnings: Positive Surprises, Forward Revisions Lift

Q2 earnings began with strong beats and upward revisions to FY25 and FY26 earnings. Buybacks and dividends are also trending higher, and investor positioning still suggests room to run.

The Week Ahead: ECB, Earnings Barrage, and Tokyo CPI

It’s a packed week for central banks, earnings, and global sentiment gauges—Thursday steals the spotlight with flash PMIs and ECB fireworks.

Monday, July 21

- NZ CPI, GBP Rightmove HPI

- CNY Loan Prime Rates (1Y & 5Y unch)

- CAD PPI, USD Leading Index

- France & U.S. short-term bill auctions

Tuesday, July 22

- RBA Meeting Minutes

- USD Redbook, Richmond PMI, M2 Money Supply

- Powell and Bowman’s last scheduled appearances

- BOE’s Bailey speaks

Wednesday, July 23

- BOJ Core CPI, EZ Consumer Confidence

- USD Existing Home Sales

- CAD New Housing Prices

- U.S. 20Y Treasury auction

Thursday, July 24

- Global Flash PMIs

- ECB Rate Decision + Press Conference

- U.S. Jobless Claims, Building Permits, New Home Sales

- Fed Balance Sheet update, CAD Retail Sales

Friday, July 25

- Tokyo CPI, German IFO

- U.S. Durable Goods Orders, Atlanta GDPNow

- GBP Retail Sales, GfK Consumer Confidence

- EZ Money Supply, CAD Wholesale Sales

Alpha Takeaway: Countdown to August 1

Markets are holding up—but it’s fragile. Beneath the surface, signs of late-cycle excess are clear:

- Breadth divergences

- Frothy retail-driven flows

- Currency instability

- Political interference in central banks

Still, liquidity is strong, cash is high, and earnings are beating. If the tariff risk is resolved cleanly, this market could rip into August. If not, the melt-up turns into a sharp repricing.

Our Stance

- Stay long quality names, but tighten stops

- Use pullbacks to add BTC, gold, and real assets with tailwind stories

- Watch Wednesday–Friday this week: ECB, PMIs, and Durable Goods may shift tone