Trump’s Tariff Game, Rate Cut Chess, and a Market That Won’t Quit

Markets continue to rise as political theatre, global deflation fears, and dovish central bank signals fuel risk appetite. Behind the headlines, structural forces are shifting: Trump’s trade tactics, Powell’s balancing act, and the dollar’s mysterious drift all converge in this pivotal week. Here’s your full macro breakdown, technical map, and trading forecast.

Market Overview: ATHs Hold, Rotation Broadens, but Risks Linger

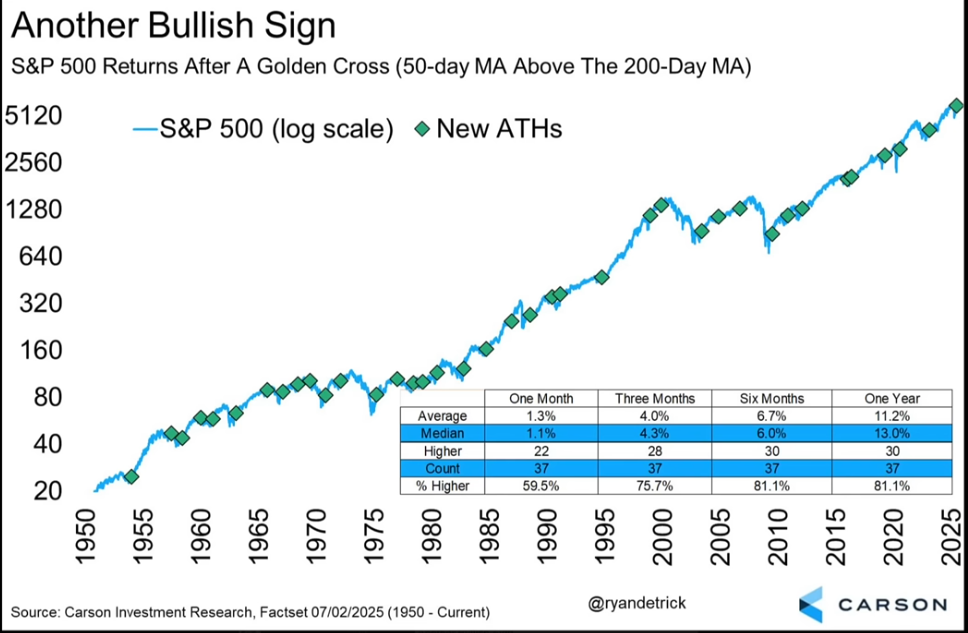

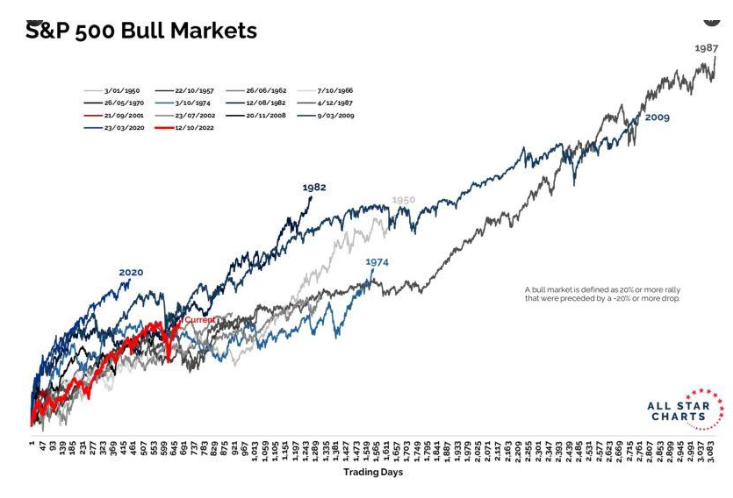

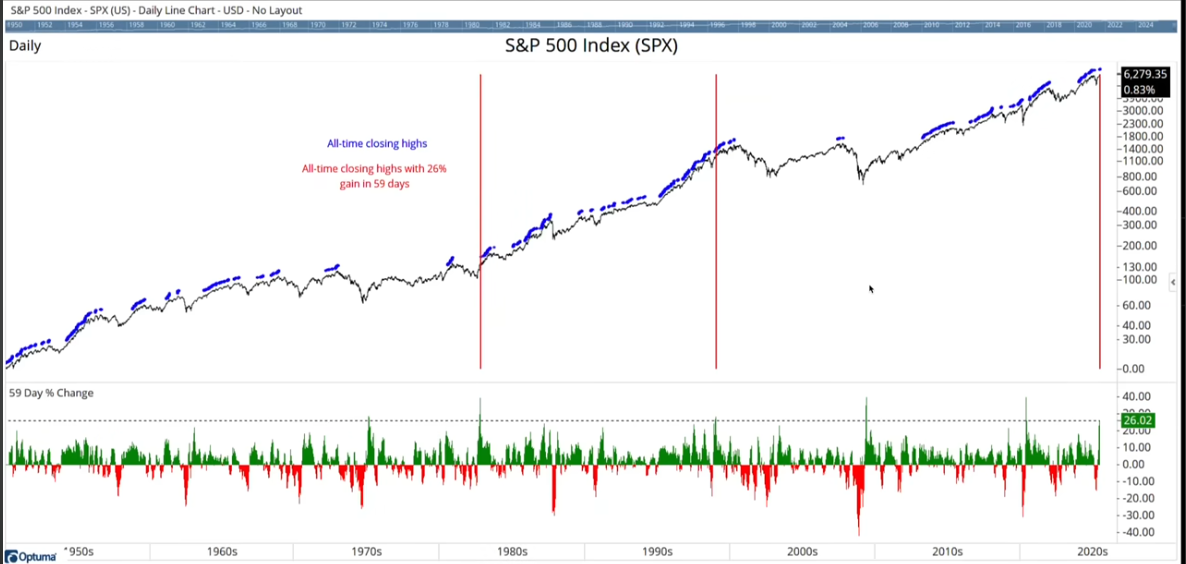

Markets continued their summer rally, shrugging off tariff anxiety and recession talk. The S&P 500 hit fresh all-time highs while small caps joined the breakout, suggesting this move isn’t just about mega-cap momentum anymore.

Underneath, however, there’s reason for tactical caution:

- SPX has rallied +26% in just 59 days— a rare historical feat

- VIX and P/C ratios show bullish complacency, but not extremes

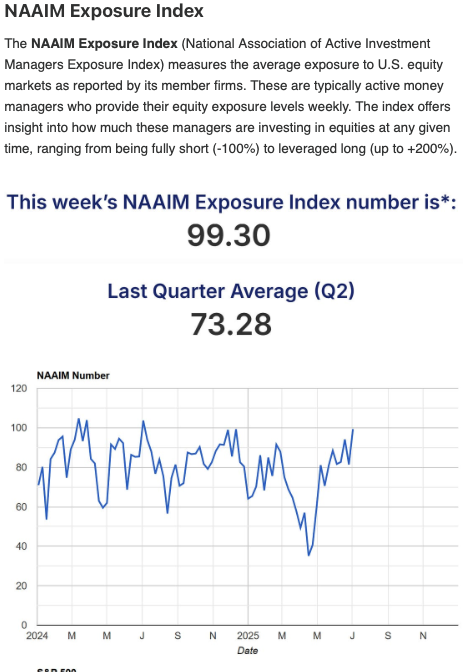

- NAAIM exposure sits just below 100, a common fade zone

- Participation breadth is improving, but is still thin in places

Liquidity and seasonality remain tailwinds, but we’re nearing zones where markets often consolidate. Traders looking for a deeper pullback may have to wait until earnings or CPI provide a catalyst.

Macro & Policy Watch: Tariff Poker, Deflation Fears, and Dollar Decoupling

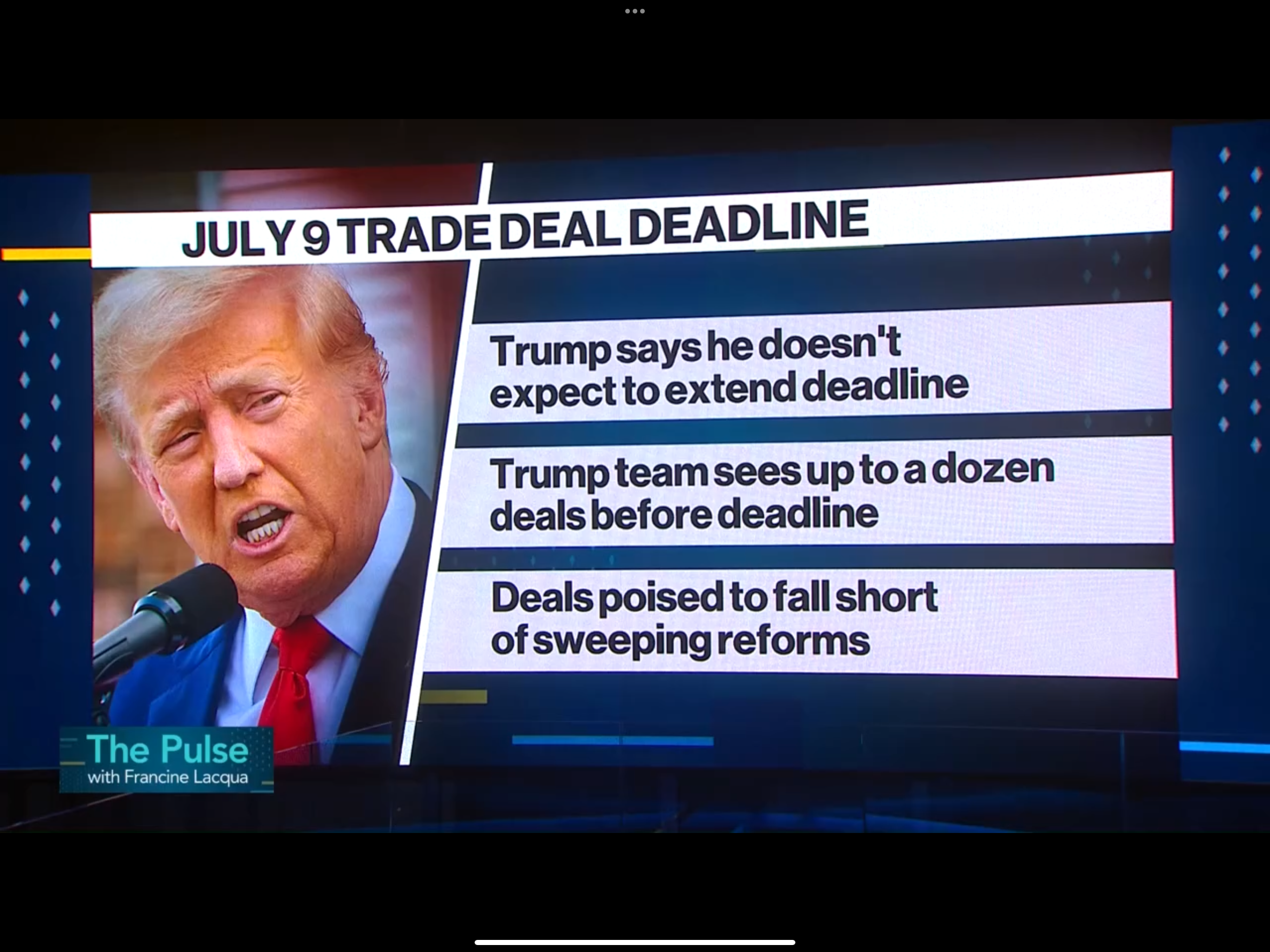

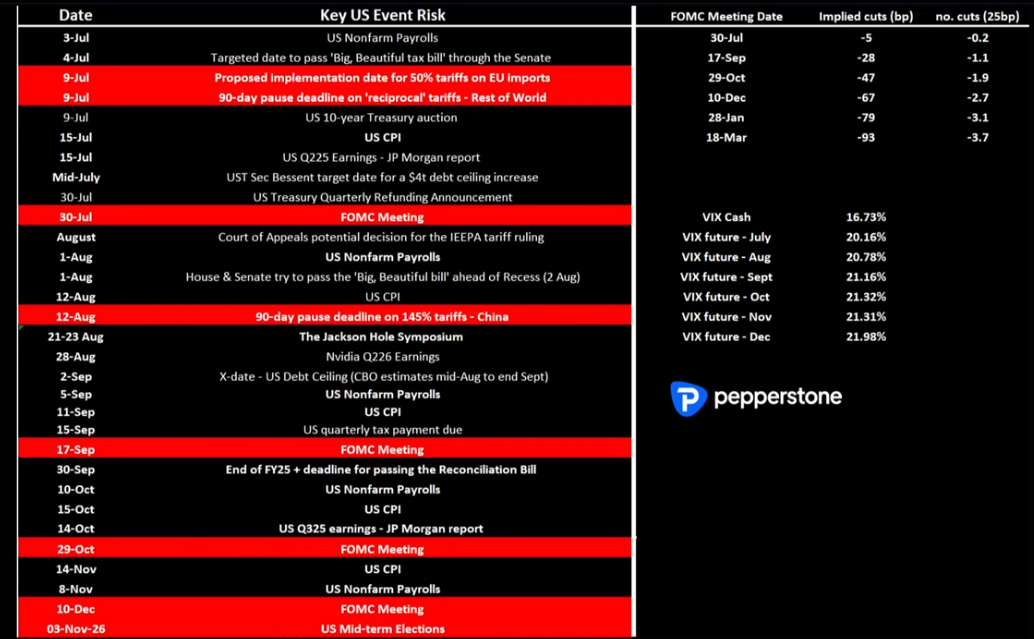

Trump’s Tariff Letters: The Clock Is Ticking

July 9 marks Trump’s self-imposed deadline for sending reciprocal tariff letters. While a deal with Vietnam is sealed EU and BRICs tensions are mounting The market expects a delay (TACO), but the risk of an actual move could rattle complacent bulls.

Trump’s rhetoric is all in: markets at highs, Powell under fire, and America “winning” on trade. Whether that narrative holds depends on how global partners respond. Aug 1st is tariff pay day.

Powell’s Messaging: Dovish, But Cornered

At Sintra, Powell admitted they would’ve cut already if not for tariff uncertainty. He acknowledged inflation is cooling and growth is solid. But politically, he’s under pressure. Trump has escalated attacks, positioning himself as the driver of both markets and monetary policy.

Meanwhile, global central banks are turning openly dovish:

- ECB and BOE speakers now see the risk of inflation undershooting

- Swap spreads are deeply negative markets expect deflation

- RBA and RBNZ decisions this week could reinforce the rate cut narrative

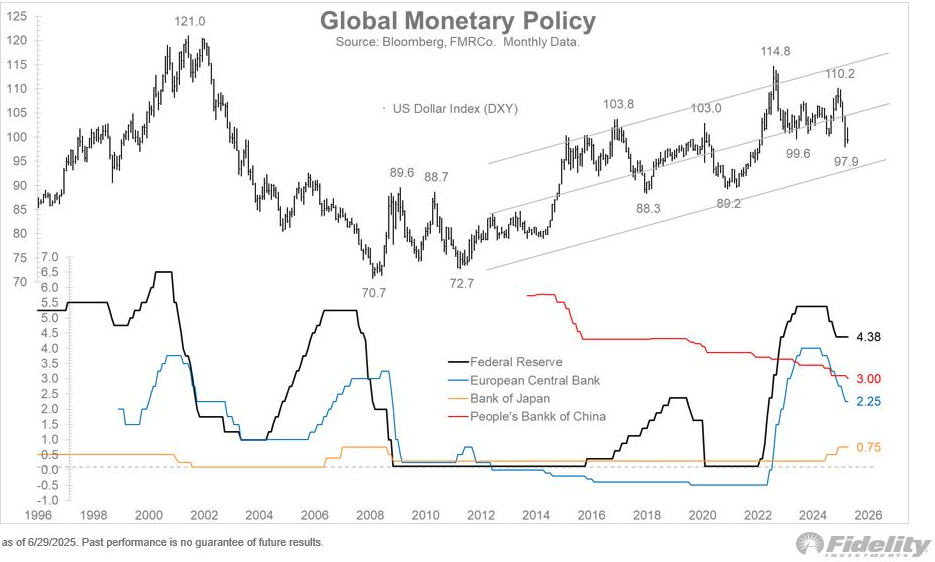

The Dollar: A Controlled Collapse?

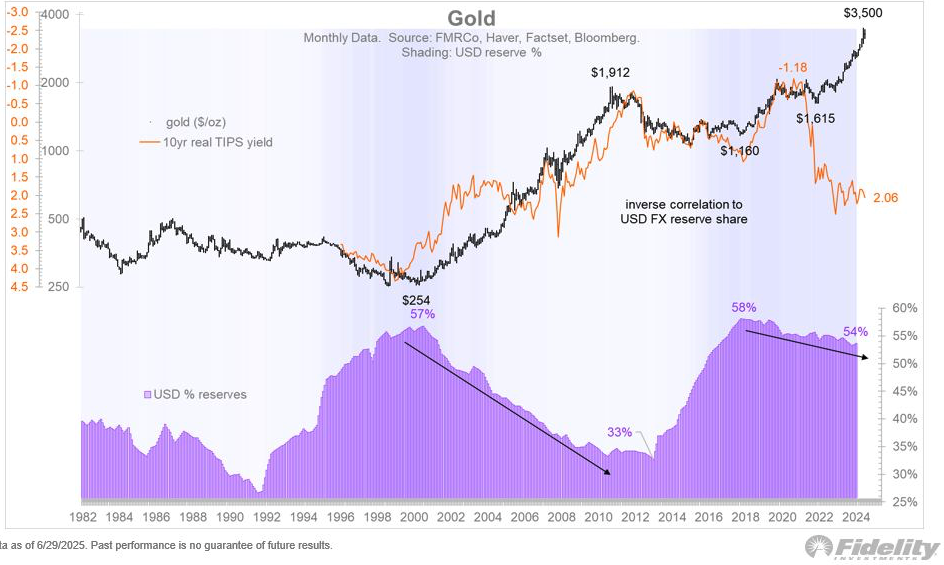

Despite leading global rates, the dollar can’t catch a bid. DXY has weakened steadily— a break in the rate-differential link. Trump’s barrage on Powell may be working, with global reserve managers rebalancing toward gold and commodities.

- Gold is consolidating not selling off—a tell for underlying demand

- EMFX and non-US assets benefit from DXY softness

- The dollar is no longer a safe haven during stress that’s a major shift

Technical & Sentiment Breakdown: Breadth Improves, but Sentiment Stretches

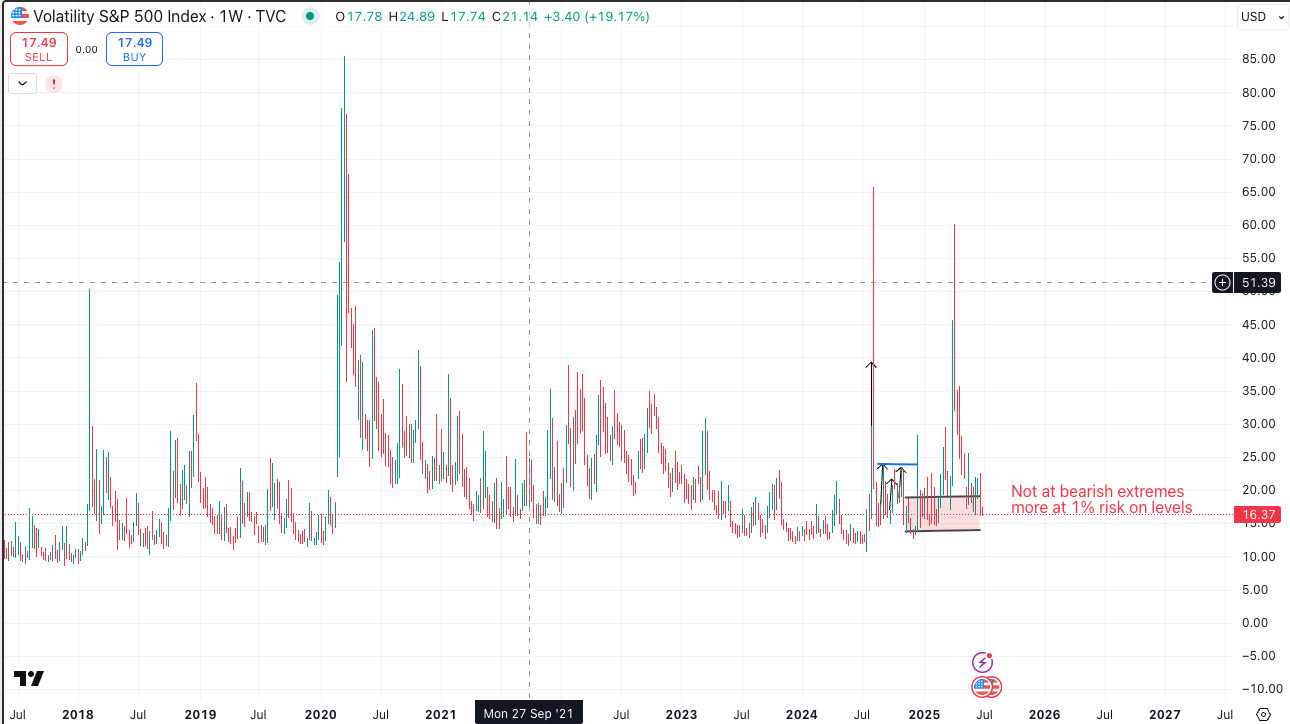

Positioning Snapshot

- VIX: Multi-month lows, showing implied calm

- Put/Call Ratio: Bullish skew (0.56), but not frothy

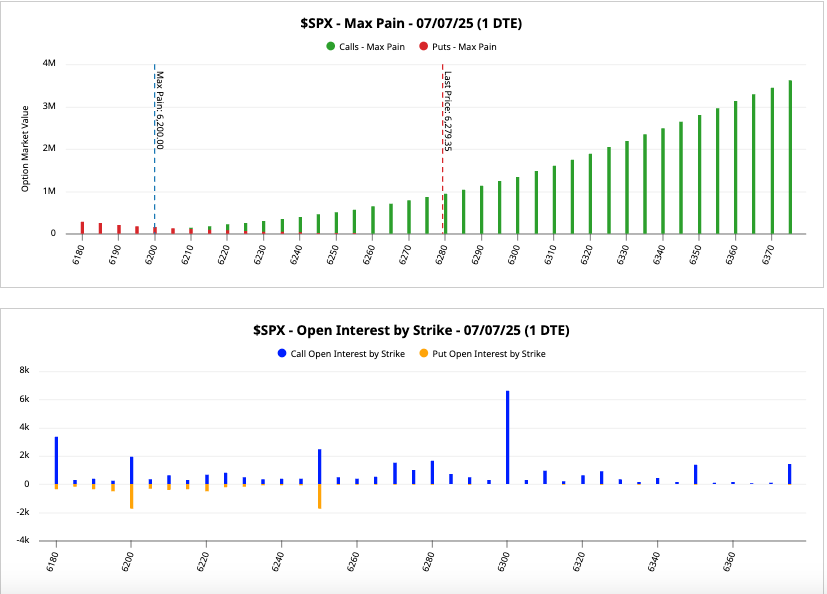

- Gamma Landscape: SPX 6300 call wall, Max Pain 6200—expect pinning near expiry

- Fear & Greed Index: firmly in “Greed” zone, but not manic

The uptrend is intact, and sentiment isn’t at red-alert levels—but we’re certainly not early. This is classic melt-up territory, powered by under-positioning finally catching up.

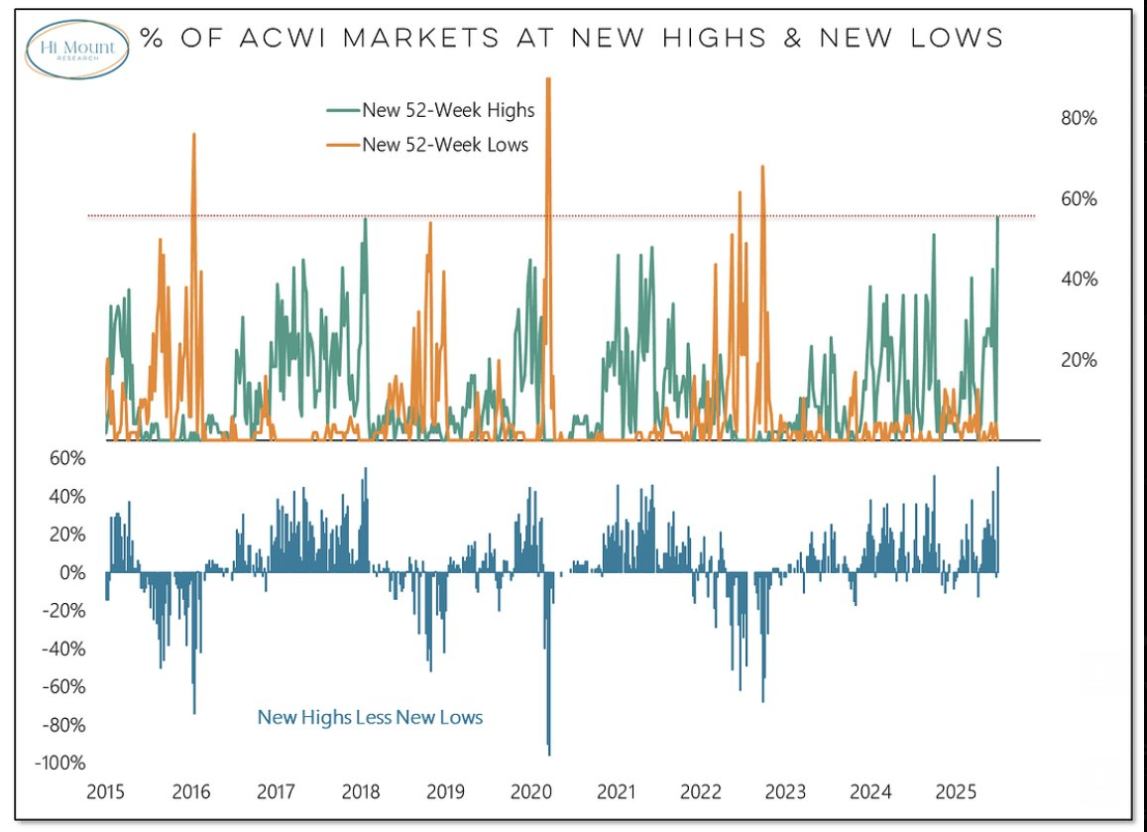

Breadth Turning Up—Finally

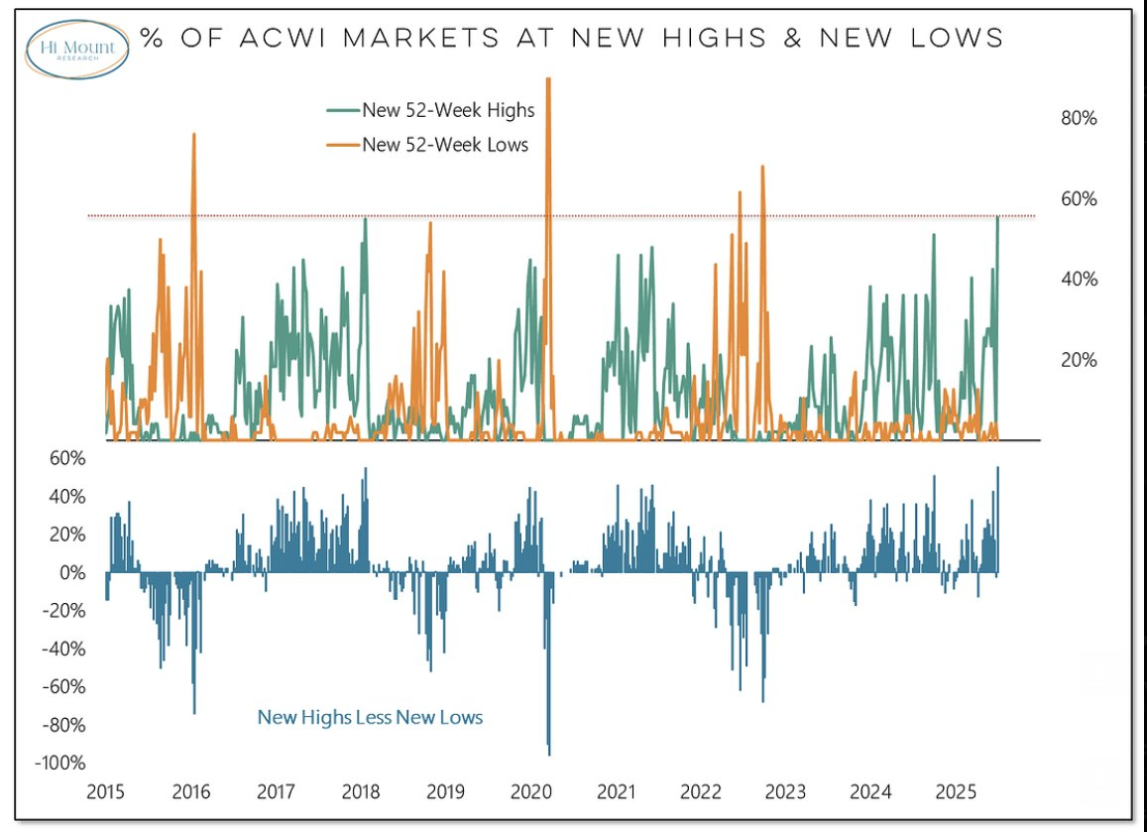

- Small caps and financials caught a bid last week

- Global equities (ACWI) broke resistance

- Participation breadth now rising, not fading

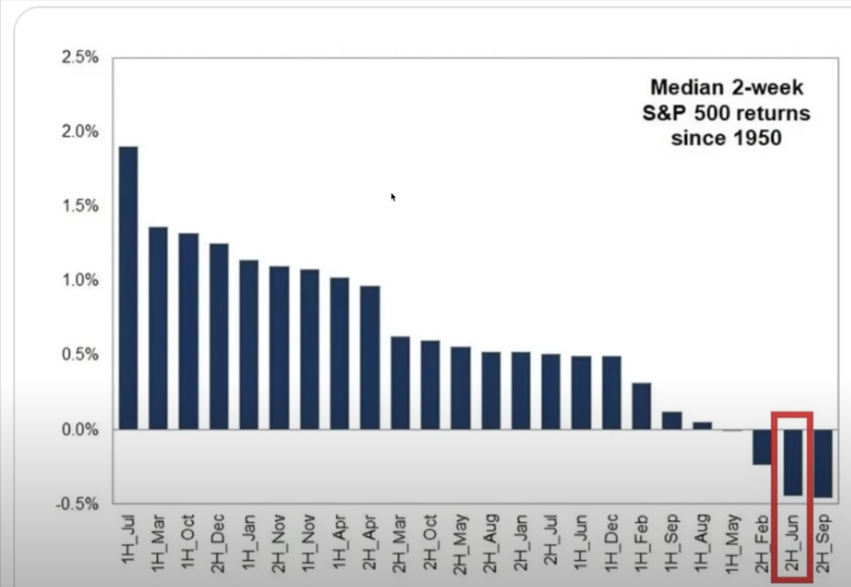

Seasonality Remains a Bullish Anchor

July's first half is historically one of the strongest stretches of the year, and this year is playing to script. But note: after massive May/June gains, July often introduces chop,especially post-CPI and into earnings season.

Last Week’s Recap: Strong Jobs, Soft Private Payrolls, and Steady Gold

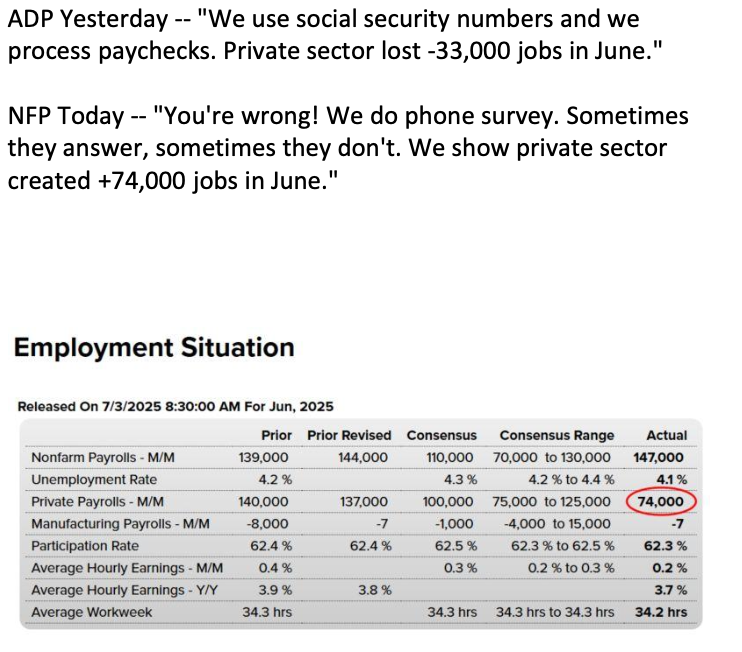

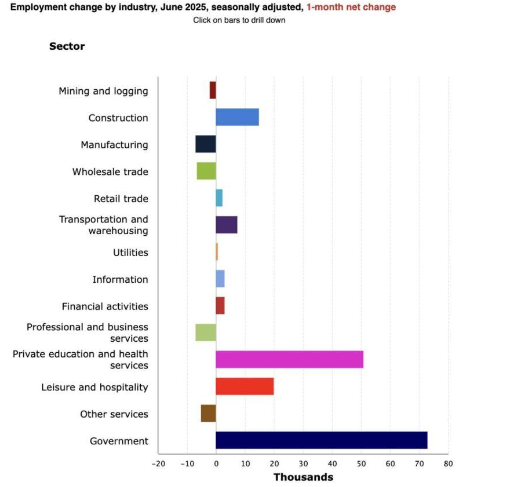

The June NFP report came in hotter than expected—147k vs 95k whisper—but the quality of the beat was questioned.

- Education and Health drove the print, likely from seasonal adjustments

- Private payrolls and manufacturing jobs declined, in line with weak ADP

- Wages softened to 3.7% YoY—lowest since July 2024

- Unemployment rate ticked down to 4.1%, despite a shrinking labour force

Net takeaway? The report was good enough to remove a July cut, but not strong enough to derail the September pivot narrative.

Elsewhere

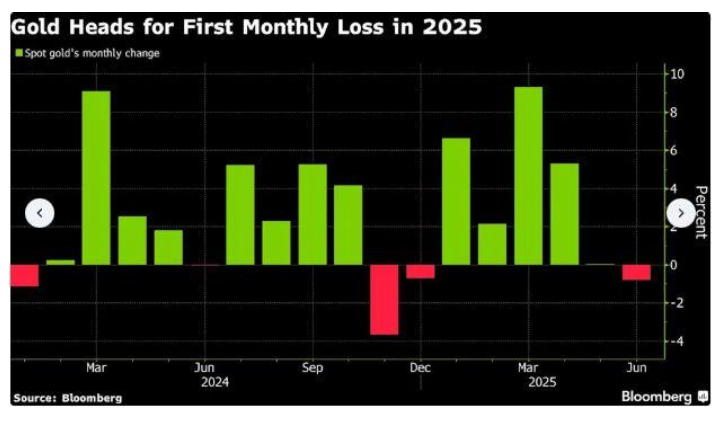

- Gold held firm, supported by central bank demand and deflation fears

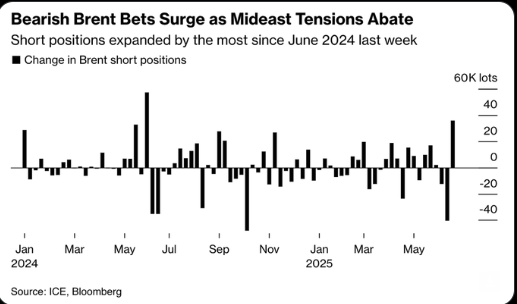

- Oil reversed lower, with Trump waiting to refill the SPR at cheaper levels

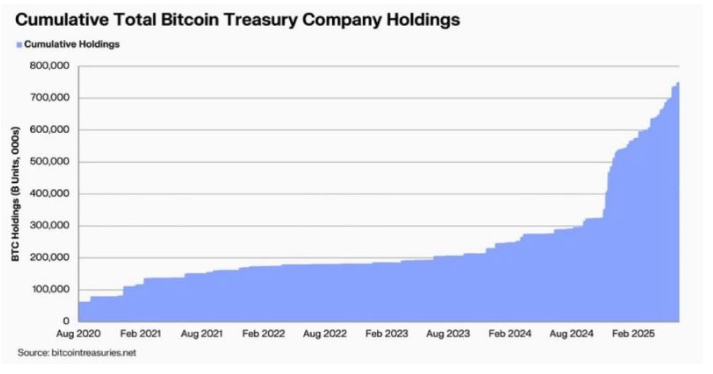

- Crypto broke out, driven by institutional accumulation and tokenisation news

The Week Ahead: Tariff Deadline, Global CPI, and Central Bank Crosscurrents

While earnings season hasn’t officially kicked off, this week brings some macro fireworks.

Monday, July 7

- UK Halifax House Prices

- Eurozone Retail Sales

- US Treasury Bill Auctions

Tuesday, July 8

- RBA Rate Decision (cut expected)

- US NFIB Small Business Optimism

- NY Fed Consumer Inflation Expectations

- US Consumer Credit

Wednesday, July 9

- Trump Tariff Letter Deadline

- China CPI/PPI

- RBNZ Rate Decision

- FOMC Minutes

Thursday, July 10

- US Initial & Continuing Jobless Claims

- Italy Industrial Production

- 30Y Bond Auction

Friday, July 11

- UK GDP

- German and French Final CPI

- Canadian Employment & Wages

- US Federal Budget Balance

Alpha Takeaway: The Bull Charges On, But Watch the Curveball

The rally is real, but the risks are rising:

- Tariff volatility is unpriced

- Breadth is improving, but stretched sentiment could trigger air pockets

- Central banks are increasingly worried about deflation, not inflation

- Dollar weakness is structural, not temporary

Our Stance

- Stay long SPX above 6200 with tight stops

- Add on dips in Gold and Crypto— safe havens with structural tailwinds

- Rotate into small caps and financials if breadth holds

- Be tactical around CPI, earnings, and the July 9 tariff deadline