Markets retreat as geopolitics flare, Fed and SNB rate moves loom, and equity breadth collapses

Here’s your full macro rundown, technical setups, and trading forecast for the week ahead.

Setting the Stage: Markets on Edge, Not in Panic (Yet)

Last week, markets stared down a textbook geopolitical risk event—and flinched. On Friday, major indices posted their worst day in weeks:

- S&P 500: -1.13%

- Dow Jones: -1.79%

- Nasdaq 100: -1.29%

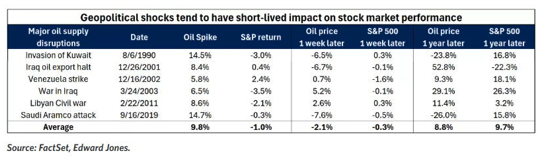

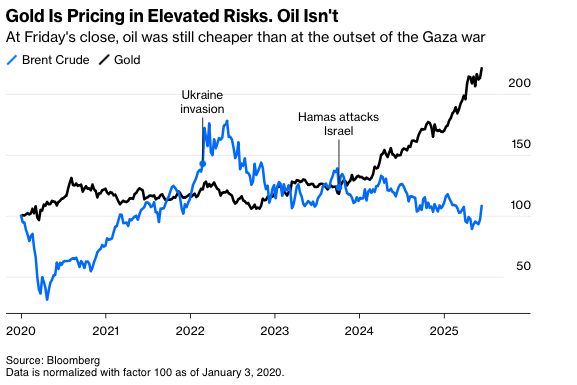

The trigger? Israeli military strikes on Iranian nuclear facilities, exactly 60 days after Tehran blew past the U.S. dismantling deadline. But unlike past cycles, the market didn’t go full panic mode. Safe-haven plays like the U.S. dollar and Treasuries didn’t catch meaningful bids.

Instead, capital rotated into Gold, which remains the primary recipient of geopolitical hedging flows, and Oil, which spiked on fears around the Strait of Hormuz—a corridor for nearly 20% of global oil supply.

Equity sentiment was already showing signs of fatigue. Breadth had narrowed, insiders like Meta’s Zuckerberg were selling, and institutional flows were lightening up. The market wasn't caught off guard—it was already nervous.

Macro & Policy Watch: Central Banks, CPI Surprise & De-Dollarisation

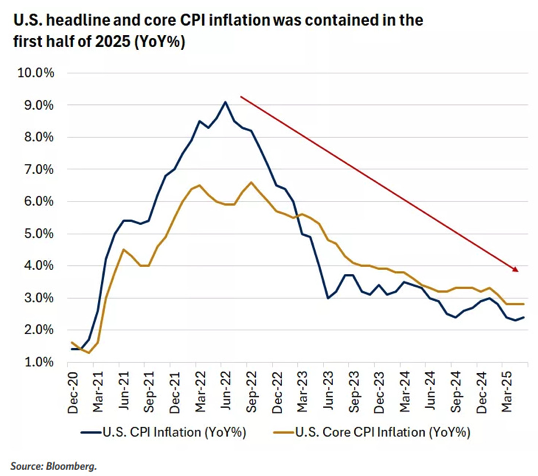

Inflation: Cool as a Cucumber

The May CPI release was a macro jaw-dropper. No analyst in the Bloomberg survey saw it coming:

- Core CPI: -1.13%

- Supercore CPI (ex-shelter services): -1.79%

- Shelter costs continue to ease, with recreation and travel showing cyclically soft prints

It looked like a pre-pandemic inflation report—low, boring, and oddly comforting. However, analyst warn that May’s data only priced in half of the new tariff impacts. The full inflationary wave (if any) may show up next month.

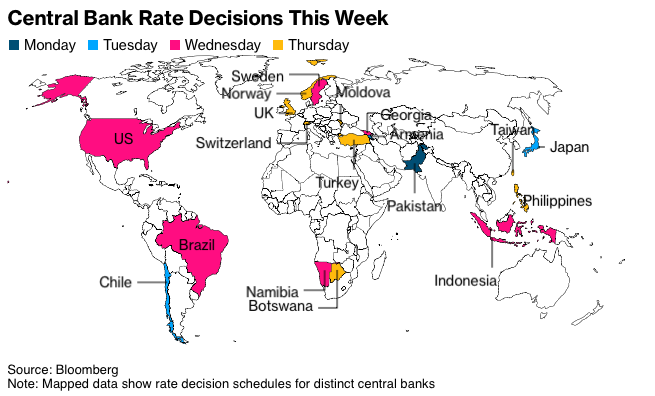

Central Banks Galore

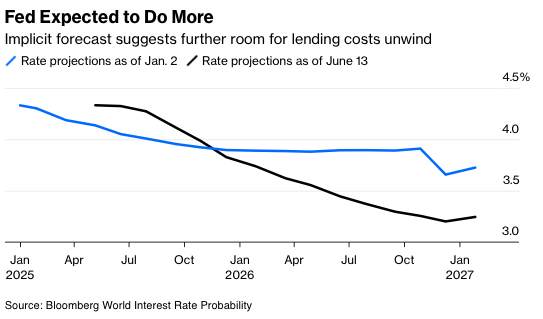

Federal Reserve (Wed)

Expected to hold, but the Summary of Economic Projections (Dot Plot) will be the showstopper. Markets want a dovish tilt, especially post-CPI.

SNB (Thu)

A cut to 0% is on deck. Swiss inflation is tame, the franc is too strong, and short-term yields are already sub-zero.

BOE, BOJ, Riksbank

All are expected to hold, but forward guidance matters. The BOE faces stagflation risks, while the BOJ must address a hawkish market despite economic softness.

De-Dollarisation & Flow Quirks

Despite strong U.S. yields, the dollar isn’t acting like a classic haven. Global capital continues to diversify:

- $15B into bonds

- $1.7B into gold

- $10B out of equities

Rate differentials aren’t luring dollar bulls, possibly due to de-dollarisation flows globally. Powell knows he’s fighting more than just inflation now—he’s fighting a confidence war in a bifurcated macro regime.

Technical & Sentiment Breakdown

Market Internals Breaking Down

Market strength is thinning:

- S&P 500: 97 new highs vs 242 new lows (net -145)

- Nasdaq 100: Short-term momentum cracked; only 22.7% of components above 5-day MA

- Russell 1000: Worst breadth print—net -400 on 5-day highs vs lows

This isn’t a “collapse” scenario yet. But it’s the kind of internal breakdown that usually precedes a corrective phase, especially with institutions exiting weaker names.

Last Week’s Recap: CPI Eases, Risk Rises

Markets were riding high until Friday’s geopolitical jolt: Israel hit Iranian nuclear infrastructure, escalating tensions but stopping short of full panic. Gold rallied, equities dropped, and bonds shrugged—a curious mix of risk-off behaviour.

CPI Shock

Meanwhile, May’s CPI print shocked to the downside:

- Core CPI: +0.13% MoM

- Supercore inflation: just +0.06%

- Shelter and cyclical services cooled notably

Flows Showed Increasing Caution

- $10B out of stock

- $15B into bonds

- Institutions dumped U.S. equities for a fifth straight week—the worst stretch since 2008

On the micro front, Adobe beat but flagged AI concerns, while Amazon and Walmart stirred fintech disruption with talk of stablecoins.

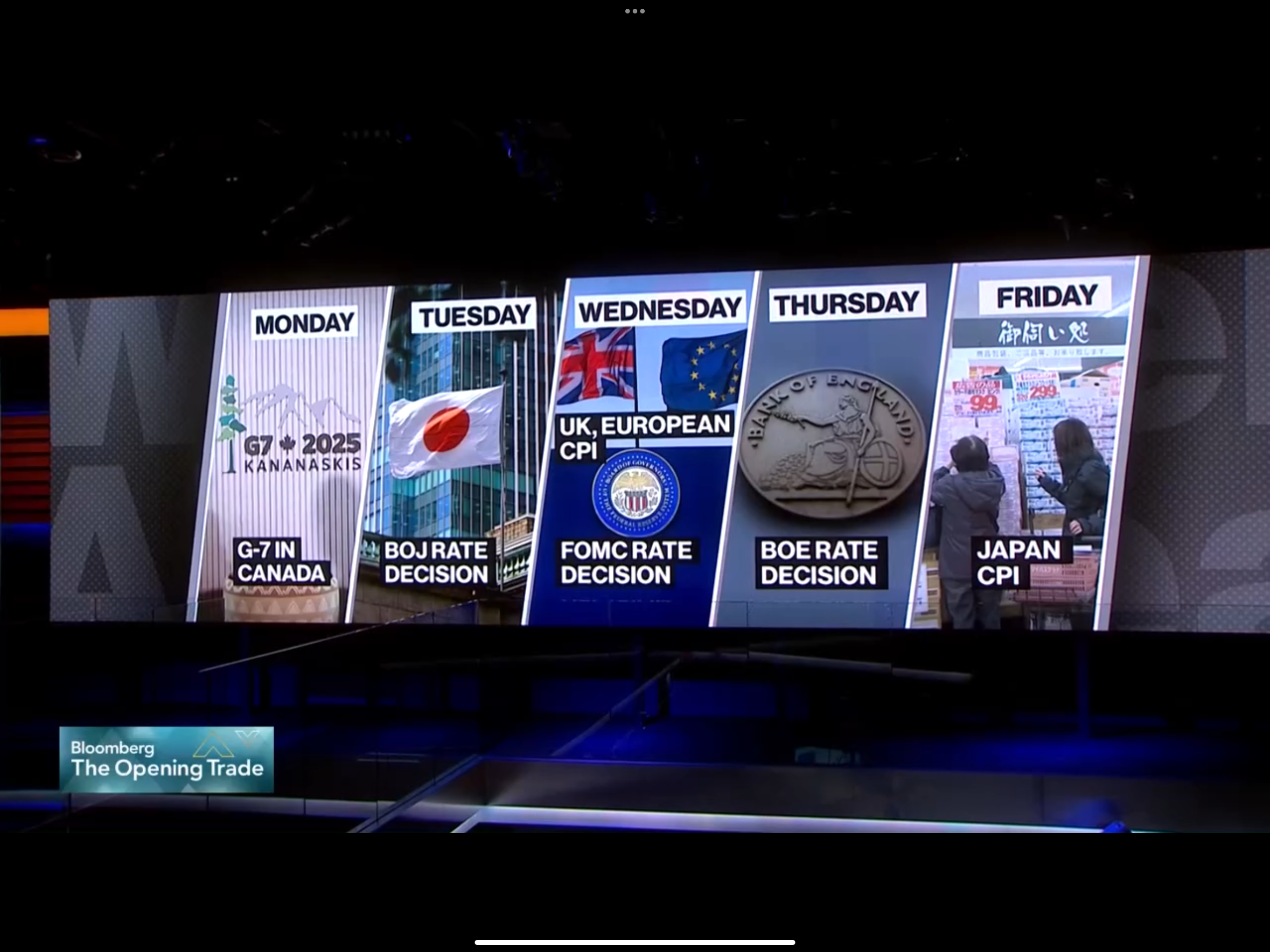

Week Ahead: Central Banks, CPI Waves, and Retail Realities

A massive week for macro watchers as five major central banks speak, CPI fallout is measured, and retail sales take the spotlight.

Monday, June 16

- CHF PPI could confirm SNB’s need to cut

- China Retail Sales, Industrial Production & Fixed Asset Investment

- Eurozone Q1 wages and labour costs

- OPEC Monthly Report

Tuesday, June 17

- BOJ Rate Decision (hold expected)

- U.S. Retail Sales + Import/Export Prices

- Industrial Production & Business Inventories

- German ZEW Sentiment

- ECB Villeroy & Centeno speak

Watch: Retail sales closely—CPI showed weak goods inflation, but tariffs may now bite.

Wednesday, June 18

- GBP CPI/RPI, Eurozone CPI, Sweden Rate Decision

- U.S. Building Permits, Housing Starts, Atlanta GDPNow

- FOMC Rate Decision & Dot Plot (SEP) – main macro event

- Powell Press Conference

- 30Y German Bund Auction

Thursday, June 19 (U.S. Juneteenth Holiday)

- CHF Rate Decision & Press Conference

- BOE Rate Decision & Minutes

- ECB Lagarde, Villeroy, De Guindos speak

- NZ GDP, AUD Employment, CHF Trade Balance

- U.S. jobless claims (released early due to holiday)

SNB likely to cut to 0%; BOE faces a stagflation trap.

Friday, June 20

- UK Retail Sales, German PPI, Japan CPI

- U.S. Philly Fed & Leading Index

- Eurozone Consumer Confidence

- BOJ Ueda speaks, ECB Bulletin release

Final inflation and sentiment readings to close a heavy macro week.

Alpha Takeaway: Short-Term Pullback Before the Next Impulse

Markets are in transition, not crisis. The soft CPI may buy time, but risks remain stacked: geopolitical flashpoints, equity breadth breakdown, and CBs trapped between slowflation and reflation.

Our Stance

- Hold core Tech

- Stay long Gold especially if conflict escalates

- Add to Defence stocks

- Keep cash for dips—expect a 2–3% retracement ahead