Geopolitics, Gamma, and a Grind Higher: Markets Lean In, But Summer Risks Linger

Markets enter the week walking a tightrope between macro fear and positioning momentum. The Iran strike, looming tariffs, and Q2 earnings risk all swirl into a cocktail of “risk-aware” rallying.

Market Overview: “The Only Certainty is Uncertainty”

Markets ended last week with a bang: a huge buy program into Quad Witching close, followed by an apparent U.S. strike on Iran’s nuclear sites. You’d expect chaos. Instead? Futures yawned, oil popped and faded, and equities held flat.

That’s your signal: this is a market looking through geopolitical drama, for now.

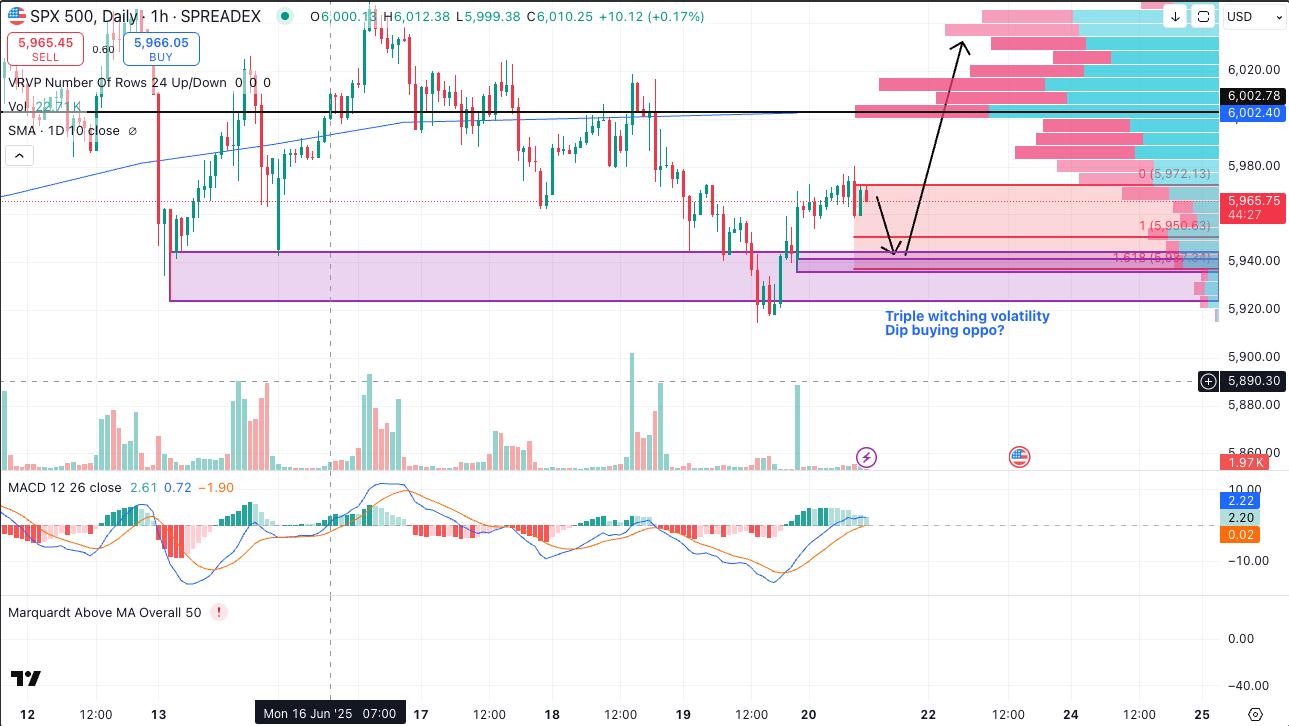

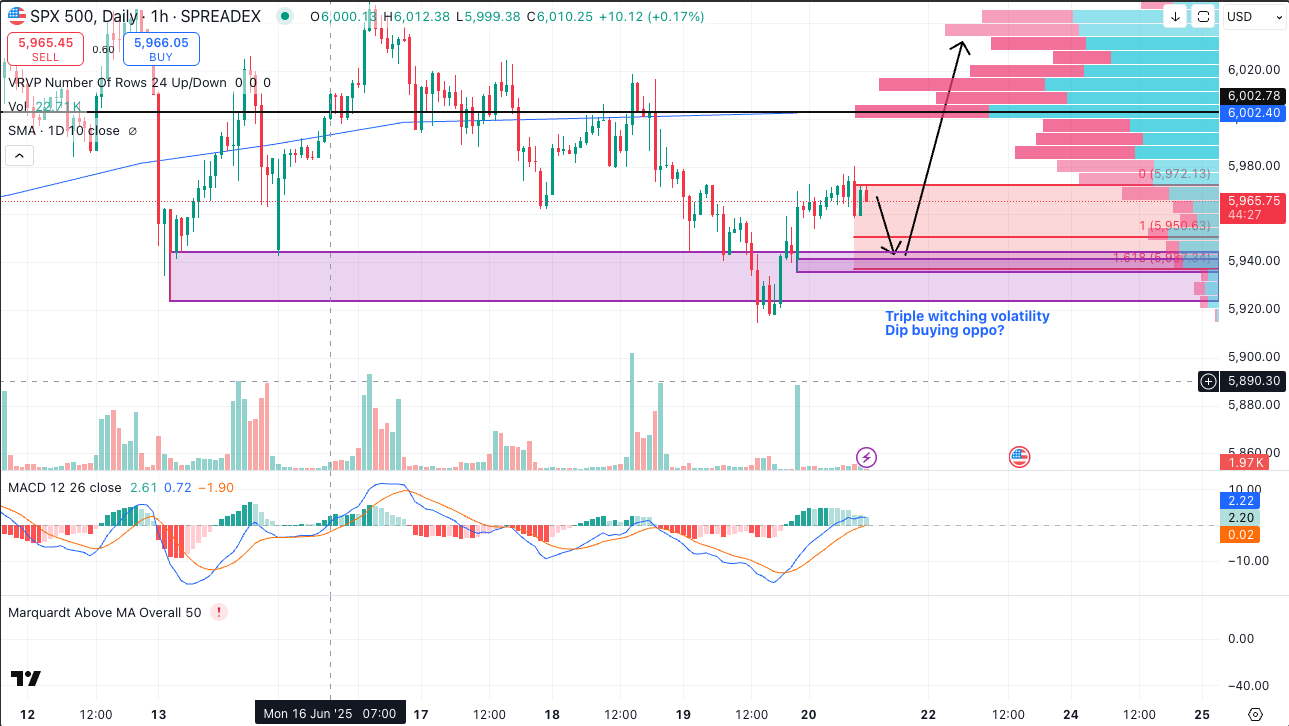

We’re hovering just 3% from SPX all-time highs, with the gamma flip at 5931 SPX defended overnight. Oil spikes and dollar dips aren’t triggering panic. But the setup says the rally from April lows could be topping out soon, with a proper summer consolidation to follow.

Key Sentiment Signals

- No VIX spike despite Middle East escalation

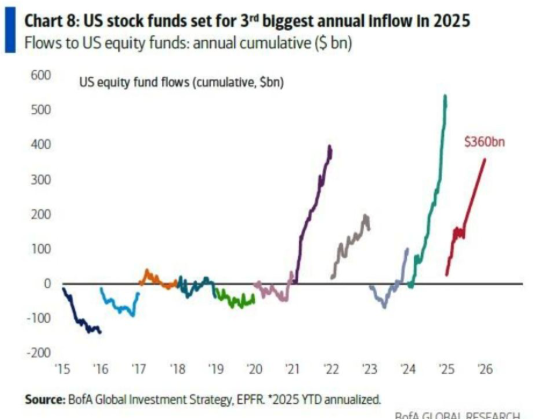

- Record equity inflows: $45B in 4 weeks, $360B annualised

- Dollar near consensus exhaustion zone (~DXY 95-96)

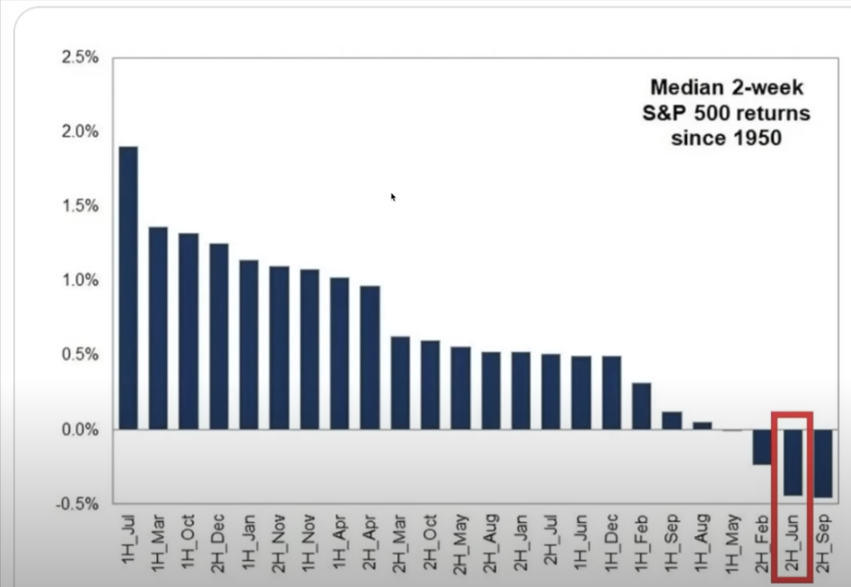

- July seasonality is strong, but end-of-June is weak historically

- Buybacks paused, leaving equities vulnerable to earnings volatility

Macro & Policy Watch: Tariffs, Central Banks, and the Middle East Wildcard

Iran Tensions: “Targeted, Swift, and Market-Tolerated”

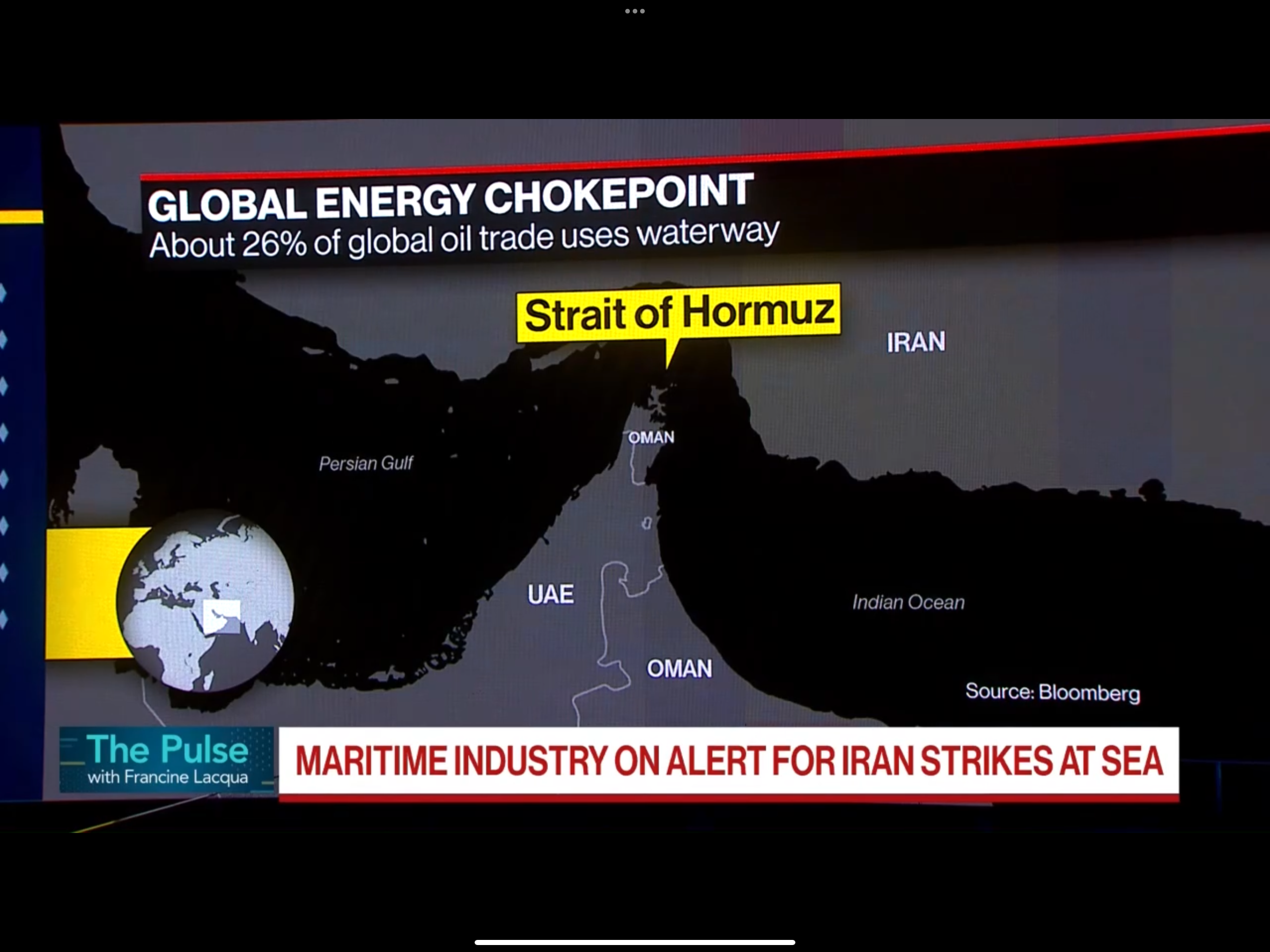

Reports confirmed U.S. action against Iranian enrichment facilities. Tehran has threatened to close the Strait of Hormuz, and analyst are already whispering $120+ oil. But for now, markets see it as containable, not escalating.

The real macro swing factor? July 9th U.S. tariff deadline. Traders expect volatility and possible resolution, but even a temporary “Trump solution” may not calm supply chains overnight.

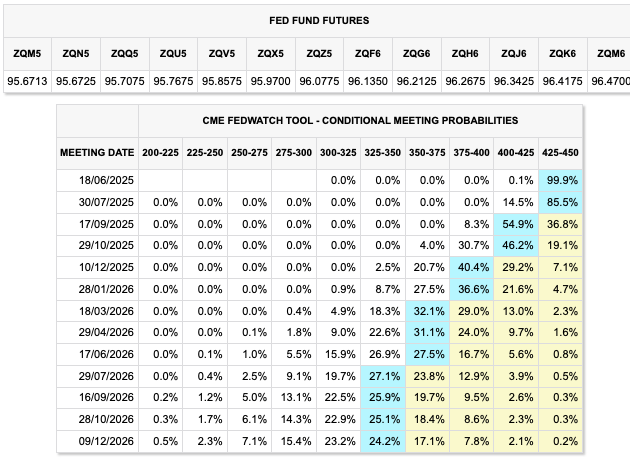

Central Banks: Dovish Drift Without a Fed Put

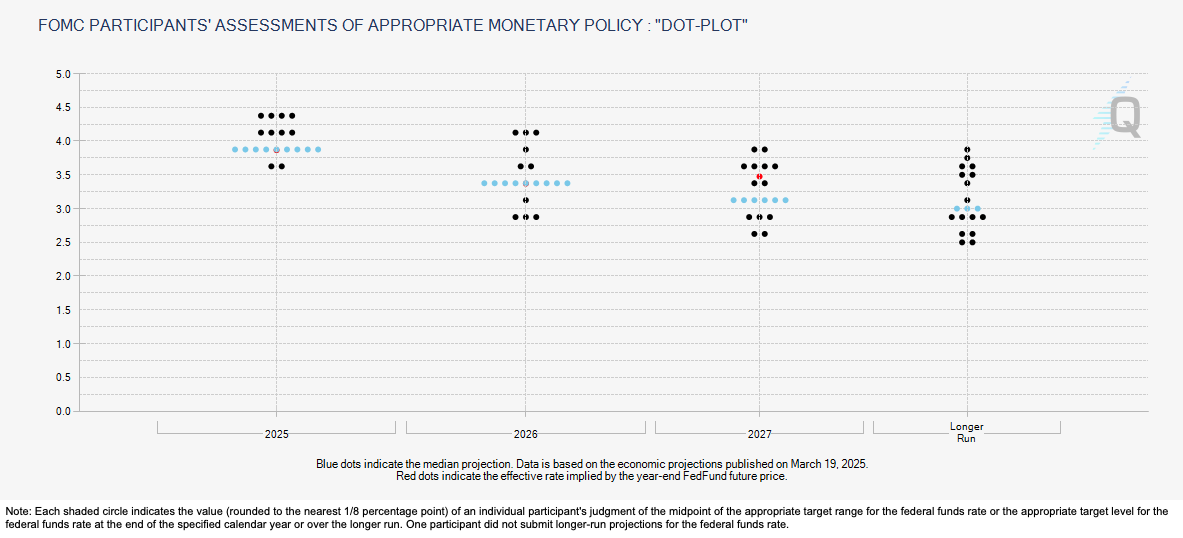

FOMC

Held rates, but raised inflation forecast to 3% for 2025. No help here.

BoE

No change, but a 6–3 split hints at August cut odds rising.

SNB and Sweden

Cut rates, citing falling inflation and weak growth.

Fed Speakers

Split between “ready to cut” (Waller) and “stand firm” (Barkin).

Powell stays cautious, citing the tariff's impact on inflation.

Meanwhile, the euro is benefiting from capital flows as Lagarde pushes “Europe’s moment” and deflation hits producer prices across the region. China’s export deflation adds fuel.

Technical & Sentiment Setups

Markets are walking the line between breakout optimism and geopolitical dread. The SPX defended its key gamma flip level at 5931, which corresponds with expiry pivots around ES 5985. This area remains critical—breaching it could trigger dealer-driven selling, while holding above supports a grind higher.

From a wave structure view, the move off the April “Liberation lows” appears to be in a potential equal-legs extended wave 4 consolidation. That implies near-term choppiness before a proper summer breakout.

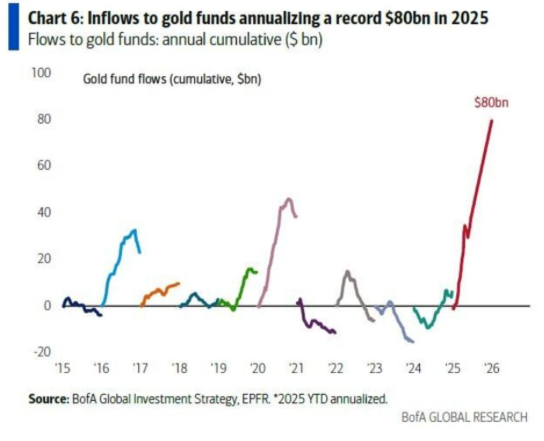

Meanwhile, precious metals remain stealth leaders. Despite geopolitical risk, gold and silver haven’t exploded—but the technicals say “stay ready.”

Gold

Best-performing asset class YTD. Inflows topped $2.8B last week—the biggest in 8 weeks. Wealth clients are still underweight (~0.4% AuM), suggesting plenty of room to run.

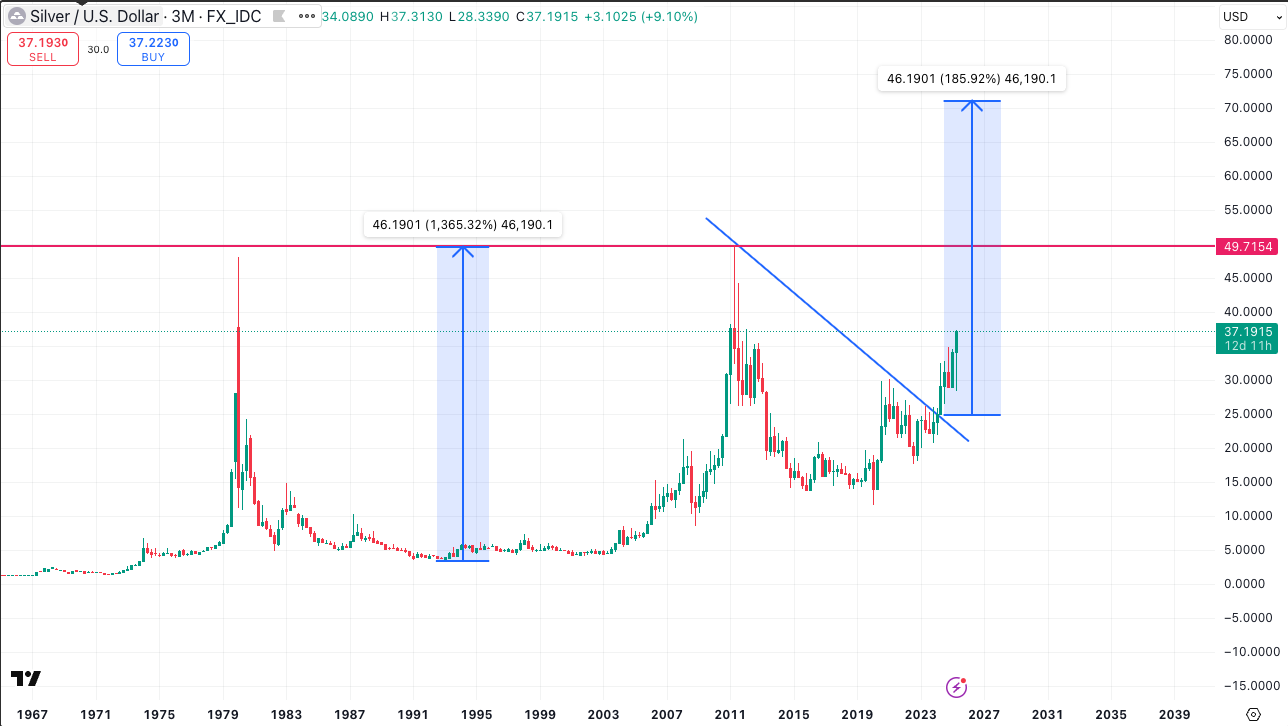

Silver

Breaking into a 12-year cup & handle pattern—technical bulls watching closely.

Dollar

Hovering near consensus oversold territory. DXY in the 95–96 zone could trigger a cathartic reversal. A breakdown would support further gold upside.

Sectors to Watch

Airlines, travel (oil-sensitive) may lag temporarily, but this may not last.

Key Setups

- SPX: Defended gamma flip at 5931

- ES futures expiry magnet at 5985

- Silver: Cup & handle in progress

- Gold: Inflows rising, under-ownership persists

- DXY: Nearing flush zone at 95–96

Last Week in Review: Strikes, Soft Data, and Flow Frenzies

Markets were shaken—but not stirred—by last week’s headlines:

Geopolitics

U.S. hit Iranian nuclear sites. Iran threatened Hormuz closure. Oil spiked, then faded.

Retail & Housing Data

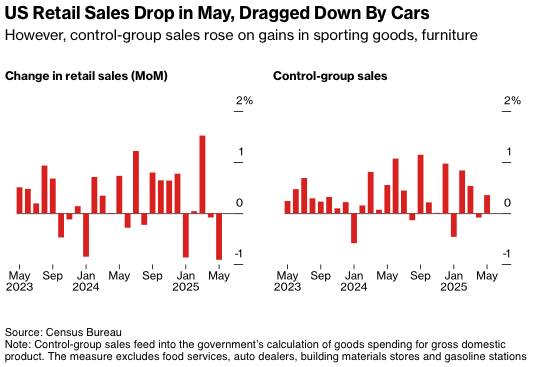

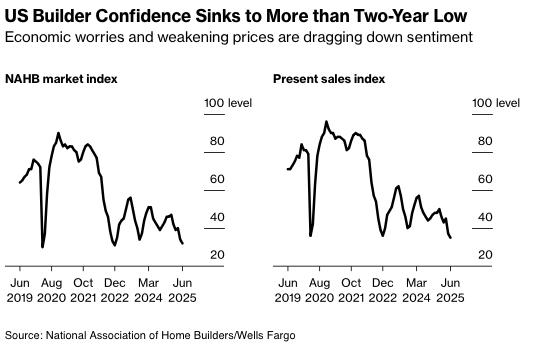

U.S. Retail Sales missed but Control group (GDP feed) solid, housing starts plunged nearly 10%, and NAHB sentiment hit decade lows in the South.

Fed

Dovish tone but hawkish SEP. No rate cuts until inflation falls.

Flows

U.S. equity inflows remain strong; EM debt saw its second-largest weekly inflow ever ($4.8B).

China

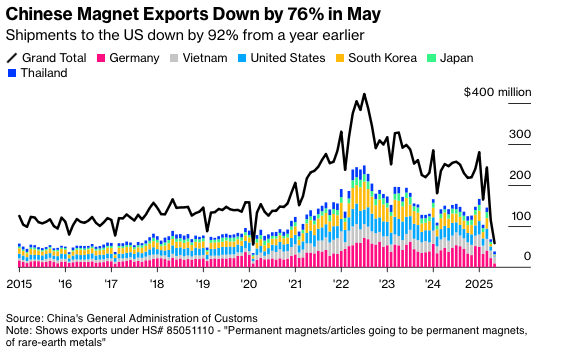

Export crash in rare earths (magnets down 76% YoY). Retail sales surged following Dragon Boat Festival subsidies.

The Week Ahead: Central Bank Parade, Macro Minefields, and Market Crossroads

This week features a heavy calendar of central bank speakers and macro prints, just as markets hover near key resistance.

Monday, June 23

- Global PMIs

- U.S. Existing Home Sales

- Multiple Fed and ECB speakers

Tuesday, June 24

- Germany IFO

- Canada CPI

- U.S. Conference Board Consumer Confidence

- Fed Chair Powell speaks

Wednesday, June 25

- U.S. New Home Sales

- Eurozone and UK car registrations (auto sector readthrough)

Thursday, June 26

- U.S. Q1 Final GDP

- Durable Goods

- Pending Home Sales

- Canada Wholesale Trade

- Fed & ECB speeches

Friday, June 27

- U.S. PCE, Personal Income & Spending

- UoM Confidence Surveys

- JPY CPI

- Eurozone Inflation & Business Surveys

This data-heavy week will likely set the tone for the July 4th holiday stretch and tariff deadline. Expect volatility. Traders should be ready to fade extremes, especially if macro beats or misses collide with geopolitical shifts.

Alpha Takeaway: Tactical Over Bold—For Now

The market is holding up remarkably well, but don’t mistake resilience for immunity.

The Backdrop Suggests the Following

- Consolidation likely: Extended wave 4 patterns imply we’re due for digestion after this rally

- Geopolitical flare-ups are headline-sensitive but not yet trend-breaking

- Tariffs are the real landmine—watch July 9th

- Dollar washout + gold buying = ongoing de-dollarisation story

- Buy dips—but not just any dip. Pick your spots around macro inflexion levels

Stay nimble. The next move could come from a Powell slip, a Hormuz flare-up, or a tariff headline at 2 a.m.