Markets defy gravity as liquidity surges, Fed signals remain mixed, and positioning remains cautious, but breadth continues to deteriorate

Here’s your complete macro deep dive, technical setups, and trading forecast for the week ahead.

Market Overview: ATHs with Narrow Breadth, Surging Liquidity, and FOMO Traps

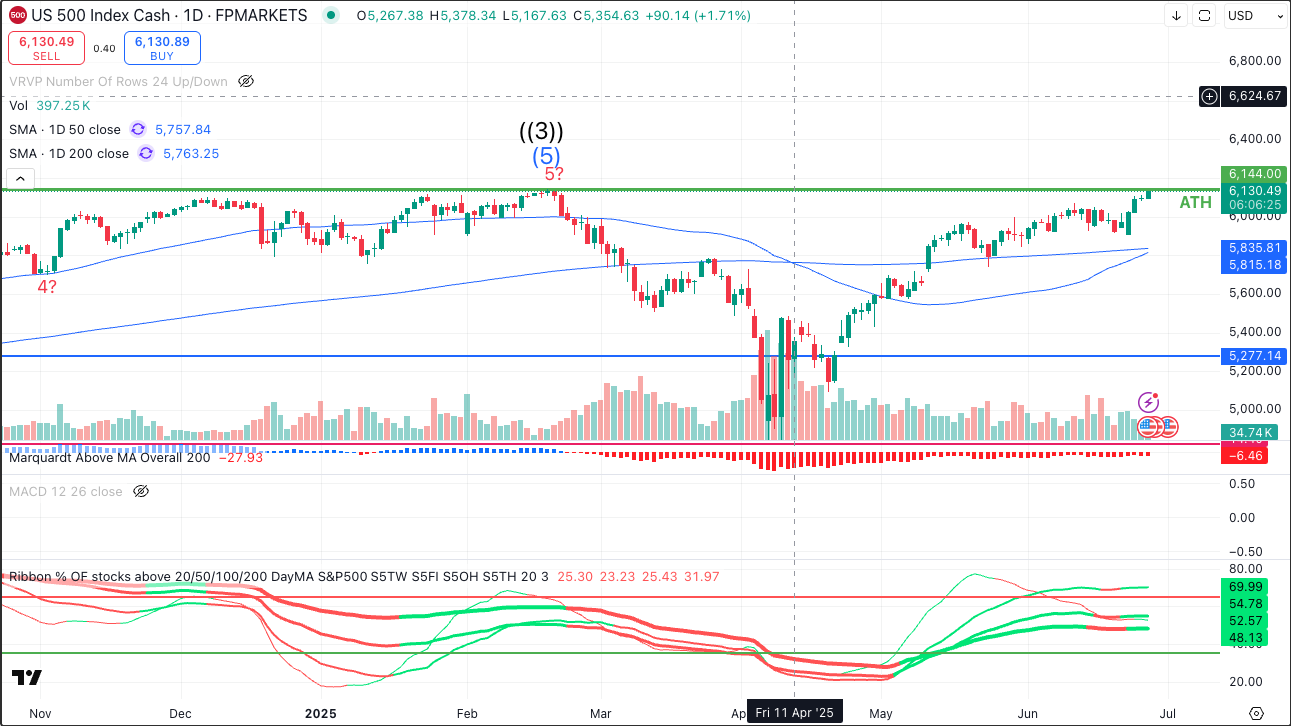

Markets charged into the final week of June with a powerful upside drift. The S&P 500 closed the week at all-time highs—but only 22 stocks in the index did the same. That kind of narrow leadership isn’t unusual at this stage in the cycle, but it does raise red flags for those watching participation breadth and institutional flows.

Traders looking for a pullback are getting steamrolled. With global M2 money supply pushing higher and political risks being sidelined, the path of least resistance remains up.

Key Market Signals

- VIX and MOVE are anchored at historically low levels

- HYG (high-yield bonds) has broken out—a clear risk-on tell

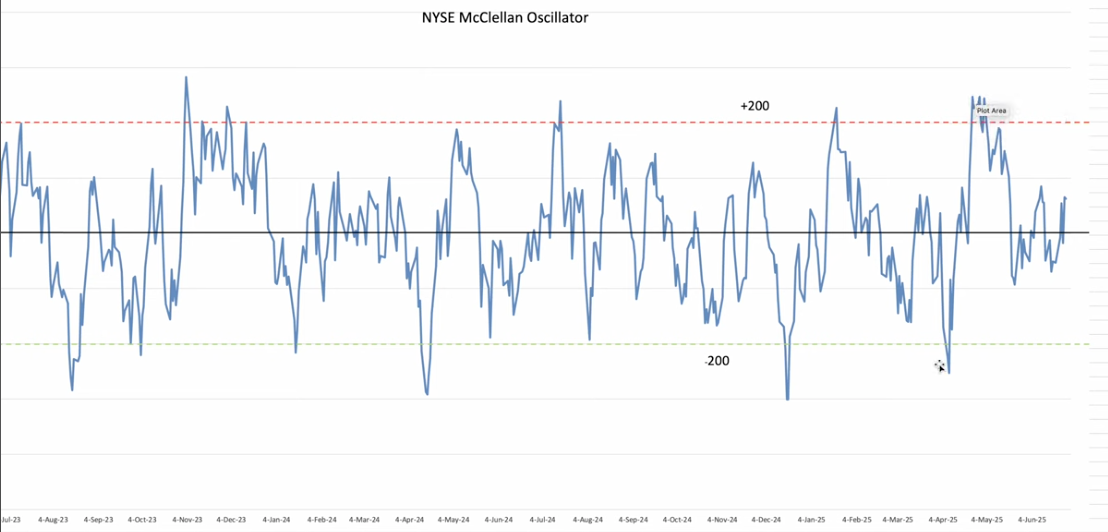

- The McClellan Oscillator remains in positive territory

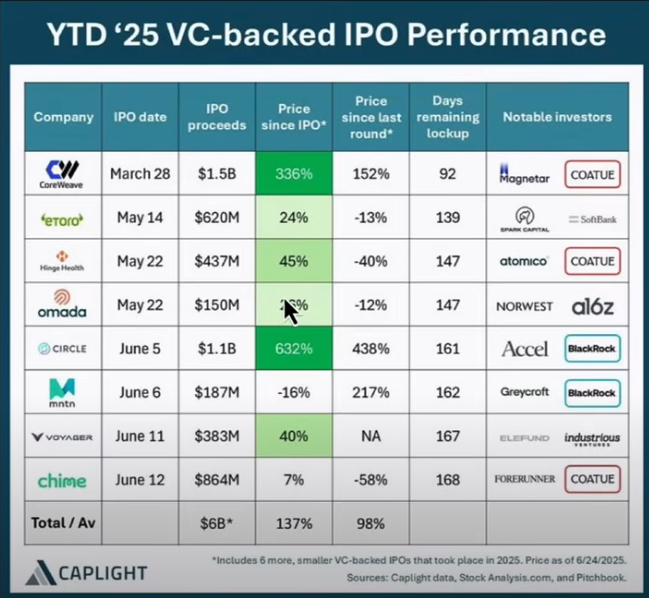

- Equity flows are being supported by a pickup in M&A and IPO activity

This isn’t a melt-up built on euphoria—yet. It’s being powered by liquidity, policy, and under-positioning.

Macro & Policy Watch: Shadow Fed, Trump’s Tax Clock, and Dollar Dump Dynamics

Powell Pushback vs Political Pressure

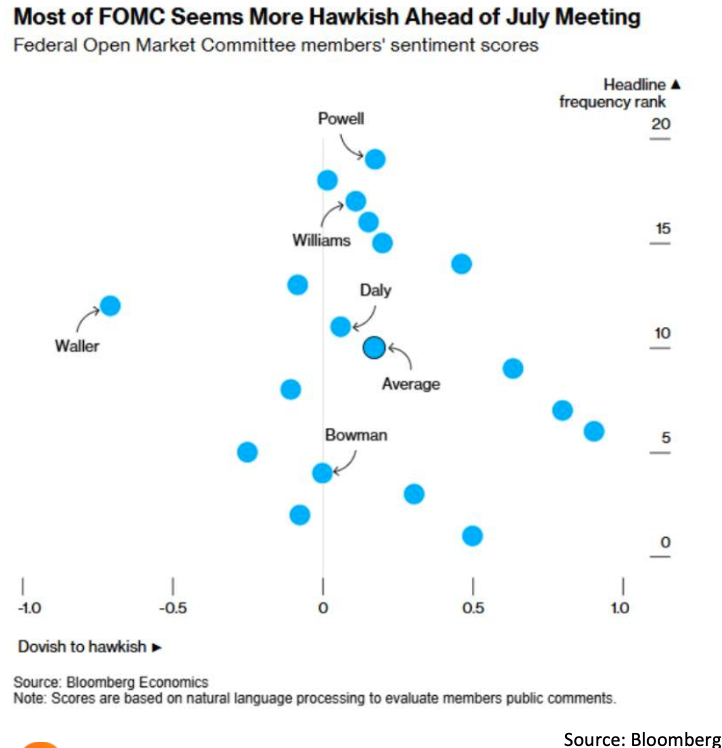

Last week, Powell and other Fed officials tried to throw cold water on July rate cut speculation—but the market didn’t fully buy it. With former Trump appointees like Waller and Bowman floating July cuts, the Fed's independence is under scrutiny. Even as Powell reasserts control, the idea of a “Shadow Fed Chief” remains a looming political risk.

Rate Cuts: When, Not If

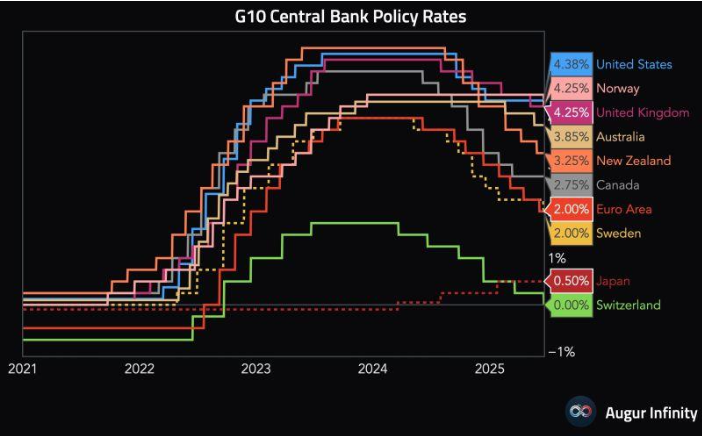

Markets aren't necessarily reacting to dovish rhetoric—they’re front-running what seems inevitable. G10 yields are falling, global inflation is easing, and M2 is rising. The current Fed speak may delay action, but traders believe it won’t change the outcome.

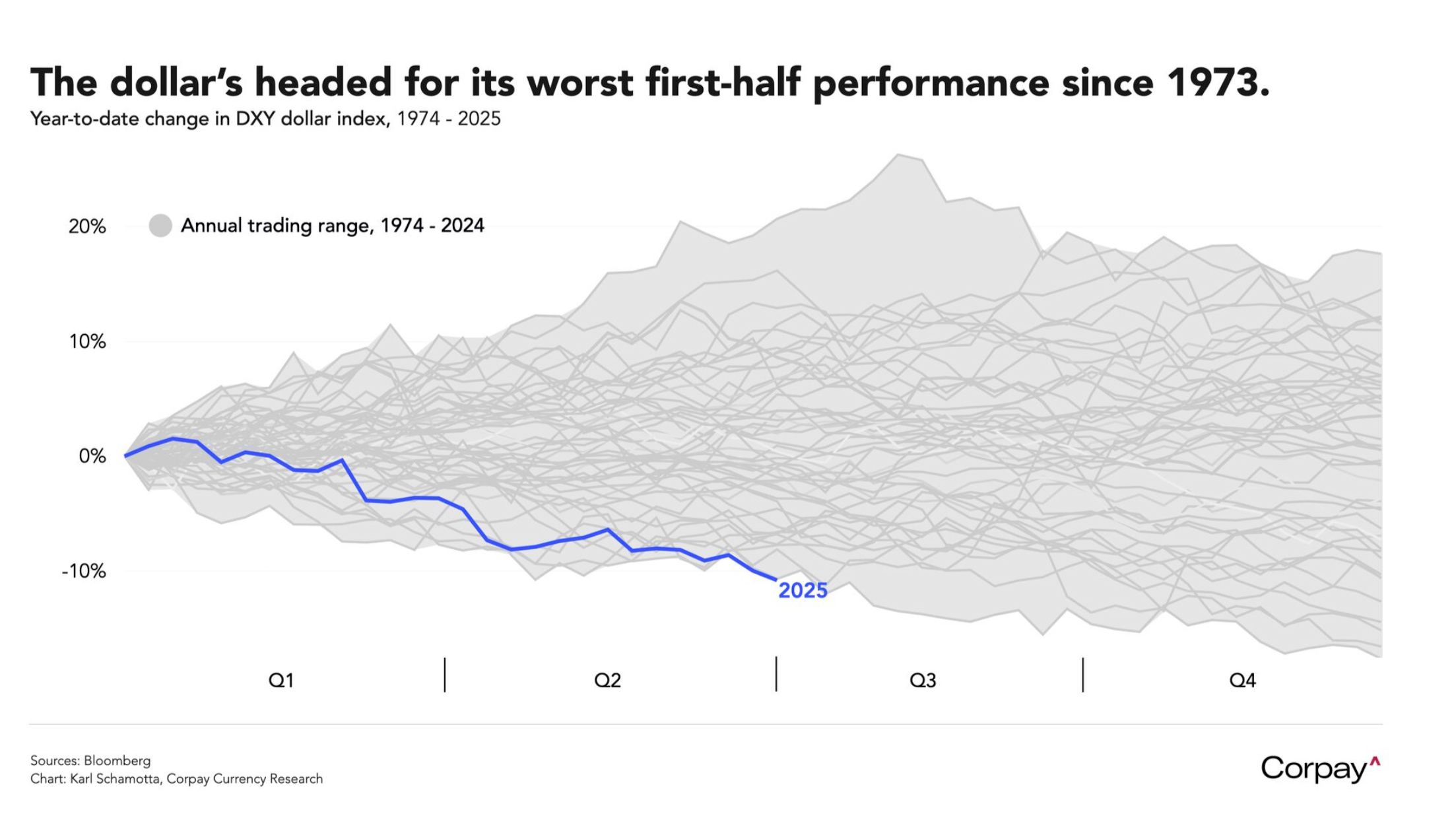

- The U.S. Dollar is in freefall, marking one of its worst stretches in years

- Rate differentials no longer support the greenback

- Liquidity is rising faster than inflation

Outside the U.S.: Reflation vs Stimulus Watch

- Germany’s PMI surprised to the upside, sparking hopes of a reflationary turnaround in Europe

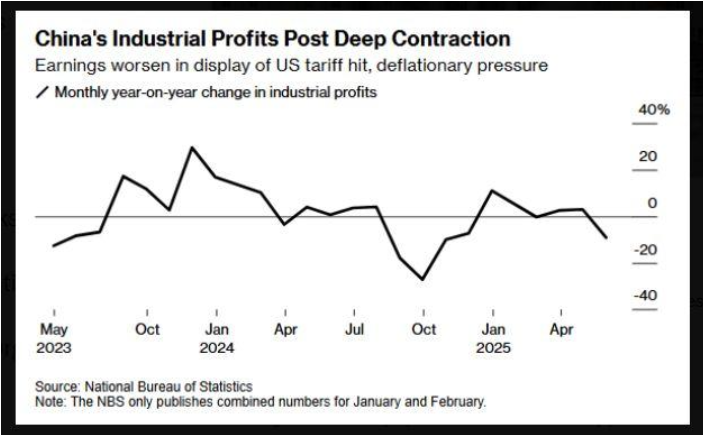

- Meanwhile, China’s corporate profits continue to disappoint, keeping the door open for a fresh round of stimulus out of Beijing

Bottom line: The market is pricing in easing, regardless of central bank rhetoric. The Fed may still hold in July, but expectations for a September pivot are building.

Technical & Sentiment Breakdown: Seasonality, Gamma Exposure & Option Frenzy

Seasonality Tailwinds Remain Intact

Statistically, July’s first half is one of the strongest stretches for equities. When June closes strong—as it did this year—July tends to continue the trend. Add a lack of fear, rising gamma levels, and light positioning, and the melt-up narrative gains legs.

Key Technical Signals

- The Nasdaq just triggered a Golden Cross, echoing the March 2023 signal that preceded an 82% rally

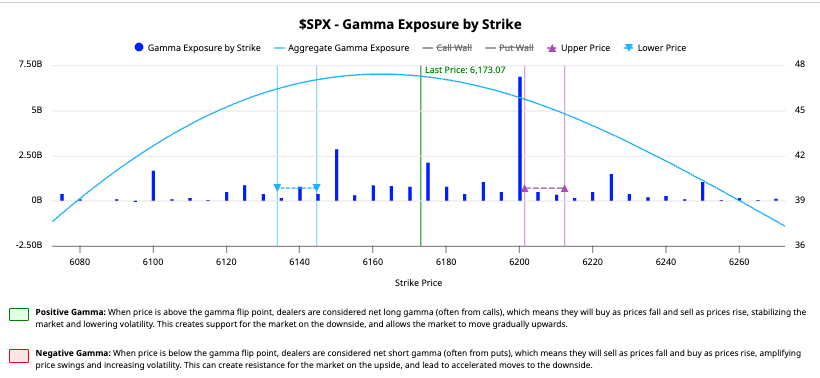

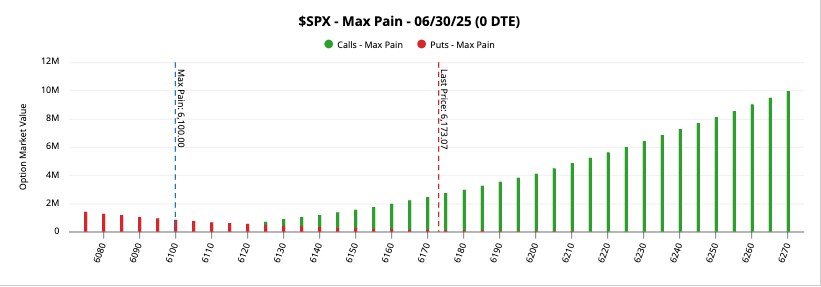

- Gamma exposure is now stacked around SPX 6200, while Max Pain sits at 6100

- 0DTE options volumes remain sky-high, amplifying intraday volatility and dealer hedging dynamics

- Momentum is still building—SPX looks primed for a breakout continuation

Last Week’s Recap: Powell Holds the Line, Housing Cracks, and Crypto Lifts Off

Markets absorbed a key week of Fed speeches, inflation data, and macro signals:

- Core PCE came in at +2.7% YoY—above expectations

- Real incomes and consumption declined

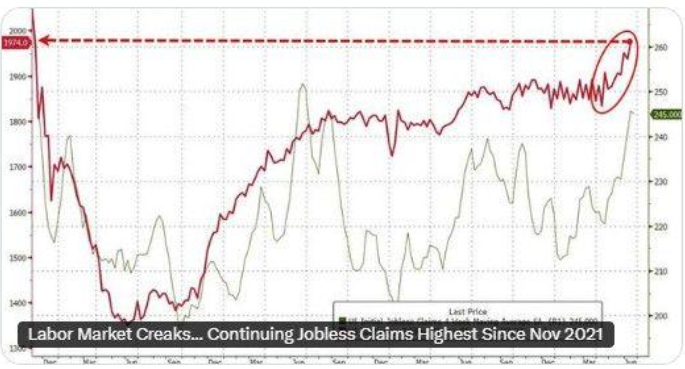

- Continuing claims climbed, signalling softening in labour markets

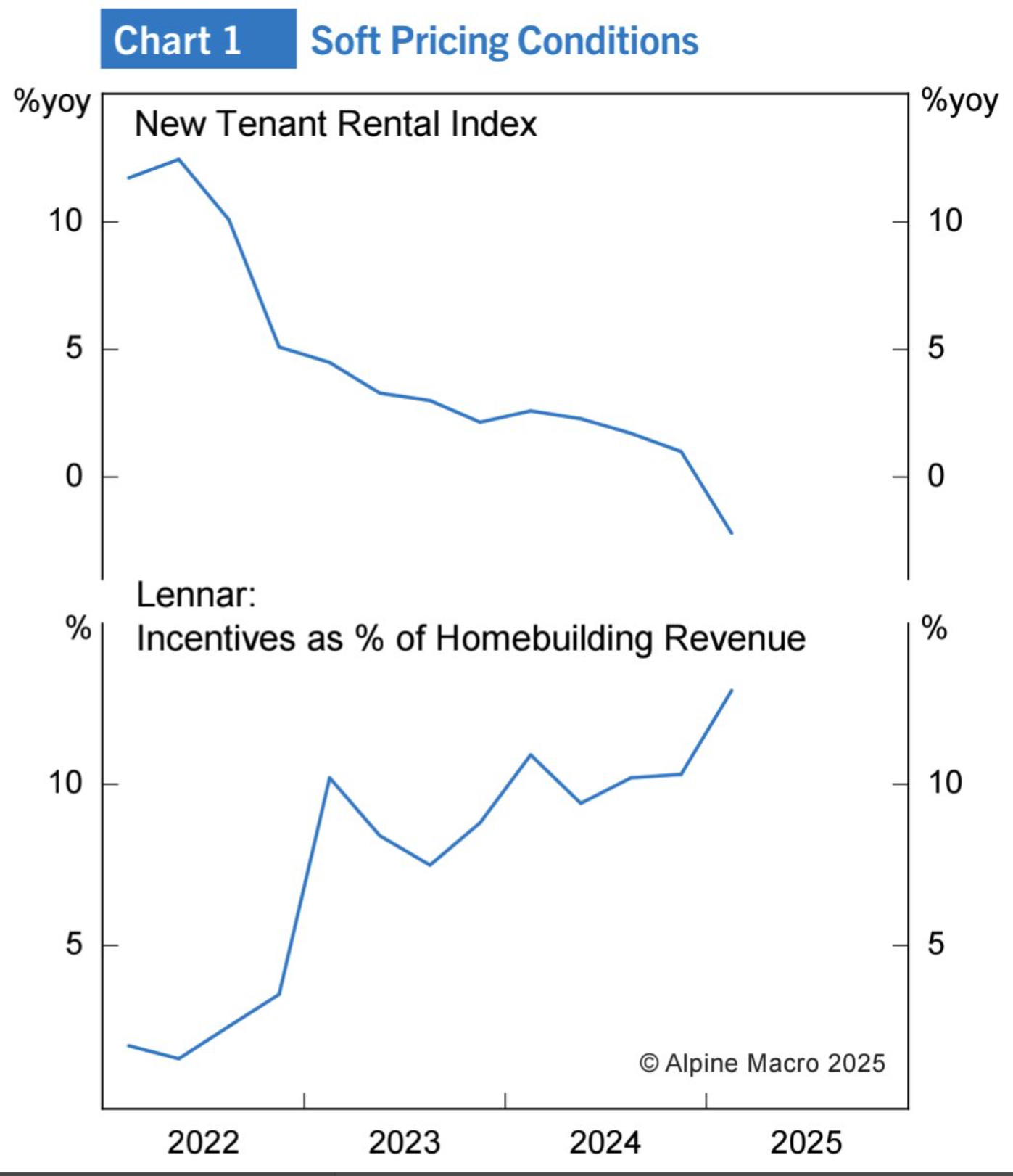

- Pending home sales were stronger, but under the surface, housing continues to slide

In the Commodity Space

- Gold sold off for a second straight week, despite steady central bank demand

- Oil dropped 13%—its worst weekly decline since March 2023

- Bitcoin surged, helped by a ruling that allows crypto to be used as collateral for U.S. mortgages via the FHFA

The Week Ahead: Big Thursday, Global Panels, and Critical Payroll Clues

A U.S. holiday-shortened week, but Thursday is absolutely stacked. Expect volatility.

Monday, June 30

- GER CPI Flash (June)

- CNY PMIs

- GBP Final Q1 GDP

- Fed speakers: Bostic, Goolsbee

Tuesday, July 1

- Powell, Lagarde, Bailey, Ueda share a panel at the ECB Forum in Lisbon

- ISM Manufacturing

- JOLTS Job Openings

- Atlanta GDPNow update

Wednesday, July 2

- ADP Employment

- Challenger Job Cuts

- Eurozone Unemployment

Thursday, July 3 (U.S. Early Close)

- Nonfarm Payrolls (NFP)

- ISM Services

- Jobless Claims

- U.S. Trade Balance

Friday, July 4 (Markets Closed)

- EZ PPI

- JPY Household Spending

- CHF Unemployment

Alpha Takeaway: Melt-Up Isn’t Mania—Yet

Risk assets are rallying, but we’re not yet in euphoric territory:

- Positioning remains cautious

- Liquidity is driving flows

- Technicals are bullish

- Geopolitical risks are priced in

- Fed credibility is being tested

Stay long into strength, but be ready to pivot if CPI or NFP surprises to the upside. Until then, the market wants to go higher.

Our Stance

- Stay long SPX, especially above 6100

- Use dips for entries in Gold & Crypto

- Watch EM and defensive rotation

- Do not fade this move—yet