Trump, Tariffs & Tactical Breadth: Rally Expands But CPI Could Reverse It

Markets delivered another strong week across major indices. S&P 500, Dow, and Russell 2000 all hit 3.5-month highs, with the Russell logging its best week since February. But behind the headlines, a wave of positioning flows, not macro fundamentals, powered the breakout. This week’s CPI, PPI, and trade talks will decide whether this is a true expansion or the last leg of the chase.

Market Overview: “Breadth Breaks Out, But Liquidity Still Drives”

The rally broadened meaningfully. Market internals show the best momentum across timeframes since March:

- 71.23% of SPX above 5-day MA

- 72.61% above 50-day

- 60.71% above 20-day

- 56.54% above 100-day

- 49.20% above 200-day

- 5-day highs outnumbered lows 4:1

VIX is sub-18, MOVE back below 100. The market is pricing in calm despite headline landmines on tariffs and inflation.

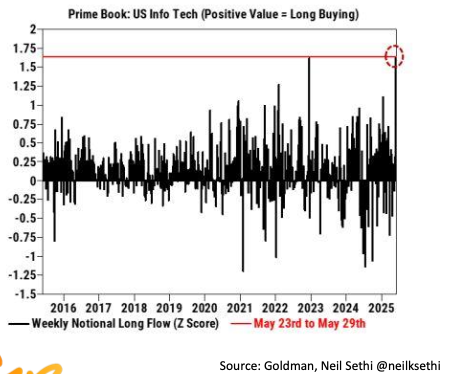

Flows are forcing the tape higher: CTAs are long, hedge funds returned midweek after fading the early rally, and mutual funds remain underweight.

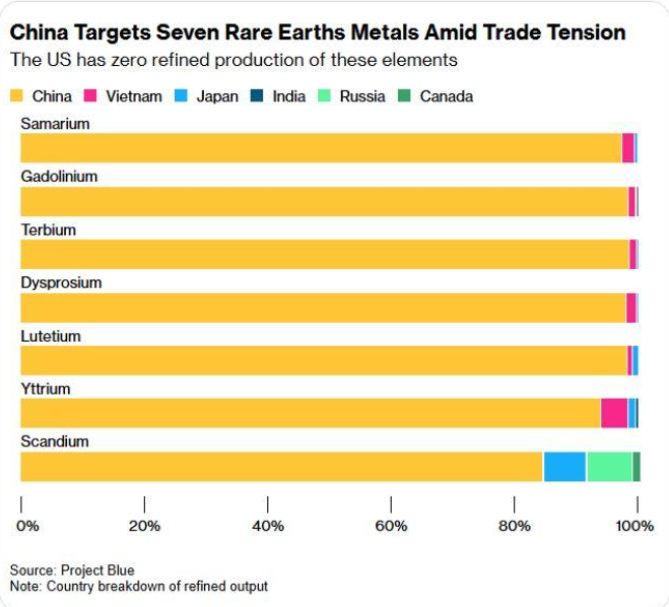

Rare earth optimism (China resumed shipments) and MAG7 rotation helped, but this is more about flow mechanics and sentiment reset than hard data.

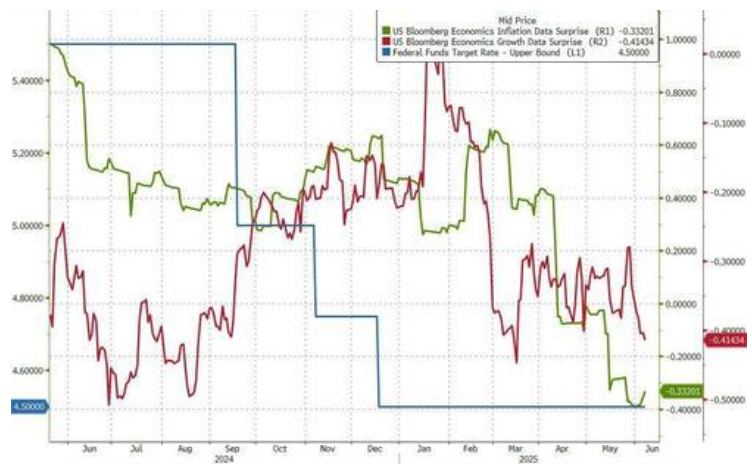

Macro & Policy Watch: “Cut Parade Continues, But Services Are Cracking”

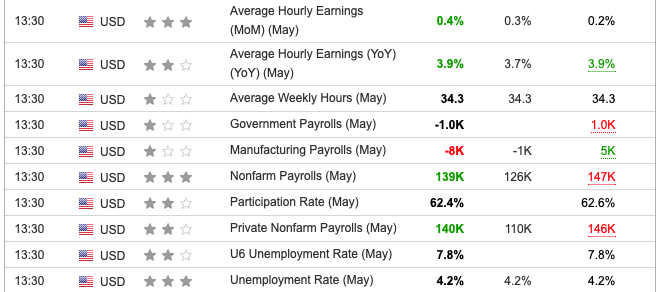

May’s Non-Farm Payrolls beat +13k with +139k print, but 95k revisions down and household employment collapsed –625k. Labour force participation dropped, and the unemployment rate held to 4.2% just on round down. It could have been much worse if those missing workers had signed on for claims. The Fed won’t love this divergence.

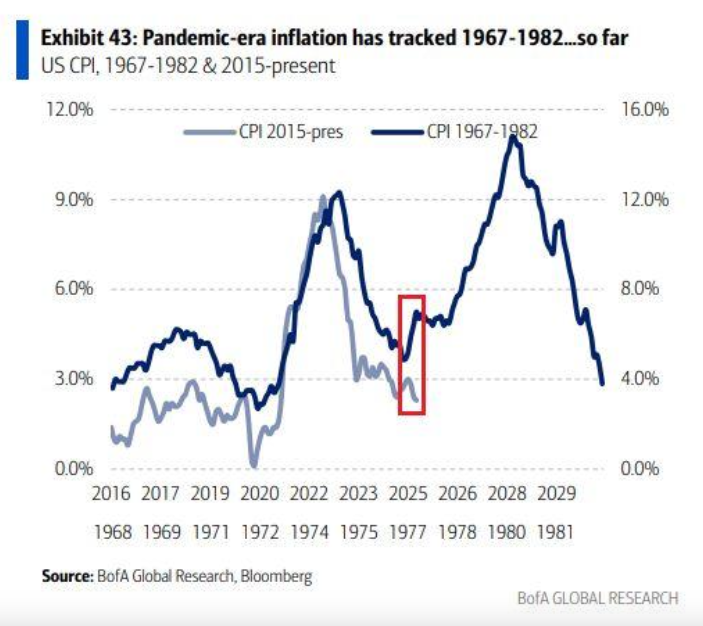

Services ISM slipped back below 50. New orders cratered. Prices paid spiked. This isn’t disinflation—it’s stagflation risk.

Central Banks Globally Are Easing

- The ECB cut 25bps

- Denmark followed

- China posted its fourth consecutive deflationary month

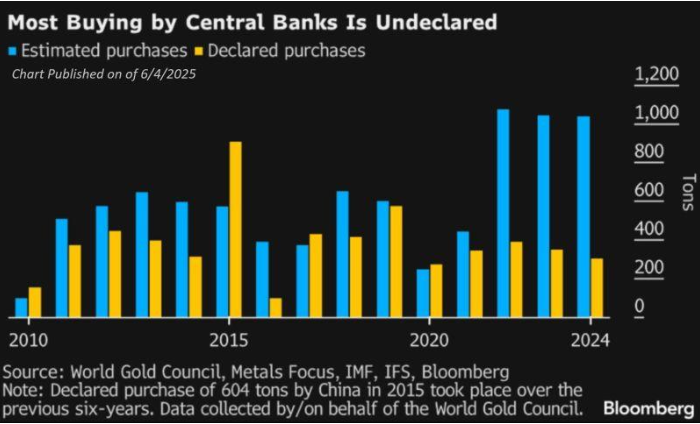

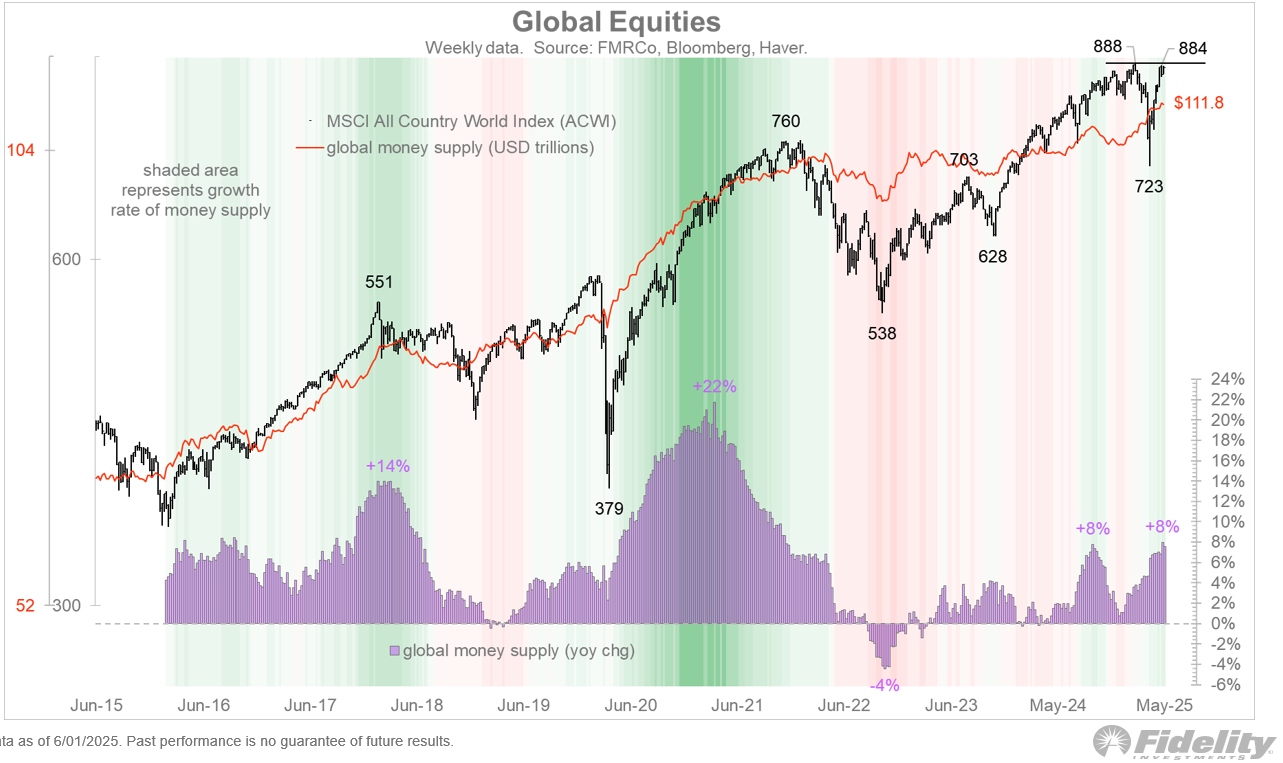

- Add stealth gold buying by EM CBs, and the case for global liquidity grows

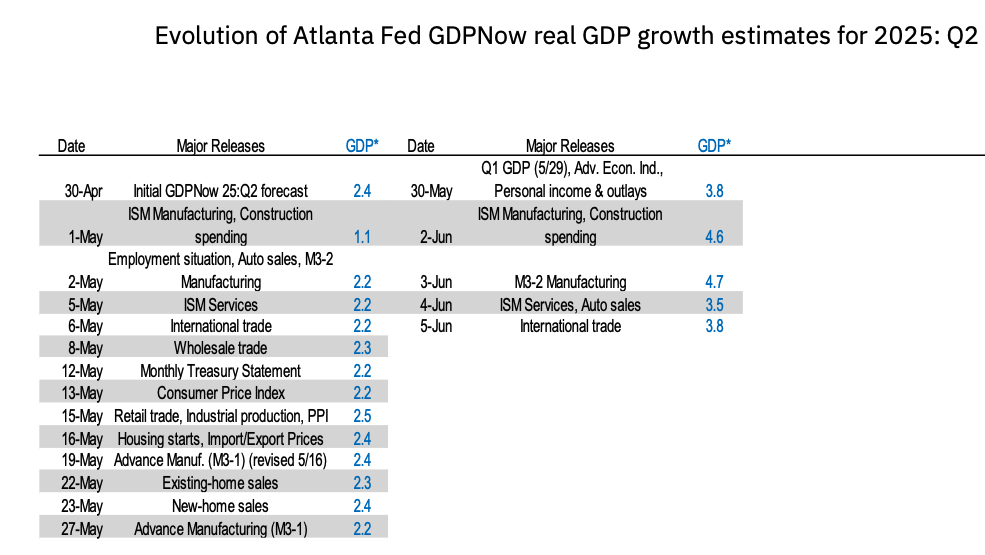

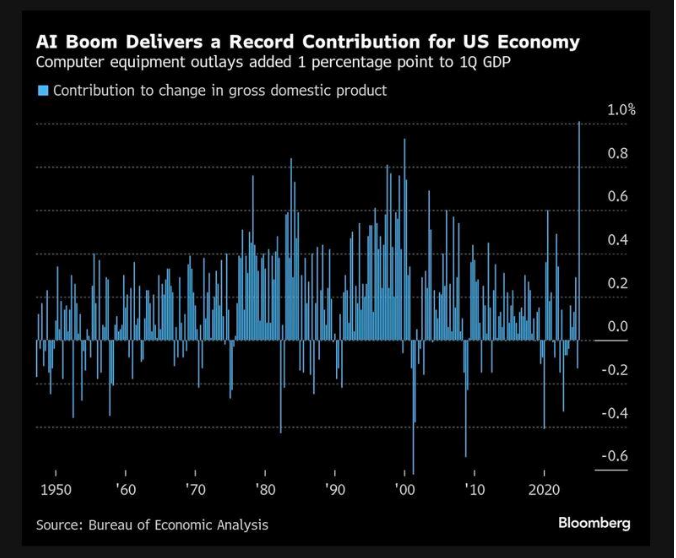

Also note: U.S. housing is decelerating—Household debt rose +$212B last quarter but Supply gapping above demand. GDPNow estimates for Q2 are now tracking +3.1%.

And Trump’s tariff poker isn’t over: capital controls are being floated again, and investors should be watching for Section 899 fallout for the dollar if foreign holdings see extra taxes. Trump is unruffled.

Technical & Sentiment Setups: “Breadth Is Real—and Still Flow-Fueled”

Internals suggest this breakout is for real rather than worries that April's was retail dip buying. Credit spreads tightened, SMID-caps outperformed, and new sector leadership emerged.

Gold

Gold’s breakout structure is intact. ETF inflows still suggest a record year, and undeclared accumulation continues beneath the surface. Silver is finally participating—watch the ratio shift…silver usually o/p in mature gold rallies.

Oil

Oil hit a 1.5-month high after bullish EIA/API surprises and China optimism. But weak demand, refinery margins, and inventories still cap upside.

Bitcoin & Positioning

Even BTC showed macro rotation signals last week as it tracked gold on weak-dollar themes and EM accumulation. Funny how mainstream it has become…

Sentiment is neutral, not euphoric. That’s an interesting middle ground. Positioning is no longer a tailwind but not yet a headwind either.

Last Week in Review: “Flows Up, Data Soft, Internals Strengthen”

- SPX, Dow, and Russell closed at 3.5-month highs

- Nasdaq gained +2%, Russell +3.19%

- MAG7 rotated, AI/chips rebounded

- China resumed rare earth shipments

- ISM Services <50, NFP mixed

- CTA flows stayed long, hedge funds turned buyers into Thursday

Gold was flat despite quiet accumulation. Oil up 3%. USD stable. MOVE drifted down. This wasn’t a “growth” week—it was a “liquidity plus positioning” week. Dips were bought by the pros this time.

Week Ahead: “CPI, PPI, Auctions, and Apple’s AI Reboot”

Each day this week holds critical macro risk but no Fed speakers (in lockdown):

Monday, June 9

- China trade talks resume in London

- Rare earth shipping deadline suggested to be positive result

- China in deflation and exports to US cratering

Tuesday, June 10

- NFIB Small Business Optimism

- 3Y Treasury Auction

- Trump expected remarks on tariffs/capital flows all week

- CPI front-run begins

Wednesday, June 11

CPI Report (First With Tariff Pass-Through)

- Core expected +0.3% MoM

- Headline YoY expected 2.5%

Additional events:

- 10Y Treasury Auction

- Apple WWDC25 continues 9th–13th, AI roadmap & chip integration

Thursday, June 12

- PPI Report

- 30Y Treasury Auction

- UK GDP

- ECB Schnabel & De Guindos speak

- Gold and silver could move if PPI low like in Europe

Friday, June 13

- Univ. of Michigan Sentiment

- 1Y / 5Y inflation expectations

- EZ Trade Balance may poke Trump

Alpha Takeaway: “Breakout Confirmed, But CPI Will Pick the Path”

Positioning has normalised, breadth is real, and volatility is subdued. But this market is still driven by liquidity and optimism, with some earnings strength but doubted macro strength. CPI and trade headlines will decide whether this is the real breakout or just a final squeeze.

Key Signals to Monitor

- SPX > 6000 = upside momentum

- CPI > 0.4% = bond selloff, risk-off

- Trade fails = semis and EM roll over

- Gold > $3,400 = reflation + policy pivot bets

We’re in a narrow volatility corridor—but one macro miss can break it. Stay nimble.