Energy Shock Intensifies, Markets Confront Stagflation Risks and Positioning Stress

Markets enter the third week of March navigating an environment where geopolitical developments and energy markets have begun to dominate macro sensitivities. Price action across assets reflects markets adjusting to sudden volatility in commodities and rising energy prices.

Beneath the surface, participation has become increasingly selective. Commodity volatility has surged from previously suppressed levels, while positioning across equities and macro assets suggests investors are reassessing risk exposure. The resulting price behaviour reflects markets reacting to the intersection of geopolitical developments, energy supply uncertainty, and renewed inflation sensitivity.

Market Overview: Energy Shock Meets Resilient Equity Structure

Equity markets have absorbed significant geopolitical developments without a complete breakdown in structure. Despite volatile headlines surrounding the conflict involving Iran and potential disruptions to energy supply routes, the S&P 500 has held relatively steady. This behaviour suggests markets are absorbing geopolitical developments without a broader deterioration in price structure.

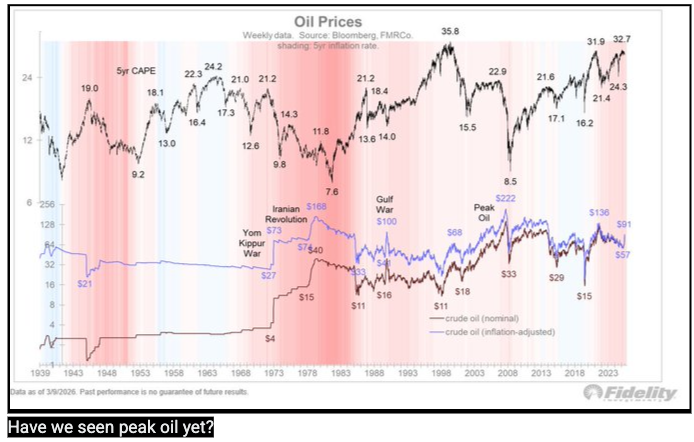

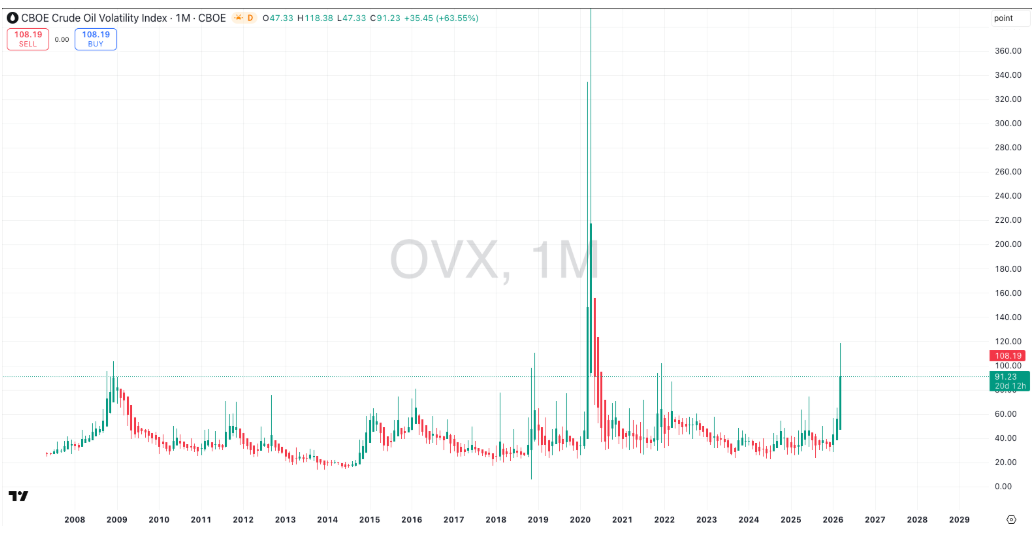

The dominant driver behind recent market behaviour has been the extreme volatility in energy markets. Oil prices experienced dramatic swings during the week, briefly approaching $120 per barrel before falling sharply below $80 and then stabilising near $95 as traders reassessed the likelihood and duration of supply disruption.

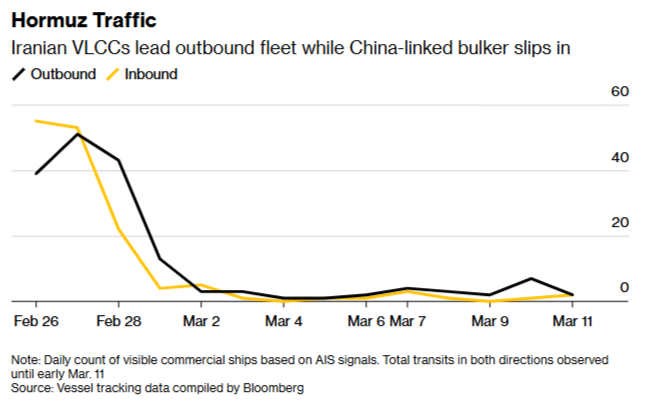

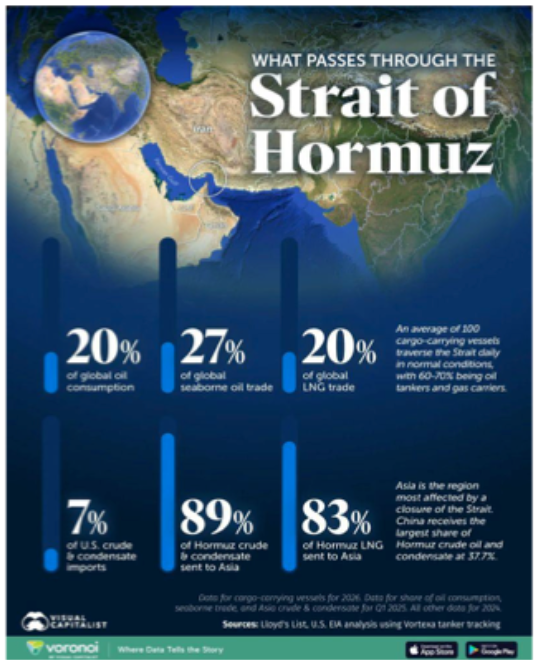

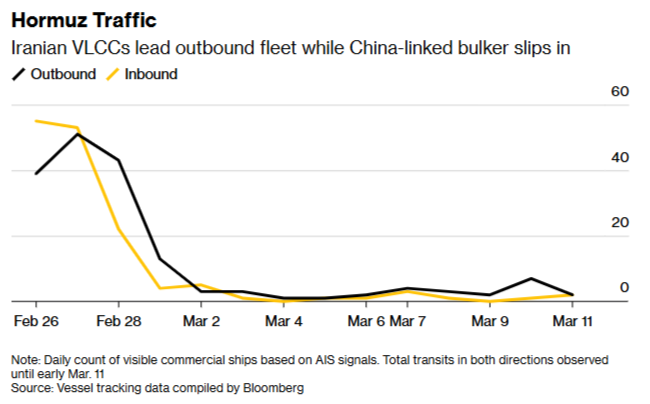

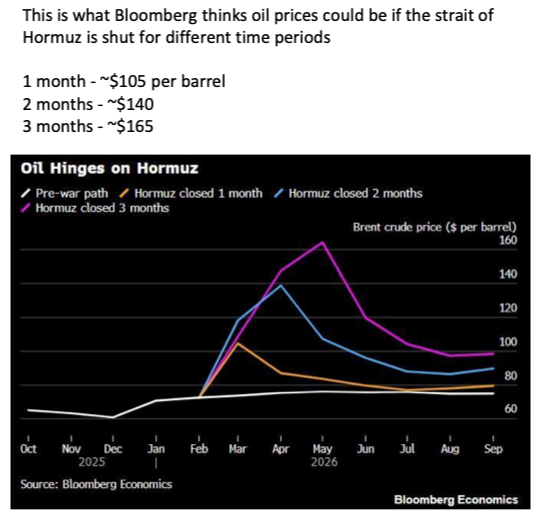

The sharp moves in crude followed escalating concerns around potential disruptions to shipping through the Strait of Hormuz, a critical global energy chokepoint through which a significant share of global oil supply transits.

These developments have increased the geopolitical risk premium embedded in energy markets and amplified macro sensitivity across asset classes.

Macro & Policy Watch: Energy Shock and Stagflation Concerns

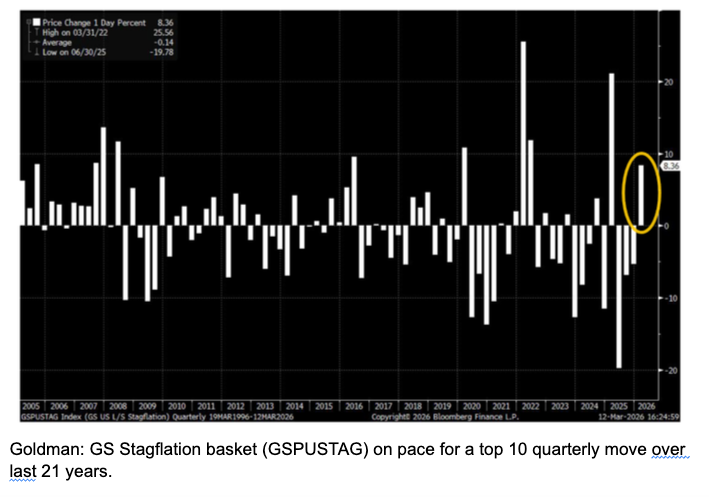

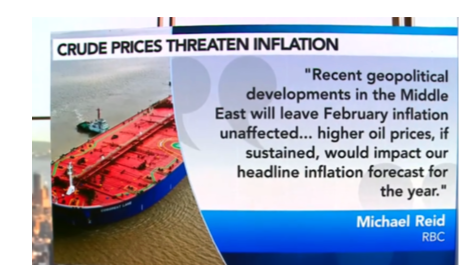

The current environment is defined by a central tension: an oil shock that simultaneously threatens economic growth while reigniting inflation pressures.

Rising energy prices tighten financial conditions and increase production costs across regions dependent on imported energy. At the same time, weaker growth signals have emerged in several major economies, raising concerns that the global economy could face a stagflationary combination of slowing growth and persistent price pressures.

The geopolitical developments surrounding Iran have also heightened concerns about the stability of global energy transport routes. Markets are closely monitoring activity around the Strait of Hormuz as an indicator of potential disruption to global oil flows.

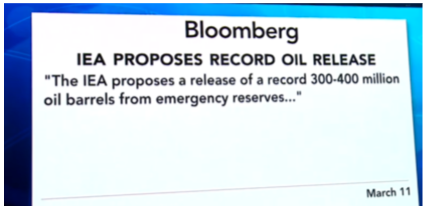

Discussions around coordinated strategic oil reserve releases have emerged, highlighting the scale of the potential supply shock and the effort to prevent disruptions from escalating into a broader energy crisis.

Even with these interventions, markets remain highly sensitive to developments surrounding energy supply and geopolitical tensions.

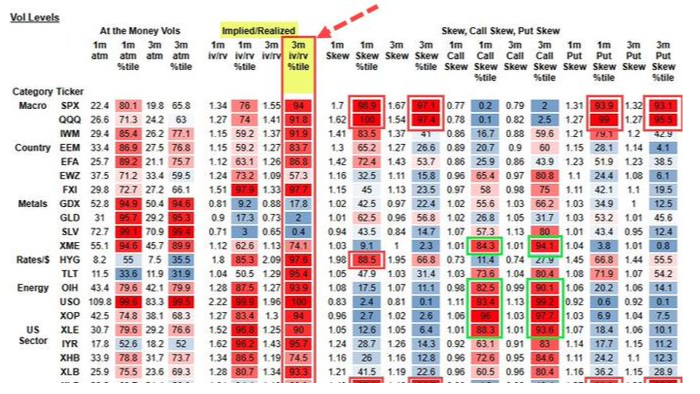

Technical & Sentiment Breakdown: Supportive, but Increasingly Fragile

While equity indices remain structurally supported, several indicators suggest the underlying environment may be becoming more fragile.

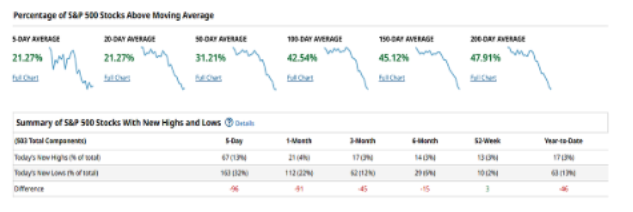

Market internals indicate participation has become increasingly selective. This type of structure often reflects cautious investor behaviour rather than broad conviction.

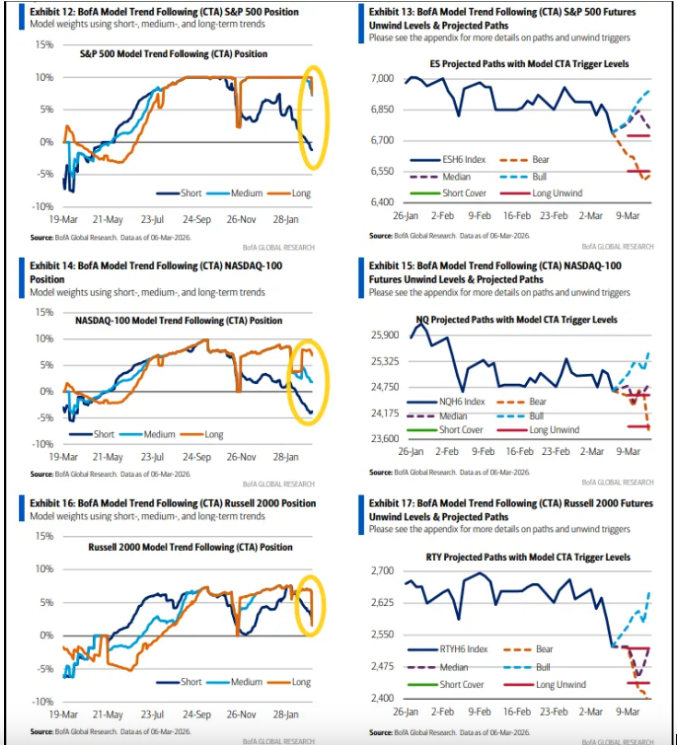

Positioning dynamics also suggest markets may be approaching an inflexion point. Systematic trading strategies such as CTAs appear to be nearing levels where trend shifts could trigger meaningful changes in flows.

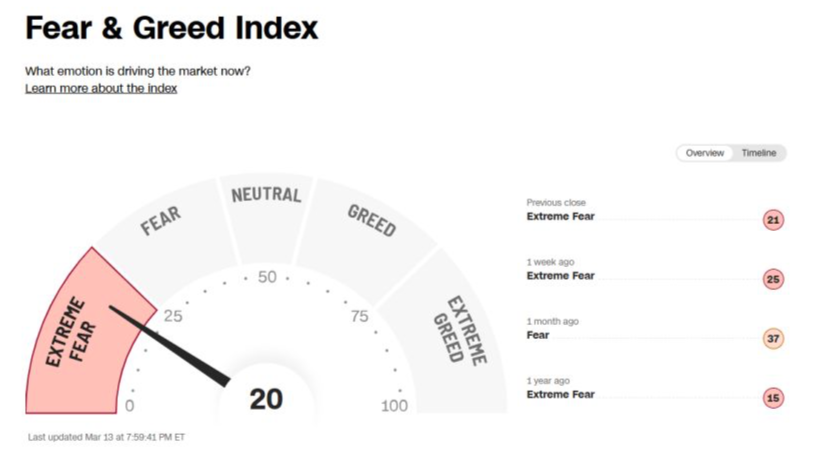

Sentiment indicators further reinforce the cautious tone. Measures of investor sentiment have moved into extreme fear territory, highlighting the degree of uncertainty surrounding geopolitical developments and energy markets.

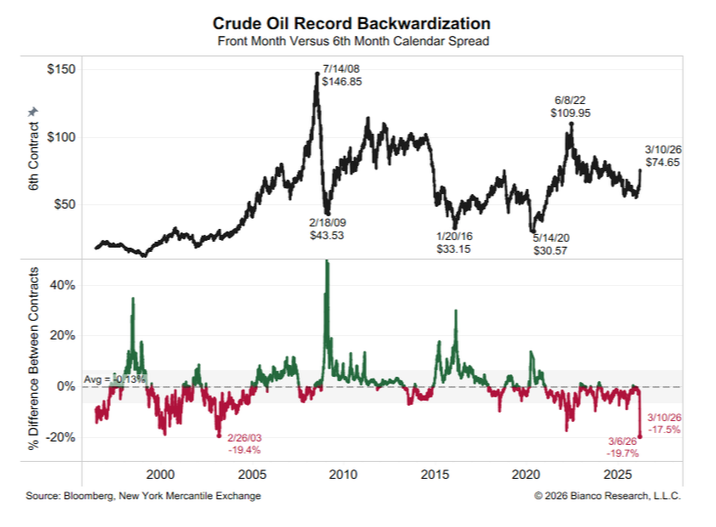

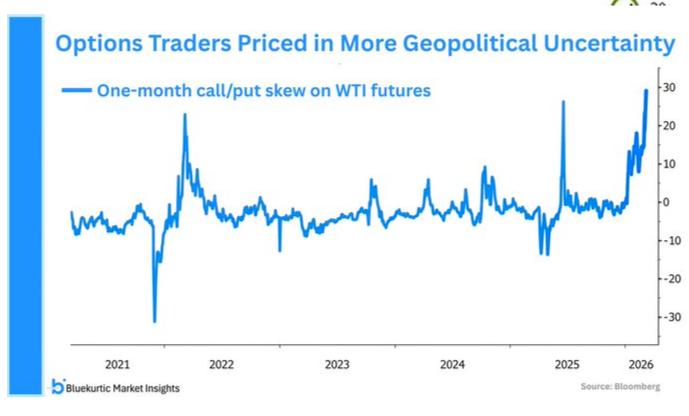

Commodity markets also display signs of structural stress. Oil futures have moved into pronounced backwardation, indicating tight near-term supply conditions relative to longer-dated expectations.

Options markets reinforce this signal. Even during temporary price declines, traders maintained demand for upside protection, suggesting persistent concern about further supply disruptions.

Last Week’s Recap: Energy Shock and Global Market Volatility

Recent market developments were dominated by geopolitical escalation and the resulting volatility in global energy markets. Rapid shifts in oil prices, geopolitical headlines, and macro data releases created heightened uncertainty across asset classes.

Key Highlights:

Macro:

Economic data delivered mixed signals regarding global growth momentum. Growth indicators softened, while inflation risks increased amid higher energy prices.

China:

Global investor participation continued to influence flows in several asset classes, reflecting the role of international positioning dynamics in shaping market behaviour.

Earnings:

Corporate developments remained secondary to geopolitical and energy market developments during the week.

Commodities:

Commodity markets became the focal point for global investors as geopolitical developments triggered extreme volatility across energy markets.

Crypto:

Digital asset markets experienced volatility alongside broader market movements during the week. Price action continued to evolve around key technical levels as market participants monitored positioning and supply dynamics.

Oil:

Crude markets remained the central driver of global market volatility as traders reacted to developments surrounding the Strait of Hormuz and potential disruptions to global supply.

The Week Ahead: Key Data and Market-Moving Signals

The week is centred on geopolitical developments and energy market sensitivity, with oil headlines and access through the Strait of Hormuz remaining a key focus. Markets will also navigate a dense calendar of central bank decisions, including the RBA, Federal Reserve, Bank of Canada, Bank of Japan, SNB, BoE and ECB. Key inflation signals will come from U.S. PPI, Canadian CPI and eurozone CPI, while housing activity, employment indicators and regional surveys may provide additional insight into economic momentum.

Monday, March 16

- China: Industrial Production, Retail Sales, Fixed Asset Investment, Unemployment Rate

- China: House Prices and Foreign Direct Investment

- Canada: CPI (MoM, YoY), Core CPI and Housing Starts

- US: Empire State Manufacturing Index

- US: Industrial Production and Manufacturing Production

- US: Capacity Utilisation Rate

- US: NAHB Housing Market Index

Tuesday, March 17

- Australia: RBA Interest Rate Decision and Policy Statement

- Eurozone: ZEW Economic Sentiment

- Germany: ZEW Current Conditions

- US: ADP Employment Change

- US: Pending Home Sales and Pending Home Sales Index

- US: API Weekly Crude Oil Stocks

- Japan: Trade Balance, Exports and Imports

- Eurozone: CPI (MoM, YoY) and Core CPI

- US: PPI (MoM, YoY) and Core PPI

- Canada: Bank of Canada Interest Rate Decision and Press Conference

- US: Federal Reserve Interest Rate Decision and Economic Projections

- US: Factory Orders

- US: Crude Oil Inventorie

- Brazil: Interest Rate Decision

- New Zealand: GDP

Thursday, March 19

- Australia: Employment Change and Unemployment Rate

- Japan: Bank of Japan Interest Rate Decision

- Switzerland: SNB Interest Rate Decision

- UK: Bank of England Interest Rate Decision

- Eurozone: ECB Interest Rate Decision

- US: Initial Jobless Claims

- US: Philadelphia Fed Manufacturing Survey

- US: Building Permits and New Home Sales

- China: Loan Prime Rate

- Russia: Interest Rate Decision

- Germany: PPI

- Eurozone: Trade Balance and Current Account

- Canada: Retail Sales

- Canada: IPPI and RMPI

- UK: CBI Industrial Trends Orders

- Spain: Consumer Confidence

Alpha Takeaway: Energy Volatility Shapes Market Psychology

Energy markets have become a central influence on current market behaviour, introducing renewed sensitivity around inflation, policy expectations, and geopolitical developments.

Equities:

Equity indices remain structurally resilient despite geopolitical escalation. However, narrowing participation and positioning stress suggest that developments in energy markets may continue to influence short-term market direction. There are signs of extreme underweights, shorts in financials and extreme downside protection levels in futures and options going into expiry week

Gold & Silver:

Precious metals have not yet displayed strong safe-haven behaviour during the current geopolitical episode, reflecting the influence of currency movements and interest rate expectations.

Crypto:

Digital assets continue to trade alongside broader risk sentiment and liquidity dynamics rather than functioning as defensive assets during periods of geopolitical stress. Could be some relative switching from gold.

Macro:

Energy markets remain the central variable shaping global macro conditions. Oil volatility, geopolitical risk surrounding transport routes, and policy responses will likely continue influencing inflation expectations and broader market behaviour. Lots of heavy upside speculation in options influencing here.

The current environment reflects a market adjusting to new macro drivers rather than experiencing structural deterioration. Positioning dynamics and geopolitical developments may continue to generate episodic volatility as markets navigate an uncertain energy landscape.