Geopolitical Shock Absorbed, Positioning Stress and Inflation Undercurrents Shape the Tape

Markets move into early March, navigating an environment where geopolitical escalation was anticipated but still capable of unsettling positioning. The response across assets reflects adjustment rather than disorder, with flows shifting toward safety before stabilising — highlighting a system that remains liquid even as uncertainty rises.

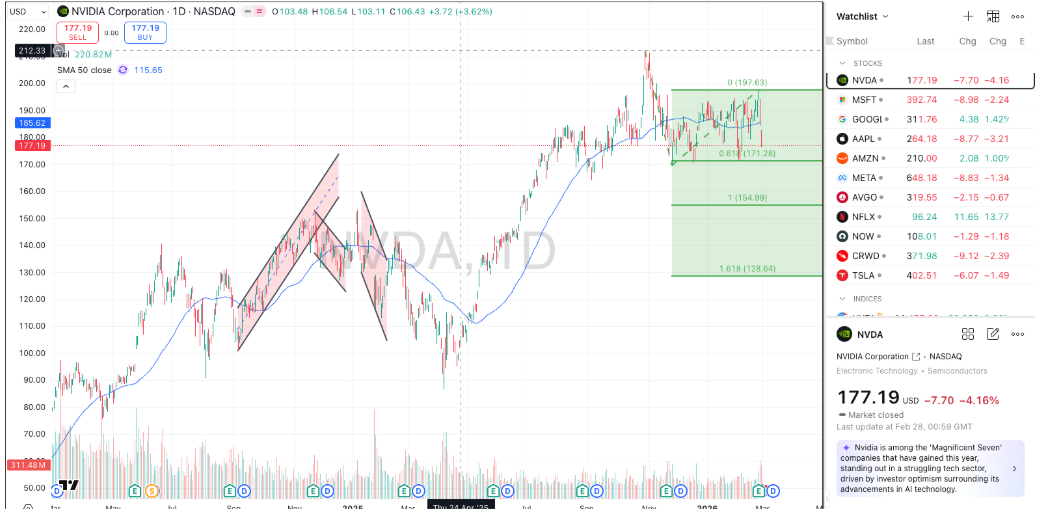

Beneath the surface, participation appears increasingly selective. Bonds briefly reclaimed their haven role, while liquid technology names absorbed selling pressure despite strong operational performance. The resulting price action suggests that stress is rotating through positioning rather than undermining the broader structure.

Market Overview: Anticipation Absorbed, Structure Intact

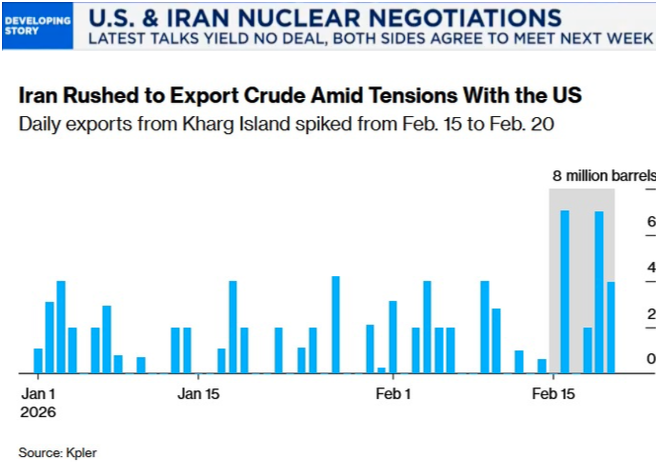

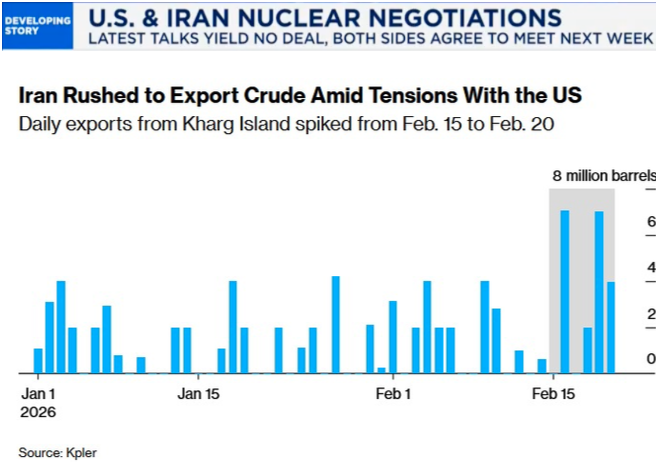

Equity markets continue to absorb geopolitical developments without losing structural footing. Oil and gas markets had already been trending higher ahead of escalation, reinforcing that current moves represent amplification of an existing trajectory rather than a new shock.

Risk-off behaviour was evident but limited in duration. Digital assets sold off before recovering, and sovereign bonds reasserted their haven role after yields briefly crossed key thresholds. This behaviour underscores a market pricing downside, but not expecting prolonged disruption.

Equities also reflected positioning dynamics. Despite strong operational performance, highly liquid names such as NVIDIA experienced declines, suggesting that de-risking flows were expressed through liquid assets rather than broad selling pressure.

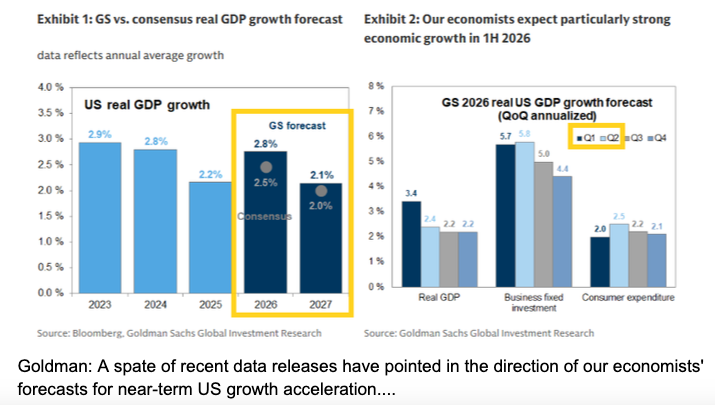

Forward expectations remain supported by investment and consumption trends, with projections suggesting growth that exceeds consensus assumptions for the year ahead.

Macro & Policy Watch: Inflation Pressure Meets Liquidity Expansion

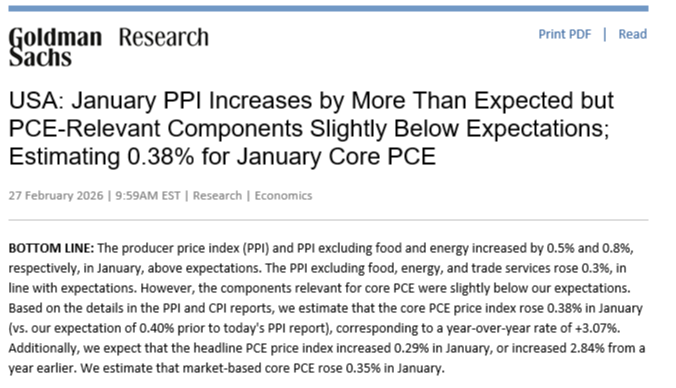

Producer price data surprised to the upside, introducing short-term margin pressure and reinforcing sensitivity to cost trends.

The data were service-heavy and do not yet materially alter inflation trajectories, but they highlight potential pressure on profit margins until clarity emerges regarding whether recent strength reflects a temporary print or a sustained shift.

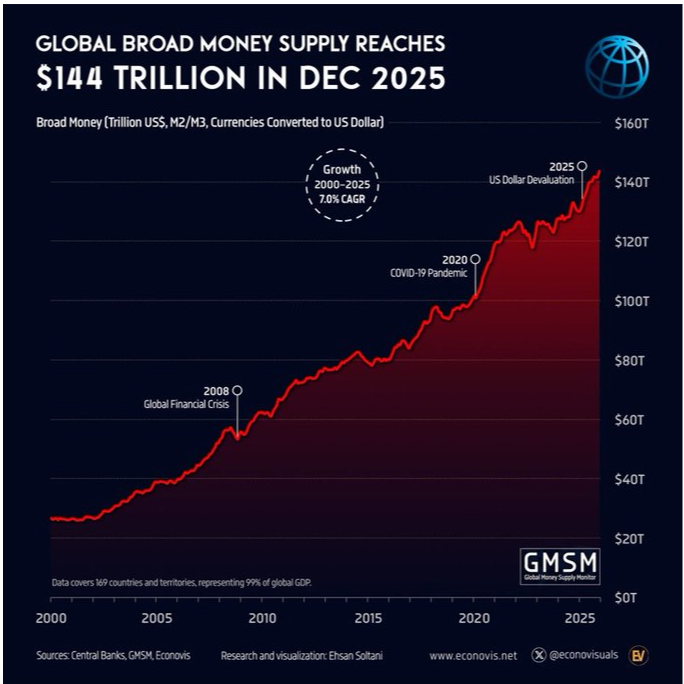

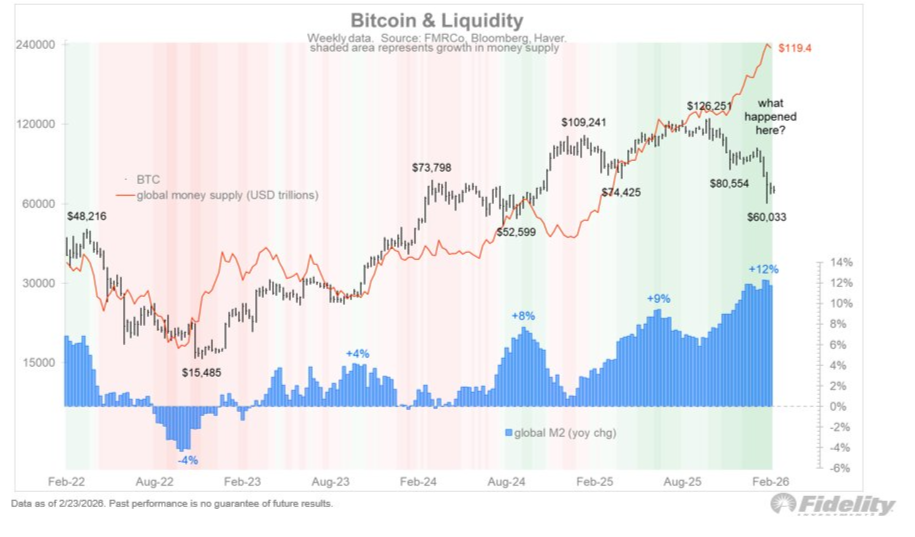

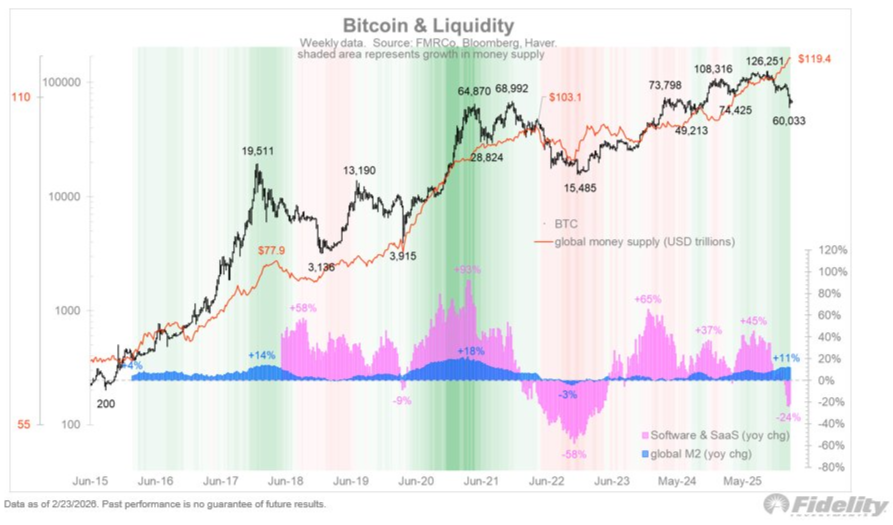

Global money supply continues to reach new highs — a dynamic historically supportive of gold and risk assets alike.

Bond markets reflected ongoing debate between safety demand and inflation persistence. Yields briefly moved through key levels before renewed demand suggested continued appetite for sovereign assets.

Energy remains a key variable. Increased freight costs and delivery risks introduce potential volatility even in the absence of structural supply disruption.

Technical & Sentiment Breakdown: Stable Structure, But Increasingly Flow-Driven

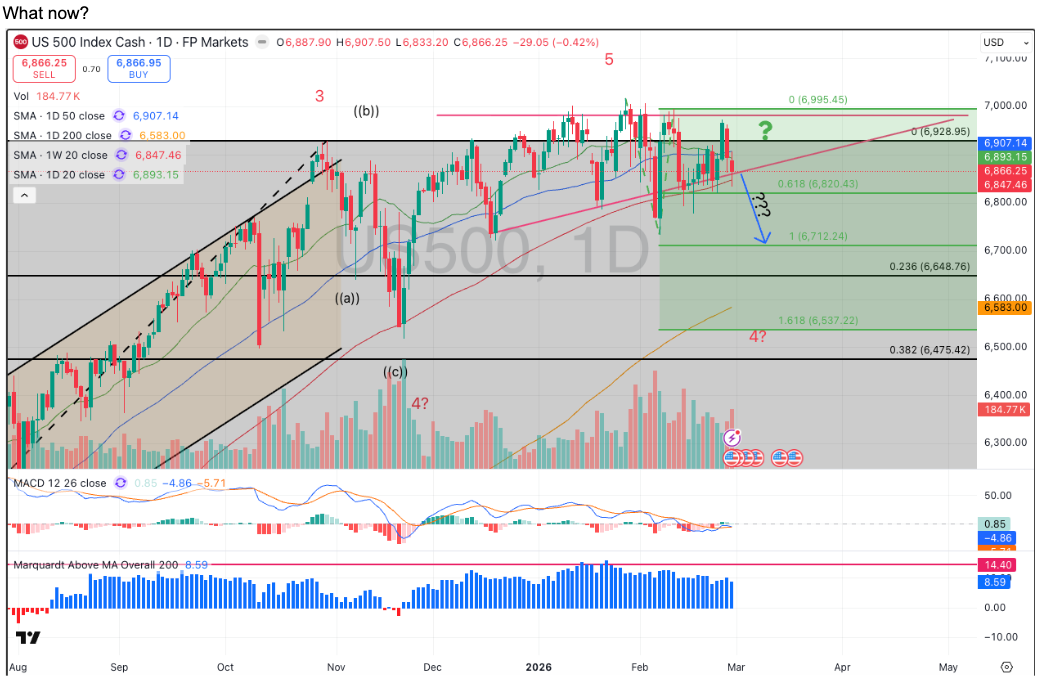

Market structure remains broadly intact, though recent behaviour suggests momentum is being shaped more by positioning than by changes in underlying growth expectations.

The sharp reaction in highly liquid technology names despite strong operational performance highlights the role of risk management flows. The selloff in NVIDIA following strong results suggests that liquid names are being used as vehicles for de-risking rather than reflecting fundamental reassessment.

This weakness occurred even as broader indices held relatively stable, indicating that risk-off expression has been concentrated in the most tradable exposures rather than across the market.

Sideways movement across indices appears to reflect both geopolitical anticipation and rotation toward defensive positioning rather than a collapse in conviction.

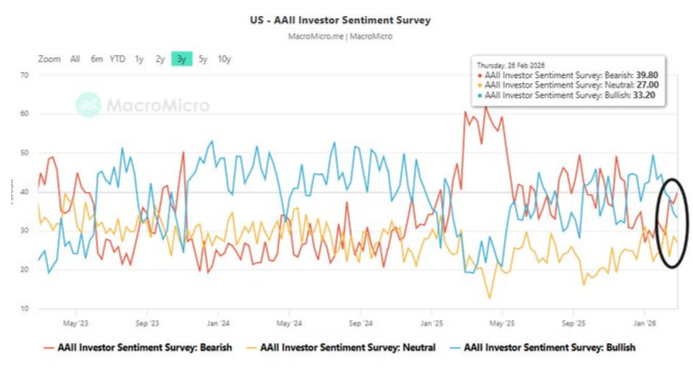

Sentiment indicators have now crossed into bearish territory.

At the same time, positioning skew shows an increased focus on downside protection, with put demand elevated relative to calls.

This shift toward defensive positioning reflects a market more concerned with downside outcomes than upside opportunity, increasing the likelihood that short-term volatility may be driven by positioning dynamics rather than macro deterioration.

Last Week’s Recap: Inflation Signals and Labour Dynamics

Recent developments reflected the coexistence of rising cost pressures and continued labour resilience, reinforcing a backdrop where growth remains intact even as profitability dynamics face short-term pressure.

Key Highlights:

Macro:

Producer prices exceeded expectations, creating short-term margin pressure while leaving broader inflation expectations largely intact. The strength was driven primarily by services, suggesting a temporary squeeze on profitability rather than a shift in long-term pricing trends.

Earnings:

Strong performance from major technology firms was met with hesitation in price action, reflecting positioning adjustments rather than earnings-driven reassessment. Selling in liquid names appeared to reflect risk management flows rather than a reassessment of long-term growth narratives.

Commodities:

Global liquidity expansion continued to support real assets, with money supply reaching new highs and reinforcing a constructive backdrop. Geopolitical developments contributed to increased sensitivity across resource markets.

Crypto:

Digital assets behaved in line with broader risk sentiment rather than acting as defensive instruments, highlighting their continued linkage to liquidity conditions. Positioning remained influenced by technology sector flows and broader software risk sentiment.

Oil:

Energy markets responded to developments that had been partially anticipated, with price dynamics reflecting both supply expectations and transport-related risk. Freight risk and delivery premiums added another layer of sensitivity to pricing behaviour.

The Week Ahead: Key Data and Market-Moving Signals

The week is centred on labour market strength and activity data, with ISM releases and Non-Farm Payrolls acting as the primary macro signals. At the same time, markets will continue to assess the duration of the ongoing conflict, given its influence on oil sensitivity and broader risk positioning.

Monday, March 2

Australia: MI Inflation Gauge, Company Profits, Business Inventories

Japan: Manufacturing PMI

India: Manufacturing PMI

Germany: Retail Sales

Eurozone: Manufacturing PMI

UK: Manufacturing PMI, Mortgage Lending and Credit Data

US: ISM Manufacturing PMI and Employment Components

US: Atlanta Fed GDPNow Update

Japan: Unemployment Rate and Capital Spending

Tuesday, March 3

UK: BRC Shop Price Index

Australia: Current Account and Building Approvals

Eurozone: : CPI and Core CPI

US: Economic Optimism Index

US: API Weekly Crude Oil Stocks

Wednesday, March 4

Australia: GDP

China: Manufacturing and Services PMI

India: Services PMI

Eurozone: : Services PMI

US: ADP Nonfarm Employment

US: ISM Non-Manufacturing PMI

US: Crude Oil Inventories

US: Beige Book

Thursday, March 5

Australia: Trade Balance

Eurozone: Construction PMI

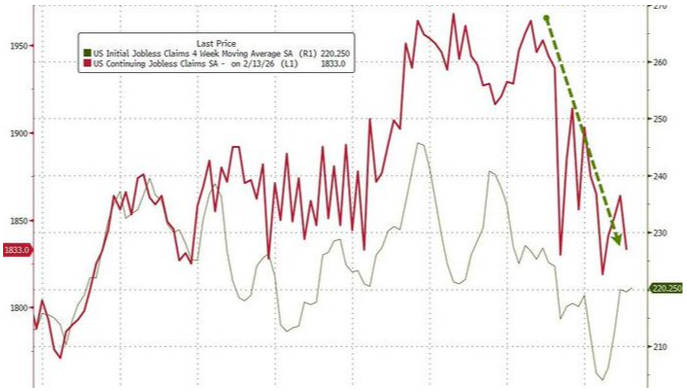

US: Jobless Claims

US: Trade Balance

US: Unit Labour Costs

US: Factory Orders

Friday, March 6

Eurozone: GDP

US: Retail Sales

US: Non-Farm Payrolls

US: Unemployment Rate

US: Average Hourly Earnings

Alpha Takeaway: Adjustment Within an Intact Framework

Markets continue to navigate evolving pressures without abandoning the broader growth narrative, with positioning shifts shaping near-term behaviour more than structural change.

Equities:

Rotation remains active, with liquid technology names absorbing positioning adjustments even as underlying performance remains strong. Recent selling appears linked to de-risking flows rather than a reassessment of long-term growth drivers.

Gold & Silver:

Liquidity expansion continues to provide structural support amid uncertainty, reinforcing their role as beneficiaries of global money supply trends.

Crypto:

Behaviour remains aligned with broader risk sentiment rather than functioning as a defensive asset, with price action continuing to track shifts in technology sector sentiment.

Macro:

Cost pressures and labour resilience are shaping expectations, reinforcing the importance of monitoring inflation trends and employment signals as growth remains broadly supported.

Markets appear to be transitioning from complacency toward caution rather than toward contraction. Liquidity remains a stabilising force, even as positioning dynamics introduce episodic volatility.