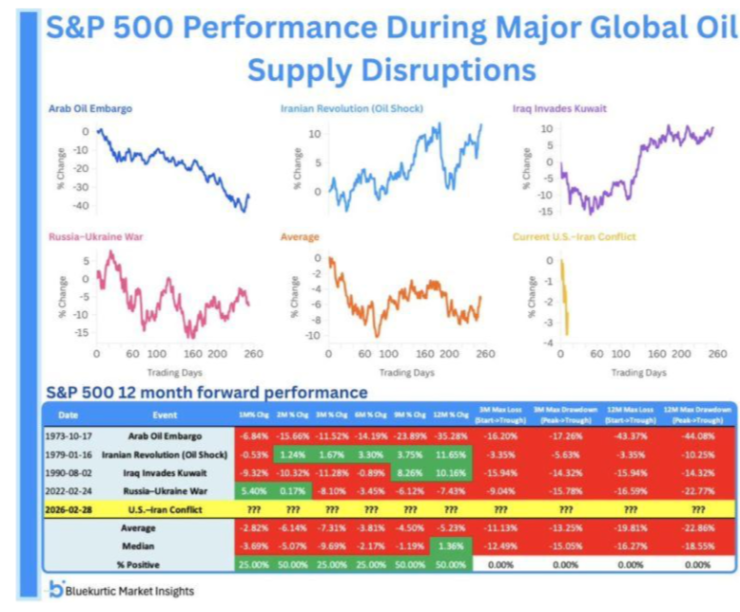

Supply Shock Dominates, Policy Tightening Persists

Markets are navigating a fragile balance between geopolitical uncertainty and policy rigidity, with price action reflecting hesitation rather than conviction. Early optimism around a contained outcome has faded, replaced by a more cautious tone as the week progressed. Liquidity conditions are tightening beneath the surface. Participation remains selective, with flows gravitating toward energy and defensive positioning, while broader risk assets struggle to maintain stability.

The underlying message is clear: stress is mounting, even if it has not yet fully expressed itself. There is also a noticeable divergence between how markets are positioned and what the macro backdrop is implying. While price action has not fully broken down, the underlying tone suggests confidence is thinning, particularly as headline-driven volatility continues to dominate.

Market Overview: Oil Shock Driving Cross-Asset Behaviour

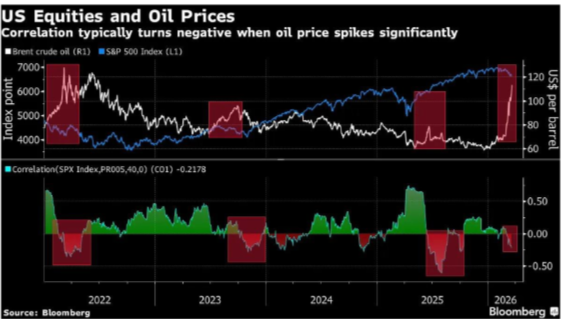

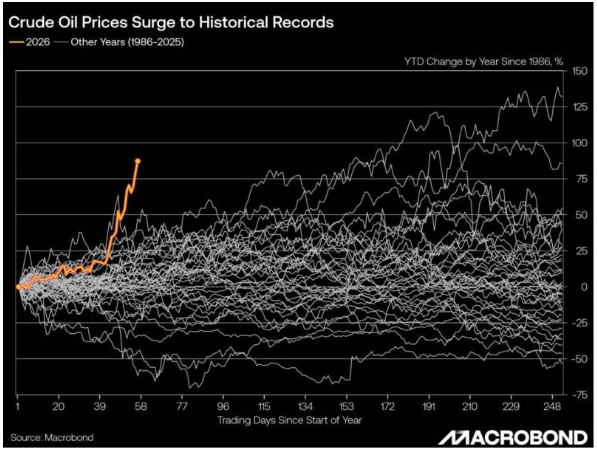

The dominant force across markets is the energy supply shock, which is now dictating cross-asset performance more than traditional macro inputs.

The current environment reflects a supply-driven disruption rather than a demand cycle. Oil markets remain tight, with physical constraints limiting the ability for supply to respond quickly. This has shifted the macro backdrop toward inflation persistence alongside slowing growth expectations, reinforcing stagflation concerns.

Equities are reacting accordingly. Historically, oil shocks have created headwinds for equity markets, and recent price action suggests that dynamic is re-emerging. Index performance reflects a lack of conviction, with rallies struggling to hold and downside pressure building.

Flows continue to show a divergence between positioning and reality. While there is still some expectation of stabilisation, price action suggests markets may need further adjustment to align with the evolving macro conditions. The inability of equities to decisively rebound highlights fragile participation rather than strong demand.

Macro & Policy Watch: Hawkish Policy Meets Supply Constraints

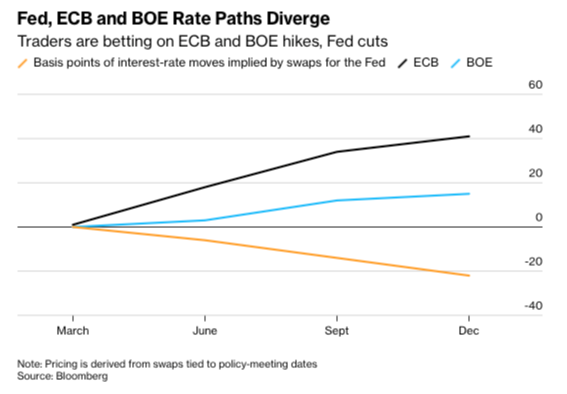

Central banks remain focused on inflation, even as the source of that inflation shifts toward supply-side pressures. The policy framework is still anchored in demand control, while the underlying issue is increasingly driven by constrained supply dynamics. This creates a mismatch between policy tools and the actual source of inflation, adding complexity to the macro environment.

Rate expectations have adjusted quickly, with markets now pricing tighter policy conditions across major economies. This shift comes despite growing concerns around growth and demand, highlighting a disconnect between policy direction and economic sensitivity.

The policy response is creating a challenging environment. Tightening financial conditions into a supply shock raises the risk of demand destruction rather than resolution, particularly as energy costs continue to rise and weigh on consumption.

At the same time, geopolitical developments remain unresolved. The lack of a clear de-escalation path keeps uncertainty elevated, reinforcing the sensitivity of markets to headline risk and energy price fluctuations. This uncertainty continues to limit conviction across asset classes.

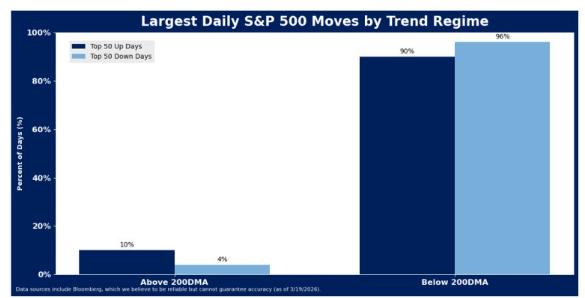

Technical & Sentiment Breakdown: Supportive, but Increasingly Fragile

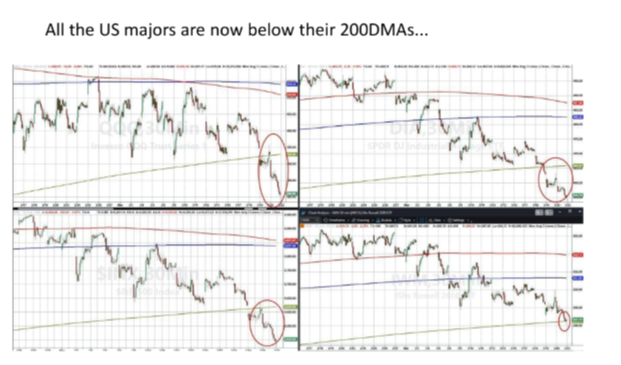

Market structure is holding, but momentum is clearly deteriorating. Price action continues to respect key levels, but the quality of moves is weakening, with less follow-through on rallies and quicker reactions to downside catalysts. This shift often signals a transitional phase rather than a stable trend.

Key indices have moved toward or below critical technical levels, suggesting a transition from trend stability to a more fragile regime. This typically results in larger and less predictable moves, particularly as liquidity conditions tighten.

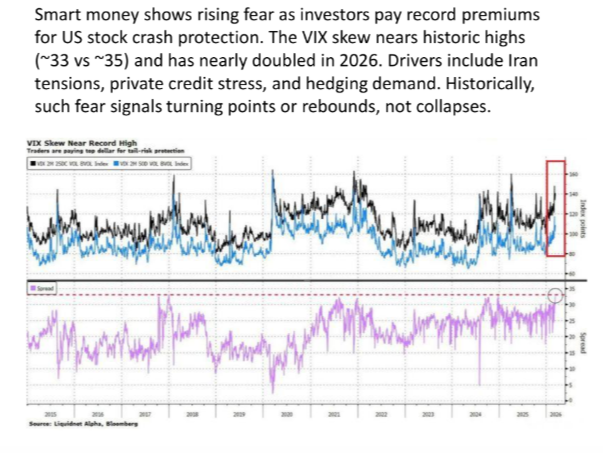

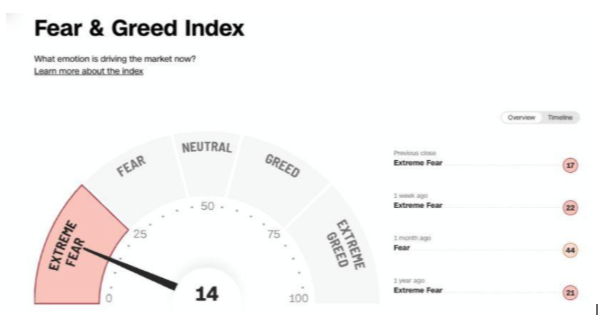

Sentiment reflects growing caution. While not fully capitulative, positioning indicates increasing defensiveness, with hedging activity picking up and investors becoming more reactive to short-term developments.

At the same time, consensus appears to be forming around downside risks. This creates the potential for sharp counter-moves, particularly if positioning becomes too one-sided. The presence of fear without full capitulation suggests that volatility will likely remain elevated.

Last Week’s Recap: Energy Shock and Policy Tension

The week was defined by a shift from cautious optimism to a more defensive posture amid intensifying macro pressures. Markets were increasingly driven by energy dynamics and policy expectations rather than traditional growth signals.

Key Highlights:

Macro:

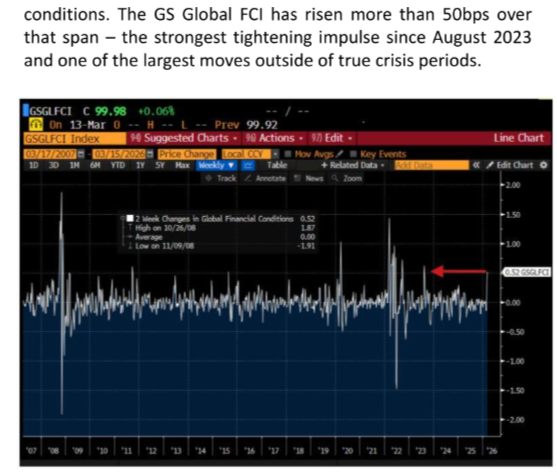

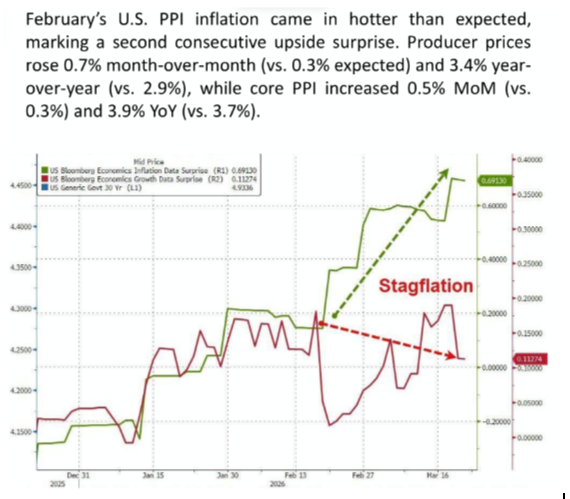

Inflation concerns remained elevated, with producer prices surprising to the upside and reinforcing the risk of persistent inflation. Financial conditions tightened meaningfully, adding pressure to growth expectations and increasing sensitivity to further shocks.

China:

Growth concerns continue to linger, with global demand expectations adjusting lower alongside broader macro uncertainty. This adds another layer of fragility, particularly as external demand becomes less reliable.

Earnings:

Corporate developments remained secondary to macro forces, with market focus firmly on energy and policy dynamics. Earnings reactions were muted relative to the broader macro-driven moves.

Commodities:

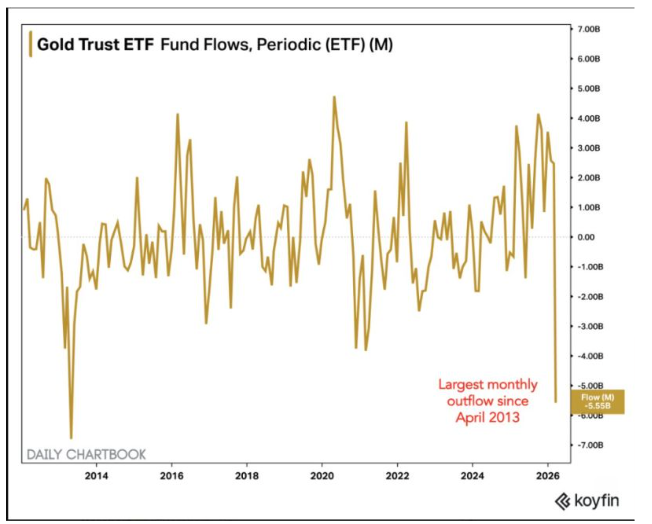

Energy markets surged, driven by supply constraints and geopolitical risks. In contrast, precious metals faced pressure despite their traditional safe-haven role, influenced by rate expectations and ongoing outflows.

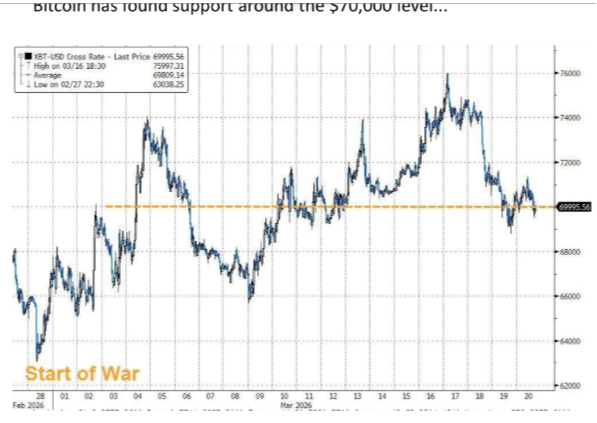

Crypto:

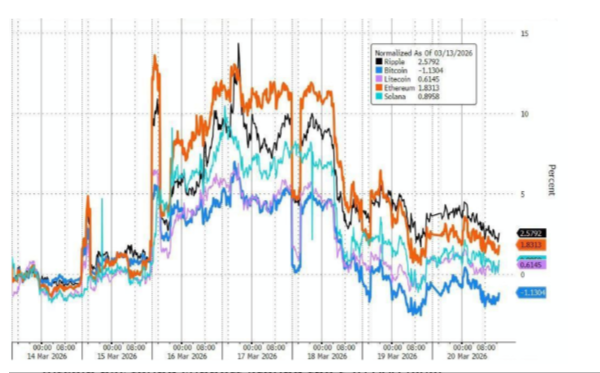

Crypto markets showed relative stability, with price action consolidating rather than breaking down despite broader risk-off sentiment. This suggests a degree of resilience, although direction remains unclear.

Oil:

Oil remained the central driver, with prices elevated and volatility driven by geopolitical developments and supply disruptions. The market continues to respond quickly to any changes in the geopolitical narrative.

The Week Ahead: Key Data and Market-Moving Signals

The calendar is relatively light, but the focus remains firmly on inflation signals and early indications of whether the energy shock is feeding through into broader data. Preliminary PMIs across major economies will provide insight into growth momentum, while CPI and PPI releases from Australia, Japan, and the UK will be watched for any early transmission effects. By the end of the week, consumer sentiment and inflation expectations data will be key in assessing how deeply current conditions are impacting demand.

Monday, March 23

- China: M3 money supply

- Spain: Trade balance

- US: Chicago Fed national activity index

- US: Construction spending

- Eurozone: Consumer confidence

- US: Atlanta Fed GDPNow

- Australia: Manufacturing & Services PMI

- Japan: CPI data (YoY & MoM)

- Auctions: France T-bill auctions, US 3-month & 6-month bill auctions

- Central bank speakers: ECB, Bundesbank, BoJ reports.

Tuesday, March 24

- Japan: PMI data (manufacturing, services, composite)

- India: Manufacturing & services PMI

- France, Germany, Eurozone, UK: PMI releases

- US: Unit labour costs & productivity

- US: S&P Global PMI data

- US: Richmond Fed indices

- US: Money supply data

- US: API crude oil inventories

- Auctions: Germany, UK, US 2-year note auction

- Central bank speakers: ECB, Fed, SNB, BoJ

Wednesday, March 25

- Australia: CPI (QoQ, YoY, and trimmed measures)

- UK: CPI, PPI, and RPI releases

- Germany: Ifo business climate and expectations

- Eurozone: ECB President Lagarde speaks

- US: Mortgage applications and housing indicators

- US: Import/export price indices

- US: Crude oil inventories and energy data

- Auctions: US 5-year note auction

- Central bank speakers: ECB, Fed, BoE, RBA

Thursday, March 26

- Japan: Core CPI and leading indicators

- Germany & France: Consumer and business confidence

- Spain: GDP data

- Eurozone: Money supply and credit data

- US: Initial and continuing jobless claims

- US: Kansas City Fed indices

- US: Fed balance sheet and liquidity data

- Auctions: US 7-year note auction

- Central bank speakers: Fed, ECB, BoE, BoC

Friday, March 27

- UK: Retail sales and consumer confidence

- Spain: CPI and inflation data

- Eurozone: ECOFIN meetings

- US: Michigan consumer sentiment and inflation expectations

- US: Wholesale inventories

- Canada: Budget balance

- Central bank speakers: Fed and ECB officials

Alpha Takeaway: Fragility Beneath Stability

Markets are balancing between structural support and growing macro pressure, with price action reflecting hesitation rather than resolution. The current environment is defined more by uncertainty than direction, with multiple forces pulling in different directions.

Equities:

Equities remain sensitive to energy-driven inflation and tightening financial conditions, with downside risks increasing as macro pressures build. Price action suggests limited tolerance for negative surprises.

Gold & Silver:

Precious metals are facing conflicting forces, with safe-haven demand offset by rising rate expectations and outflows. This has led to a consolidation of previous gains. Is it re-entry time yet?

Crypto:

Crypto continues to consolidate, showing relative resilience but lacking a clear directional catalyst. Stability here contrasts with broader market volatility but does not yet indicate strength.

Macro:

The macro backdrop is increasingly defined by supply constraints and policy tightening, creating a challenging environment for risk assets. The interaction between these forces will likely dictate near-term market direction.

Markets are not yet in full capitulation, but the underlying conditions suggest fragility. The coming sessions will likely determine whether stability can hold or further adjustment is required.