Geopolitical Risk Peaks, Positioning Extremes Build Beneath Weak Structure

Markets are entering the week with a noticeably heavier tone, as risk appetite fades and participation becomes increasingly defensive. What began as cautious optimism early in the week gave way to late-week de-risking, with flows suggesting investors were more focused on protecting downside than chasing upside. The shift was not abrupt, but gradual — a steady erosion of confidence as macro uncertainty built through the week.

Beneath the surface, oil and the dollar are tightening financial conditions. This tightening is subtle but impactful, feeding into pricing across assets and limiting upside follow-through. The result is a market that feels fragile, reactive, and highly sensitive to headlines, with positioning now leaning heavily toward caution rather than conviction.

Market Overview: Risk-Off Positioning Dominates as Structure Weakens

Equity markets are showing clear signs of stress, with breadth deteriorating and key technical levels either breaking or sitting on thin support.

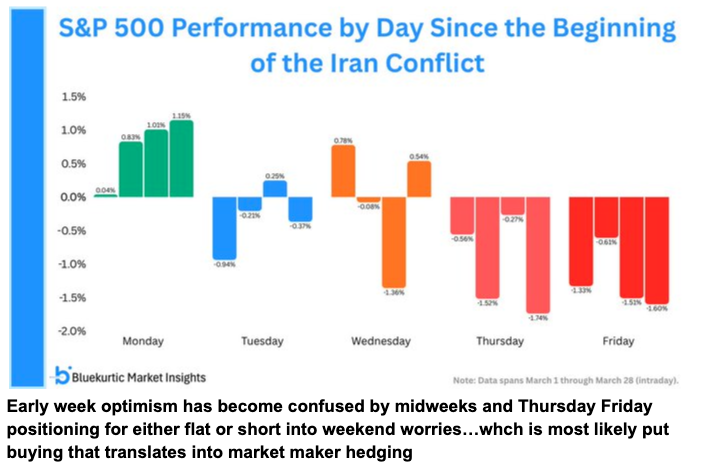

The shift in tone across the week was notable — early optimism faded into persistent selling pressure, particularly into Thursday and Friday, where positioning reflected weekend risk aversion rather than directional confidence. This type of price action typically reflects uncertainty rather than a strong bearish conviction.

The underlying structure suggests a market trading like a downtrend, where rallies are consistently sold into rather than extended. with systematic strategies and shorter-term participants dominating price movements. There is limited evidence of strong dip-buying flows stepping in with conviction.

At the core of this shift is the macro overlay, where geopolitical developments and energy markets are dictating sentiment more than traditional economic drivers. This has created a market environment where price action is being shaped externally, reducing the reliability of typical technical signals and increasing sensitivity to news-driven moves.

Macro & Policy Watch: Energy Shock, Rates Pressure, and Geopolitical Constraints

The dominant macro driver remains the ongoing geopolitical tension in the Middle East, with particular focus on critical energy transit routes and escalation risks. Developments around shipping restrictions and regional positioning have reinforced concerns around supply disruption, while the timeline of the conflict remains uncertain despite expectations of a relatively contained duration.

This has elevated oil’s role from a cyclical input to a core macro transmission mechanism, tightening financial conditions and feeding directly into inflation expectations. The market is increasingly treating energy as a constraint on policy flexibility rather than just a component of inflation.

Simultaneously, bond yields have moved higher, reflecting concerns around inflation persistence and the potential policy response. The recent behaviour in rates suggests that the bond market is reasserting itself as the dominant force.

Policy expectations remain conflicted, with markets balancing between inflation risks and eventual easing scenarios, increasing the likelihood of volatility across both rates and equities.

Technical & Sentiment Breakdown: Supportive, but Increasingly Fragile

While the broader structure shows signs of weakening, sentiment and positioning metrics suggest conditions are becoming stretched, introducing the potential for instability in both directions. But the market is no longer cleanly positioned for continuation.

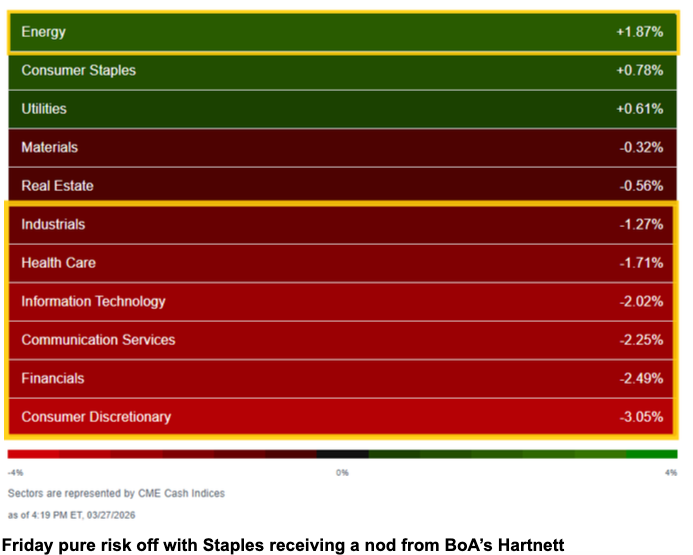

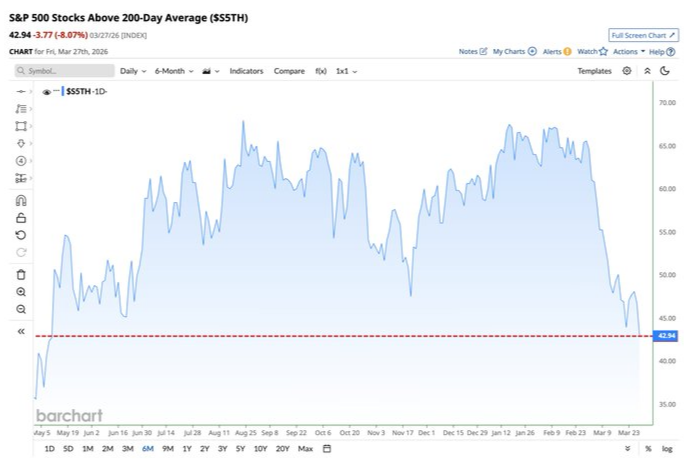

Breadth indicators highlight the extent of the pressure, with large parts of the market trading below key moving averages. This reflects a broad-based risk-off move, rather than weakness isolated to specific sectors or themes.

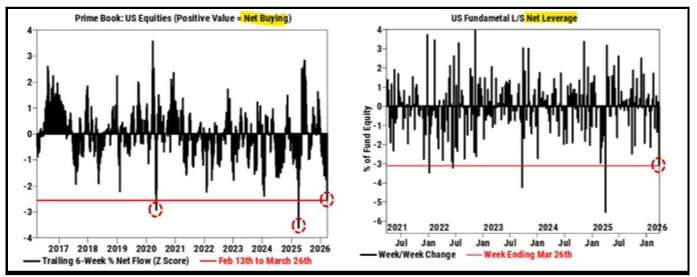

At the same time, positioning data suggests that hedging activity and short exposure have increased materially, indicating a market that is already leaning defensive. This type of positioning can limit further downside momentum unless new catalysts emerge.

Volatility has remained elevated, reinforcing the idea that uncertainty is actively being priced, not ignored. Sustained elevated volatility tends to create more abrupt moves and less stable trends.

The combination of weak structure and stretched positioning creates a fragile equilibrium, where even modest shifts in narrative could lead to sharp counter-trend moves or accelerated downside, depending on the catalyst.

Last Week’s Recap: From Early Optimism to Late-Week De-Risking

The past week reflected a clear transition from initial stability to defensive positioning, with macro developments gradually overriding underlying market resilience. The shift in tone was most visible in the latter half of the week, where flows indicated increasing caution and reduced willingness to hold risk into uncertainty.

Key Highlights:

Macro:

Rising input costs and energy pressures continued to build, reinforcing concerns around inflation persistence driven by supply-side constraints. These pressures are not yet fully reflected in broader data but are increasingly visible in leading indicators and upstream inputs.

China:

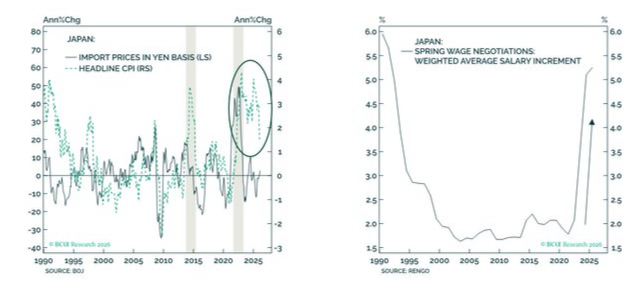

Energy dynamics are being viewed through the lens of broader global pricing trends, with implications for demand cycles and inflation trajectories. The interaction between energy costs and domestic conditions remains a key area of focus.

Earnings:

Corporate outlook remains sensitive to macro uncertainty, particularly around cost pressures and demand visibility. This is contributing to a more cautious tone, even in the absence of widespread negative revisions.

Commodities:

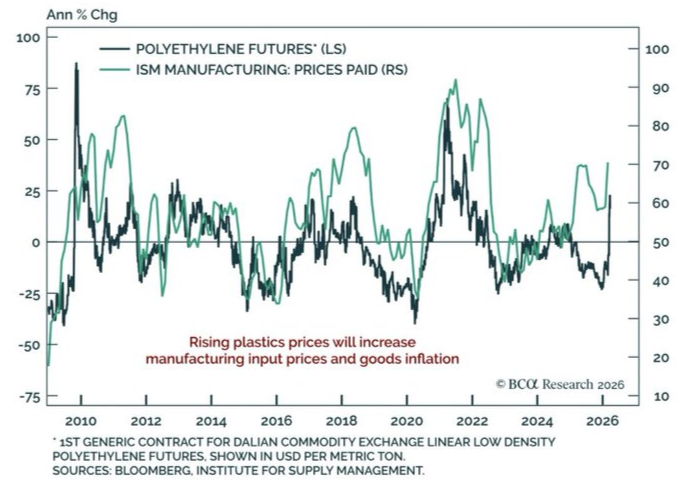

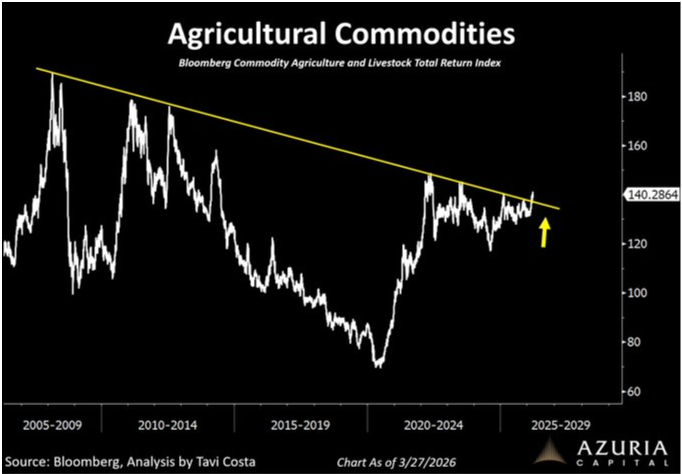

Agricultural and input-related commodities continue to highlight upstream inflation pressures, suggesting that cost pressures may continue to feed through into broader price levels over time.

Crypto:

Digital assets remain under pressure, with extended weakness reflecting reduced speculative participation and broader risk aversion. The persistence of downside highlights the absence of strong inflows.

Oil:

Energy markets remain central to the macro narrative, with pricing reflecting both current constraints and forward-looking risks tied to geopolitical developments. The balance between supply concerns and market expectations continues to drive volatility.

The Week Ahead: Key Data and Market-Moving Signals

The week is driven by a dense macro calendar alongside ongoing geopolitical developments, with a focus on central bank communication, inflation data, and labour market signals. Markets will be reacting through the lens of yields, oil, and positioning, with data likely reinforcing or challenging the current macro narrative.

Monday, March 30

- Germany: CPI (regional and national)

- UK: Credit, lending, and money supply data

- EU: Business sentiment and consumer confidence

- US: Dallas Fed Manufacturing Index

- US: 3-month and 6-month bill auctions

- Fed Chair Powell and Fed speakers

Tuesday, March 31

- Japan: CPI (Tokyo), unemployment, retail sales

- China: Manufacturing and non-manufacturing PMIs

- Australia: RBA meeting minutes

- UK: GDP and housing data

- Germany: Retail sales and unemployment

- France: CPI and consumer spending

- Eurozone: CPI and core inflation

- US: House price indices and Chicago PMI

- US: Consumer confidence and JOLTS job openings

- US: API crude oil inventories

- Fed and ECB speakers

Wednesday, April 1

- Japan: Tankan survey (business outlook)

- China: Manufacturing PMI

- Europe: Manufacturing PMI (France, Germany, Eurozone, UK)

- US: ADP Nonfarm Employment

- US: Retail sales and core retail sales

- US: ISM Manufacturing (prices, employment, orders)

- US: Crude oil inventories

- Fed, ECB, and BoC speakers

Thursday, April 2

- South Korea and China: CPI

- India: Manufacturing PMI

- Italy: Retail sales

- US: Initial and continuing jobless claims

- US: Trade balance, exports, and imports

- Canada: Trade balance

- US: Fed balance sheet and reserve data

- ECB Economic Bulletin

Friday, April 3

- Japan and China: Services PMI

- US: Nonfarm Payrolls (NFP)

- US: Unemployment rate and participation

- US: Average hourly earnings

- US: S&P Global Services and Composite PMI

- Global: Good Friday holiday (low liquidity conditions)

Alpha Takeaway: Positioning Extreme, Macro Uncertain

Markets are navigating a period where macro-driven volatility and positioning extremes are interacting in real time, creating a fragile but reactive environment. The balance between structure and sentiment is becoming increasingly delicate.

Equities:

Many markets have either broken key supports or are sitting on them, with rallies being heavily leaned on and price action reflecting a clear risk-off tone. Positioning into the end of the week also suggests caution, with flows leaning defensive.

Gold & Silver:

Gold has bounced off the lower trendline, marking a classic point of potential rally or pivot, with price action sitting at a level where a move higher or rejection becomes important.

Crypto:

Crypto is set for a sixth consecutive red month, matching one of its worst historical runs, highlighting persistent weakness and lack of sustained buying.

Macro:

The pace of US10Y yields is dictating market direction, while oil and the dollar are tightening financial conditions, reinforcing the pressure across assets.

There are optimum conditions for a counter-trend consolidation rally, with positioning stretched and markets already leaning defensive. That said, the environment remains headline-driven, with rates and geopolitics continuing to dictate direction. Trade carefully.