Energy Shock Emerges, Inflation Sensitivity Returns to the Fore

Markets move into the second week of March, navigating an environment where geopolitical developments and energy markets have begun to reshape macro sensitivities. Price action across assets suggests that positioning has become more cautious as markets adjust to higher energy prices and evolving geopolitical developments.

Beneath the surface, participation appears increasingly selective. Commodity volatility has lifted from previously suppressed levels, currency dynamics are adjusting to global trade sensitivities, and equity indices are approaching key technical thresholds. The resulting price action reflects markets becoming increasingly responsive to energy dynamics and inflation risk.

Market Overview: Energy Repricing Meets Structural Stability

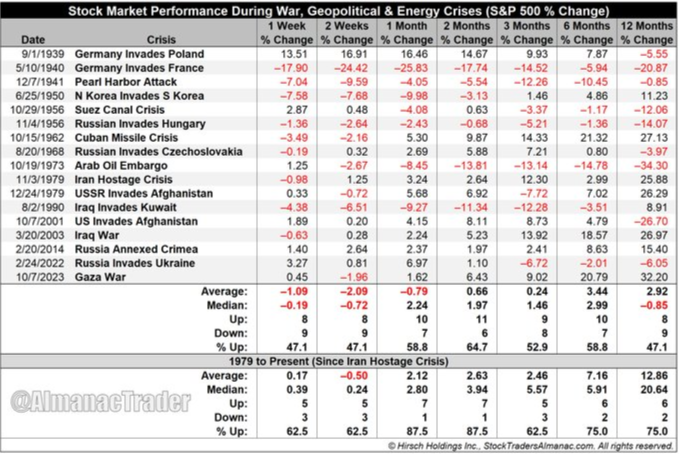

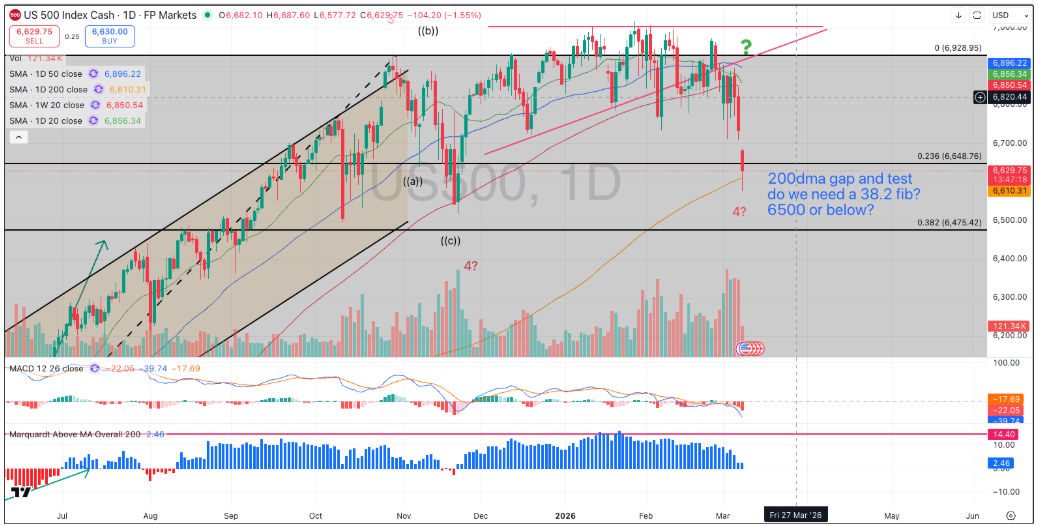

Equity markets have been absorbing recent developments without a broad deterioration in price structure but lost the 100dma and wicked the 200dma on the SPX overnight. Recent developments in energy markets have amplified macro sensitivity across asset classes, particularly as oil prices surged sharply following renewed geopolitical tensions.

The move in crude followed growing concerns around transport disruptions and geopolitical tensions affecting the Strait of Hormuz. Reduced maritime activity and heightened military developments in the region increased the perceived risk premium embedded in energy markets.

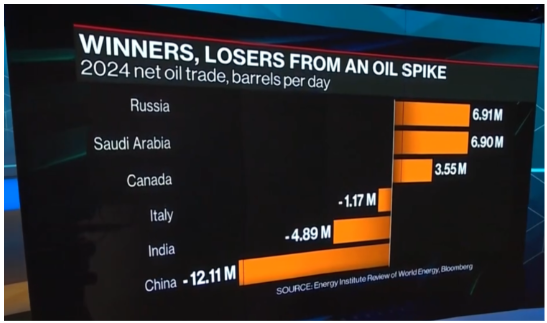

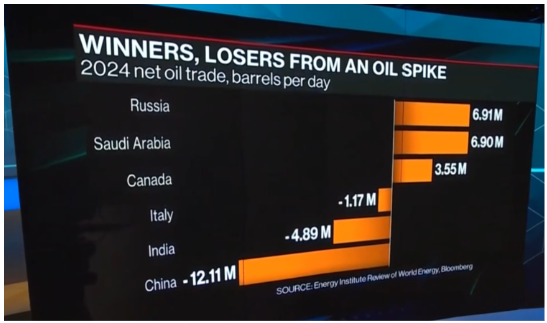

This shift in energy pricing has broader implications across global markets. Economies heavily dependent on imported energy face potential inflation pressure, while resource exporters may benefit from higher commodity prices.

Despite this volatility, equity markets have not yet experienced widespread structural damage. Instead, recent behaviour suggests markets are adjusting to geopolitical developments and energy price volatility rather than responding to a clear deterioration in macro data.

Macro & Policy Watch: Inflation Sensitivity Re-emerges

Energy markets have become a central macro variable once again. Rising crude prices introduce renewed sensitivity around inflation expectations, particularly through transportation and energy cost channels.

This dynamic increases sensitivity around inflation expectations as energy prices rise. Inflation pressures linked to commodity prices can influence expectations around monetary policy, especially when economic data remains mixed.

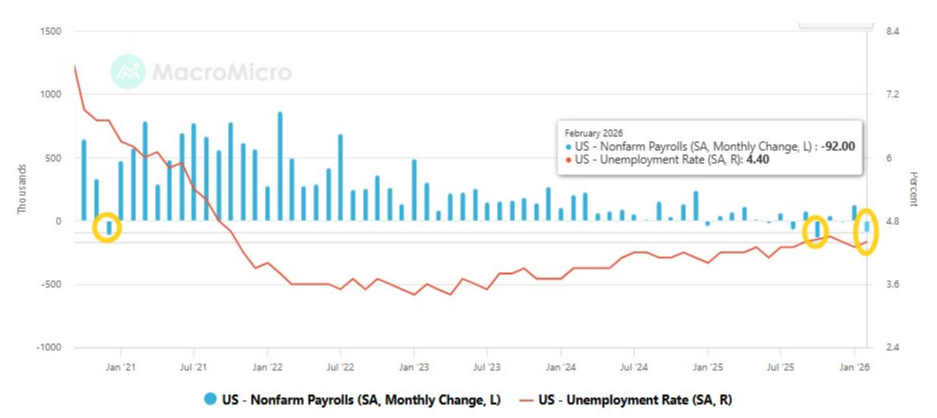

Labour market data continues to show uneven signals. Employment growth softened in the latest reading, though some interpretations suggest technical factors may have influenced the result.

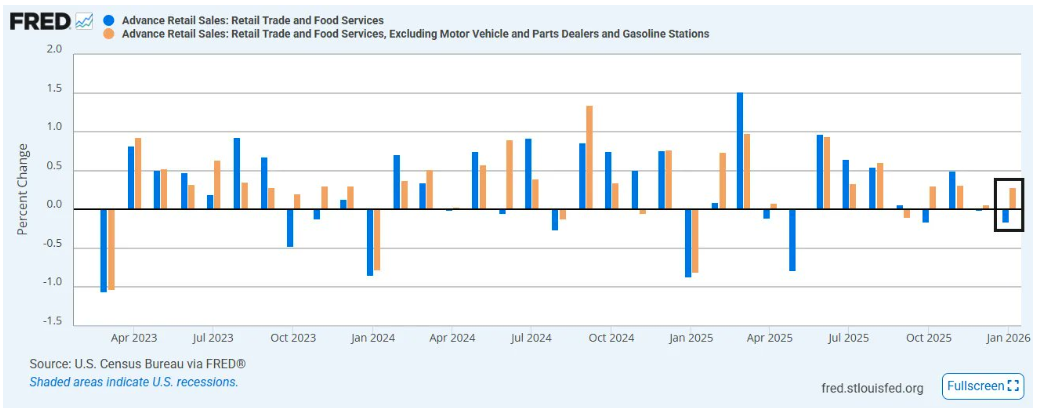

Consumer spending data reinforced the mixed macro picture. While several discretionary categories weakened, the retail control group — which feeds into GDP calculations — remained positive, indicating that underlying consumption has not materially deteriorated.

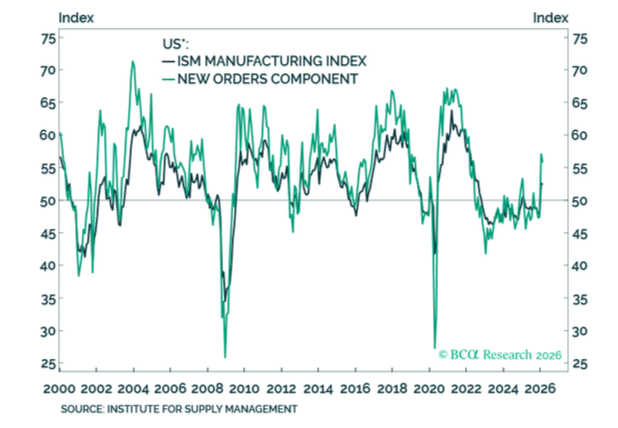

Manufacturing indicators also strengthened, with both the ISM manufacturing index and new orders components improving.

Outside the United States, policy dynamics remain uneven. China has lowered growth expectations but has not yet deployed significant stimulus measures, leaving fiscal support relatively limited.

Technical & Sentiment Breakdown: Supportive, but Increasingly Fragile

Market structure across equities remains broadly intact, though several indicators suggest momentum may be slowing.

Currency markets are beginning to reflect these shifting dynamics. The U.S. dollar is approaching important technical levels as positioning dynamics continue to evolve.

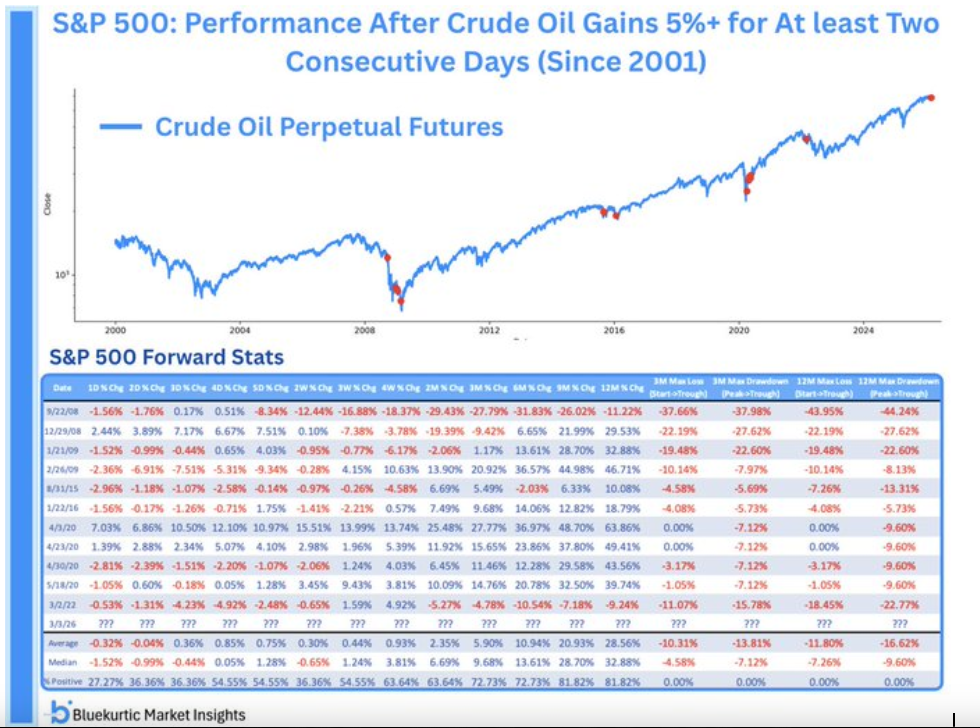

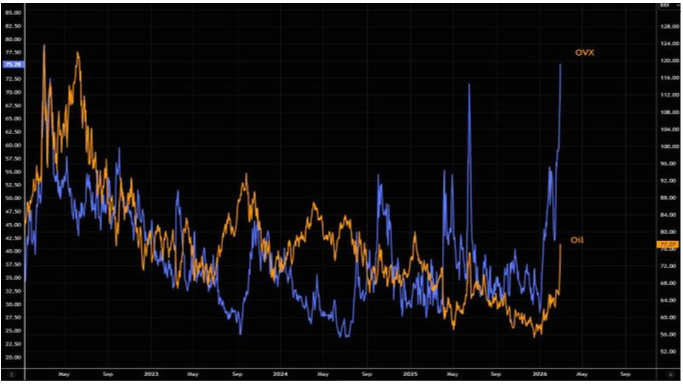

Volatility dynamics have also changed meaningfully in energy markets. After a prolonged period of subdued fluctuations, oil volatility has surged alongside the sharp repricing in crude prices.

Equity indices are now approaching key technical levels. The S&P 500 recently interacted with major moving averages that often act as important inflection points for trend continuation or reversal.

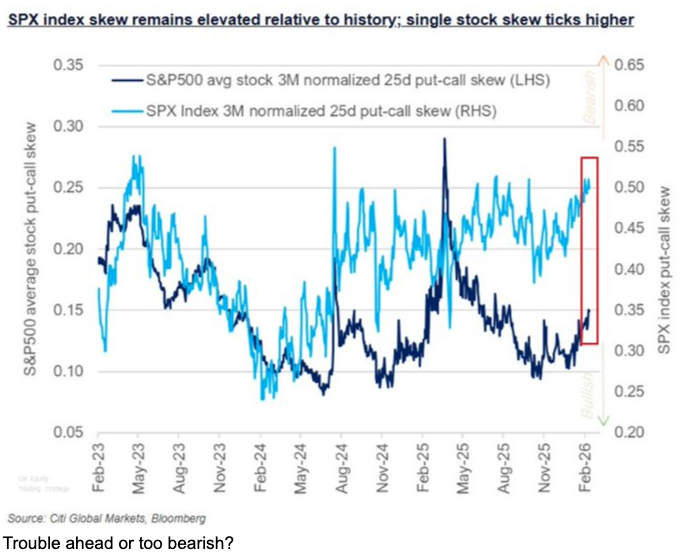

Options positioning further reflects growing caution. Skew dynamics suggest increased demand for downside protection even while indices remain broadly supported.

Last Week’s Recap: Energy Volatility and Mixed Macro Signals

Recent market developments reflected a shift in attention toward energy markets and geopolitical developments, while macro data continued to provide mixed signals regarding economic momentum.

Key Highlights:

Macro:

Labour market data delivered a softer reading, though the weakness may partially reflect technical adjustments rather than a structural deterioration in employment conditions.

China:

Growth projections were lowered while fiscal stimulus remained limited, suggesting policymakers are adopting a cautious approach toward economic support.

Earnings:

Equity markets continued to exhibit concentrated leadership, with flows rotating through the most liquid exposures rather than broad market selling.

Commodities:

Energy markets became the focal point as crude prices surged following geopolitical developments and concerns surrounding transport routes and production dynamics.

Crypto:

Crypto markets continue to trade around key technical structures while momentum signals remain mixed.

Oil:

Crude markets reacted sharply to developments surrounding the Strait of Hormuz and broader geopolitical tensions affecting the region.

The Week Ahead: Key Data and Market-Moving Signals

The week centres on the US CPI on Wednesday, which will be closely watched by markets. Growth signals will also be watched through Japan's GDP early in the week and UK and US GDP releases on Friday, alongside JOLTS job openings and Michigan consumer sentiment.

Monday, March 9

China: CPI (MoM), CPI (YoY), PPI (YoY)

Japan: GDP (Q4), GDP Annualised, Private Consumption, Capital Expenditure

Japan: Leading Index, Coincident Indicator, Economy Watchers Index

Eurozone: German Factory Orders, German Industrial Production

Eurozone: Sentix Investor Confidence

US: CB Employment Trends Index

US: NY Fed 1-Year Consumer Inflation Expectations

Tuesday, March 10

UK: BRC Retail Sales Monitor

Australia: NAB Business Confidence, Building Approvals

China: Imports, Exports, Trade Balance

Eurozone: German Trade Balance, German Imports and Exports

France: Trade Balance and Current Account

US: NFIB Small Business Optimism

US: Existing Home Sales

US: API Weekly Crude Oil Stocks

Japan: PPI (MoM, YoY)

Wednesday, March 11

Germany: CPI (MoM, YoY), HICP

US: CPI (MoM, YoY), Core CPI

US: Real Earnings

US: Crude Oil Inventories

US: Federal Budget Balance

Thursday, March 12

US: Initial Jobless Claims, Continuing Claims

US: Housing Starts and Building Permits

US: Trade Balance

US: Natural Gas Storage

US: Atlanta Fed GDPNow

Friday, March 13

UK: GDP (MoM, YoY), Industrial Production, Manufacturing Production

Eurozone: Industrial Production

US: GDP (QoQ) and GDP Price Index

US: Core PCE Price Index and PCE Price Index

US: Personal Income and Personal Spending

US: Durable Goods Orders

Canada: Employment Change and Unemployment Rate

US: JOLTS Job Openings

US: Michigan Consumer Sentiment and Inflation Expectations

Alpha Takeaway: Energy Sensitivity Returns

Markets are adjusting to the re-emergence of energy as a dominant macro driver, introducing renewed sensitivity around inflation and policy expectations.

Equities:

Indices remain structurally supported but are approaching technical levels where positioning and sentiment may play a larger role in determining short-term direction. Could an input cost like oil de-rail earnings growth for 2026/7? That is key now.

Gold & Silver:

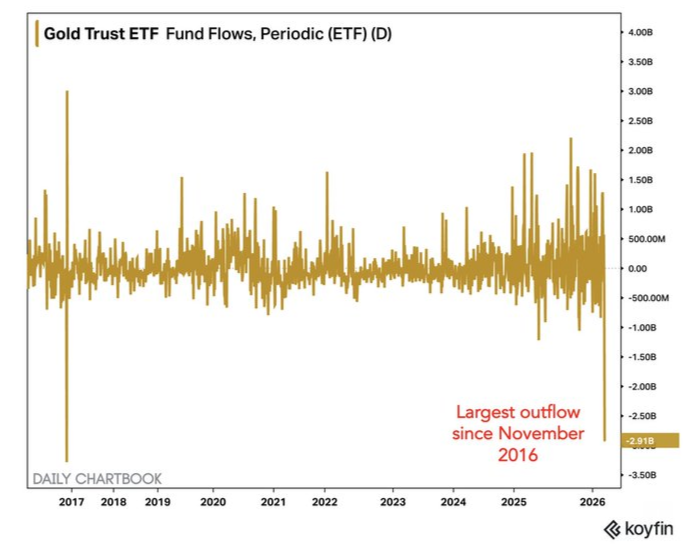

Precious metals continue to experience mixed flows as interest rate dynamics and macro positioning influence investor allocation decisions. Recent ETF outflows may be the factor for weakness here.

Crypto:

Digital assets remain closely linked to broader liquidity conditions and risk sentiment rather than functioning as independent defensive assets.

Macro:

Energy prices, inflation expectations, and policy responses are increasingly shaping global market dynamics.

The current environment reflects a market adjusting to new variables rather than one undergoing structural deterioration. Positioning dynamics may continue to drive episodic volatility as markets respond to geopolitical developments and energy price movements.