Earnings Momentum Accelerates, While Geopolitical and Inflation Risks Quietly Build

Markets continue to trend higher, but the character of the move increasingly reflects an environment being driven by earnings momentum and positioning flows rather than broad macro clarity.

Strong guidance revisions, improving forward estimates, and persistent participation in AI-linked themes continue to support equities, even as multiple cross-asset warning signs begin to emerge underneath the surface.

At the same time, correlations across commodities, rates, currencies, and risk assets are beginning to shift. Geopolitical tensions around the Strait of Hormuz, higher fuel costs, and inflation-sensitive supply pressures are creating a more fragile backdrop beneath an otherwise resilient equity market. The result is a market that continues trending higher, but with increasing sensitivity to macro developments.

Market Overview: Earnings Expansion Continues to Support Equities

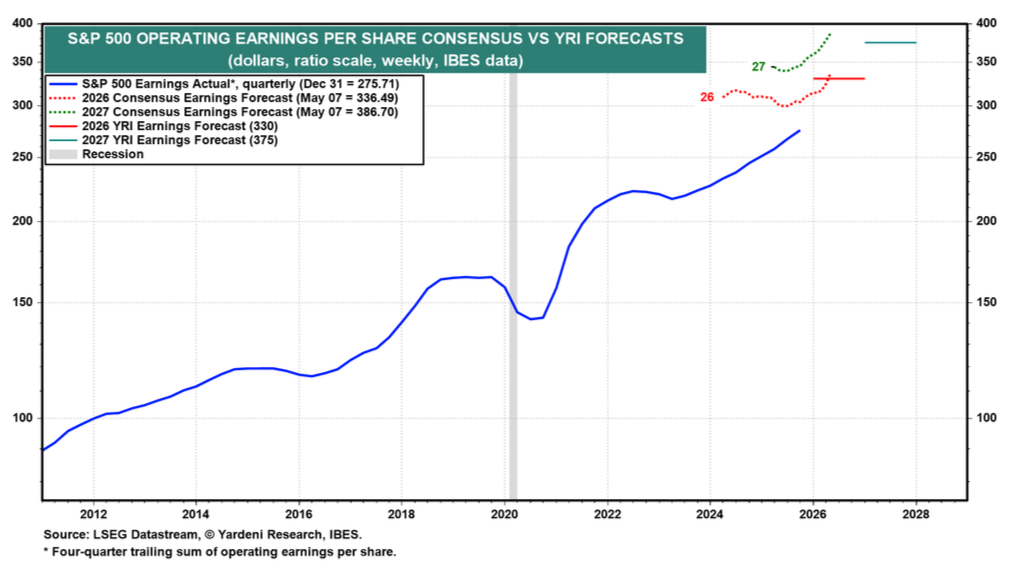

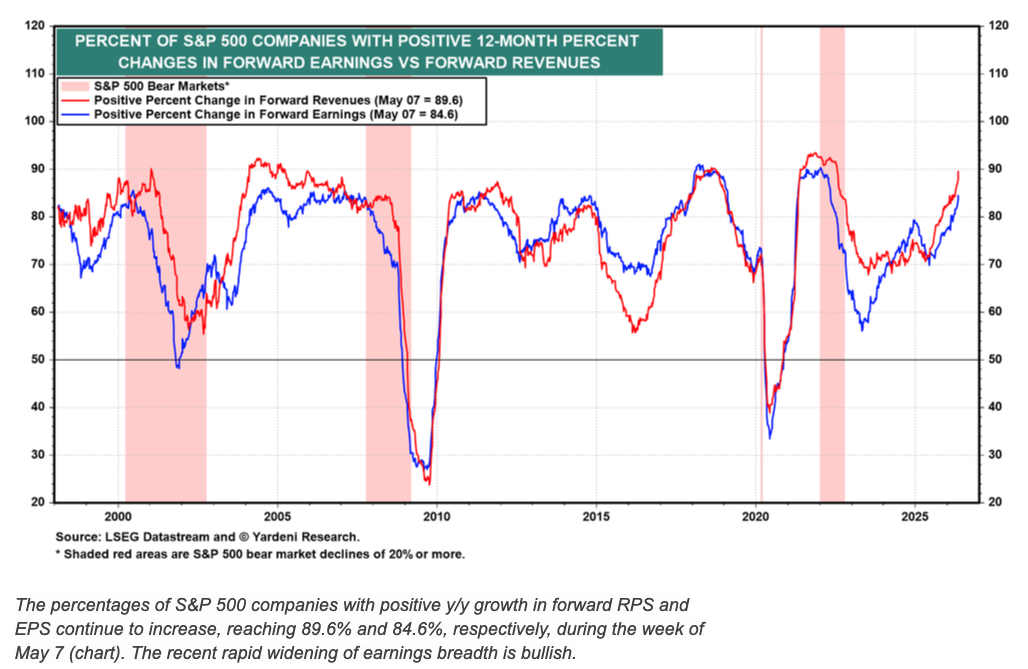

Equities remain supported by an unusually strong earnings backdrop, with consensus S&P 500 estimates continuing to rise at one of the fastest rates on record. Forward expectations for both 2026 and 2027 continue being revised aggressively higher, continuing to support the broader move in equities.

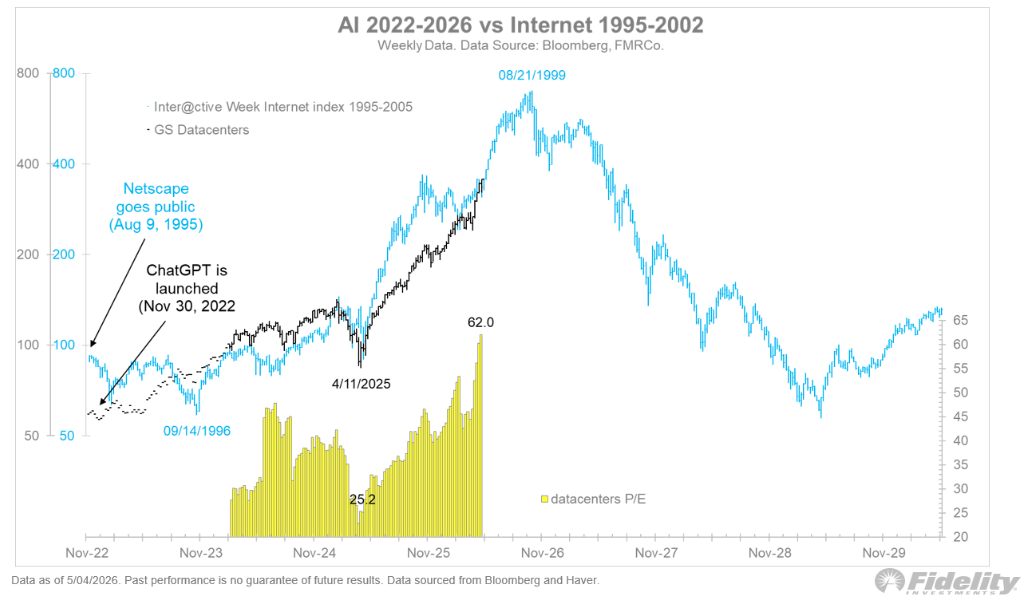

Technology and AI-linked leadership continue dominating broader index performance, but the report repeatedly highlights that earnings breadth itself is also improving beneath the surface. Positive revisions are expanding beyond a narrow group of mega-cap names, helping support the broader structure of the rally.

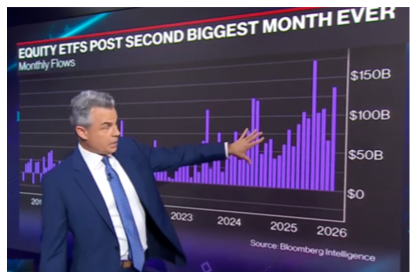

Positioning dynamics also remain an important driver. The rally continues pulling underinvested participants back into the market as momentum extends.

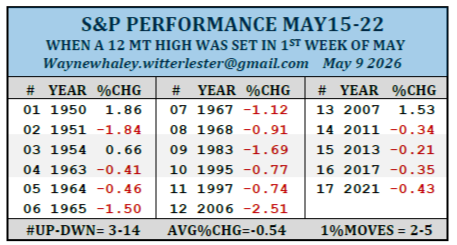

At the same time, the report highlights growing caution around concentration and momentum extension. Seasonal patterns suggest the potential for short-term consolidation during the second half of May, particularly within a midterm year backdrop where summer volatility has historically increased.

Overall, the broader trend remains constructive, supported by earnings momentum, liquidity conditions, and persistent participation in growth leadership. However, the increasing reliance on momentum and positioning flows suggests a market becoming progressively more sensitive to macro shifts and leadership rotation.

Macro & Policy Watch: Geopolitical Stress, Fuel Costs, and Inflation Pressures

The macro backdrop continues to become more layered as geopolitical risks, energy dynamics, and inflation pressures interact simultaneously.

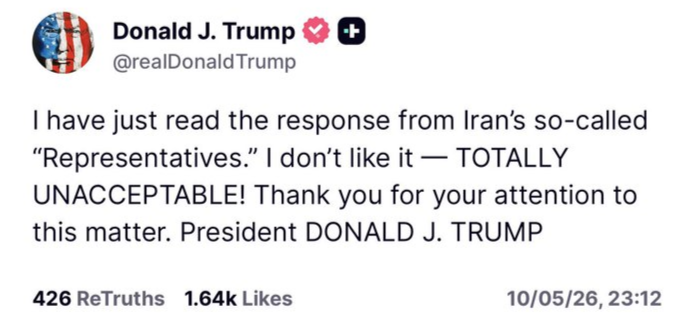

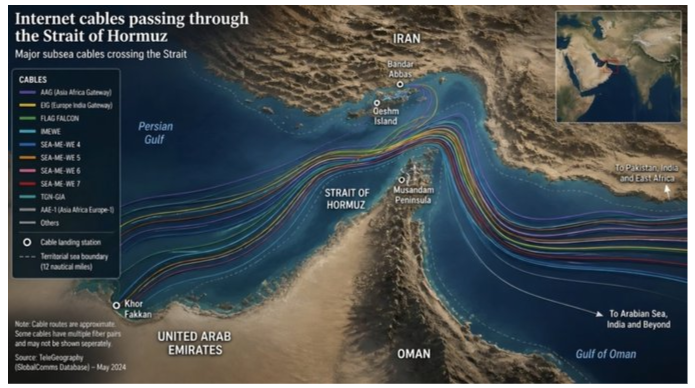

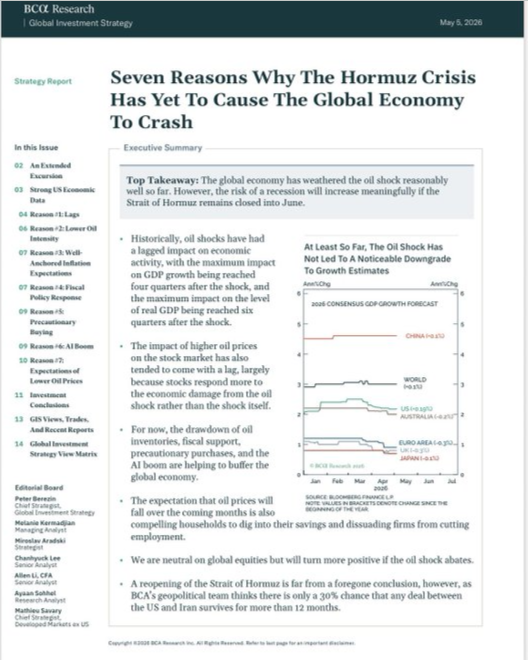

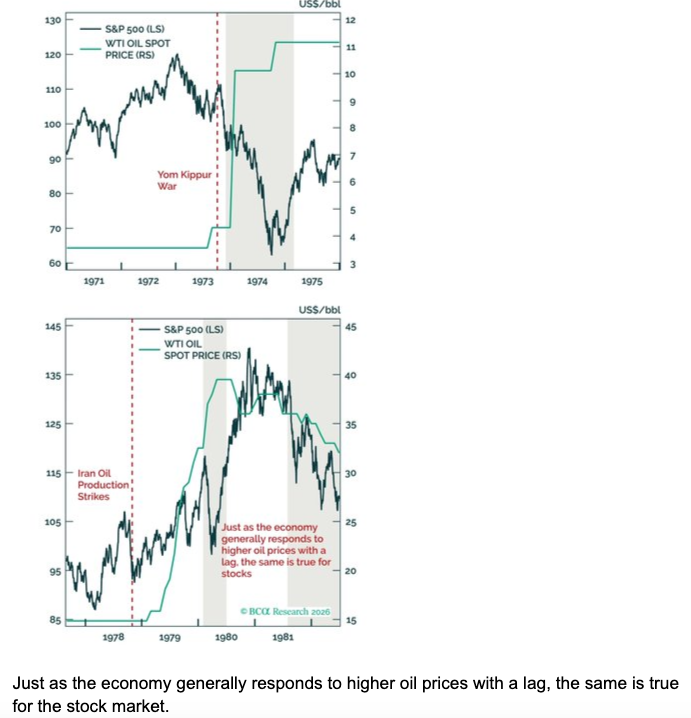

A major focus throughout the report remains the Strait of Hormuz and the broader implications of Iranian escalation risks. Discussions surrounding shipping rules, tanker seizures, and undersea communication cables continue raising concerns around disruption risks tied to the region.

The report repeatedly raises the possibility that oil markets are not fully reflecting the broader geopolitical risk premium currently building underneath the surface.

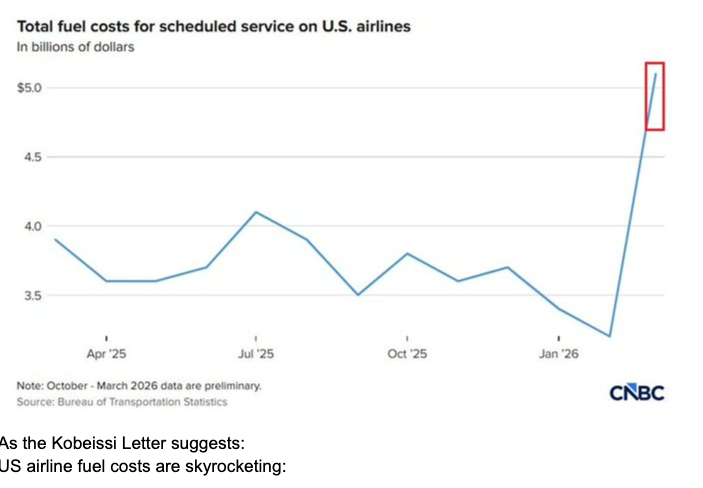

At the same time, fuel costs are increasingly feeding into broader inflation expectations. Airline pricing pressures, rising transportation costs, and supply-side disruptions continue reinforcing concerns that inflation pressures could remain elevated even as growth conditions remain relatively resilient.

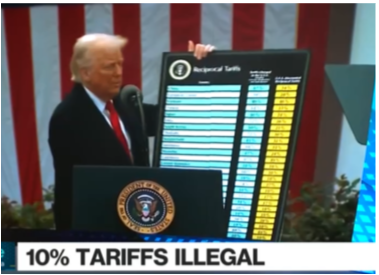

Trade policy and global political developments also remain part of the broader macro environment. Tariff rulings, ongoing US-EU negotiations, and China-related developments continue adding complexity to the global policy backdrop.

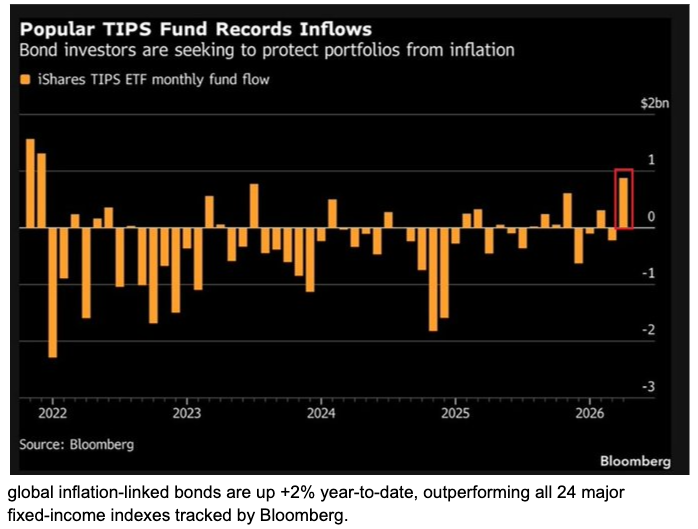

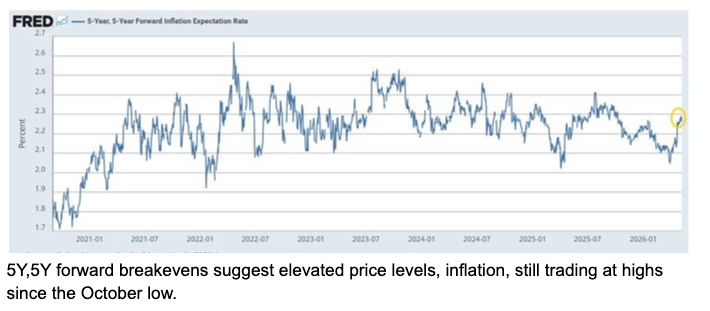

Inflation expectations themselves also continue showing signs of stabilisation at elevated levels, while breakeven inflation measures remain firm despite continued policy uncertainty.

Meanwhile, FX intervention discussions from Japan and broader global liquidity conditions continue influencing cross-asset correlations and rate expectations.

Technical & Sentiment Breakdown: Supportive, but Increasingly Fragile

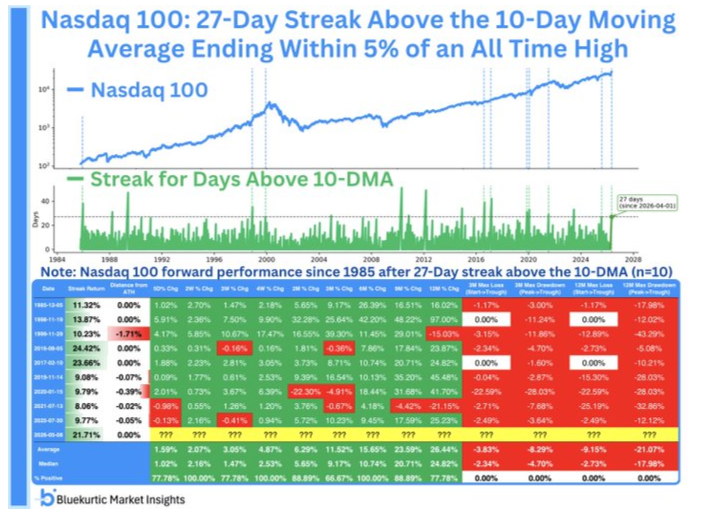

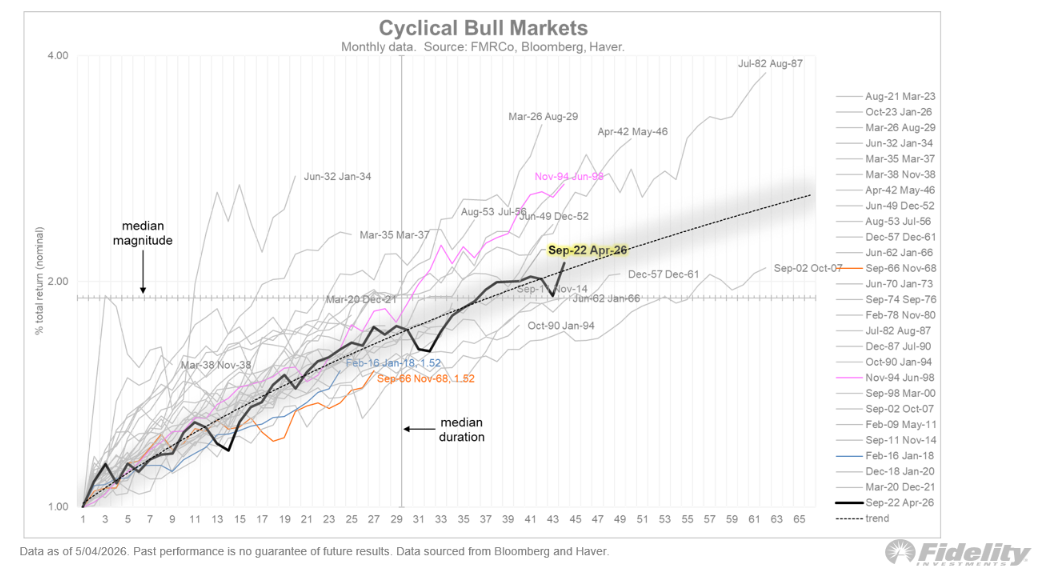

The broader technical trend remains intact, with equity indices continuing to hold strong momentum conditions near highs. Historical comparisons highlighted throughout the report suggest similar Nasdaq structures have historically tended to continue trending rather than reverse immediately.

Longer-term cyclical conditions also continue appearing supportive, reinforcing the idea that the broader market structure remains intact even as shorter-term positioning becomes increasingly extended.

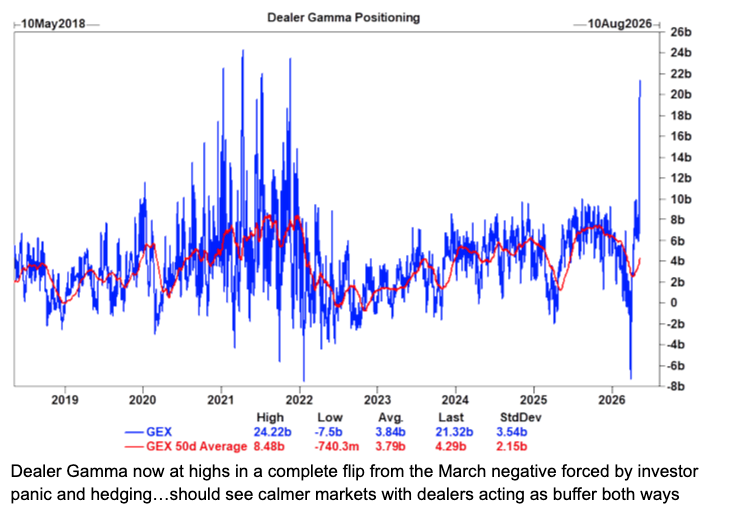

At the same time, positioning conditions continue to become increasingly crowded. Dealer positioning and momentum participation continue supporting the move.

The report also repeatedly raises caution around concentration and historical analogue comparisons tied to previous technology-led expansions. While earnings continue supporting the broader move, the combination of narrow leadership and increasingly crowded positioning increases sensitivity to shifts in leadership and positioning.

Cross-asset relationships are also becoming increasingly important, with commodities, inflation hedges, rates, and equities reacting more closely together as macro liquidity conditions continue shaping broader market behaviour.

Overall, trend conditions remain constructive, but the internal quality of the move is becoming more sensitive to shifts in positioning, leadership, and macro conditions.

Last Week’s Recap: Strong Earnings Momentum, Rising Macro Complexity

The past week continued reflecting a market supported by strong earnings revisions and resilient momentum, while geopolitical tensions, inflation pressures, and commodity dynamics became increasingly important beneath the surface.

Key Highlights:

- Macro:

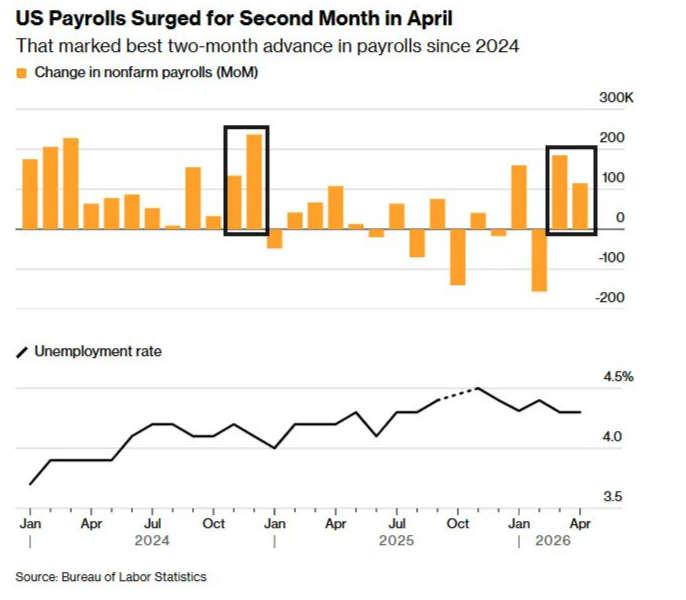

Labour market data remained broadly supportive, with payroll gains continuing while wage growth moderation remained intact. At the same time, consumer sentiment readings remained historically weak, while inflation expectations continued to rise.

- China:

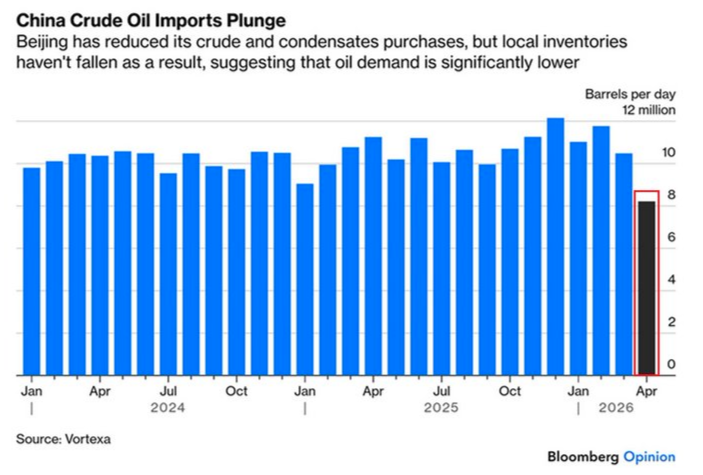

China-related developments remained closely tied to the broader commodity and demand backdrop. The report highlighted oil reserve behaviour, gold accumulation dynamics, and broader implications for global pricing and trade flows.

- Earnings:

Earnings remained one of the strongest pillars supporting equities, with forward revisions continuing to accelerate across multiple sectors. Energy and technology-linked themes remained particularly important drivers of upward estimate revisions. - Commodities:

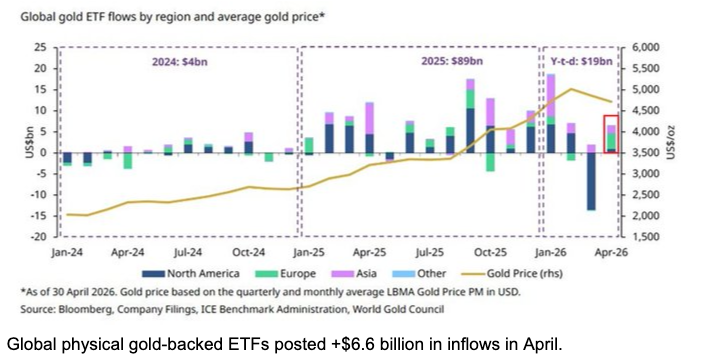

Commodity markets continued responding to geopolitical risks, inflation expectations, and supply-side pressures. Copper maintained strong breakout conditions while gold flows recovered sharply alongside renewed ETF inflows.

- Crypto:

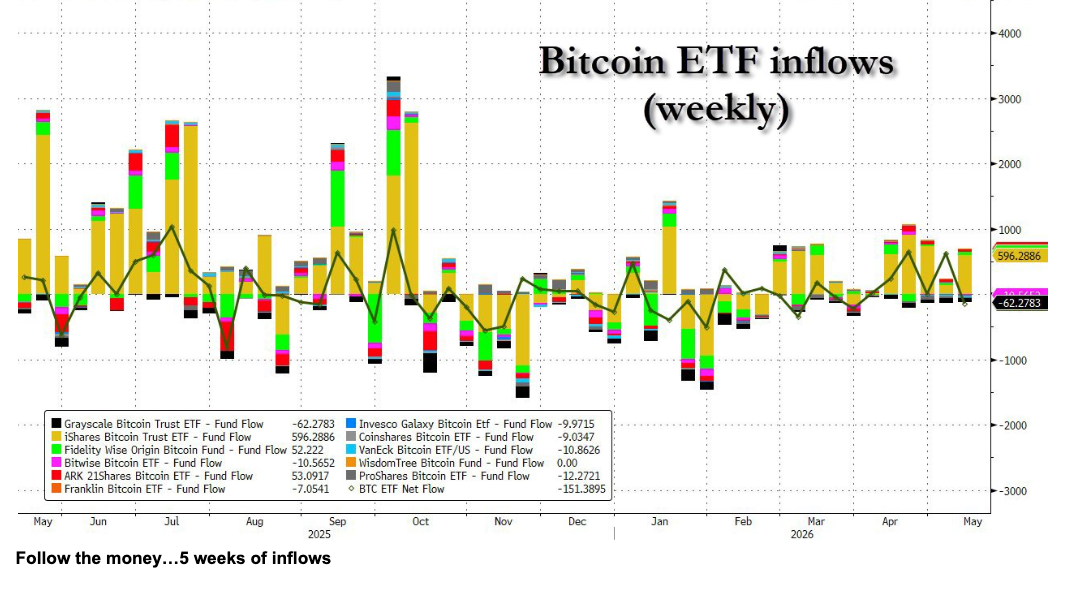

Crypto continued seeing supportive inflows alongside broader inflation-hedge discussions, while Bitcoin participation remained supported by continued ETF inflows.

- Oil:

Oil remained central to the macro narrative, with Strait of Hormuz developments, fuel shortages, and shipping concerns continuing to shape inflation and supply expectations.

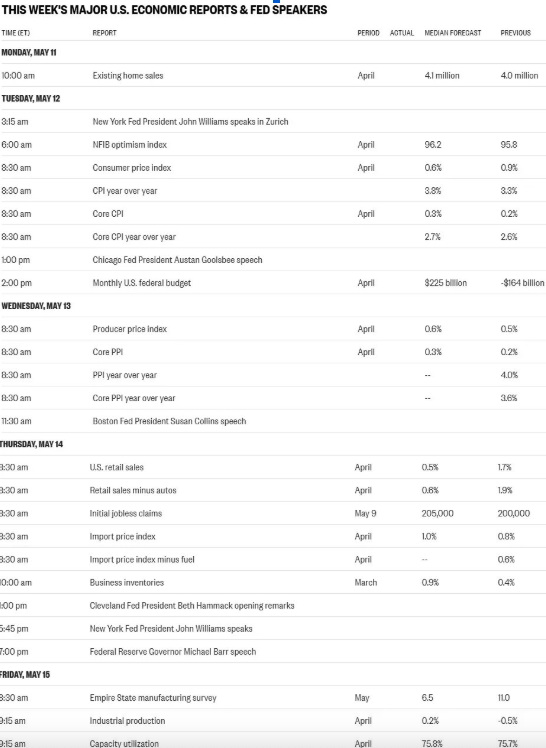

The Week Ahead: Key Data and Market-Moving Signals

The week ahead remains focused on inflation, consumption, and rates, with US CPI, retail sales, and PPI expected to drive macro expectations. Treasury auctions, energy reports, and ongoing Fed communication will remain central for liquidity and rate pricing, while the Senate vote on Kevin Warsh as Fed Chair remains an important policy focus for markets.

Monday, May 11

• Australia: Building Approvals and Housing Data

• China: CPI and PPI Inflation Data

• US: Existing Home Sales and Employment Trends Index

• Germany & France: Short-Term Debt Auctions

• US: 3-Month and 6-Month Bill Auctions

• US: 3-Year Note Auction

• Germany: Bundesbank Monthly Report

Tuesday, May 12

• Japan: Household Spending and Foreign Reserves

• Australia: Westpac Consumer Sentiment and NAB Business Confidence

• Germany: CPI and HICP Inflation Data

• US: NFIB Small Business Optimism

• US: ADP Employment Change

• US: CPI and Core CPI

• US: Federal Budget Balance

• US: API Crude Oil Inventories

• Japan: BoJ Summary of Opinions

• US: WASDE Report and EIA Short-Term Energy Outlook

• US: 10-Year Note Auction

Wednesday, May 13

• Japan: Current Account and Bank Lending Data

• New Zealand: Inflation Expectations

• Eurozone: GDP, Employment, and Industrial Production

• US: MBA Mortgage Applications

• US: PPI and Core PPI

• Germany: 30-Year Bund Auction

• US: 30-Year Bond Auction

• OPEC Monthly Report

• IEA Monthly Report

• UK: BoE MPC Member Mann Speaks

• Canada: BoC Summary of Deliberations

Thursday, May 14

• UK: GDP, Industrial Production, Manufacturing Production, and Trade Balance

• Spain: CPI and HICP Inflation Data

• China: New Loans, M2 Money Supply, and Total Social Financing

• US: Retail Sales and Core Retail Sales

• US: Initial and Continuing Jobless Claims

• US: Import and Export Prices

• US: Business Inventories

• US: Atlanta Fed GDPNow Update

• Japan: 30-Year JGB Auction

• UK: BoE MPC Member Pill Speaks

Friday, May 15

• Japan: PPI Inflation Data

• South Korea: Export, Import, and Trade Balance Data

• Hong Kong: GDP Data

• India: Import, Export, and Trade Balance Data

• Europe: Reserve Assets and ECB Economic Bulletin

• US: NY Empire State Manufacturing Index

• US: Industrial Production and Manufacturing Production

• US: Capacity Utilisation Rate

• Canada: Manufacturing Sales and Housing Starts

Alpha Takeaway: Earnings Strength Meets Rising Cross-Asset Fragility

Markets remain supported by strong earnings revisions, improving breadth, and continued participation in AI-linked leadership. Earnings momentum and positioning continue supporting the broader trend even as macro conditions become increasingly layered underneath the surface.

- Equities:

Equities continue benefiting from accelerating forward earnings expectations and strong positioning dynamics, although concentration and momentum extension remain increasingly important risks to monitor. - Gold & Silver:

Precious metals continue reflecting broader inflation, liquidity, and reserve allocation dynamics. Strong ETF inflows and continued accumulation trends remain supportive for the broader structure. - Crypto:

Crypto continues benefiting from supportive inflows and broader inflation-hedge positioning, alongside continued participation in the broader risk and alternative asset backdrop. - Macro:

Geopolitical tensions, rising fuel costs, inflation-sensitive supply pressures, and shifting cross-asset correlations continue shaping the broader macro backdrop and influencing market sensitivity.

The broader trend remains constructive, but the report increasingly highlights a market where concentration, positioning, and macro conditions are becoming increasingly important. Momentum remains supportive, though the environment underneath is becoming progressively more complex.