Introduction: Buckle Up – Uncertainty may just have come off the Menu

Markets have been jittery, and for good reason. A continued walk up of indices in the face of increased macro risks has seen many fearing bears reappearing at the obvious resistance levels. Volatility continues to slide back to 20. Hawkish Fed rhetoric, geopolitical jitters and sliding Services prints with high prices paid lead to many including powell fear Stagflation. The S&P 500 continues to take out resistance levels and the positive news of China tariffs sees new highs for the rally. Bears talking of downside to growth now removed and the pro investors are short or underweight at the top of the rally. Record levels of uncertainty in result commentaries may just be about to be replaced by upgrades!

Key Market Themes: Sentiment Shifts, Liquidity Signals & Market Positioning

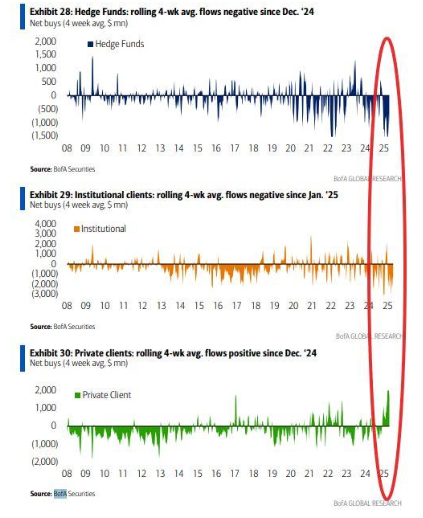

Risk Appetite: Retail All-In, Pros Hesitant

We are at a classic inflection point. Professional investors remain underweight, having missed the violent upside reversal triggered by the US-China tariff détente. Meanwhile, retail positioning has surged— "Buy the Dip" is not just alive; it’s euphoric.

This divergence between institutional caution and retail enthusiasm is critical. When private wealth clients lean in this hard, the market often finds itself overextended—even if fundamentals eventually catch up. Whether this is genuine conviction or a fear of missing out remains to be seen. As it is the 90day pause on US/China tariffs plus global liquidity suggests Risk on

The FOMO Trade & Short Squeeze Dynamics

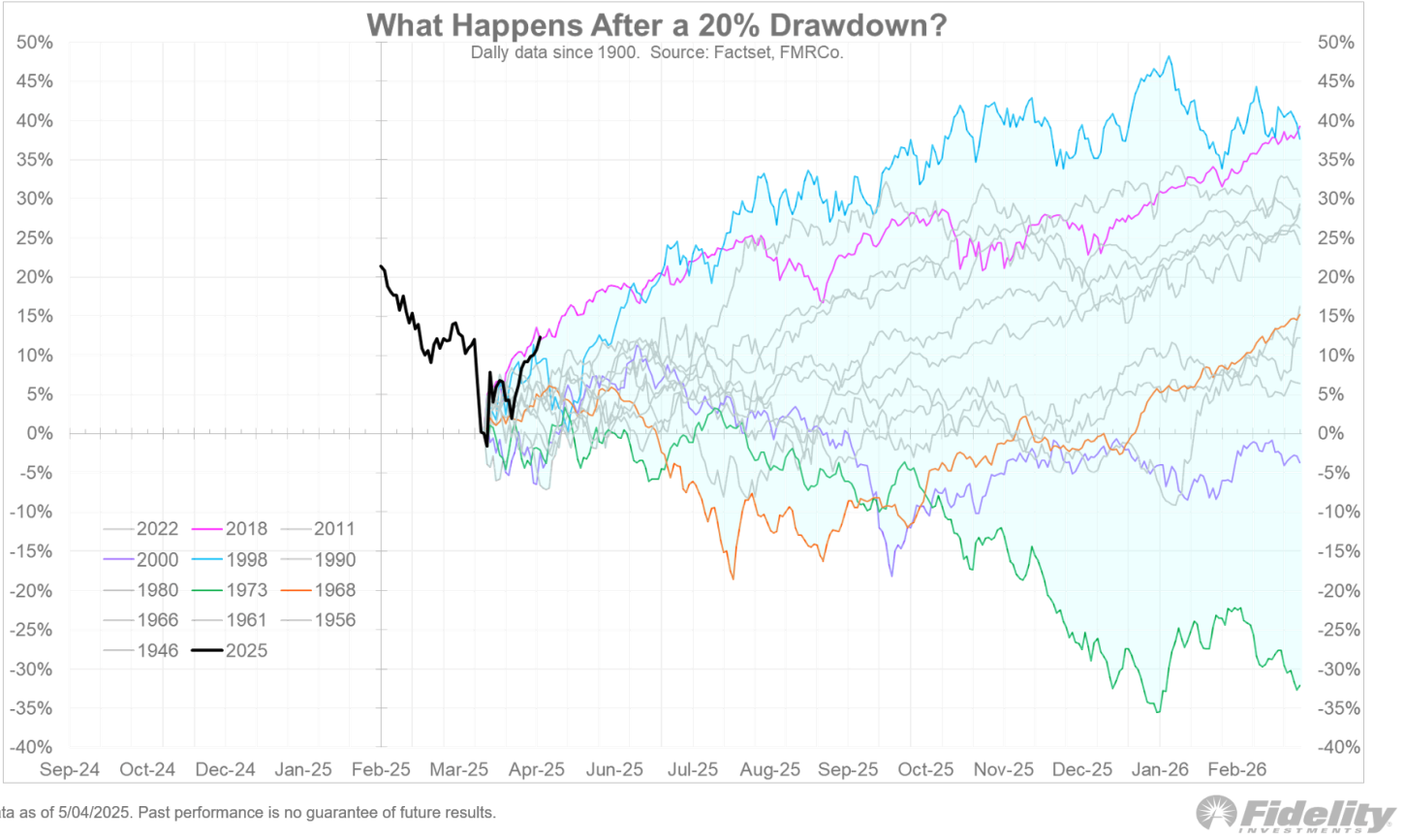

The comparison to 1996–1997 is gaining traction. Initially thought to be a repeat of the 1998 growth shock/mini crash narrative, price action now suggests we could be moving into an exuberant melt-up phase. It also mirrors the 2018 Trump 1.0 playbook with a growth shock ultimately ignored and no low re-test. Shorts may have to chase the market now that the downside tail risk has been chopped off.

Ed Yardeni, one of the more prominent market bulls, has reduced his recession probability to 35% and raised his year-end SPX target above 6000. That shift alone has caught strategist desks off-guard. Many had called for earnings downgrades and encouraged clients to wait for trough multiples around 15x forward earnings— levels that now feel increasingly out of reach.

Liquidity Is Speaking Louder Than Rates

The Fed might be on pause, but liquidity is not. The Fed SOMA account absorbed $38 billion in bonds last week boosting QE, and the PBOC added liquidity. It’s not official QE, but it’s having a similar impact. A short-VIX unwind created a stir but couldn’t stop the vacuum higher for equities.

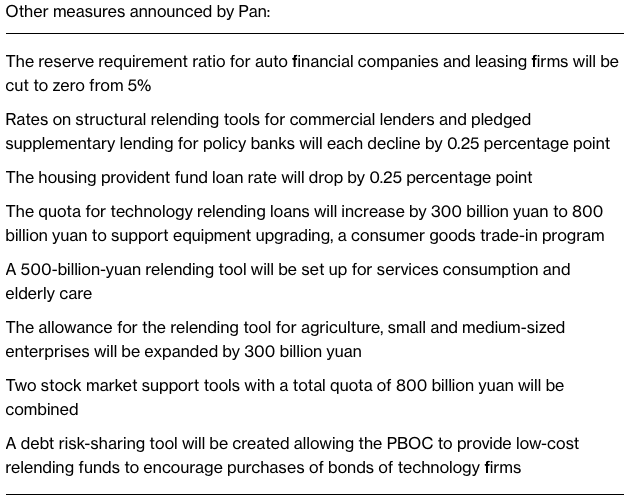

Meanwhile, China has quietly enacted 10 new policy measures, including a cut to the 7-day reverse repo rate and a 50bps reduction in reserve requirements. That’s a clear signal that Chinese policymakers are easing preemptively before any hard data shock manifests.

Safe Havens Softening, but Still Relevant

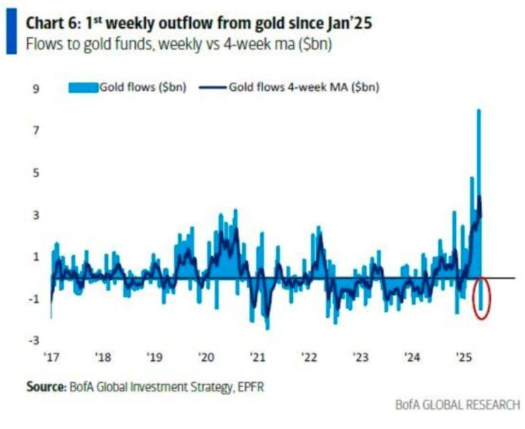

Gold saw outflows for the first time in weeks, and Silver continues to underperform. That said, with deflationary pressure lurking from Chinese oversupply and geopolitical tail risks simmering, the safe haven trade isn’t dead, just subdued.

Positioning Risk: The Pain Trade Is Higher

The biggest tell of the week? The short base is thinning. Tactical shorts got blown out on the gap-up after the US-China reprieve. Now the same desks that warned about valuation excess are scrambling to re-enter the market at higher prices.

When the pain trade is up, underperformance becomes its own risk. If key macro deals (EU, China) materialize, there’s scope for further chases—especially in semis, tech, and AI leadership sectors.

Sector Rotation: Chips, Tech, and Cyclicals

Semiconductors (SMH) and XLK have led the rally—and for good reason. With Trump's team signaling a rollback of Biden’s Chips Act restrictions,regulatory clouds are lifting. The market likes that.

Also, the Chips Act has quietly flipped from an earnings drag to a sentiment tailwind. Combined with strong seasonals and improving guidance, the tech leadership remains structurally intact—for now.

Yield Curve & Dollar Moves: A Quiet Warning?

The US 30Y yield is pushing toward 5%, and yet equities remain unfazed. That divergence won’t last forever. If bond yields break higher, expect risk assets to reassess quickly, unless it is genuine growth with moderate inflation.

At the same time, the DXY has broken its 20-day moving average, forming an inverse H&S pattern that signals more dollar strength ahead—particularly if Europe and China data undershoot.

Last Week’s Recap: What Moved the Needle

FOMC Shock

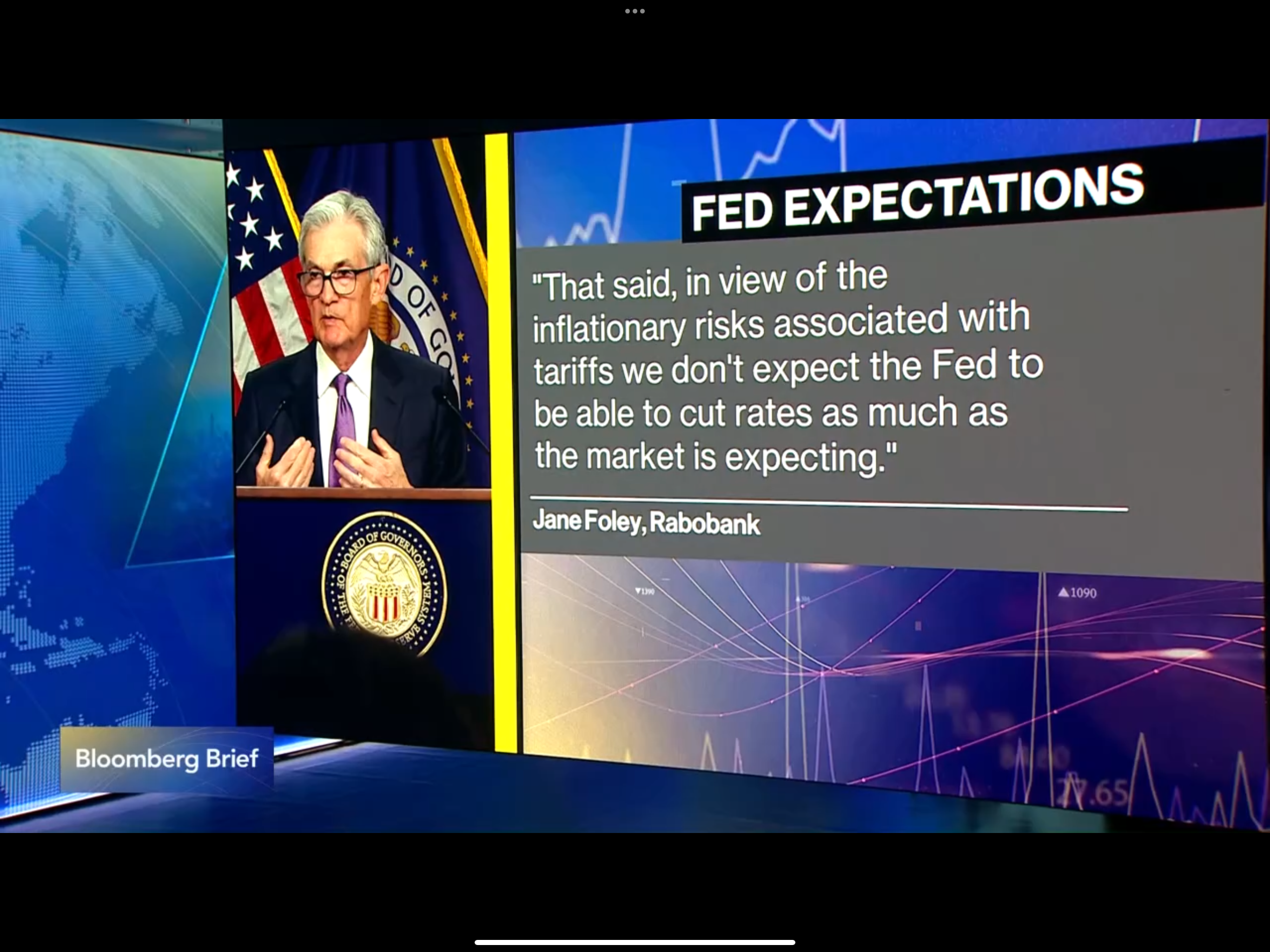

Powell further removed the Fed PUT focused on STAGFLATION and June fell off the rate cut list.

UK Trade Deals

Quickly followed India deal with the US one. Already a trade surplus for the US but Trump used as an example for good behaviours

USD Trade

Showed mega front-loading imports

China PBOC

Rate cuts part of 10 Monetary policy boosts

Earnings

Tech showed cracks at ARM, SMCR and Marvell on China market concerns. Is the market topping fears surfaced

US Chips Act

Trump looking to ditch Biden’s dud and light the fireworks

Geopolitics

South Asian tensions flared with India and Pakistan squabbling. Initially underpinned gold but it saw its first weekly outflow.

The Week Ahead: Buckle Up for Event Risk

Must-Watch Events

US CPI (Tues)

Was much awaited until the China 90day truce…any blips up will be seen as short term

JPY PPI (Wed)

Any pressure for the inputs side of supply. BOJ already downgraded economic outlook

OPEC Monthly Report (Wed)

Will they have factored in the China deal improvement on tariffs for end demand?

US Retail Sales (Thurs)

A critical read on consumer resilience; should be positive with front loading demand high

UK and EZ GDP (Thurs)

Both Central banks have downgraded growth will it show up here or be ignored now anyway

CHF PPI (Thurs)

Already seeing negative rates at the front end

JPY GDP (Fri)

Will it confirm the BOJ concerns

USD Michigan Surveys (Fri)

All about whether consumers picked up on the China mood music in the survey period…if not it will in two weeks time…Soft data about to firm up

Actionable Takeaway: Trade the Tape, Not the Narrative

The market looked like it was running on fumes—short vix trades removed anticipating renewed volatility, soft landing hopes but rate cut dreams in tatters post FOMC, PBOC providing liquidity support in abundance and the Fed supporting bond market auctions. Technicals were flashing warnings, and macro risks were resurfacing. BUT the US and China decided enough was enough. Big reverse engine on Facts change:

Equities Forecast

SPX new high for the rally, pro money needs to address downside tail removal, bias is pullbacks will be bought and a risk on period ahead.

FX Setup

Dollar bid short term on capital flows coming back to the US. CPI may reveal tariff fears this week but will be seen as transitory/temporary. Safe-haven flows likely to see unwinds.

Commodities Watch

Gold and oil seeing geopolitics tension ease and risk on flows ease safe have demand. Inflation may rear its head this week and OPEC + EIA outlooks on Oil may have to factor in the China positives. Oil should retest the supply zone above at least

Macro Trends to Watch

US inflation trajectory and consumer spending resilience, China demand, central bank policy is liquidity + = risk on. US headlines from the Middle East. International money flow, does it continue back to the US?