Inflation Pressures Re-Emerge Beneath the AI Rally, Bond Markets Begin Testing the Market’s Comfort Zone

Markets continue consolidating recent gains, but the character of the move increasingly reflects an environment where inflation and rates are beginning to matter again. Strong earnings revisions, resilient US growth data, and continued participation in AI-linked leadership continue supporting equities, even as bond yields and inflation-sensitive assets start creating more friction underneath the surface.

At the same time, cross-asset relationships are becoming increasingly important. Oil, yields, currencies, and risk assets are reacting more tightly together as geopolitical uncertainty and inflation pressures continue feeding through the broader macro environment. The result is a market that remains constructive overall, but one becoming progressively more sensitive to rate stability and funding conditions.

Market Overview: Earnings Momentum Continues Supporting Equities

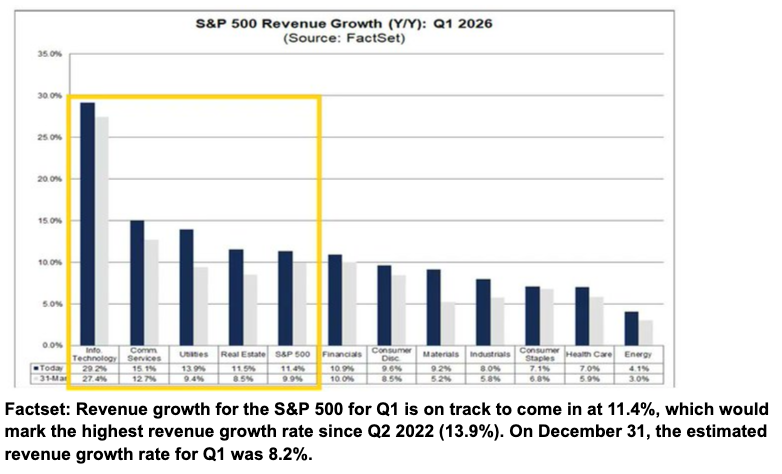

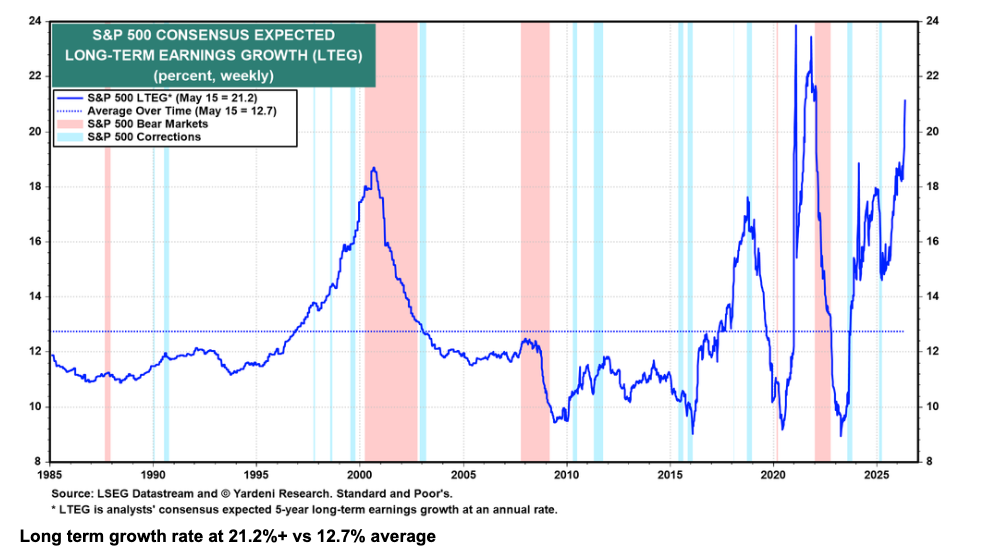

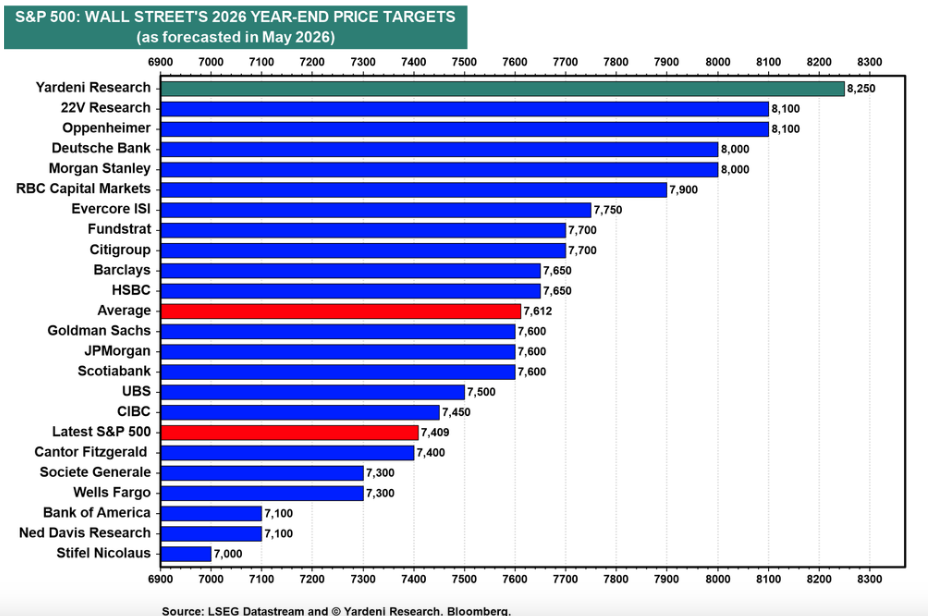

Equities remain supported by a strong earnings backdrop, with forward expectations and revenue growth estimates continuing to move higher across the S&P 500. The broader move higher continues reflecting improving fundamentals rather than pure multiple expansion, while earnings breadth itself also remains healthy beneath the surface despite concentration concerns around AI leadership.

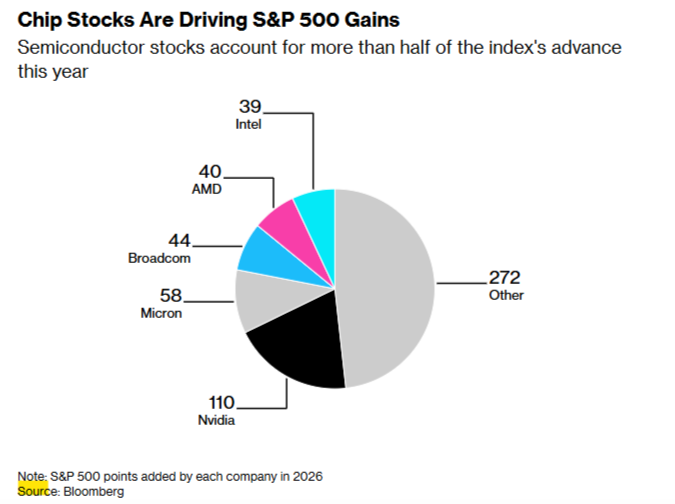

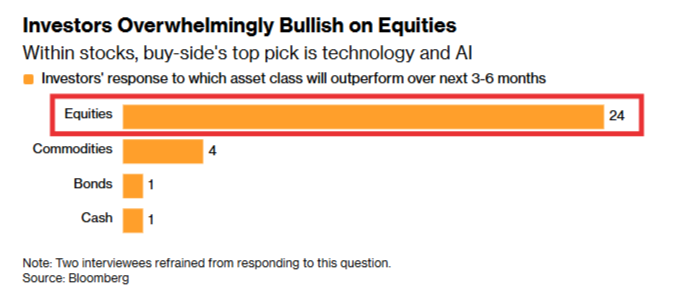

Technology, semiconductors, and AI-linked infrastructure continue dominating broader market performance. Institutions and retail investors continue supporting equity exposure, while many hedge funds remain comparatively cautious, preferring to avoid downside risk rather than aggressively chase upside at current levels.

The report repeatedly highlights that the market is increasingly balancing two competing narratives simultaneously. On one side, earnings momentum and nominal growth remain supportive. On the other hand, inflation pressures and rising yields are beginning to tighten financial conditions again.

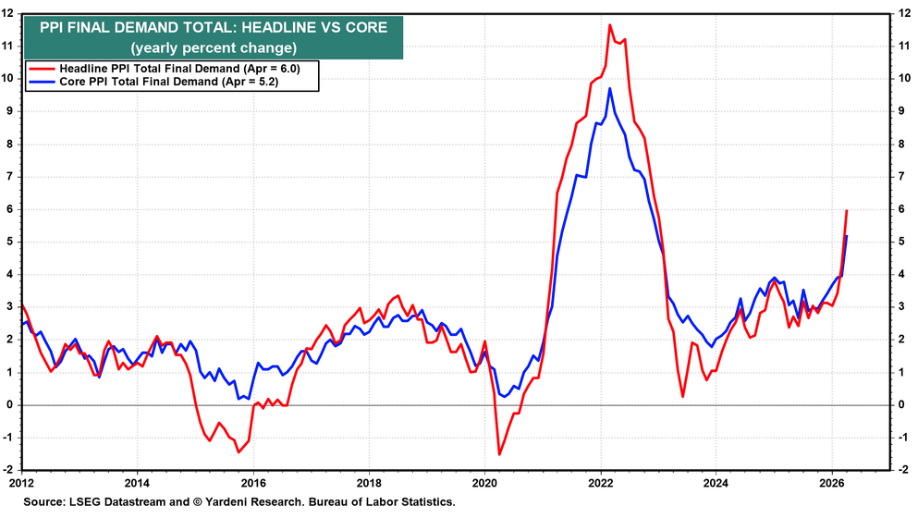

Producer prices accelerated during the week, while freight costs and electricity prices also moved higher, reinforcing concerns that inflation pressures may be broadening beneath the surface.

Overall, the broader structure remains constructive, but the market environment is becoming progressively more dependent on rate stability and continued earnings delivery.

Macro & Policy Watch: Geopolitical Stress, Inflation Echoes, and Rising Yield Pressure

Geopolitical developments remained central to the broader macro backdrop throughout the week. The report repeatedly highlights that the longer the conflict environment persists, the more inflationary pressure appears to be feeding through energy markets, transportation costs, and broader funding conditions globally.

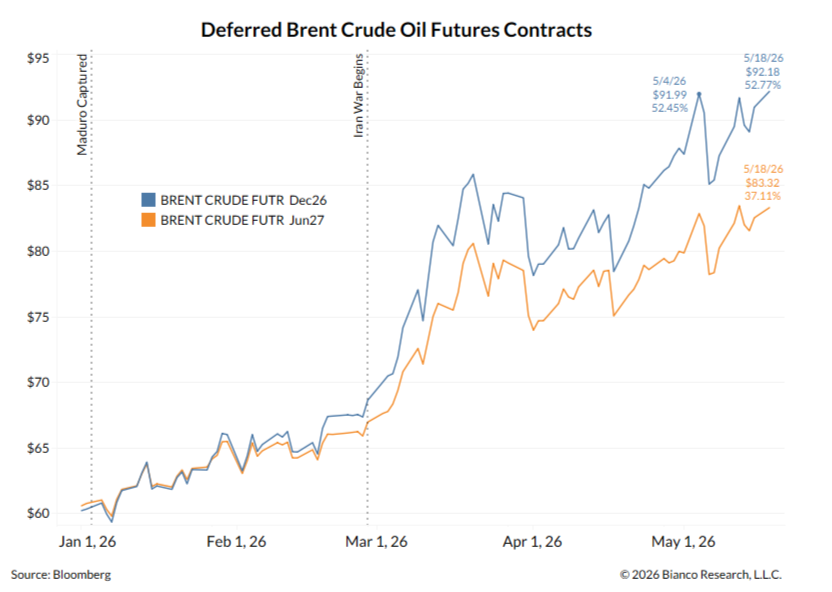

Oil markets increasingly reflect this tension as futures pricing continues adjusting closer toward spot markets. Energy markets remain central to the inflation discussion as geopolitical instability continues shaping supply expectations and inflation-sensitive positioning.

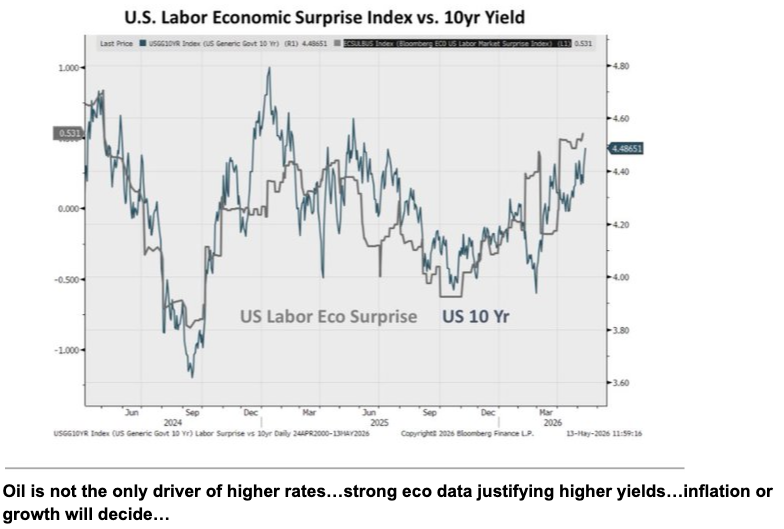

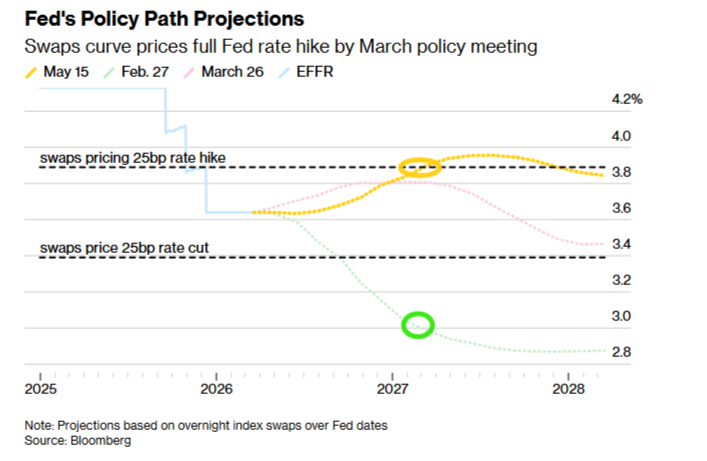

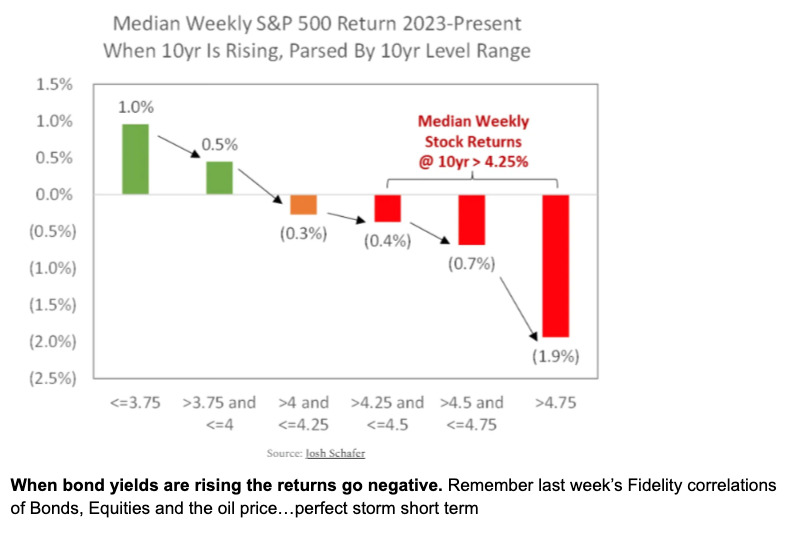

At the same time, bond markets are beginning to reassert themselves as the market’s primary stress point. US interest-rate futures increasingly reflect the probability of another Fed hike, while long-duration Treasury yields moved sharply higher during the week.

The report repeatedly emphasises that rising yields are becoming increasingly important for broader risk appetite, particularly as governments continue managing elevated funding requirements alongside persistent inflation pressure.

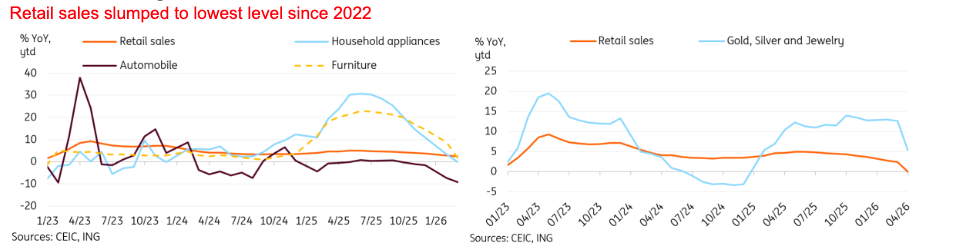

Meanwhile, China’s macro backdrop weakened across several areas during the week. Retail sales, industrial production, and fixed asset investment all disappointed, reinforcing concerns around slowing domestic momentum despite resilient export activity.

Currency markets also continued to favour higher-yielding and energy-linked exposures as inflation and geopolitical concerns remained elevated globally.

Technical & Sentiment Breakdown: Supportive, but Increasingly Fragile

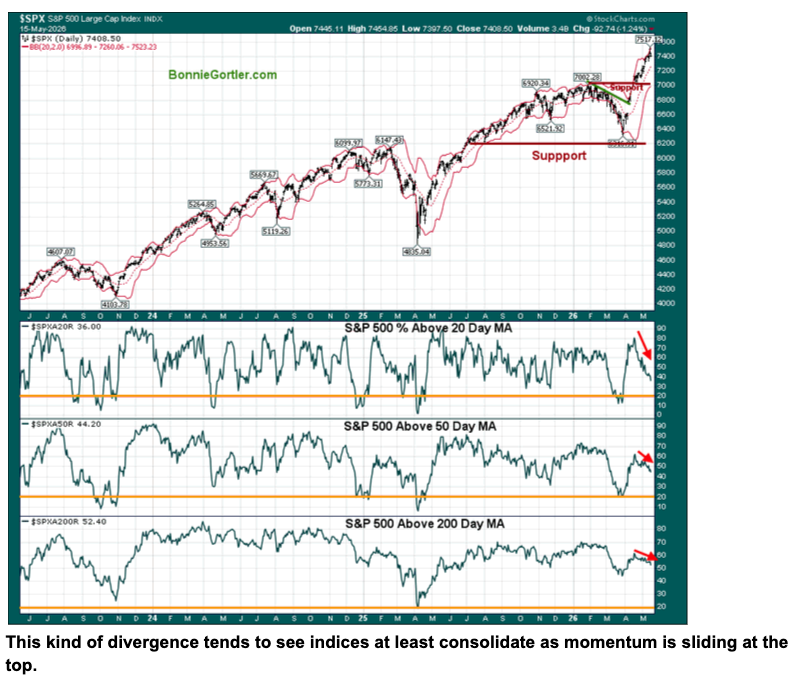

The broader technical structure remains supportive, with major indices continuing to hold near highs while AI-linked leadership remains dominant across the market.

At the same time, however, market breadth continues deteriorating underneath the surface. Participation remains increasingly concentrated around a relatively small group of mega-cap technology and semiconductor leaders.

The report repeatedly pushes back against immediate bubble comparisons, highlighting that earnings momentum and corporate profitability remain significantly stronger than during previous speculative cycles. However, positioning and sentiment conditions continue to become increasingly crowded.

Cross-asset relationships are also becoming increasingly important. Bond yields and equities remain highly correlated in the current environment, reinforcing the idea that rate stability may become the single most important variable for risk assets moving forward.

Meanwhile, the market continues strongly rewarding companies aggressively investing in capex and R&D rather than prioritising buybacks, reinforcing the broader AI infrastructure and growth-investment narrative underneath the rally.

Overall, trend conditions remain constructive, but the internal quality of the move is becoming increasingly dependent on yields, positioning, and continued earnings momentum.

Last Week’s Recap: Rising Inflation Concerns Meet Relentless Earnings Momentum

The past week reflected a market still supported by strong earnings revisions and resilient growth conditions, while inflation pressures and bond-market volatility increasingly began shaping broader macro behaviour underneath the surface.

Key Highlights:

- Macro:

Producer prices accelerated during the week while inflation-sensitive inputs continued moving higher, reinforcing concerns that inflation pressures may be broadening beyond energy markets alone. At the same time, retail sales and GDP-related data remained resilient, continuing to support the broader nominal growth backdrop.

- China:

Chinese data disappointed broadly across retail sales, industrial production, and fixed asset investment. Concerns around slowing domestic momentum continued building as markets increasingly focused on weaker internal demand conditions.

- Earnings:

Earnings momentum remained one of the strongest supports for equities, with technology and communication services continuing to lead broader revenue growth expectations. Earnings breadth also remained healthy despite increasing concentration around AI leadership.

- Commodities:

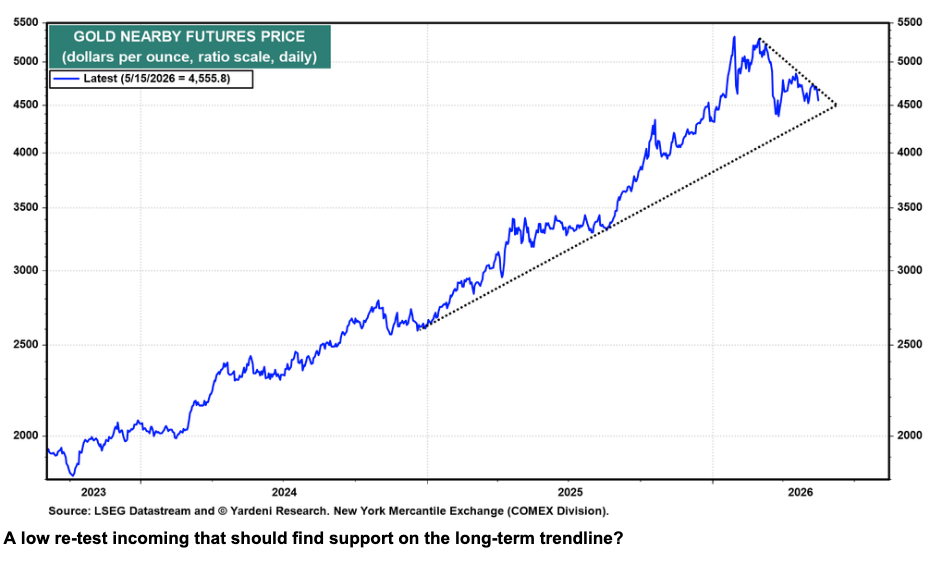

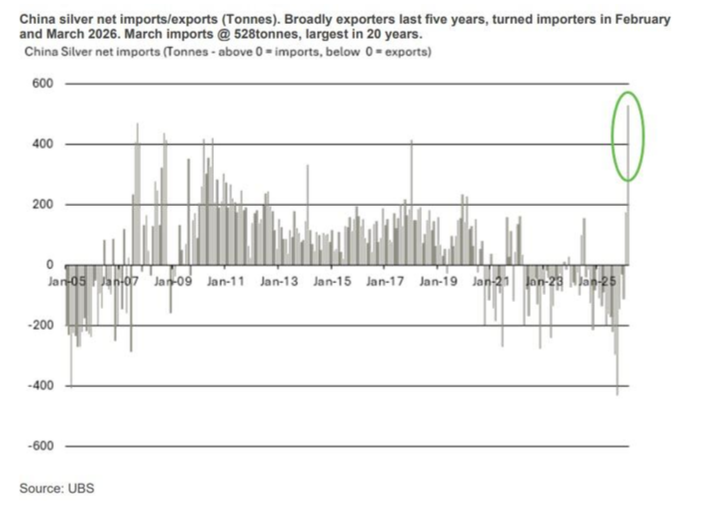

Precious metals continued reacting to inflation expectations, geopolitical instability, and real-rate dynamics. Gold remained supported by central-bank demand and monetary inflation concerns against price inflation and higher rates competition, while silver continued benefiting from supply deficits and investment demand.

- Crypto:

Crypto markets experienced deleveraging pressure during the broader risk-off move as leveraged long positioning was reduced. Despite volatility, broader positioning continued reflecting consolidation rather than structural breakdown.

- Oil:

Oil remained central to the broader macro narrative as futures markets increasingly adjusted toward spot pricing amid persistent geopolitical uncertainty and inflation-sensitive positioning.

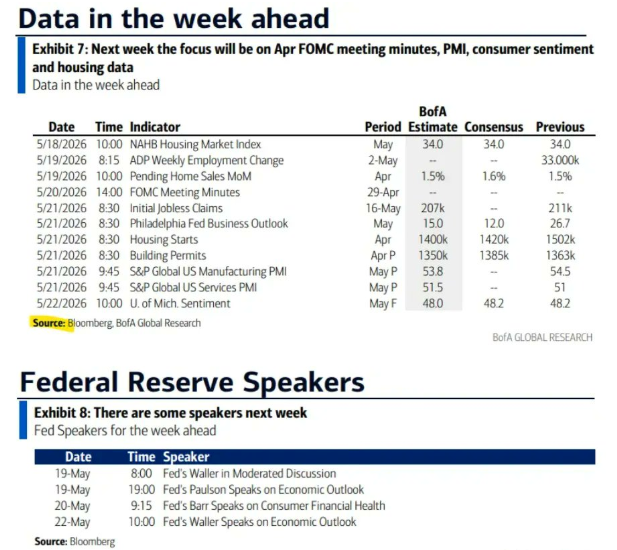

The Week Ahead: Key Data and Market-Moving Signals

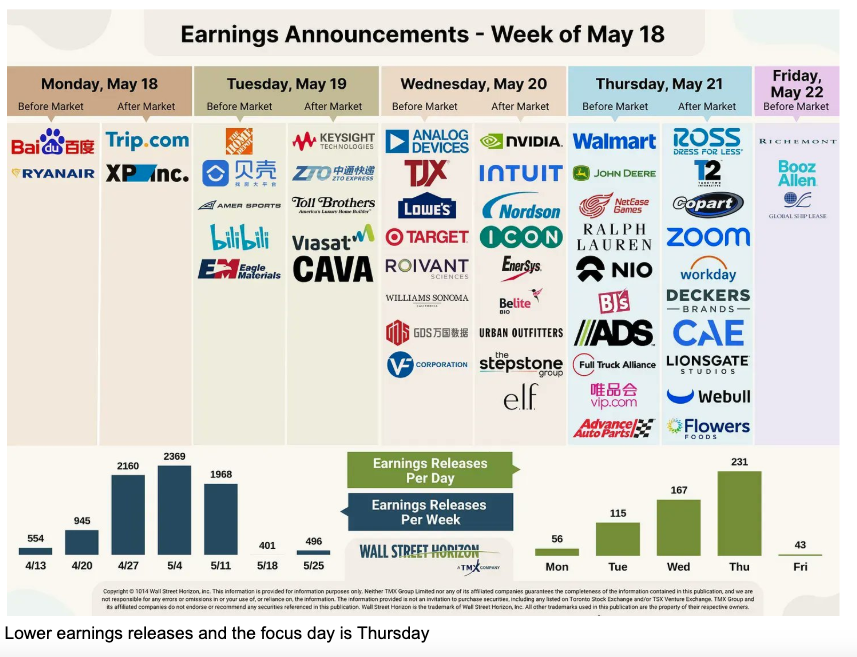

The week ahead remains focused on inflation, growth, and rate sensitivity, with global PPI releases, PMIs, sovereign yields, and Nvidia earnings expected to remain central for broader market positioning. Wednesday stands out as the key inflation day globally following last week’s strong US producer price print, while Nvidia and Walmart earnings will remain important for AI leadership and consumer sentiment expectations.

Monday, May 18

• China: Retail Sales, Industrial Production, Fixed Asset Investment, and House Prices

• China: NBS Press Conference

• US: NAHB Housing Market Index

• US: TIC Flows and Foreign Buying Data

• Japan: 5-Year JGB Auction

• UK: BoE MPC Member Mann Speaks

• Germany: Bundesbank Monthly Report

Tuesday, May 19

• Japan: Q1 GDP Data

• UK: Employment Data and Wage Growth

• US: ADP Employment Change

• Canada: CPI and Core CPI Data

• US: API Weekly Crude Oil Inventories

• US: Fed Waller Speaks

Wednesday, May 20

• China: Loan Prime Rate Decisions

• UK: CPI, Core CPI, and PPI Inflation Data

• Germany: German PPI

• Eurozone: CPI and Core CPI

• US: Crude Oil Inventories

• US: FOMC Meeting Minutes

• US: Nvidia Earnings

Thursday, May 21

• Australia: Employment Data

• Japan: PMI Data

• Eurozone: Manufacturing and Services PMIs

• UK: Manufacturing and Services PMIs

• US: Initial Jobless Claims

• US: Philadelphia Fed Manufacturing Index

• US: Housing Starts and Building Permits

• US: S&P Global Manufacturing and Services PMIs

• US: Atlanta Fed GDPNow Update

• US: Walmart Earnings

Friday, May 22

• Japan: National CPI Data

• Germany: GDP and Ifo Business Climate Data

• UK: Retail Sales

• Canada: Retail Sales Data

• US: Michigan Consumer Sentiment and Inflation Expectations

• US: Leading Economic Index

• US: Fed Waller Speaks

Alpha Takeaway: Earnings Strength Continues, While Bond Markets Tighten the Margin for Error

Markets remain supported by strong earnings momentum, resilient nominal growth, and continued participation in AI-linked leadership. Earnings revisions and investment flows continue supporting the broader trend even as macro conditions become increasingly layered underneath the surface.

- Equities:

Equities continue benefiting from strong earnings breadth, AI-linked investment flows, and resilient growth expectations, although rising yields and increasingly narrow leadership remain important risks to monitor. NVIDIA on Weds night effectively concludes Q1 earnings season and perhaps the last short term catalyst into the Holiday weekend

- Gold & Silver:

Precious metals continue reflecting broader inflation, real-rate, and geopolitical dynamics. Structural demand conditions remain supportive, though short-term direction continues reacting closely to movements in yields.

- Crypto:

Crypto continues behaving as a higher-beta liquidity and risk asset, with recent volatility reflecting deleveraging and positioning adjustments rather than broader structural weakness.

- Macro:

Inflation pressures, rising bond yields, geopolitical instability, and increasingly tight cross-asset correlations continue shaping the broader macro environment and influencing positioning across asset classes.

The broader trend remains constructive, but the market increasingly appears more sensitive to rates, inflation, and positioning conditions beneath the surface. Momentum remains supportive, though the environment underneath is becoming progressively more fragile and increasingly dependent on stability across bond markets. The odds of an end to the war lessen but the Bond market is at previous Trump TACO levels…markets are overdue a pause but beware the Truth Social Put trade if things became ugly in the rates market…tight stop losses!