Moody’s Cuts, Bond Market Shifts, and the Liquidity Mirage: Can the Rally Hold?

Markets hit a wall as Moody’s strips the U.S. of its final AAA rating, Trump’s tax bill faces internal fire, and semis signal exhaustion. Volatility is creeping back, macro clarity is fading, and traders are left navigating a deeply uncertain setup. This week brings a lighter macro calendar, but the aftershocks from last week are just beginning.

Market Overview: “Sentiment Led the Rally—Now Data Must Defend It”

The market came into last week high on hope—China de-escalated, Middle East diplomacy stole headlines, and the Trump Put looked alive and well. But behind the optimism, cracks are forming.

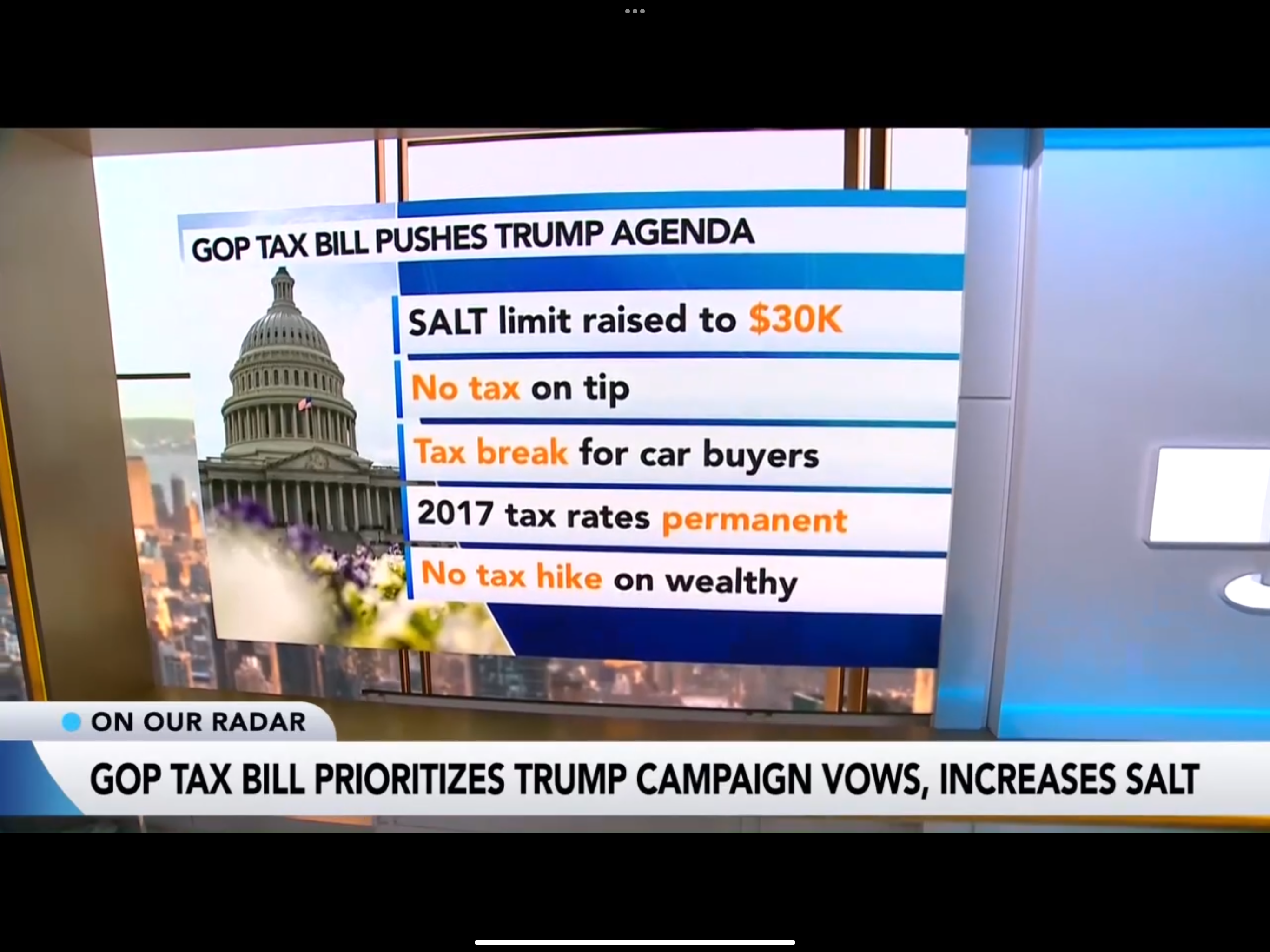

Moody’s downgrade of U.S. credit to Aa1 on Friday was more than symbolic. It confirmed what bond vigilantes have already been pricing in: that deficits are spiralling, and Washington is asleep at the wheel. That downgrade landed just as Trump’s blockbuster tax bill hit friction, with conservatives baulking over cost and timing.

“Moody’s isn’t a friend of Trump, and the timing is no accident. A mid-debate downgrade is a political blow and a market risk.”

Meanwhile, markets reversed right after Friday’s options expiry, a classic rug-pull, leaving gaps open and gamma support stripped away.

Buffett hoarding cash, Burry shorting, Trump spinning—this sums up sentiment.

the actor

Key Sentiment Signals

- Moody’s joins Fitch and S&P in downgrading U.S. credit

- Trump’s tax bill faces internal GOP resistance

- The volatility bubble popped in the final 15 minutes on Friday

- Burry exits stocks, loads puts—volume spikes at highs

- Treasury short interest surging—were big players front-running the downgrade?

- VIX saw 6 consecutive weeks down—until last week

- Retail continues to pile into 3x/5x ETFs—classic late-cycle pattern

Macro & Policy Watch: Debt, Politics, and the End of Forecast Certainty

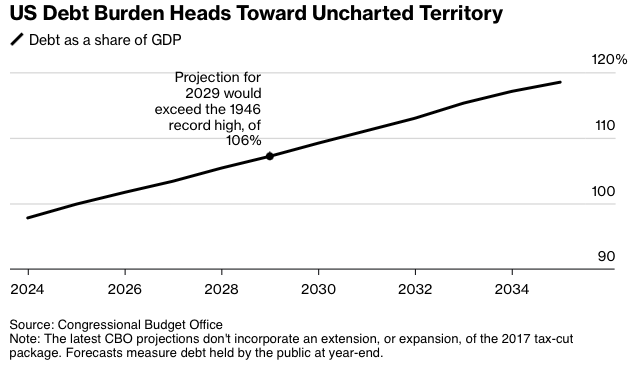

Moody’s Downgrade: America’s Last AAA Falls

Moody’s cited “the decline in fiscal metrics” and the unrelenting rise in U.S. debt and deficits. Their downgrade came with a stable outlook, but the message is clear: the U.S. is not immune to debt math.

Lawmakers are trying to extend parts of the 2017 tax cuts, costing $3.8 trillion over a decade. Even Trump loyalists blocked the bill Friday, citing cost. The pressure is mounting.

“The downgrade reflects not just policy failure, but structural market concerns. Borrowing costs are heading higher.”

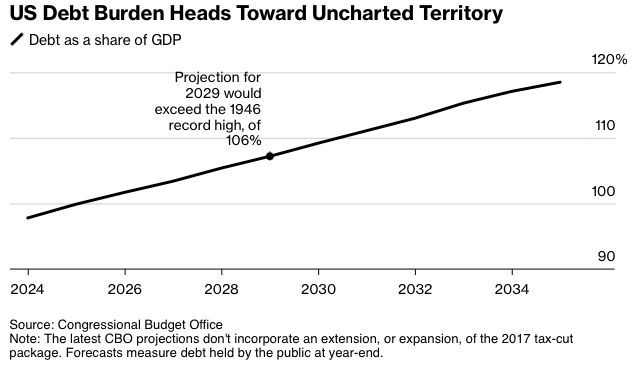

US debt burden projection

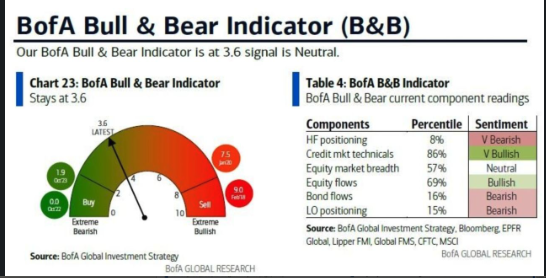

BOA Bull Bear

Central Banks Abandon the Forecast Compass

Both the Fed and the Bank of England are dropping traditional forecast-based signalling. Powell admitted that post-GFC frameworks don’t apply anymore. The BoE’s Andrew Bailey confirmed that baseline projections will now come alongside scenario alternaFtives—an admission that economic models are failing under repeated supply shocks.

Bernanke’s policy review is influencing this shift, but the result is less clarity for markets.

“The Fed is guiding without a map. The BoE just tore up the old one.”

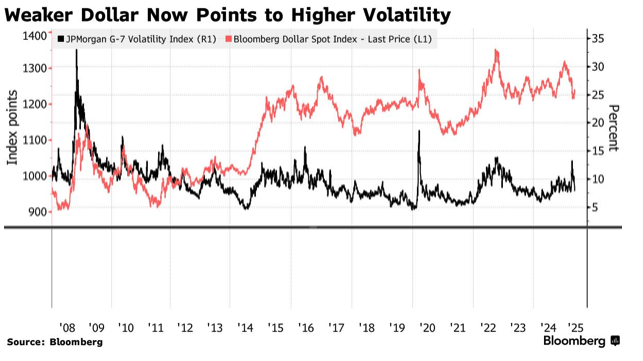

Dollar Wobble: From Safe Haven to Warning Signal

The weak dollar, once a sign of risk-on flows, is now being read as capital flight. Treasury auctions are once again being quietly supported by the Fed. That’s QE in all but name.

“QT may be slowing, and nobody’s admitting it. If that’s true, this rally was liquidity-driven, not fundamentals-based.”

Weaker dollar volatility cost higher

Technical & Sentiment Setups: Rally Stretched, Risks Rising

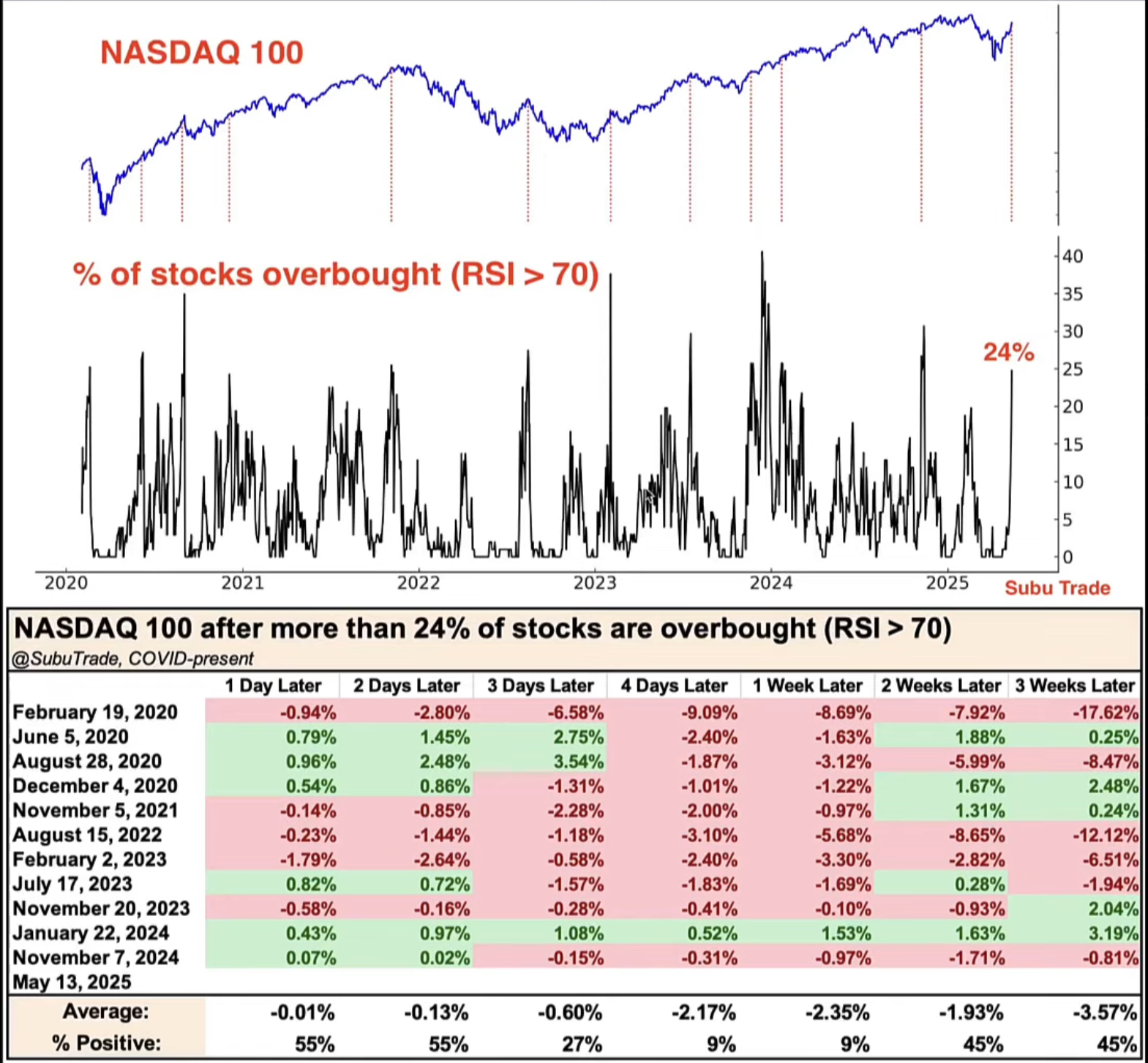

Semis, SPX, Nasdaq—Signs of Exhaustion

Volume surged last week near the top of the recent rally, especially in QQQ, SPY and NDAQ. The SMH/SPY ratio rolled over. Semis are no longer leading. Nasdaq has printed a wedge top, and SPX has opened gaps with no gamma support below.

“High volume at resistance is rarely bullish—especially when hedges are gone and retail is leveraged.”

Leveraged Retail, Bearish Hedge Funds—Classic Pain Setup

Hedge fund positioning remains bearish, but retail is doubling down via leveraged ETFs. This is exactly what happened before the last blow-off tops in 2021 and 2018.

“The most dangerous place to be is comfortably long into a leveraged retail rally with no gamma floor.”

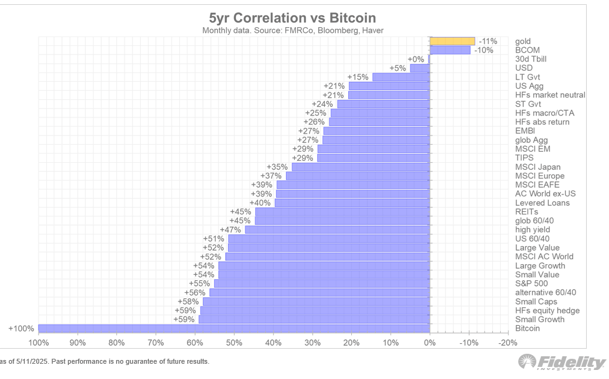

Gold & BTC: Ready for a Store-of-Value Rotation?

Gold has bounced from the buy zone mentioned last week. BTC is consolidating after outperforming. The disconnect between the two may resolve, especially if the dollar sees another wobble.

Last Week in Review: China Starts It, Moody’s Ends It

China De-escalates, Retail Cheers, Bond Markets Frown

The week started with optimism as China agreed to de-escalate tariffs, reducing barriers and agreeing to crack down on fentanyl. Trump called it historic. But Friday’s downgrade stripped away the sugar-coating.

Key Data Recap: Signs of Cooling

CPI: Flat headline, but core shelter still rose—airfares, insurance, and used cars fell

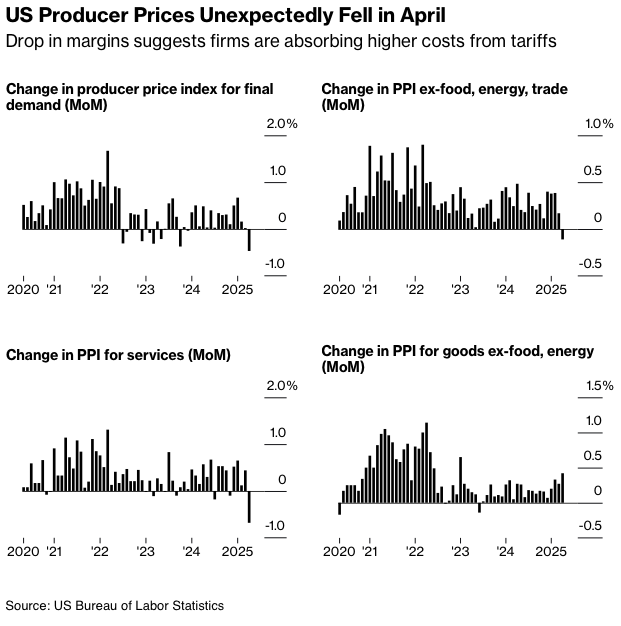

PPI: Negative surprise—monthly deflation hints at margin stress

Imports: Ex-fuel imports rose 0.8% MoM—re-stocking or demand?

Retail Inventories: Still front-loaded—upside risk to Q2 GDP?

“Disinflation, not inflation. But cracks are forming in margins, not prices.”

The Week Ahead: Light Calendar, Heavy Implications

Monday, May 19

China's retail sales, industrial production, and fixed investment

Eurozone final CPI

Trump-Putin call + Tax bill signing attempt

FOMC speakers (Williams, Bostic, Logan, Kashkari, Jefferson)

USD auctions: 3m, 6m Bills

Earnings: Trip.com , Ryanair, Naturgy Energy

Tuesday, May 20

China Loan Prime Rate (expected cut)

RBA Rate Decision (cut expected)

CAD CPI, EZ Consumer Confidence

FOMC Barkin, Bostic, Collins

Earnings: Palo Alto, Home Depot, Vodafone, Toll Bros

Wednesday, May 21

UK CPI

German 10Y Bund auction

US 20Y Bond auction

JPY & NZ trade balances

Earnings: Target, Lowe’s, TJX, Zoom, Baidu, Medtronic

Thursday, May 22

Global Flash PMIs: US, UK, EZ, Japan

US 10Y TIPS auction

US Jobless Claims, Existing Home Sales

Earnings: Ross Stores, Intuit, Analogue Devices

Friday, May 23

GBP Retail Sales, GfK Consumer Sentiment

EZ Trade Balance

US New Home Sales, Building Permits

CAD Retail Sales

JPY CPI

Alpha Takeaway: Wait for the Fall or the Follow-Through

Markets may be at an inflexion. If bulls can hold the line, the ingredients for a gamma squeeze are there. But without clear data support and amid massive policy uncertainty, any bounce could be short-lived.

“This market has gaps below, no hedges, and retail is overleveraged. If you're long, you're betting on political miracles.”

Here’s What to Track

- Watch SPX 5900—break it, and the structure turns bearish

- If bulls defend this week’s gaps, a June gamma squeeze is in play

- BTC and Gold may start moving in sync, especially if dollar weakness accelerates

- TIPS auction on Thursday could shake inflation narratives

- Treasury yields are still climbing—watch bank appetite and foreign demand