Tariff Tensions, Bond Blowouts, and Breadth Breakdown: The Calm Is a Trap

Markets limped into Memorial Day weekend with Trump firing trade threats, bonds buckling under supply pressure, and equity breadth flashing red. The short-term calm masks unresolved risks: global bond tantrums, capital flight from the dollar, and a rally losing internal momentum. This week brings NVIDIA earnings and crucial inflation reads, with traders on edge.

Market Overview: “The Orange One Returns. So Does Vol.”

Memorial Day began with Trump threatening Apple with 25% tariffs unless it manufactures in the U.S., alongside a 50% tariff on EU imports from June 1st. By Sunday night, he backed off, delaying the EU action to July 9th, triggering a 1% futures pop. But Asia still closed lower, and U.S. markets remain stuck in a loop of headline roulette.

Trump’s volatile antics are losing their bite, but not without damage. Institutions are maintaining underweight risk exposure, steering away from USD and U.S. bonds. The broader takeaway? Globalisation is being replaced by segmentation, and the market narrative has moved decisively toward medium-term inflation pressureand capital realignment.

Despite short-term rallies, underlying market participation is weak:

- Just 12.1% of S&P 500 stocks are above their 5DMA

- 337 S&P stocks hit new lows vs just 19 new highs last week

- Russell 1000: 688 new lows vs 40 new highs

- Even the Nasdaq 100—hovering near all-time highs—posted a net-61 in new highs vs lows. Breadth is worse than it looks. The rally has narrowed, and historically, this kind of deterioration precedes major risk-off moves.

Macro & Policy Watch: Bond Yields Won’t Blink

The Big Bill Passes, But So Do Big Worries

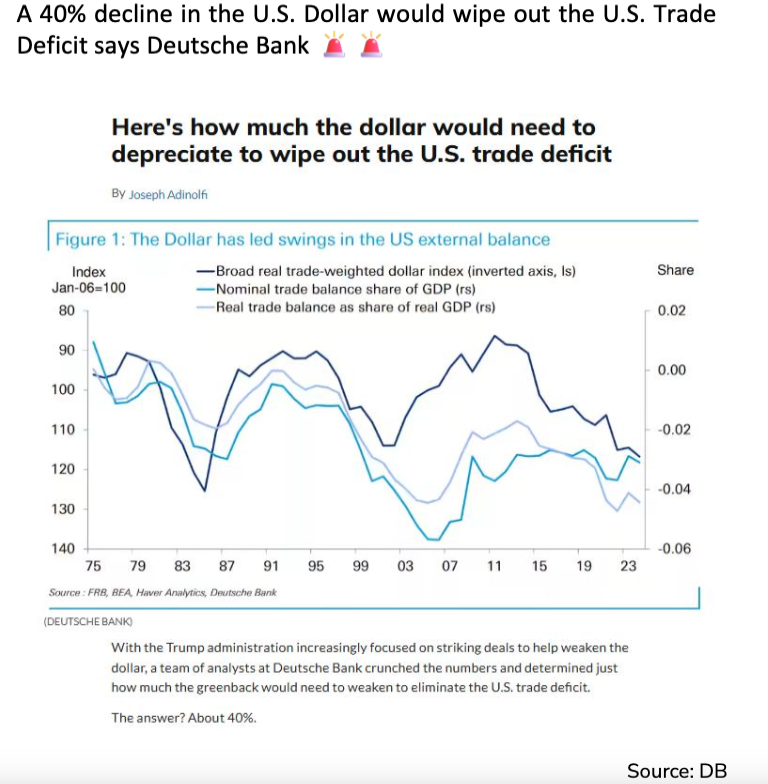

Trump's tax bill passed the House, but not without serious dissent. The Senate will likely soften it, but it’s already filled with long-term fiscal risks. As Bessent admitted, “We’re going for growth to fix the deficit.” Translation? Print money, suppress yields, or devalue the dollar by 40% to shrink the debt-to-GDP ratio.

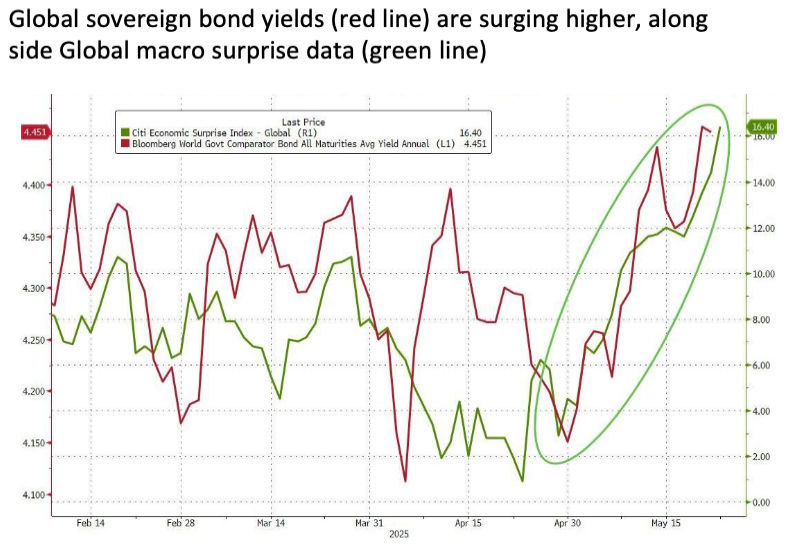

This fiscal pivot comes just as long bonds throw a tantrum. The 20Y auction midweek was brutal, with yields hitting 5.1%, a level not seen since 2007.

And it’s not just the U.S. :

- Japanese yields are surging, threatening a capital repatriation wave

- Foreign inflows are drying up just as the U.S. ramps up issuance

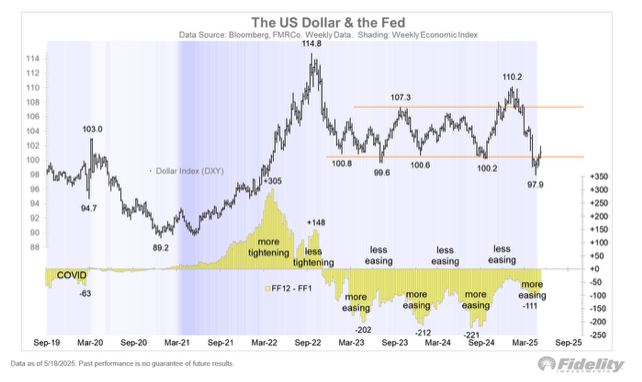

The dollar, meanwhile, isn’t trading on rate differentials—it’s trading on capital flows and fiscal credibility. Waller offered a hint: if tariffs stay capped at 10%, the Fed could ease. But if chaos drags into late summer, all bets are off.

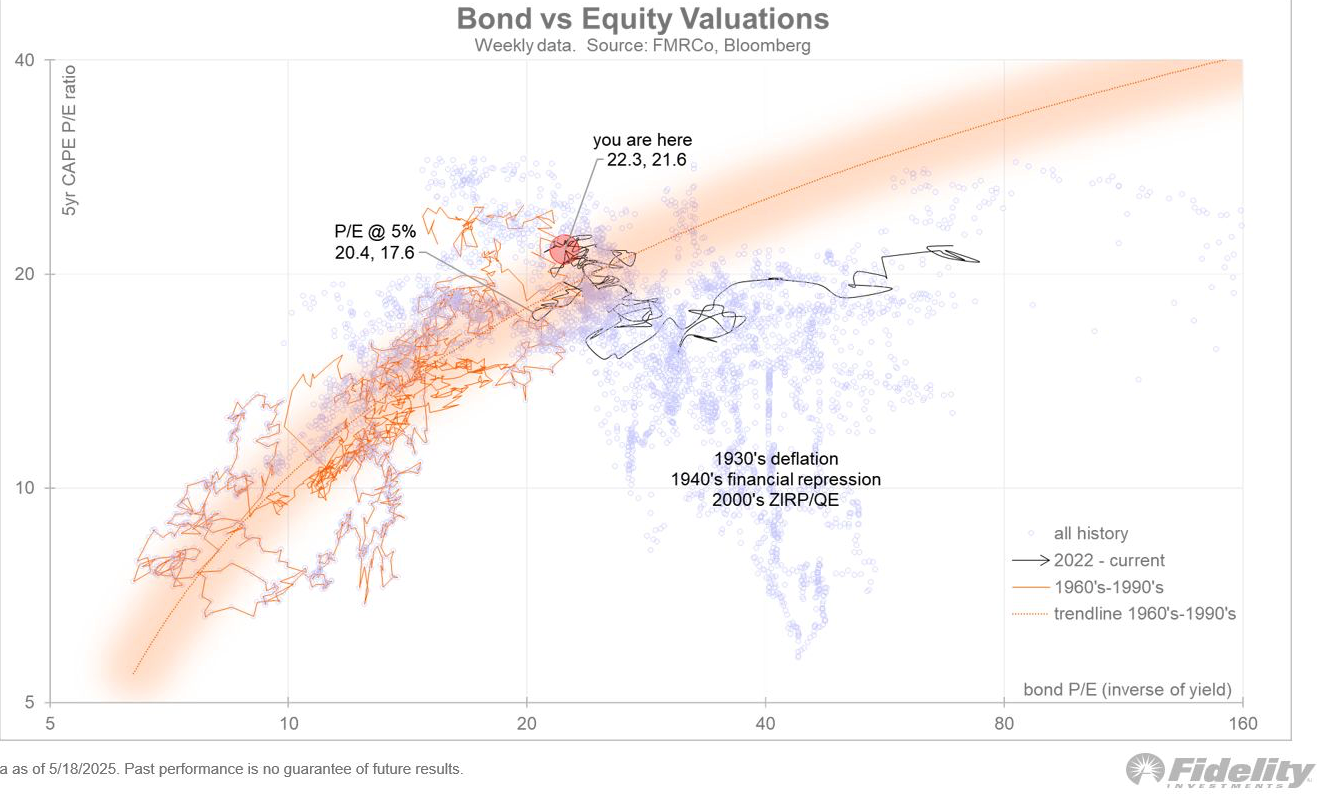

“5% long bond yields are the new line in the sand. The market is deciding, not the Fed.”

Technical & Sentiment Setups: Rally Has No Legs

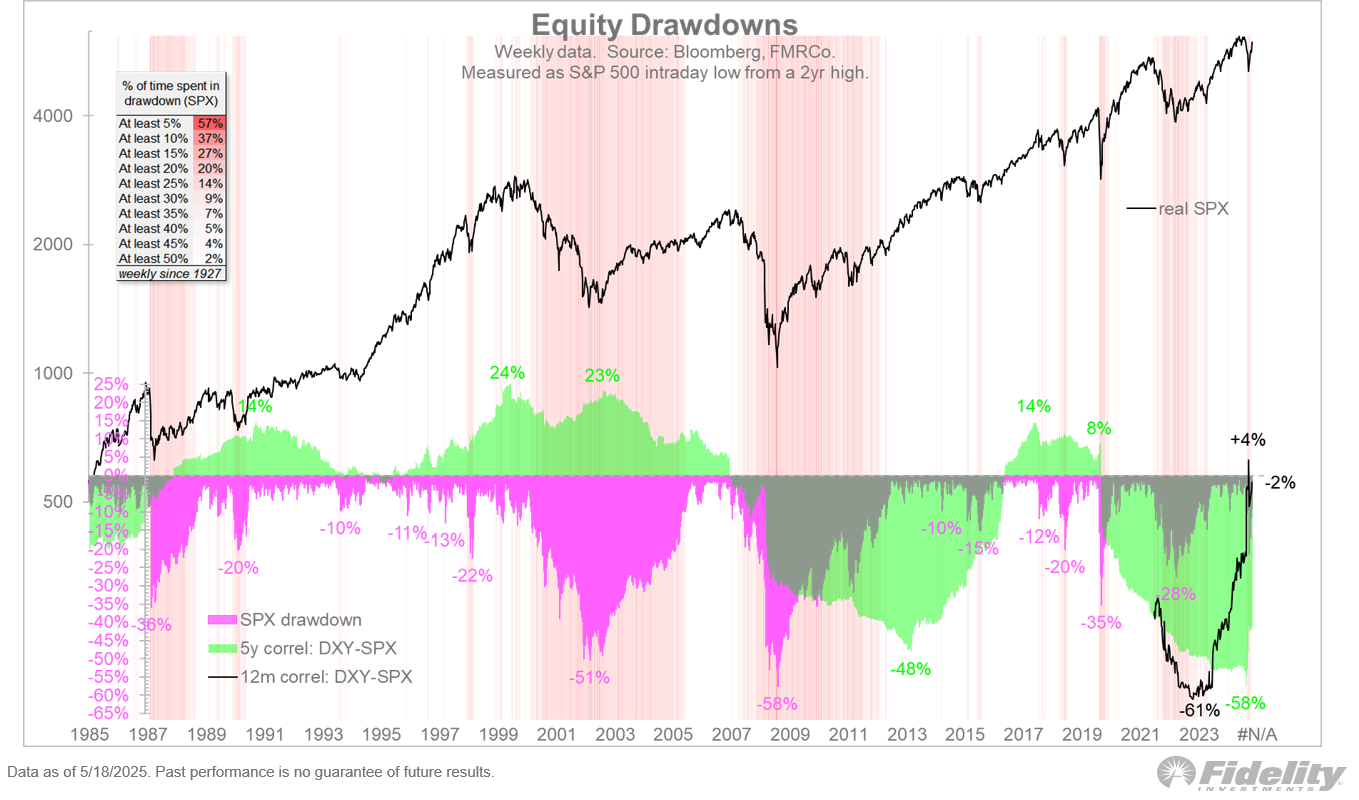

Markets are near highs, but momentum is rotten. Short-term breadth has cratered, and institutional hedges are stacking up. That’s a classic bull trap setup.

- Only 18.8% of Nasdaq stocks are above 5DMA

- SPX P/E multiples under pressure from rising 5%+ yields

- Bear ETF flows dwarf bullish flows in both size and quality

Breadth isn’t just weak—it’s deteriorating faster than index watchers realise. This realises the same internal setup that led to the 2018 Q4 and 2022 mid-cycle rug pulls.

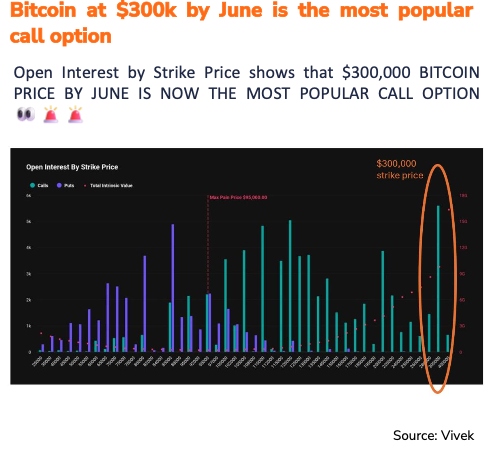

Gold and Bitcoin are soaking up safe-haven flows. BTC tagged a new ATH at $111K and chatter o,f $300K targets is growing.

Last Week in Review: Trump, Tariffs & Tech Divergence

Macro Recap

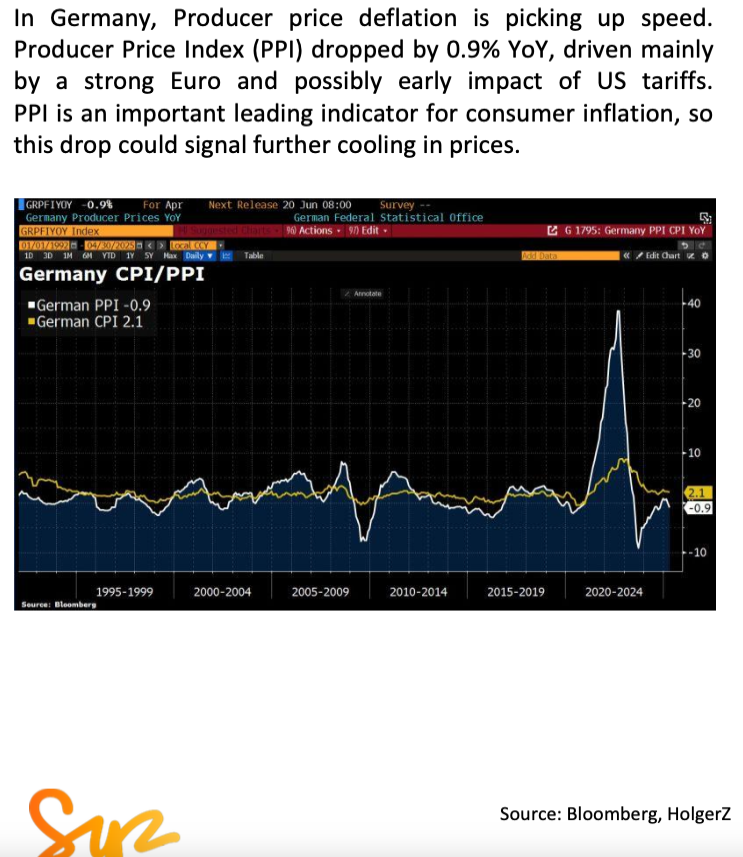

- UK CPI beat with Core at 3.8%, while German PPI collapsed—global disinflation lingers

- U.S. PPI and existing home sales disappointed, while durable goods suggested capex stabilisation

- Gold surged, BTC flew and the dollar lost friends fast

Earnings Snapshot

- Urban Outfitters +22.8% : Comps, margins, and subs all beat

- Ross Stores -14% : Withdrew guidance over tariff risk

- Deckers -16%, Target and Home Depot both weak

- Snowflake +14%, Intuit +8% : AI and cloud remain bright spots

The standout? Defensive positioning, not earnings growth, drove moves. Even strong beats were met with scepticism unless macro tailwinds aligned.

Week Ahead: NVIDIA and the Inflation Domino

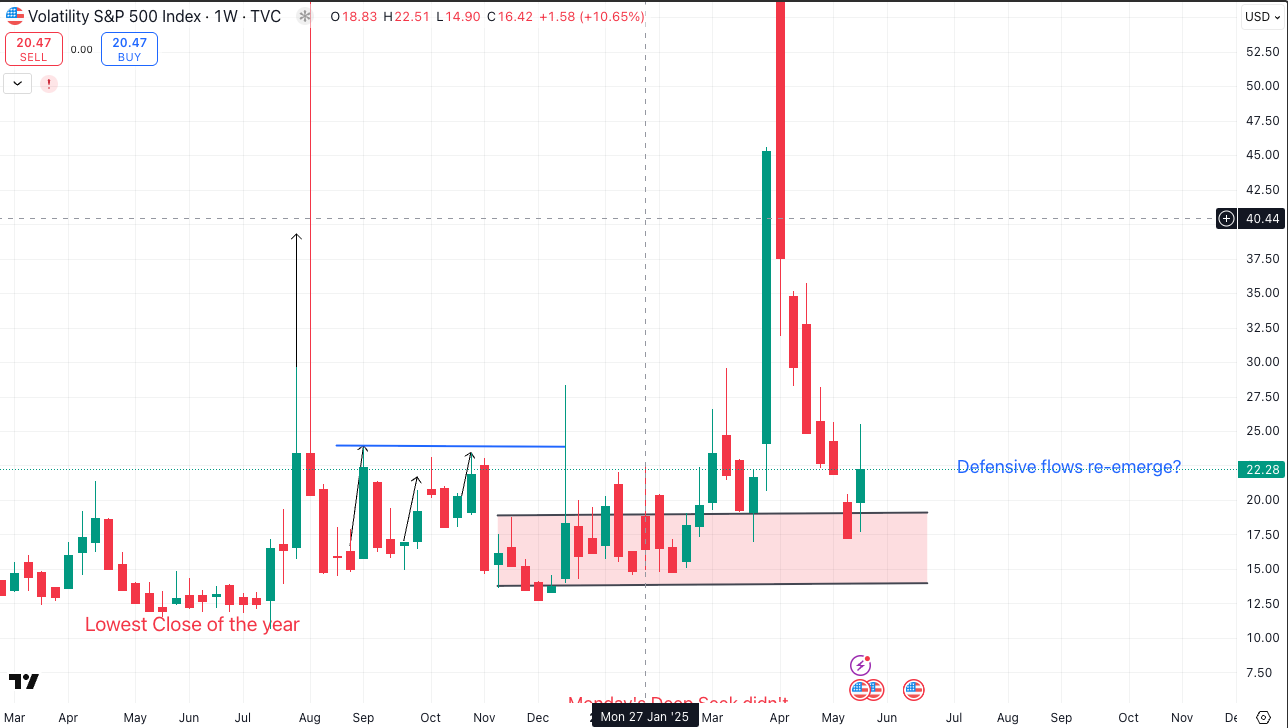

This week could tip the balance. The calm in VIX, VVIX, and MOVE is deceptive. Events to watch:

Monday, May 26 (US Half Day)

Bank holiday

Powell speaks (1940 UK)

CHF employment, JPY Leading Indicators

Earnings: JOYY Inc

Tuesday, May 27

US Durable Goods, Wholesale Sales, HPI

Earnings: PDD Holdings, Xiaomi ADR, AutoZone

Fed speakers: Kashkari, Hauser, Nagel

Wednesday, May 28

NVIDIA earnings after hours—the week's main event

FR Consumer Spending, GDP, PPI

CHF ZEW, US Richmond/Dallas PMIs

OPEC Meeting

FOMC Minutes (1900 UK)

Earnings: Salesforce, BAE, Macy’s, Synopsys, C3.ai

Thursday, May 29

US GDP (2nd read), Initial Claims, Pending Home Sales

Earnings: DELL, Best Buy, Zscaler, Lululemon, Gap, AEO

Switzerland & Sweden closed for Ascension Day

Friday, May 30

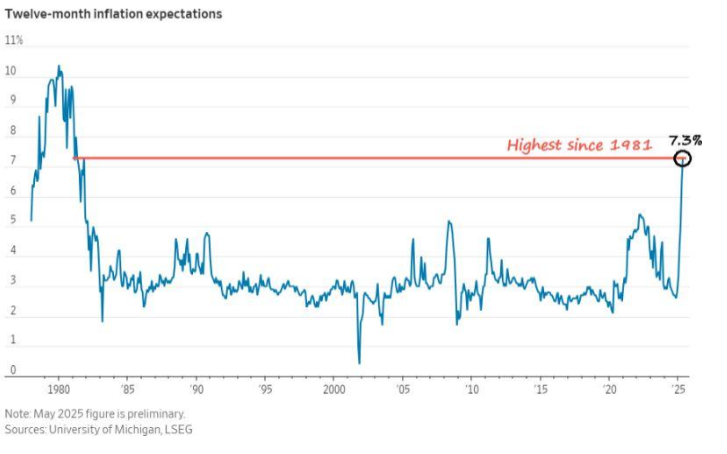

Big data day: US PCE, Chicago PMI, Goods Trade Balance, Michigan Inflation Expectations

GDP from Germany, Italy, and Canada

Earnings: Costco, Shoe Carnival, Up Fintech

Alpha Takeaway: Fade the Bounce, Watch the Internals

The bounce into Memorial Day has little breadth, heavy hedging, and bond pressure behind it. Unless SPX breadth improves and yields settle, we’re staring down a likely retest.

“Capital is voting with its feet—out of the dollar, into gold, commodities, and global equities.”

Watch For

- SPX breadth recovery—if it doesn’t come soon, a sharp leg down is in play

- NVIDIA’s impact—can it re-ignite sentiment or confirm tech fatigue?

- PCE and Michigan data—core to assessing the Fed’s next move

- 30Y and 20Y auctions—bond vigilantes are back

- USD flows, if the dollar cracks further, ex-US equities and commodities may shine