Earnings Momentum Extends, But Macro Pressures and Narrow Participation Begin to Build

Markets continue to push higher, but the underlying character of the move reflects a recovery driven more by positioning than conviction. The rally has been sustained by strong earnings and participants being pulled back into risk, rather than a broad improvement in macro clarity.

Beneath the surface, however, the structure is becoming more uneven. Earnings are delivering, and positioning continues to support the move, but rising yields, geopolitical developments, and concentrated leadership are beginning to tighten conditions. The result is a market that is still trending higher, but with growing sensitivity to macro shifts and changes in leadership.

Market Overview: Leadership Strong, Participation Lagging

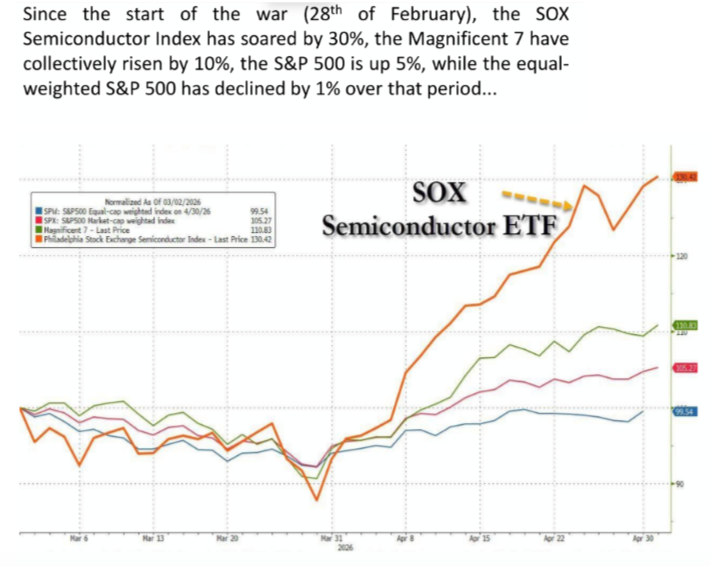

Equities continue to push higher, supported primarily by strong earnings delivery, particularly within large-cap technology and semiconductor names. This has driven index-level performance, with a relatively narrow group of leaders doing most of the heavy lifting.

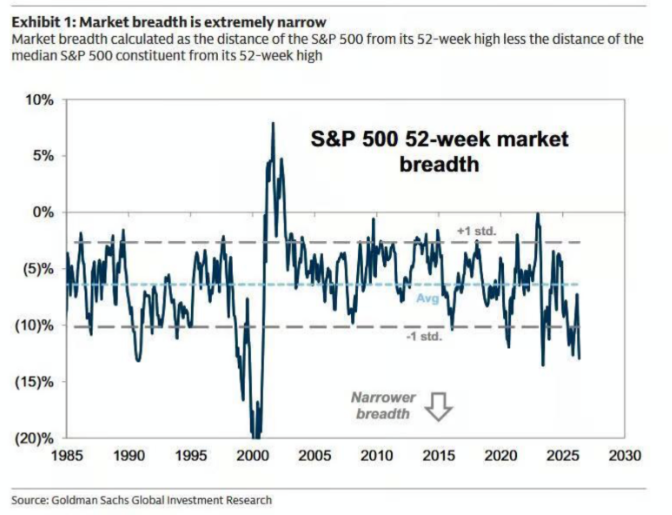

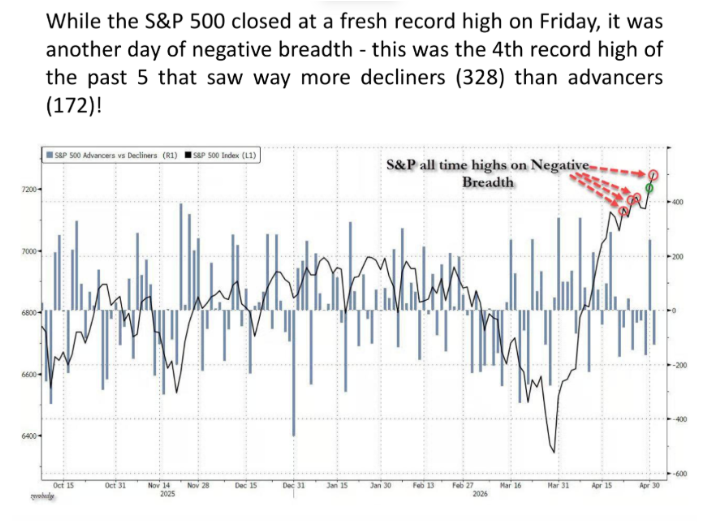

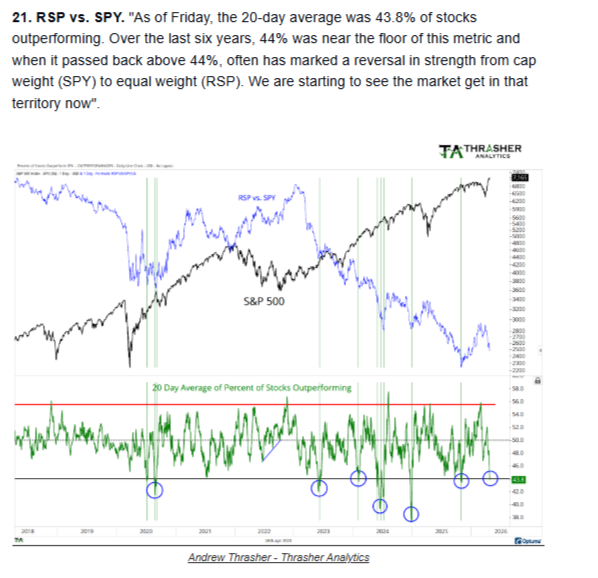

While the trend remains intact, participation is not keeping pace with price. Index highs are increasingly occurring alongside weaker breadth, suggesting that the rally is not being reinforced across the broader market.

This creates a structure where price is being sustained more by positioning, with under-owned participants being pulled back into the move as the rally extends.

Overall, conditions remain constructive, but the combination of narrow leadership and weaker participation points to a market that is still advancing, with increasing sensitivity to shifts in sentiment and leadership.

Macro & Policy Watch: Rates, Energy, and Policy Complexity

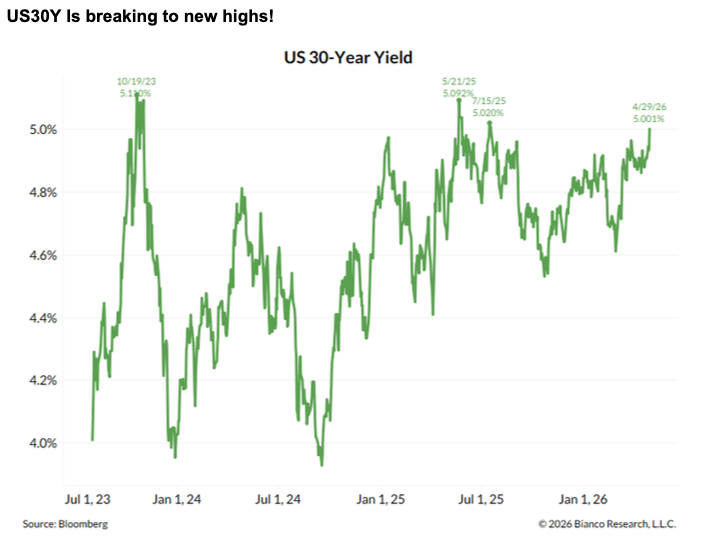

The macro environment has become more layered, with multiple forces interacting simultaneously. A key development has been the move higher in yields, driven by a combination of strong economic data, elevated energy prices, and a more hawkish policy tone.

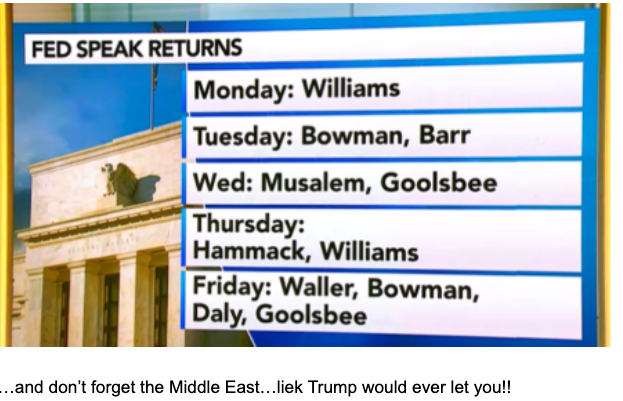

At the same time, policy expectations have become more complex. While rate cuts are not expected in the near term, internal differences within the central bank framework have emerged, adding complexity to the interpretation of policy direction.

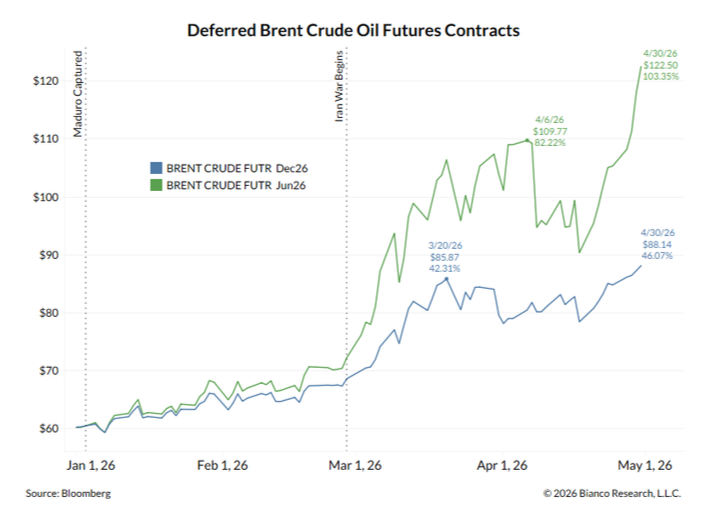

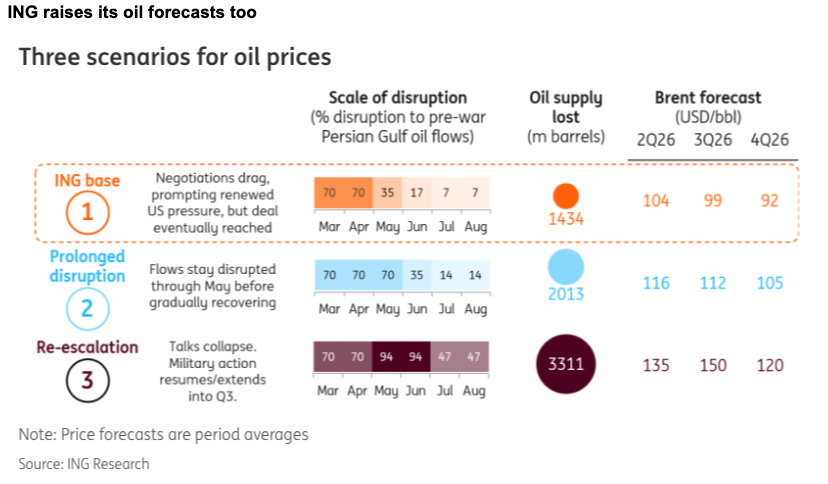

Geopolitics continues to play a central role, particularly through its impact on energy markets. Oil prices have been bid higher as supply disruptions and ongoing tensions persist, reinforcing inflation concerns and feeding back into rate expectations.

Structural shifts in energy markets are also emerging, with changes in production dynamics adding another layer of uncertainty to supply expectations.

These developments collectively suggest that macro conditions are tightening, even as positioning continues to support market conditions.

Technical & Sentiment Breakdown

Supportive, but Increasingly Fragile

The broader trend remains intact, with indices continuing to push higher, supported by earnings and positioning flows. However, the internal quality of the move is weakening, even as the price holds firm.

Breadth remains a key concern, with index highs increasingly occurring alongside weaker participation. This divergence does not break the trend, but it reduces resilience and increases sensitivity to shifts in leadership.

The rally also remains concentrated in a narrow group of sectors, particularly technology and semiconductors, reinforcing the idea that strength is not broadly distributed.

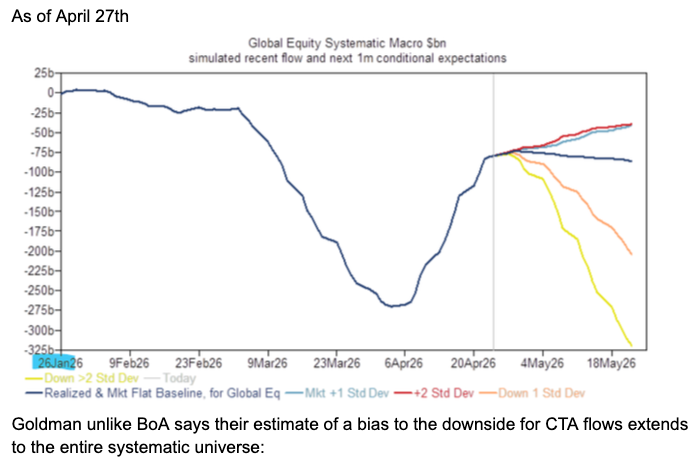

Positioning continues to support the move, with previously under-exposed participants being pulled back into the market. However, this suggests price is being sustained more by flows than fresh conviction.

At the same time, support from these flows is beginning to moderate, while the pace of the move and narrowing participation point toward a higher likelihood of consolidation.

Overall, the trend remains supported, but weakening internal confirmation and reliance on flows suggest a more fragile structure with increasing sensitivity to shifts in sentiment and leadership.

Last Week’s Recap

Strong Headlines, Mixed Underlying Signals

The past week was characterised by strong headline performance alongside increasingly mixed underlying signals. Growth and earnings remain supportive, but inflation pressures, rates, and geopolitical developments are beginning to shape the broader narrative.

Key Highlights

Macro

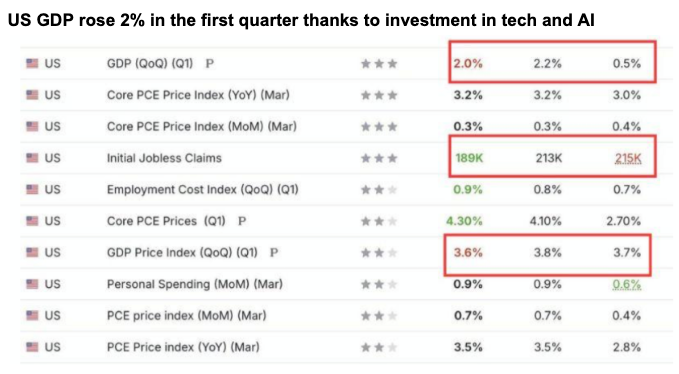

Economic data continues to show resilience, with growth supported by investment trends while inflation remains a persistent consideration. The combination reinforces the complexity of the current macro environment.

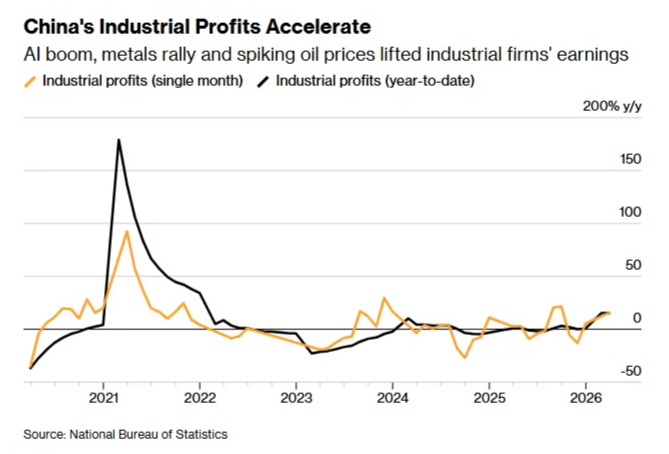

China

China remains part of the broader global demand and pricing backdrop, with developments continuing to feed into overall macro conditions.

Earnings

Earnings continued to provide a key pillar of support for equities, particularly within technology and AI-related sectors, reinforcing the upward momentum in indices.

Commodities

Commodity markets reflected ongoing geopolitical developments, with energy and related inputs continuing to respond to supply dynamics and evolving expectations.

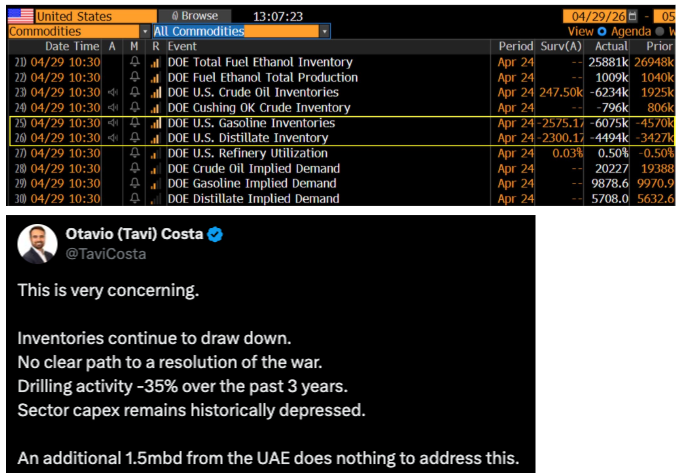

Oil

Oil remained central to the macro narrative, with prices continuing to move higher as geopolitical developments and supply considerations persisted.

The Week Ahead

Key Data and Market-Moving Signals

The week is driven by a dense global macro calendar, with a strong focus on central bank communication, labour market signals, and services activity. Liquidity conditions are uneven early in the week due to multiple holidays, while the back half is dominated by US data and policy signals that will feed directly into rate expectations.

Monday, May 4

• China, Japan, UK: Public Holidays

• Global: Manufacturing PMI releases

• US: Factory Orders, Durable Goods

• US: Loan Officer Survey

• EU & US: Multiple ECB and Fed speakers

Tuesday, May 5

• Australia: RBA Interest Rate Decision and Policy Statement

• China, Japan, South Korea: Public Holidays

• US: ISM Non-Manufacturing PMI

• US: JOLTS Job Openings

• US & Canada: Trade Balance

• US: New Home Sales and Building Permits

• US: API Crude Oil Inventories

• Global: ECB, Fed, BoE speakers

Wednesday, May 6

• Global: Services & Composite PMI releases

• Europe: Industrial Production and PPI

• US: ADP Employment Change

• US: Mortgage Applications and Housing Indicators

• US: Crude Oil Inventories

• Global: Continued central bank communication

Thursday, May 7

• US: Initial Jobless Claims and Continuing Claims

• US: Unit Labour Costs and Nonfarm Productivity

• US: Consumer Credit and Inflation Expectations

• Europe: Retail Sales and Construction PMI (growth signals)

• China: FX Reserves (macro stability signal)

• Global: Fed and ECB speakers continue

Friday, May 8

• US: Nonfarm Payrolls, Unemployment Rate, Wage Growth

• US: Participation Rate and Labour Market Detail

• US: Michigan Consumer Sentiment and Inflation Expectations (1Y & 5Y)

• Canada: Employment Data and Wage Growth

• Europe: German Industrial Production and Trade Balance

• UK: Housing Data and Mortgage Rates

Alpha Takeaway

Uptrend Intact, but Conditions Tightening

Markets remain supported by earnings and positioning flows, but the balance of risks is shifting as macro pressures build and participation narrows.

Equities

Equities continue to be driven by strong earnings and positioning flows, though leadership remains concentrated and breadth limited.

Gold & Silver

Precious metals continue to reflect broader macro dynamics and positioning conditions, rather than acting purely as a geopolitical hedge.

Rates

Yields are reasserting themselves as a key driver, with higher rates beginning to matter more for risk assets as macro pressures build. The interaction between inflation expectations and policy signals is increasingly shaping market direction.

Macro

Rising yields, persistent inflation pressures, and energy-driven dynamics are increasingly shaping the market environment and influencing risk appetite.

The broader trend remains constructive, but the path forward is likely to be less smooth. Consolidation appears increasingly likely as markets adjust to evolving macro conditions.

https://docs.google.com/document/d/1M95AulzcMPFEhvcEWWN02psztrHWFg5yTZmPQ_CUPeQ/edit?tab=t.0