Volatility Lurks, Macro Moves Take Centre Stage

This week’s trading forecast unpacks sticky macro risks, a fragile technical setup in equities, and what traders should expect from Services PMIs, Central Bank speak with FOMC, BOE, Sweden and Norway decisions, and money flows. Stay sharp, volatility isn’t done with us yet.

Market Overview: Vol Cools, But Risks Simmer Beneath

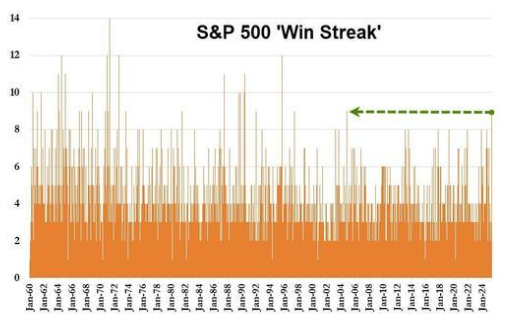

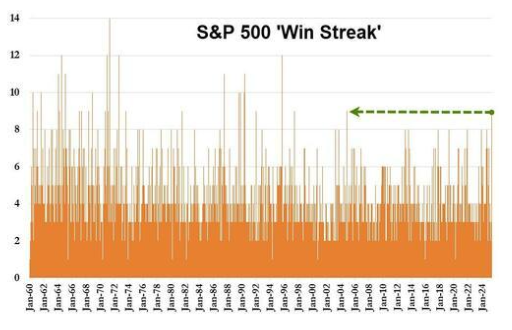

The SPX put in a 9 day winning streak not seen since Nov 2004. Data mainly held up and finished with a solid jobs report, earnings continue to beat and the combo saw markets snap back—but don’t be fooled. Beneath the relief rally, we’re staring down some persistent structural headwinds. Big tech's earnings outperformed, yet breadth remains a problem under the hood. Equity inflows were dominated by FANG-heavy positioning, and bond markets didn’t endorse equity optimism. European flows are ex-US, ex-UK and into Europe

- SPX rallied 2.94% on the week, fully recovering from April’s weakness.

- VIX dropped into 22s, but remains elevated; hedging remains sticky at the wings.

- Dollar Index (DXY) held steady despite NFP upside beat, with 4 cuts still priced in.

- Gold saw its 2nd week of decline as safe haven flows rolled off and oil slipped again on OPEC+ panic pumping at the lows, a strange mix of risk on & demand down.

Macro & Policy Watch: Sticky Inflation & Political Tension

The Fed remains data-dependent, but markets may be underestimating just how “sticky” inflation is shaping up to be. Services PMIs dominate most Western economies and we see updates. ISM prices paid has been in the 60s for a few prints now will that keep trending on tariff expectation?

- April ISM Services (Monday) is the marquee risk; still a survey but an important one. Will growth hold up or is this the first crack?

- FOMC (Wednesday) with no change expected Will Powell make any response to Trump’s poking? Market is expecting 4 cuts by Dec 25.

- US growth is slowing: top down GDP tracking estimates have been cut and so have bottom up earnings.

- Geopolitics: US-China tensions re-escalated as tariffs re-enter the conversation.

- BOE set to cut while they can (Thursday) 25bps to 4.25%.

Technical & Sentiment Analysis: Bounce or Bull Trap?

SPX reclaimed 5600, and held the 50-day average but still looks more like a reflex rally than a trend resumption. Breadth is still weak, and options positioning is overly reliant on mega-cap beta.

- Hammer Time? SPX printed a Monthly chart bullish hammer—but only after a sharp 5% drop. Follow-through matters.

- Options exposure remains tilted toward calls, suggesting traders are still chasing upside, not hedging.

- VIX slide continued slowly to 22, but VVIX (vol of vol) has cooled below 100 and into the upper bound of risk on.

Last Week in Review: NFP Held Up, GDP Went Negative, Flows Tell All. Mag4 Boost

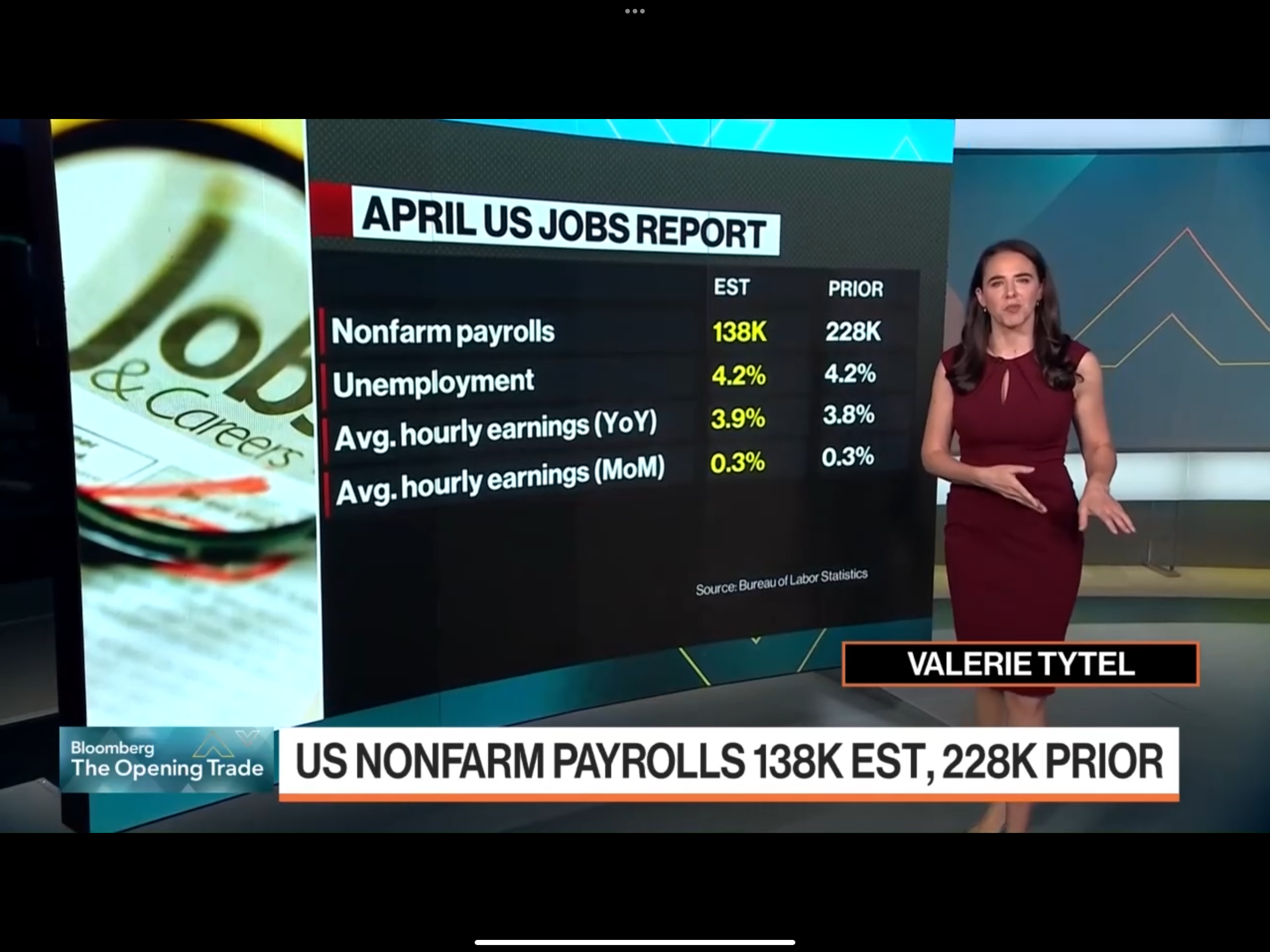

Trump backed down on Powell threats but kept pushing him to cut. NFP didn’t crater this time (+175k vs. 138k expected)—cooler wage growth gave bulls cover to push higher.

- NFP was solid and cooled immediate growth fears, but was no silver bullet. UR went up but held on rounding.

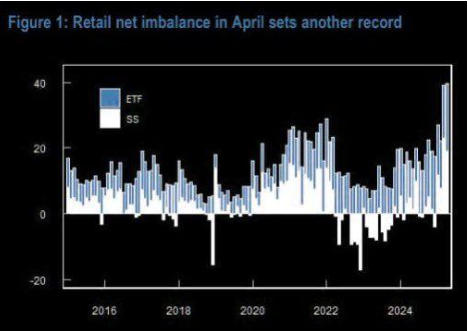

- Retail flows continued to favour tech-heavy funds, reinforcing the narrow rally concern.

- Meta, Microsoft, Amazon and Apple either beat or came in no worse than expected justifying inflows for now.

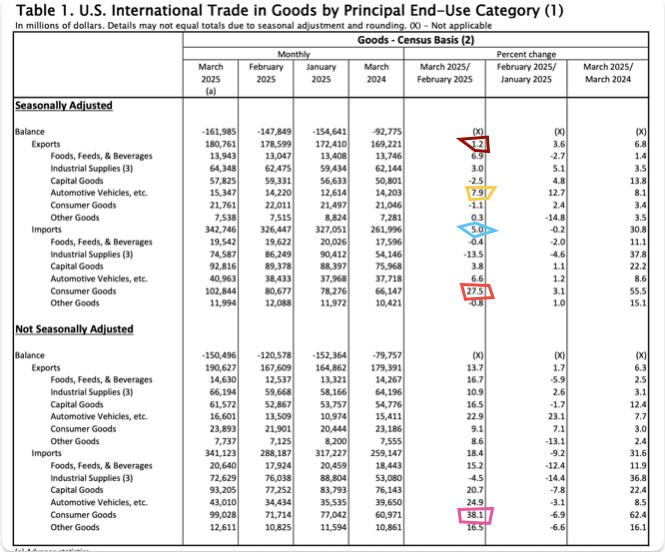

- US trade showed massive front-running imports ahead of tariffs.

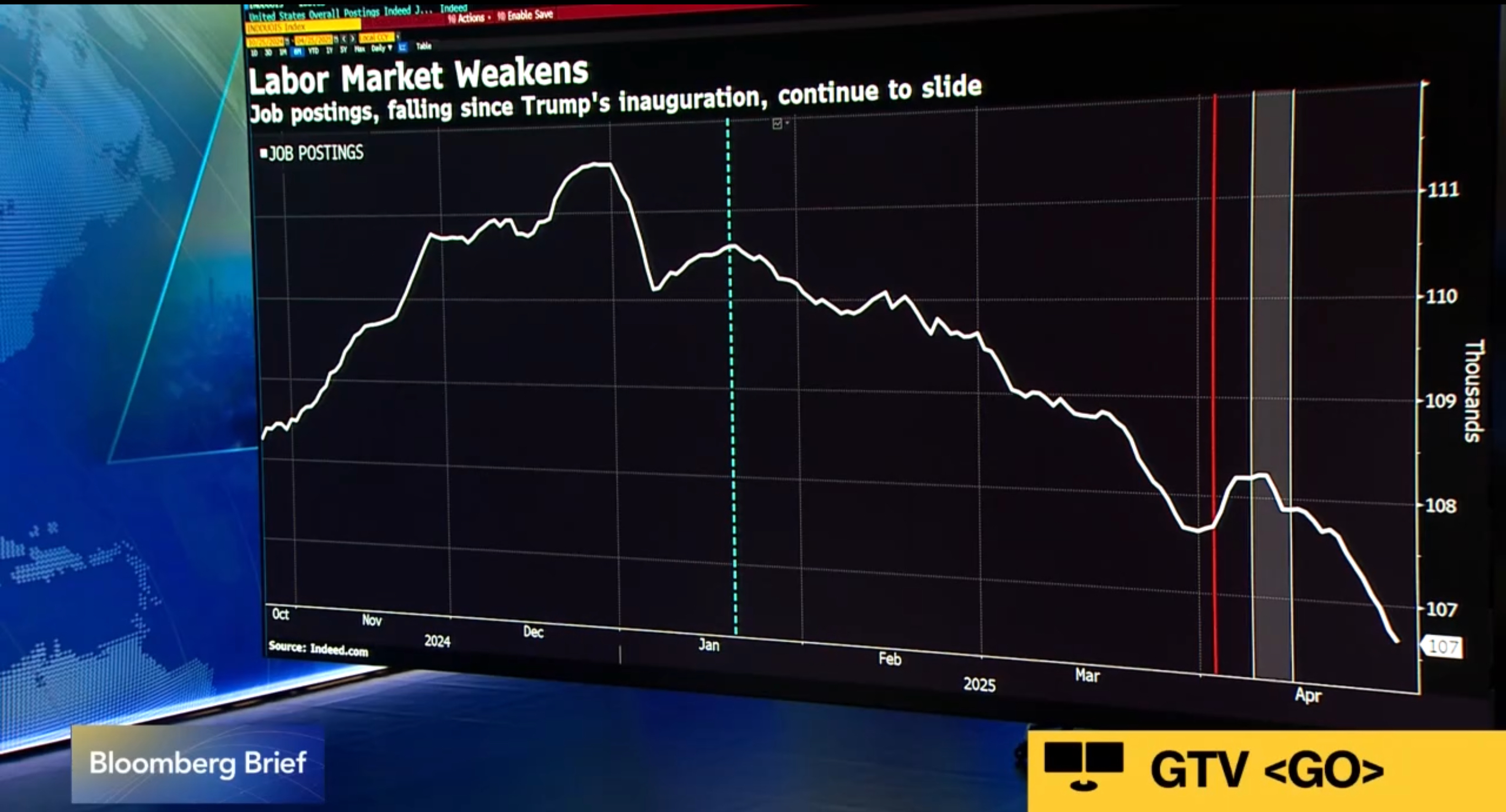

- US Jolts showed much lower openings but Quits were high showing confidence in March.

- Gold drifted on lack of fear with bulls all in but Treasuries saw defensive demand on heightened recession fears ahead—a classic sign of macro confusion.

The Week Ahead: ISM Services Looms, Sentiment Shifts, Global Macro in Motion

Much slower week with a Services slant—excitement maybe midweek with FOMC Fed-speak and BOE decisions. With sentiment already fragile, even “secondary” data could fuel volatility.

Monday, May 5

- CHF CPI everything pointing to intervention and more rate cuts; heading towards deflation fast.

- US ISM Services PMI (Apr) – The big one today. After last week’s ISM Manufacturing miss, a weak print here would confirm growth fears.

Tuesday, May 6

- Eurozone Services PMI (Final, Apr) – Still stuck in stall speed. Little hope for big upside surprise.

- IBD/TIPP Economic Optimism Index – Important context for how households are perceiving inflation and policy.

Wednesday, May 7

- No major data scheduled – Likely a positioning and digestion day.

- Traders will be leaning into FOMC setups; options positioning should get more skewed.

Thursday, May 8

- Jobless Claims – Saw a big jump last week that was too late to make it into the NFP survey; any further rise could stoke slowdown fears.

- Wholesale Inventories (Mar Final) – Backwards-looking but still useful for tracking goods demand.

- BOE decision…25bps cut expected to 4.25% enough to see inflows into the UK?

Friday, May 9

- UK March Industrial Production – could confirm stagflationary pressures but should be post a rate cut. The FTSE100 has risen despite outflows anyway.

- Canadian employment – Any tariff destruction yet for the 51st State?

Alpha Takeaway: Don’t Trust the Bounce, Macro Risks Still Bite

Last week’s bounce felt good, but it wasn’t healthy. The rally was driven by gamma flow, light positioning, and relief of it could have been worse, not real conviction. Beneath the surface, data is seen deteriorating but holding on for now, breadth remains poor, and defensive assets like gold and bonds are still catching solid bids within some volatility.

The market is not trading a soft landing—it’s trading a short squeeze in a shallow pool of liquidity.

Here’s what matters:

- SPX breadth remains weak. Only 43% of S&P names are above their 50-day MA. Big tech is doing the heavy lifting.

- Positioning is light. CTA net exposure is still off the highs, and retail is hesitant.

- Gold remains bid despite equity upside, classic defensive behaviour.

- Bond yields fell until a strong, mixed NFP. Growth fears remain this is not a risk-on green light yet.

- Earnings have not cratered to the April call down levels but have not been re-rated for the remainder of the year yet. SPX 5680 is 21x forward FY25 earnings-Muddled ground and large sellers came in on Thursday night. Danger of driftback remains