Rotation, Policy Fog, and a Market That Refuses to Break

Despite a week filled with warnings — AI exuberance, political uncertainty, credit-market whispers, and a government data blackout — the market delivered something few expected: resilience beneath the surface. What looked like risk-off was, in reality, a sharp sector rotation hiding inside the noise.

The tape was messy, but not broken.

The narrative was loud, but price action was quietly orderly.

Market Overview: A Reset, Not a Breakdown

The week began with bearish chatter: talk of an overdue crash, hand-wringing about AI excess, and even an odd cameo from Michael Burry trying to stir support for his short on Palantir. But markets didn’t crack — they rotated.

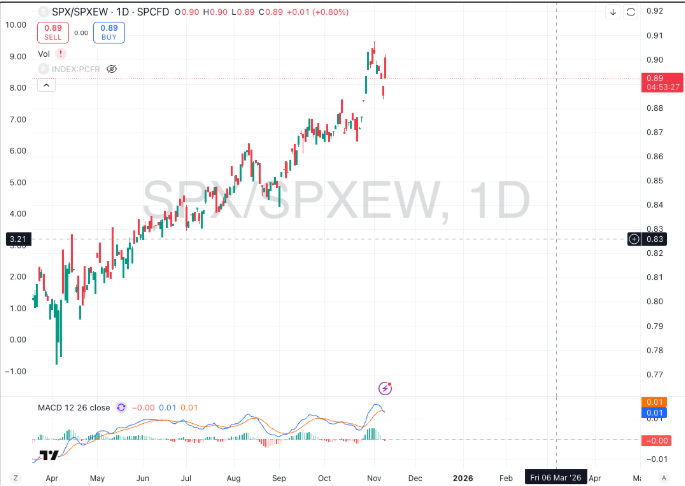

Equal-weight S&P outperformed until Friday, when a powerful post-lunch rally reversed the tape despite disappointing UoM sentiment numbers.

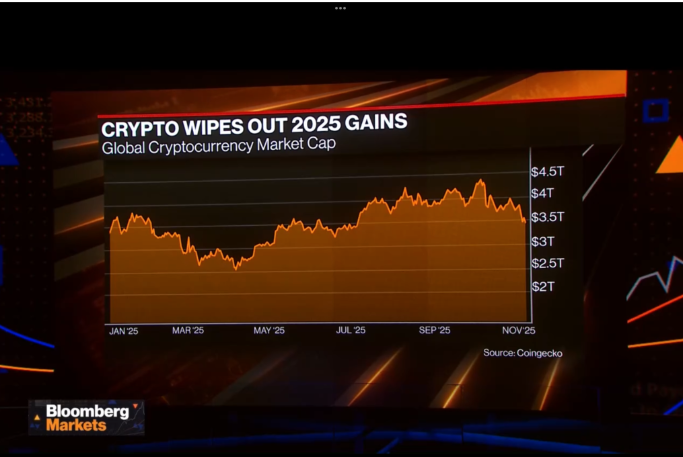

Gold defended its 50-day. Oil drifted but stayed constructive. Crypto tested lows but bounced hard as long-term holders handed supply to institutional “Treasury Whales.

Despite the gloom, liquidity kept flowing — and that mattered more than the noise.

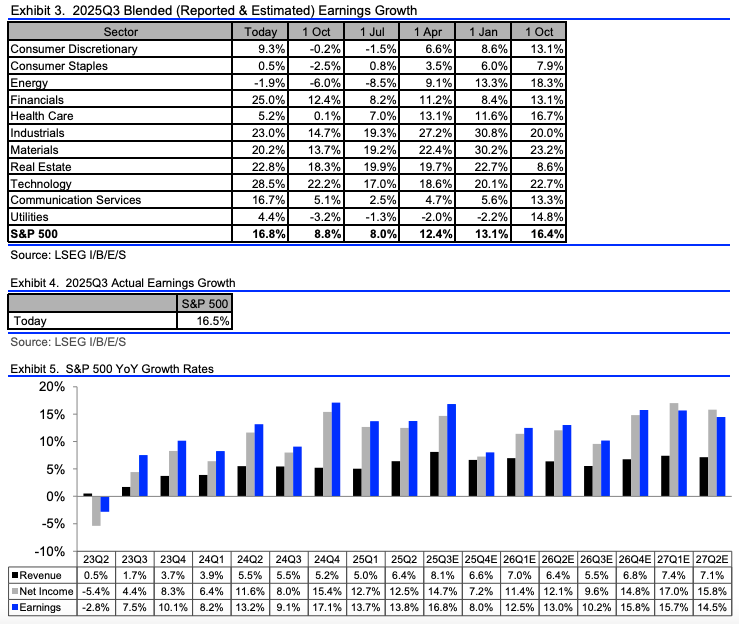

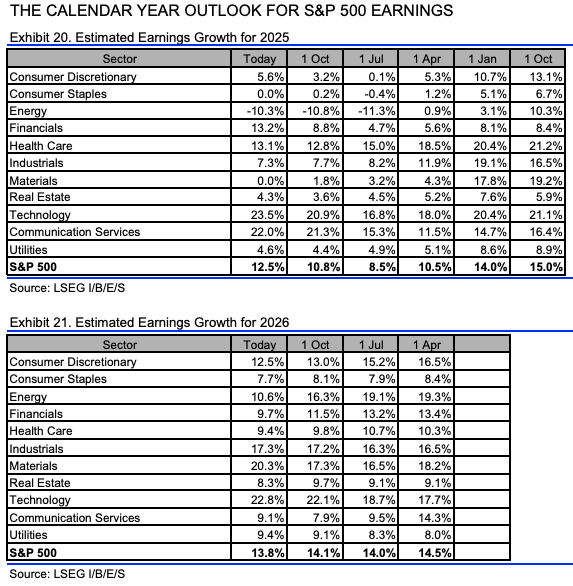

Corporate earnings remained exceptionally strong, beating Q1 and Q2 — but analysts still refuse to lift FY26 expectations.

The short-term looks great.

The long-term still looks foggy.

Macro & Policy Watch: Tariffs, Fed Caution, Shutdown Chaos

1. SCOTUS vs Trump’s Tariffs: A Potential $80B Shock

Supreme Court arguments challenged the legality of Trump’s reciprocal tariffs, with Chief Justice Roberts calling them effectively “taxes on Americans.”

If they are struck down, the Treasury could owe $80 billion in refunds, steepening the curve and complicating deficit math.

2. Fed Tone: Cautious, Split, and Inflation-Focused

Fed speakers delivered a mixed bag:

- Jefferson: policy still restrictive

- Powell: December cut is “far from a foregone conclusion”

- Waller and Goolsbee diverged

- Hammack was aggressively hawkish

Meanwhile, QT runoff ended, and markets absorbed the prior 25bps cut cleanly.

The Fed doesn’t want to talk about stocks — but they certainly don’t mind cooling them.

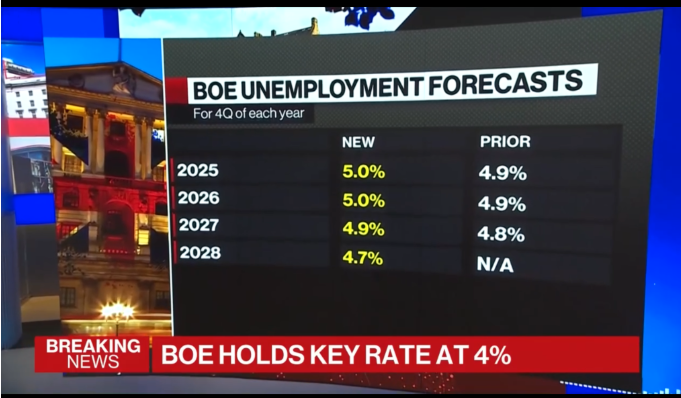

3. BOE’s Missed Opportunity

The BOE nearly surprised with a cut, but Bailey refused to back the doves, opting for caution despite clear economic strain in the U.K.

Shutdown disruptions added another layer of confusion — with most economic releases frozen, traders relied entirely on private data like ADP, Challenger, and Redbook.

Technical & Sentiment Breakdown: Rotation Beneath the Surface

1. S&P 500 Defends 50DMA, Reverses Hard Into Friday

The S&P 500 tested its 50dma near 6666 (ominous, but powerful) and launched a fierce reversal.

- Breadth broadened.

- Small and midcaps led.

- Equal-weight S&P outperformed cap-weighted.

A correction in sentiment, not fundamentals.

2. Tech: Gravity, Not Failure

Mega-cap tech finally cooled:

- Semis: –4% to –6%

- FANG+: pulled back

- XLK retook its opening levels

- AI leaders are still attracting massive capex

But the story was position-reset, not structural damage.

NVIDIA’s dominance remains a structural force — its $5T market cap warps everything around it.

3. Energy, Staples, Health Care Rotate In

- Energy caught a bid from surging natural gas prices.

- Health care and staples were steady winners.

- Utilities and real estate stabilised late as yields softened.

4. Gold & Oil

Gold hugged $4k and its 20dma.

Oil drifted and struggled with long-term resistance.

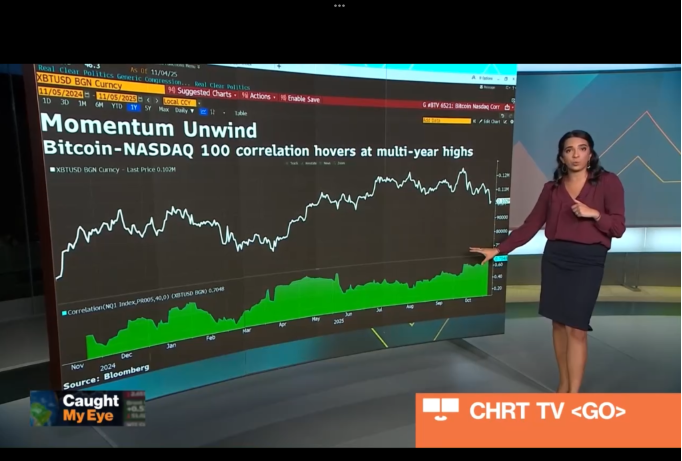

5. Crypto: The Liquidity Tell

- Bitcoin repeatedly broke $100k, then staged a clean reversal.

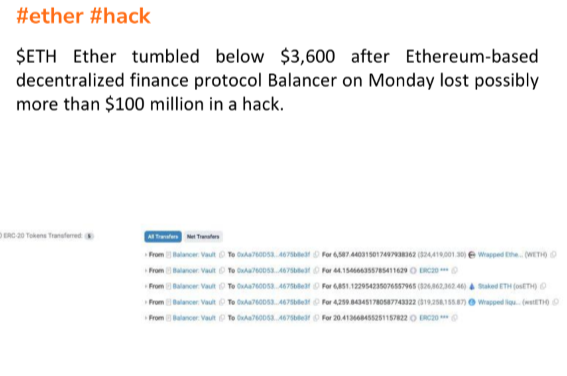

- Ethereum held its 200dma despite the Layer-2 hack.

- Solana saw strong inflows.

Crypto once again signalled risk sentiment hours before equities followed.

Last Week’s Recap: Layoffs, Rotation Flows, and Cross-Asset Stabilisation

Markets kicked off cautiously but rallied into Friday as private-sector data filled the shutdown vacuum, layoffs spiked, and rotations replaced fear. Sentiment improved as breadth broadened late week, crypto stabilised, and earnings once again outperformed short-term expectations even as long-term visibility softened.

Key Highlights

Macro

The government shutdown halted key releases, forcing traders to rely on ADP, Challenger, Redbook, and UoM. Challenger job cuts surged to 153,074, the highest October print since 2003, pushing YTD layoffs above 1 million. UoM personal-finance sentiment collapsed, inflation expectations stayed elevated, and Fed speakers kept December rate-cut odds uncertain with mixed hawkish-dovish tones.

China

China posted a rare CPI uptick after months of deflation, though the move appears Golden-Week-driven rather than structural. The improvement eased global disinflation pressure temporarily, but a sustained rise would remove one of the market’s biggest macro tailwinds.

Earnings

Q3 earnings beat both Q1 and Q2 momentum, even as FY26 estimates drifted lower again. M&A surged across sectors — from Kimberly-Clark’s ~$50B Kenvue deal to Pfizer and Novo Nordisk bidding for Metsera — reinforcing corporate balance-sheet strength in an otherwise cloudy macro environment.

Commodities

Gold held the $4k area and its 20DMA, remaining structurally constructive. Oil drifted lower and struggled to reclaim long-term resistance amid seasonally soft demand and macro uncertainty.

Crypto

No clean breakout, but no breakdown either. Bitcoin slipped below $100k multiple times before reclaiming it, while Ethereum held its 200DMA despite a $100M Layer-2 hack. Large wallets accumulated steadily as long-term holders handed supply to institutional treasuries.

The week reinforced a rotation-driven, liquidity-sensitive market: cautious at the surface, but quietly stabilising underneath.

The Week Ahead: Shutdown Filters, Fed Firehose, and Rotation Catalysts

Four days of dense global data, an intense Fed-speaker lineup, and AI-sensitive earnings shape the week ahead. With U.S. government releases still constrained, traders will lean on private-sector indicators to gauge labour conditions and inflation stickiness.

Monday, Nov 10

- Australia: Building Approvals

- Japan: Coincident Index, Leading Index

- Eurozone: Sentix Investor Confidence

- U.S.: Wholesale Inventories, Wholesale Trade Sales

- Talking Heads: BoJ Nakagawa; BoE Lombardelli; FOMC Daly; Fed Musalem

Tuesday, Nov 11

- Canada: Holiday (Armistice/Remembrance)

- U.K.: Earnings & Unemployment

- China: M2, New Loans, Total Social Financing

- Eurozone: German & Eurozone ZEW

- U.S.: NFIB Small Business Survey, Redbook

- Talking Heads: Lagarde; Vujcic; Sleijpen; Greene; Dhingra; Jones

Wednesday, Nov 12

- Germany: CPI

- Italy: Industrial Production

- Global: OPEC Monthly Report

- U.S.: MBA Mortgage Data; API Crude Oil

- Auctions: German 30-Year Bund; U.S. 10-Year Note

- Talking Heads: Barr; Schnabel; De Guindos; Pill; Williams; Paulson; Waller; Bostic; Miran; Logan

Thursday, Nov 13

- Australia: Unemployment

- U.K.: GDP, Industrial Production, Trade Balance

- Eurozone: Industrial Production

- U.S.: Jobless Claims; Core CPI; Productivity; Oil Inventories

- Earnings: Disney; Applied Materials

- Talking Heads: Kocher; Schnabel; Bailey; Nagel; Hammack; Tschudin; McPhee

Friday, Nov 14

- China: Retail Sales; Industrial Production; Unemployment

- Eurozone: CPI; GDP; Trade Balance

- Canada: Manufacturing & Wholesale Sales

- U.S.: Atlanta Fed GDPNow

- Earnings: JD.com ; Nubank

- Talking Heads: Vujcic; Balz; Elderson; Bostic; Logan

Alpha Takeaway: Bounce Valid But Fragile and Flow-Dependent

The market’s rebound remains intact. Liquidity pockets are improving, earnings are doing the heavy lifting, and rotation continues to broaden participation. But narrow leadership, elevated correlations, and macro fog demand precision and discipline.

Equities

Rotation improved, but leadership remains concentrated. Buy controlled dips in structurally strong areas; avoid weak sectors fighting major trend breaks. Breadth needs to be confirmed for momentum to extend.

Gold & Oil

Gold’s resilience above $4k keeps the structural bull case alive. Oil remains vulnerable with soft demand and resistance overhead — conviction requires a clean reclaim of trend levels.

Crypto

Positioning reset is mostly complete. Institutional flows continue, and BTC’s Friday reversal again led equities. A stable liquidity backdrop could trigger range breakouts later this month.

Macro

Shutdown-distorted data makes Fed commentary unusually important. December rate-cut odds are drifting, not fixed. If funding stress eases into December’s QT shift, risk assets can extend higher; if not, volatility returns quickly.

The market remains bullish — but narrow, levered, and sensitive to liquidity tremors. Trade strength tactically, buy weakness selectively, and stay alert to rotation inflexion points.

The message is simple:

- Trade the setups, not the stories.

- Be tactical.

- Respect rotation.

- Survive the week.