Liquidity Cracks, Narrow Breadth, and a Market Stuck in Transition

The U.S. government shutdown finally ended, but instead of relief-driven strength, markets delivered a confused, uneven tape. Liquidity tightened, breadth weakened, and crypto suffered heavy technical damage. Yet the long-term trend remains intact — this is not a breakdown, but a transition phase where fatigued markets wait for a catalyst.

Investors are navigating a late-cycle environment defined by margin pressure, constrained liquidity, cautious policy signals, and slowing global impulse. The next major turning point now hinges on Nvidia’s earnings, the returning data cycle, and whether liquidity stabilises into December.

Market Overview: Relief Without Confidence

The shutdown’s conclusion should have lifted markets — instead, equities slumped. Thursday saw sharp selling across technology and high-beta names, and Friday opened soft again before covering flows offered mild relief.

The real shock came from the liquidity side:

The Treasury is rebuilding its General Account toward $1T, draining reserves from the financial system just as traders hoped for fresh liquidity.

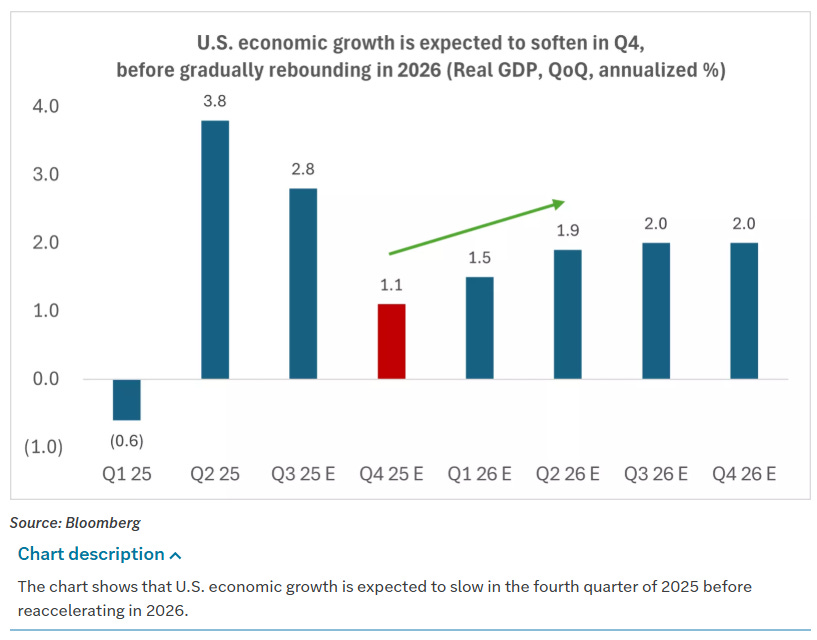

The economic impact is severe. The CBO expects the six-week freeze to cut Q4 GDP by 1.5 percentage points, dragging expected growth into the 1.0%–1.5% range.

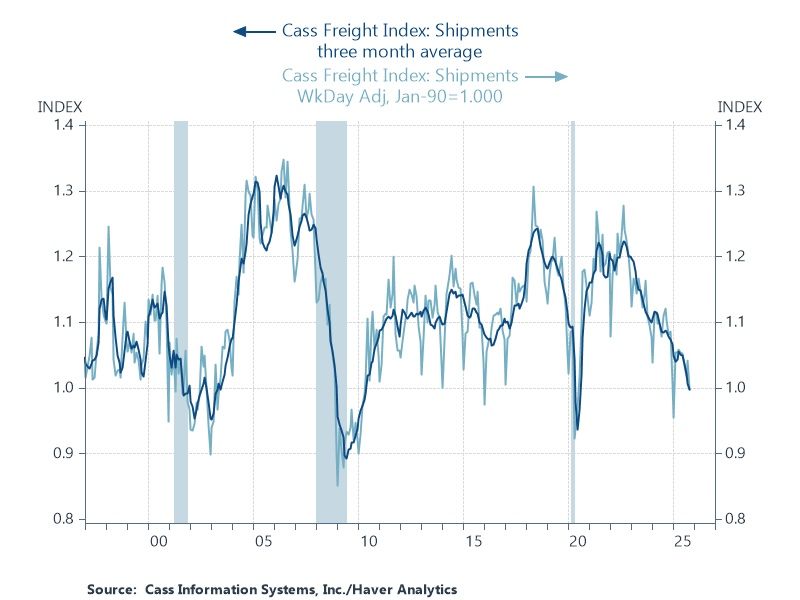

Freight softness amplified macro anxiety. With shipping indices weakening again, traders debated whether this signals an early recession impulse or simply tariff noise.

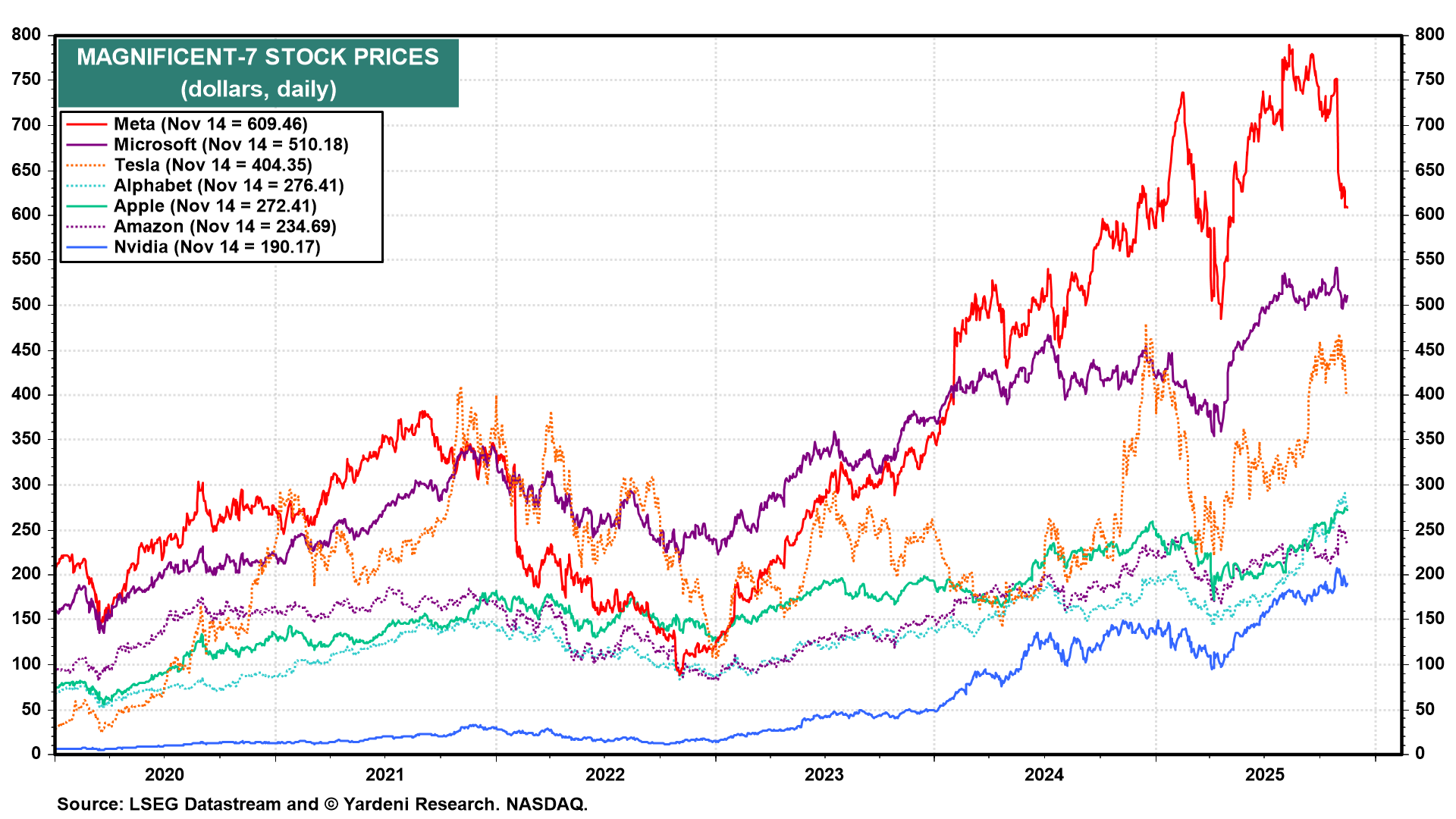

Meanwhile, mega-cap concentration deepened. The S&P 500’s reliance on its largest names remains historically high — making the tape more sensitive to downside shocks.

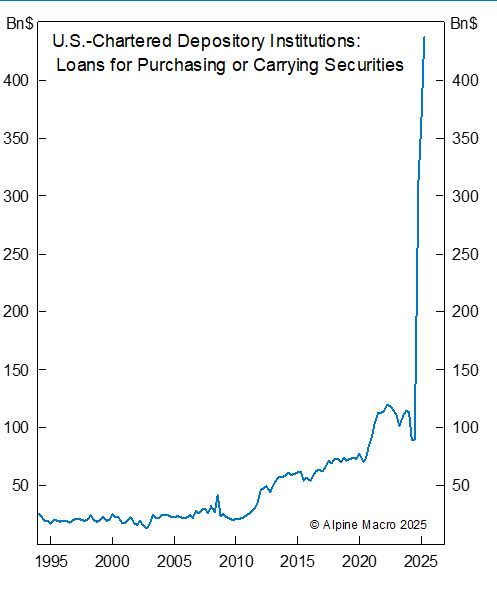

Liquidity can also be seen unwinding through rising margin debt and stress in higher-leverage segments.

The message from price action is simple:

Relief is not conviction — markets want proof before committing.

Macro & Policy Watch: A Fragmented Fed and Slowing Global Liquidity

Fed communication turned sharply mixed last week.

- Logan resisted further cuts.

- Schmid warned against over-easing.

- Musalem leaned defensive.

- Daly flagged downside risks in the labor market.

The result?

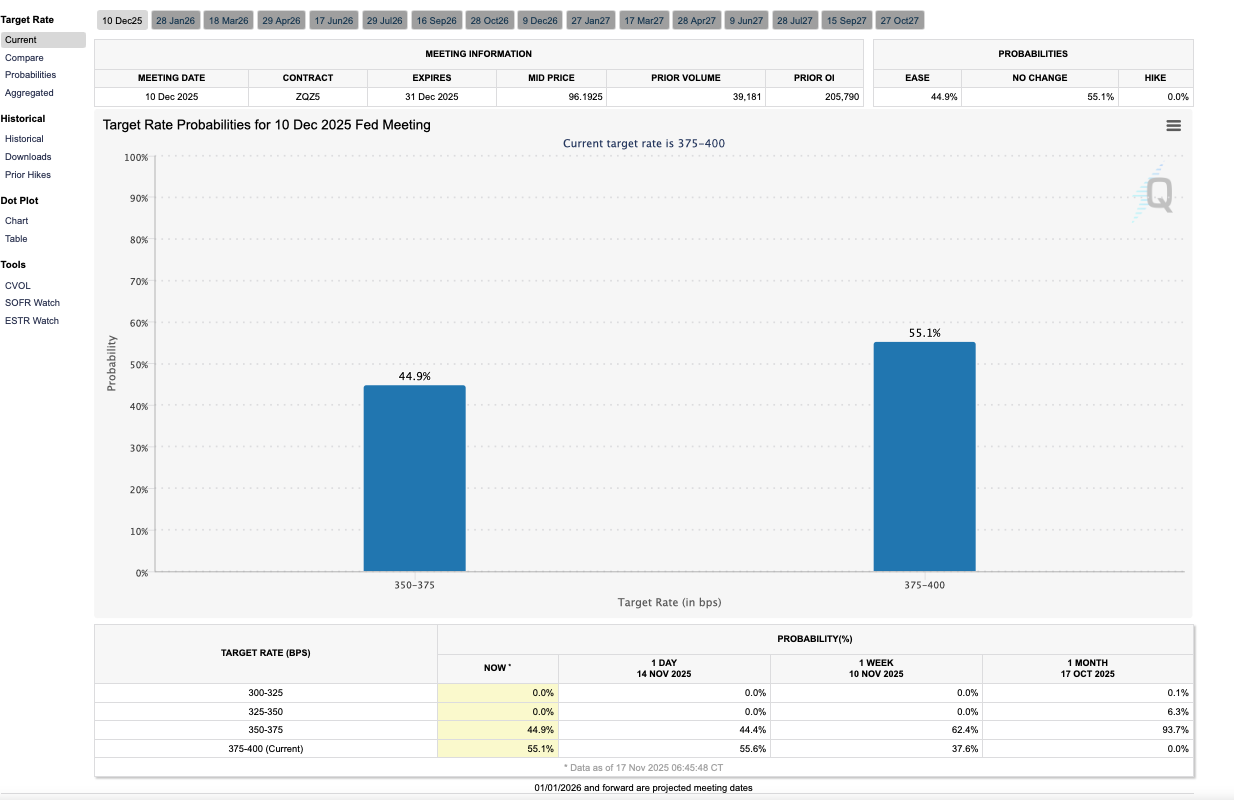

Markets have dramatically repriced December expectations — odds now sit well below 50%.

Globally, the liquidity impulse is fading. The past year delivered 167 rate cuts, but only 81 are expected in the next 12 months. This slowdown is showing up in crypto, credit spreads, and risk-asset sensitivity.

Energy capacity emerged as the real bottleneck in AI scaling, not chips. China’s aggressive push in nuclear and renewables contrasts with U.S. affordability politics — a divergence that will shape 2026 sector dynamics.

Emerging markets continue to show improving deal flow, led by Asia’s tech ecosystem and supportive capital environments.

And with Japan’s fiscal expansion amplifying inflationary dynamics, the yen continued to hover near critical pivot levels — a key variable for global carry trades.

Technical & Sentiment Breakdown: A Correction Inside a Larger Uptrend

Breadth deterioration continued across indices:

- Only 32%–42% of SPX & Nasdaq components sit above short-term moving averages

- New lows dominate the 5-day and 1-month windows

- Correlations are rising

- Tech leadership is weakening

And yet — the bigger trend remains intact.

The S&P 500 has now held above its 50DMA for 198 consecutive days, one of the longest streaks since 1950.

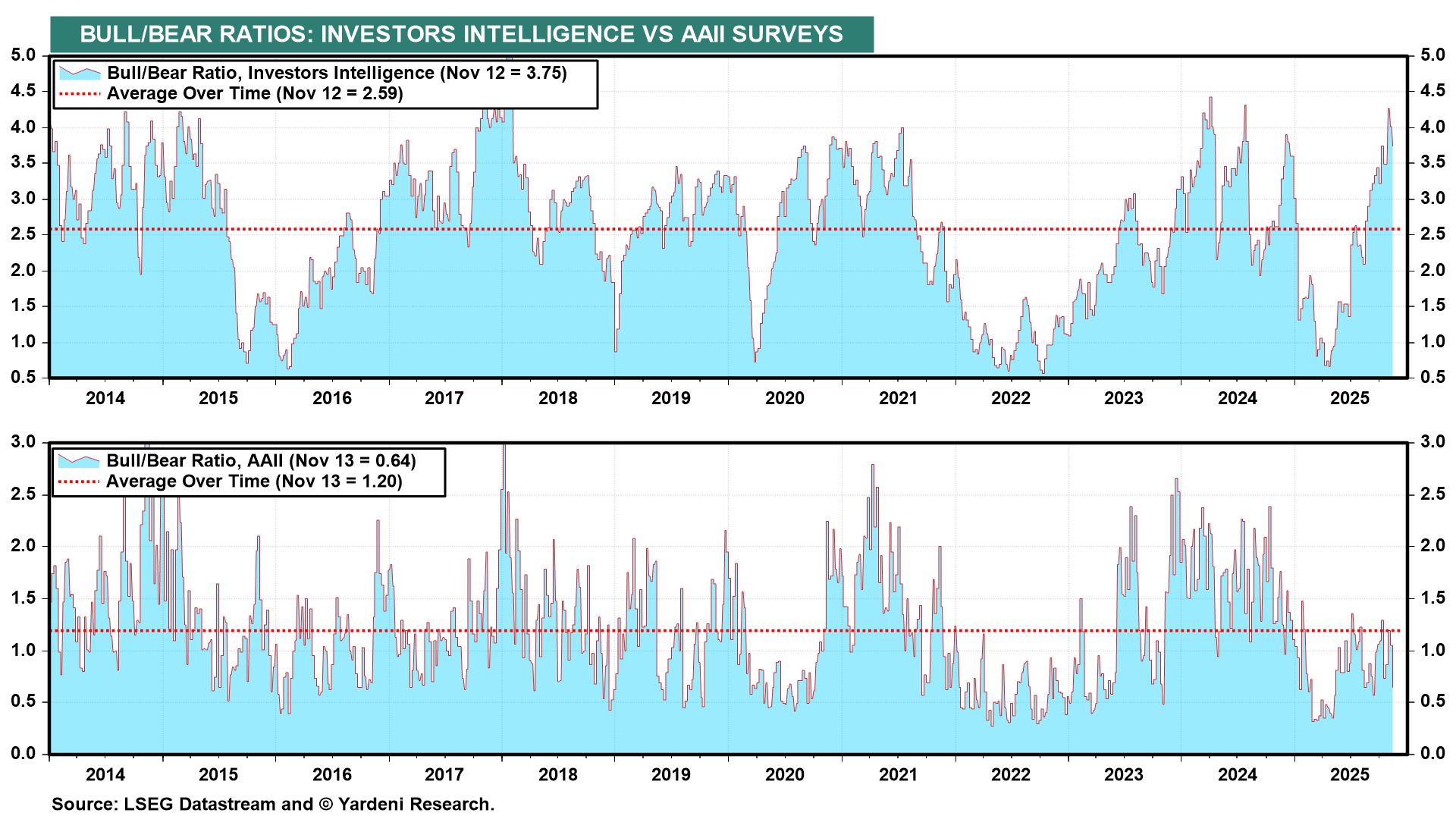

Sentiment has shifted from bullish to structurally complacent — the kind of mood that precedes volatility spikes.

Breadth remains fragile.

When only a narrow group is holding up the index, downside moves accelerate quickly. The Russell 1000 and equal-weight indices reflect deeper underlying weakness.

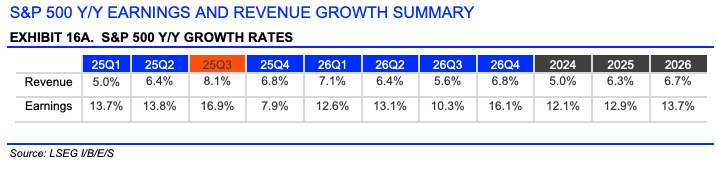

Earnings, however, remain strong.

Q3 has produced an 82% beat rate, the strongest since 2021 — an important counterweight to technical weakness.

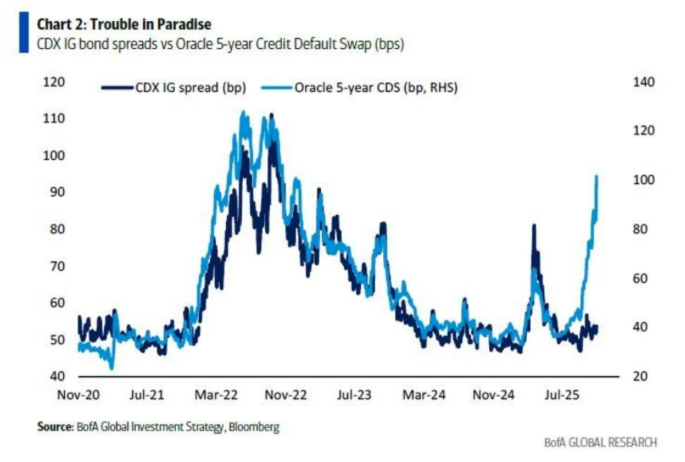

Credit spreads also reinforce caution. They continue to widen at the margin — not aggressively, but persistently.

The takeaway:

This is a correction driven by positioning and liquidity, not fundamentals.

Last Week’s Recap: Shutdown Ripples, Tech Anxiety, and Crypto Stress

Markets opened weak but recovered into Friday as end-of-week covering, improving sentiment pockets, and strong earnings offered support — despite liquidity cracks and risk-off momentum earlier in the week.

Key Highlights

Macro

The shutdown ended, but the liquidity drain continued. Treasury’s TGA rebuild is absorbing system cash, tightening conditions. The GDP hit could be 1.5 percentage points in Q4.

China & Global

Freight data softened again, raising questions about whether global demand is slowing or merely distorted by trade policy shifts.

Earnings

Q3 earnings held up markets. 82% of S&P companies beat estimates — the highest since 2021. Healthcare, materials, and staples led the upside.

Additional earnings insights noted high investor concentration in mega-caps, amplifying reaction risk into NVDA’s print.

Commodities

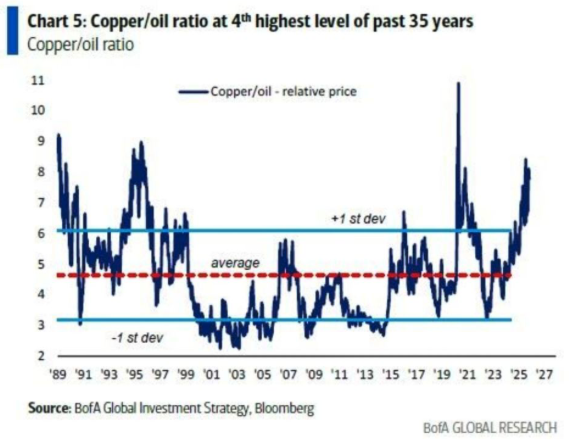

Gold saw a margin-driven dip but held long-term support. Silver’s volatility mirrored liquidity pressures. Copper’s strength hints at PMI improvement ahead — a bright macro signal.

Crypto

BTC broke below the 200DMA and $100k amidst halving anxiety and ETF outflows. Structural Wave ((4)) correction remains intact.

Ethereum slipped toward key supports near 3100.

Oil

WTI struggled at its 50DMA amid inventory builds and conservative demand forecasts.

oil outlooks holding pressure

The Week Ahead: Data Returns and NVDA Takes the Spotlight

With the government reopened, markets will finally resume a full macro data cycle. The week is dense, and NVDA sits at the centre of global risk appetite.

Monday, Nov 17

- Fed Speakers: Williams, Jefferson, Kashkari, Logan, Waller

- U.S. Budget Statement

- EU Economic Forecasts

Tuesday, Nov 18

- ADP Employment

- NAHB Housing Index

- Industrial Production

- API Oil Stock

- RBA Minutes

Wednesday, Nov 19

- U.K. CPI

- Eurozone CPI Final

- U.S. Mortgage Apps

- Building Permits

- EIA Inventories

- FOMC Minutes

- Fed: Barkin, Williams

- Earnings: NVIDIA (after hours)

Thursday, Nov 20

- U.S. Existing Home Sales

- Philadelphia Fed Index

- EU/Spain/Germany PPI & Trade

- China Loan Prime Rate

- Fed: Goolsbee, Dhingra

Friday, Nov 21

- Flash PMIs (U.S., EU, Japan, India)

- Real Earnings

- Michigan Sentiment

- Fed Speakers: Williams, Logan, Jefferson

Alpha Takeaway: A Market in Transition — Not a Breakdown

Liquidity is tight, breadth is weak, crypto is volatile — yet recession is not the base case, and long-term equity structure remains intact. This is a corrective phase inside a broader uptrend, not an end-of-cycle top.

Equities

Expect choppy upside attempts until breadth improves. NVDA’s report is the single biggest catalyst of the week. A strong beat could restore leadership and stabilize semis.

Gold & Silver

Gold remains structurally bullish despite margin-driven softness. Silver continues to behave like a leveraged liquidity proxy — volatile but constructive.

Crypto

BTC weakness is liquidity-driven. Wave ((4)) structure remains the base case. Institutional inflows on dips remain the most important bullish divergence.

Macro

December cut odds have collapsed. Shutdown distortions may produce noisy data. But with the Fed debating cuts — not hikes — the macro regime still favors rotation, not recession.

The market is waiting for a catalyst, not collapsing.

Stay selective, stay patient, and let breadth confirm the turn.