Liquidity Cracks, Narrow Breadth, and the Market Stuck in Transition

Markets spent the week wrestling with a confusing mix of seasonality, liquidity stress, and fragile sentiment. What should have been a clean fourth-wave reset has turned into a deeper psychological shakeout, with even committed dip buyers beginning to question the playbook. The backdrop remains messy: repo-market tightness, heavy U.S. Treasury issuance, margin-linked selling in crypto and tech, and a structural lack of breath beneath October’s highs.

Despite this, the larger roadmap still points toward a year-end finish above current levels. But with forced selling still in the system and volatility-control flows ready to unwind, the path remains uneven — and patience, not aggression, continues to be rewarded.

Market Overview: Liquidity Strains and the Forced Seller Era

Liquidity, not fundamentals, dominated price action. The report highlights that large U.S. Treasury issuance — particularly ahead of Dec 2 — continues to pressure risk assets. Each round of supply has forced marginal buyers to dump high-beta equities, crypto, and even precious metals.

The Nasdaq 100 fulfilled its classic corrective target, tagging the 20-week moving average and wicking below the 24k zone — the traditional bounce level in a wave-4 structure.

But technicals aren’t the only stress point. Breadth was weak into the October top, with euphoric flows into unprofitable tech and gold masking underlying fragility. Vol-control models remain primed to sell on any VIX breakout, and CTA positioning suggests further forced liquidations if indices slip again.

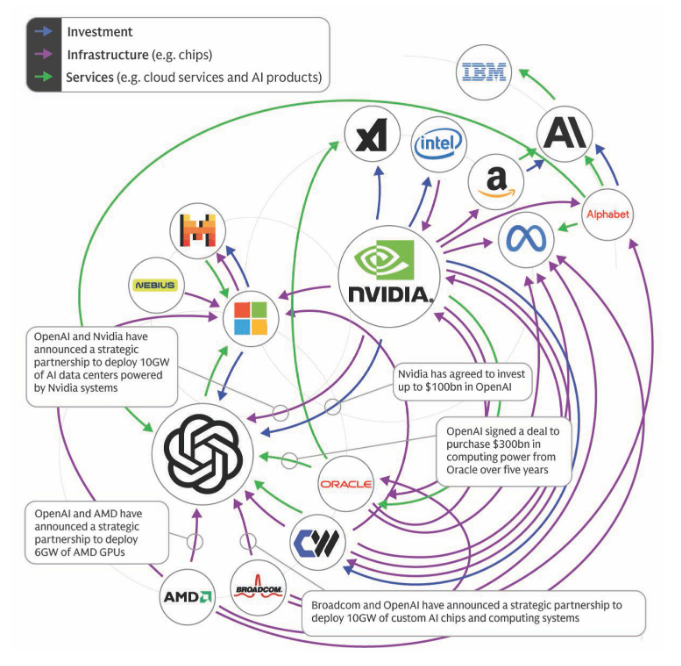

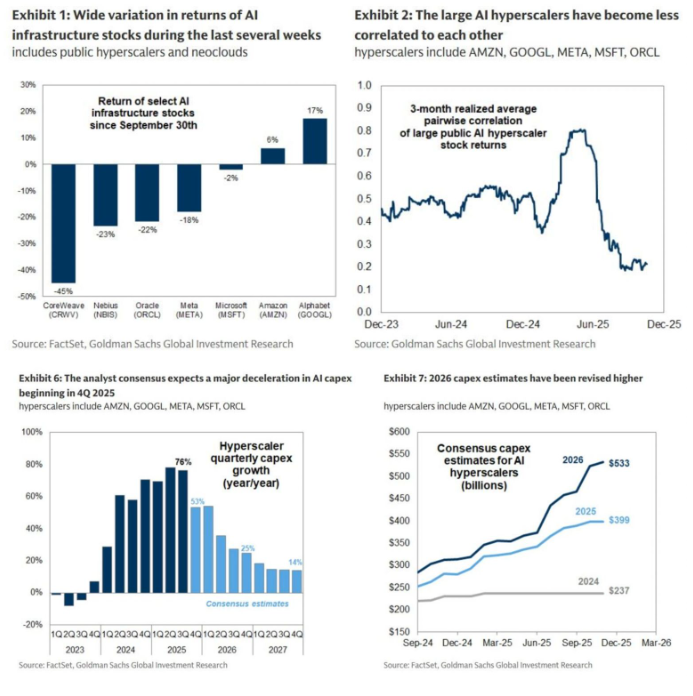

The AI narrative also lost momentum. NVIDIA delivered a beat-and-raise, but the market expected more — and concerns surfaced about circular client financing and off-balance-sheet risk reminiscent of 1990s structures. While Jensen Huang reiterated structural tailwinds in accelerated computing and agentic AI, the market was unconvinced.

Seasonality argues for upside, but liquidity argues otherwise. For now, liquidity is winning.

Macro & Policy Watch: Data Divergence, Global Liquidity, and Fed Vote Math

The macro landscape is growing more contradictory.

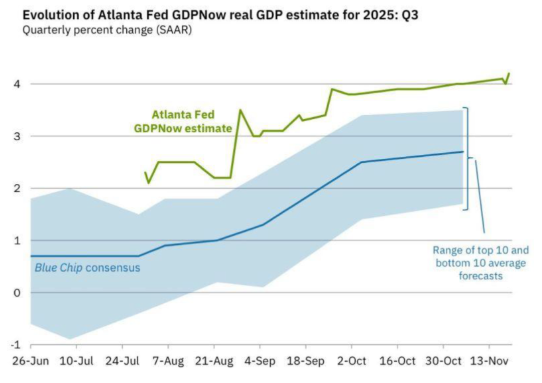

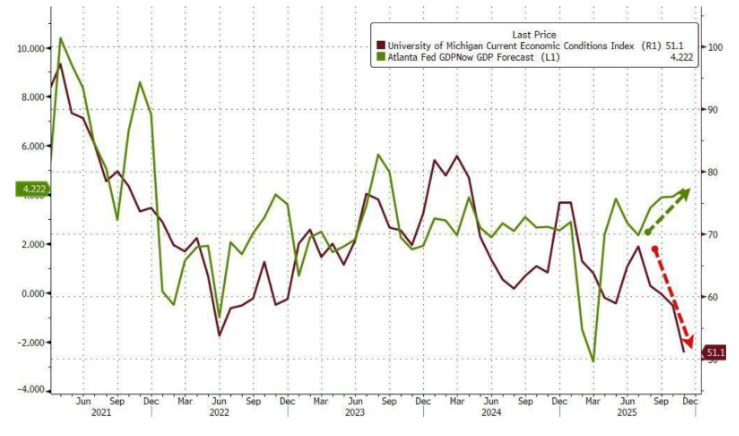

The Atlanta Fed GDPNow model prints a robust 4.2% for Q3 — far above economist expectations — while the University of Michigan sentiment index collapses.

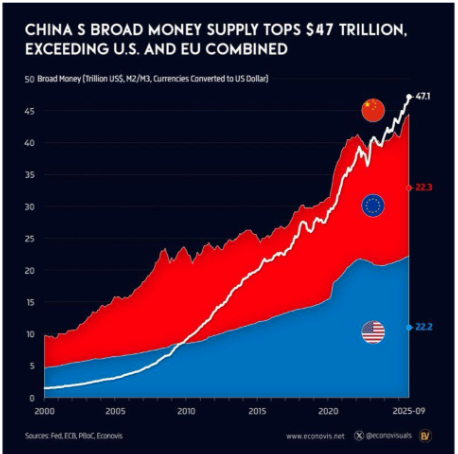

Globally, liquidity is stirring. China’s money supply now exceeds that of the U.S. and EU combined, a structural force that remains under-appreciated but will inevitably flow into global risk assets.

Japan re-entered centre stage with a massive ¥110B stimulus package under PM Takaichi — targeting AI, semiconductors, and advanced manufacturing. The Bank of Japan is simultaneously monitoring a USDJPY pivot zone, raising the probability of FX intervention or even a rate hike.

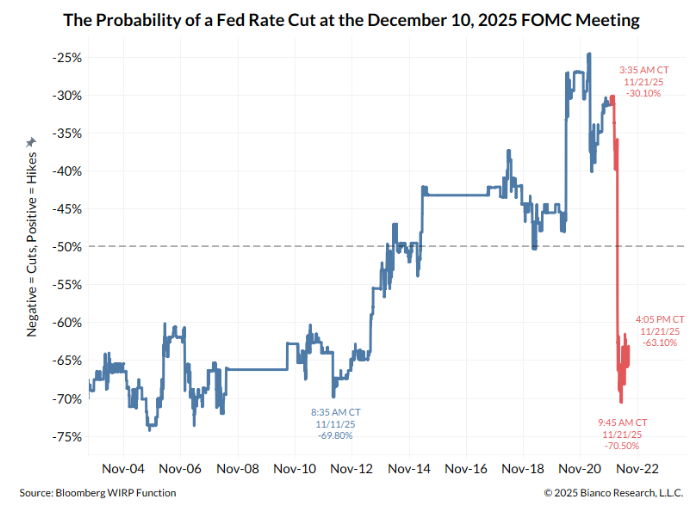

But the week’s biggest macro theme was the FOMC vote math.

Based on member speeches, the PDF maps the December FOMC breakdown as:

- 5 against a cut

- 5 for a cut

- Powell and Jefferson are uncertain

Then John Williams signalled support for a cut — effectively pushing Powell into the dovish column.

Markets reacted sharply.

Yet the probability settled around 63% due to deep uncertainty: a narrow 7-5 vote has not occurred since 1983, and the Fed has no formal tie-breaking process for a 6-6 outcome.

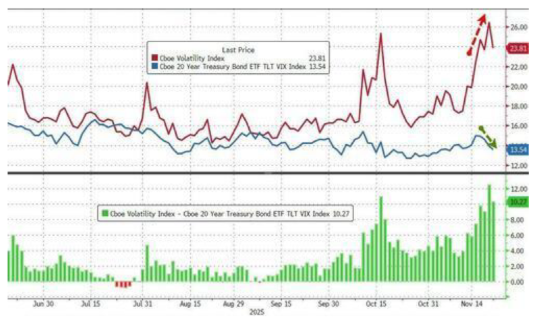

Bond volatility (MOVE) eased while VIX stayed elevated — a peculiar split that reflects liquidity stress without credit panic.

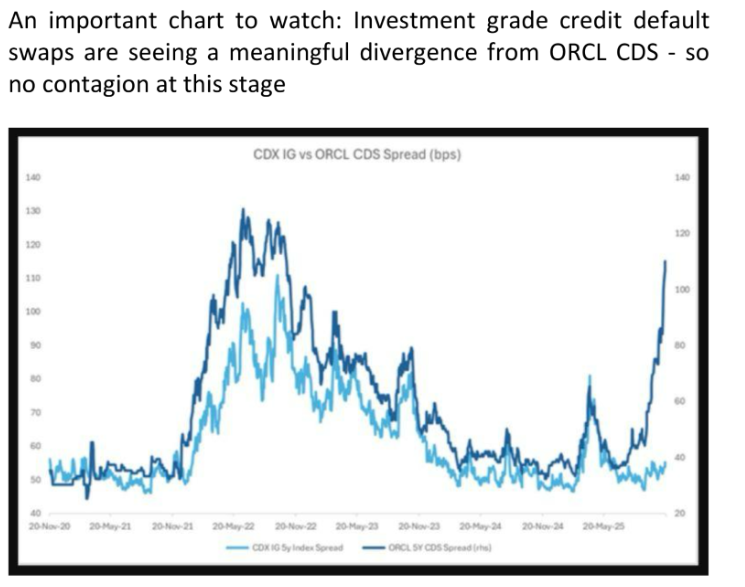

Credit concerns resurfaced around Oracle, while the Blue Owl financing withdrawal highlighted tightening conditions beneath the surface.

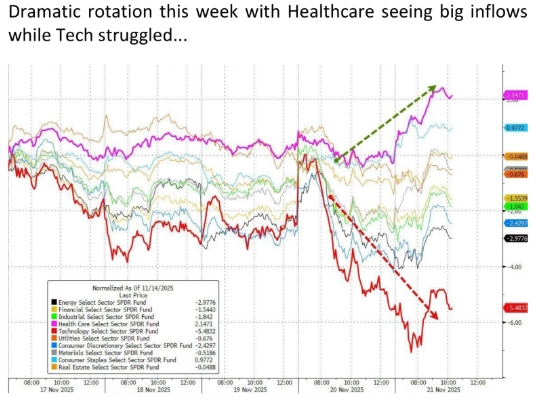

Flows into defensive sectors — particularly Healthcare — underscore rising macro caution.

Technical & Sentiment Breakdown: Fragile Setups and Rotational Stress

Markets remain choppy and indecisive. Intraday rallies continue to fail as volatility-control models sell into strength and liquidity remains thin. Hedge funds continue rotating defensively, while retail and long-only investors persist in buying dips — but the forced-selling dynamic still dominates short-term flows.

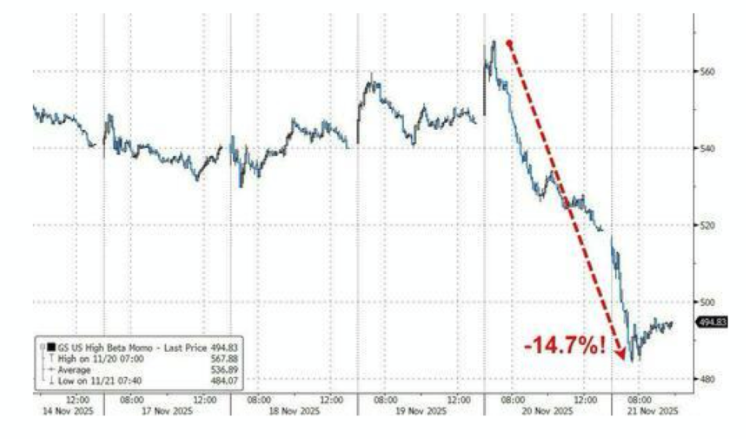

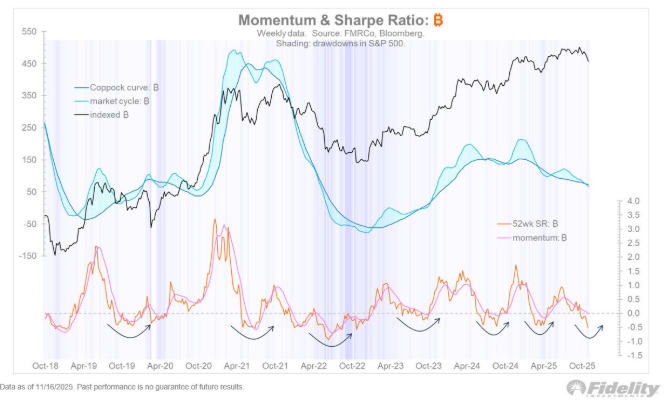

Momentum stalled sharply, posting one of the weakest weeks of the year. Breadth remains narrow, systematic selling remains active, and the unwind of crowded positions continues to pressure the tape.

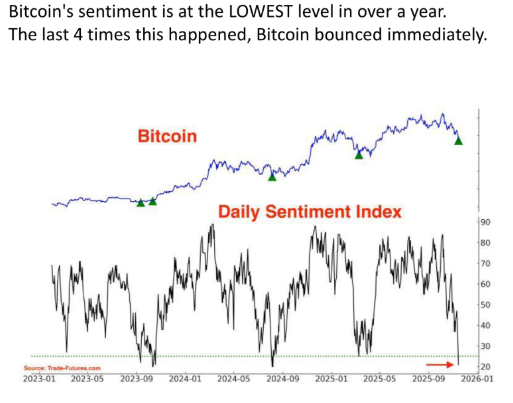

Crypto flows show whales offloading into institutional hands — a late-stage stress signature consistent with forced deleveraging, but one that also sets the stage for a potential counter-trend bounce as positioning resets.

Last Week’s Recap: Liquidity Squeeze, AI Stress, and a Chaotic Reversal

Markets opened the week under sustained liquidity pressure — driven by Treasury issuance, funding stress, and forced selling across high-beta tech and crypto — but stabilised into Friday as seasonal flows began to reappear and Fed vote-math clarified slightly.

Key Highlights

Macro:

Massive Treasury issuance weighed on equities and crypto as cash was pulled toward government paper. Bond markets kept volatility contained even as equity markets absorbed forced liquidations.

AI & Tech:

NVIDIA’s beat-and-raise failed to generate upside as circular financing concerns resurfaced. AI enthusiasm faded into broad tech weakness, with semiconductors and hyperscalers hit hardest.

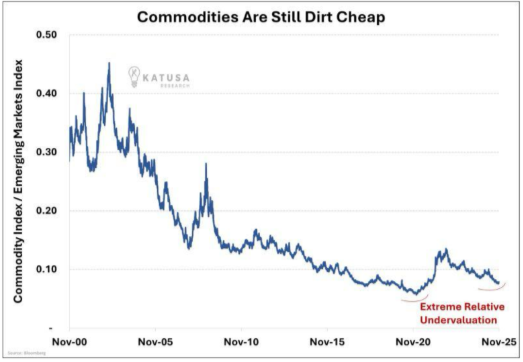

Commodities:

Gold and silver consolidated as margin-related selling hit precious metals alongside the broader risk-off pressure.

Crypto:

Midweek selling — triggered by the linkage between leveraged AI trades and crypto — produced a heavy flush, but underlying accumulation continued at lower levels.

Oil:

Crude drifted lower as weak demand indicators and geopolitical de-escalation headlines capped upside attempts.

The Week Ahead: Data Barrage Meets a Fragile Tape

A holiday-shortened U.S. week still brings a dense macro cluster — especially Wednesday’s data barrage — while Fed officials extend their blackout, leaving markets without verbal guidance during a fragile period.

Monday, Nov 24

- Japan: Labour Day (Holiday)

- Germany: Ifo Expectations, Assessment & Climate

- U.S.: Chicago Fed National Activity Index

- U.S.: Bill auctions, 2Y auction

Tuesday, Nov 25

- Germany: GDP

- Spain: PPI

- U.S.: Retail Sales (rescheduled), PPI, Redbook, House Price Index, CB Consumer Confidence, Pending Home Sales

- U.S.: API Crude Data

- U.S.: 52-week auction, 5Y auction

Wednesday, Nov 26

A macro storm:

- Core Durable Goods

- Core PCE (Q3)

- Q3 GDP + Price Index + Sales

- Trade Balance

- New Home Sales

- Chicago PMI

- Beige Book

- U.S. 4W, 8W, and 7Y auctions

Thursday, Nov 27

- U.S.: Thanksgiving (Holiday)

- Global data: Eurozone sentiment, NZ retail sales, Italian indicators

Friday, Nov 28

- Japan: Tokyo CPI, Industrial Production

- Germany: CPI

- Eurozone: Retail Sales

- Canada: GDP

- U.S.: Chicago PMI

Alpha Takeaway: A Wave-4 Reset with Melt-Up Potential — If Liquidity Behaves

The market’s foundation remains fragile. Liquidity strain, Treasury supply, and forced selling continue to distort short-term behaviour — yet the broader structural roadmap remains intact: a wave-4 reset, followed by a Q1 push and a major Q3 2026 high.

Equities

A counter-trend rally remains likely if Thursday’s lows hold. A break below them risks delaying the Santa rally and extending the wave-4 chop.

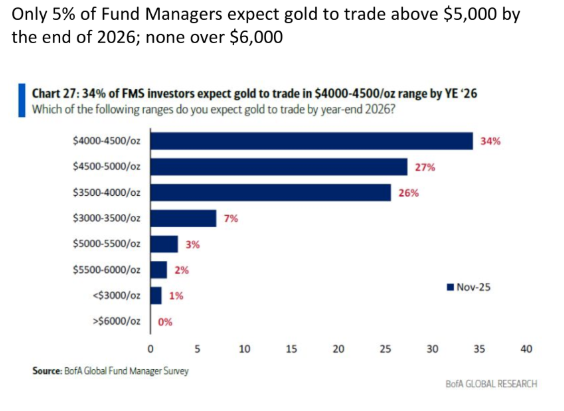

Gold & Silver

Momentum paused as metals absorbed margin-linked selling, but structurally they remain bullish — especially if risk assets see another wave of volatility.

Crypto

Institutional absorption signals the bottoming process is advancing, despite elevated volatility and forced liquidation pockets.

Macro

The December cut leans likely, but the unprecedented vote split means volatility will be dictated by how narrow the vote is — not just the outcome.

Trade the liquidity, not the narrative. The melt-up case lives — but only if the market survives wave-4 without a deeper liquidity accident.