Melt-Up Momentum, Fed’s Pushback, and Breadth at Breaking Point

Markets closed October with a powerful bid, fueled by structural earnings strength, a historic AI capex cycle, and a Trump–Xi trade pause that lowered geopolitical temperature. Yet beneath the surface, pressure points are quietly building. The melt-up narrative is gaining conviction, but the tape is narrow, liquidity is wobbling at the edges, and Powell just reminded traders that December is not a one-way bet.

This is still a bull. But it’s a bull with a pulse — not a machine. And right now, that pulse is elevated.

Market Overview: Melt-Up Meets Micro-Cracks

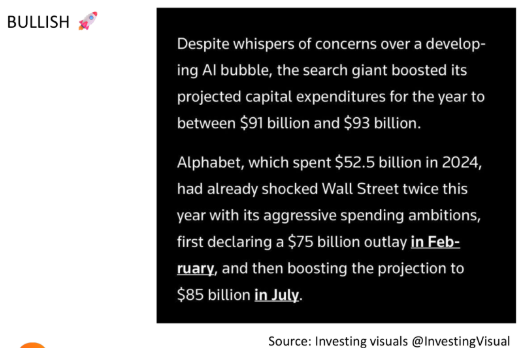

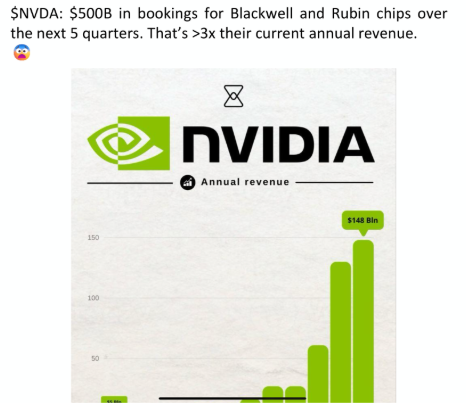

Trump and Xi delivered a one-year trade truce — not a victory lap, but a confidence anchor. MAG5 earnings reinforced the AI capital cycle, with Amazon and Alphabet leading execution while Meta’s capex surge tested sentiment. Nvidia’s roadmap keeps pulling forward demand, and the market is finally acknowledging the public-private investment flywheel powering US tech leadership.

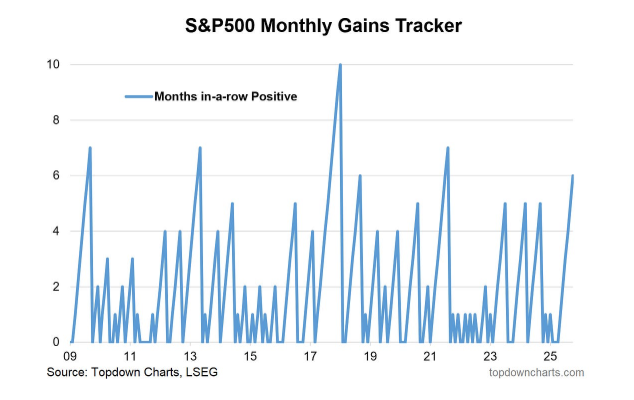

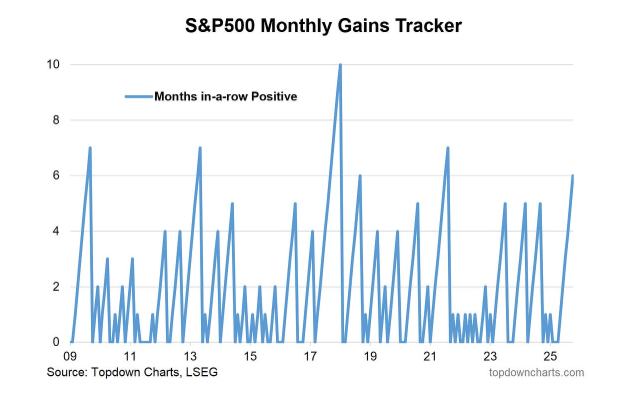

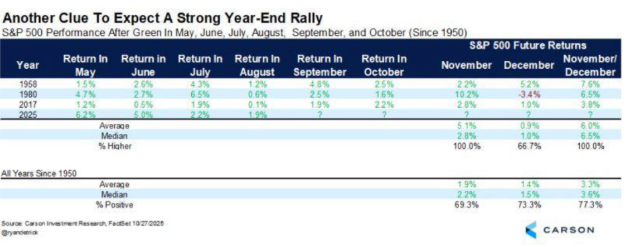

The S&P 500 ended October +2.27%, its sixth straight monthly gain, historically a precursor to further strength. November seasonality remains the strongest month on record.

However, leadership continues to shrink. The S&P printed an all-time high with 80% of components closing red — the most negative breadth ever recorded on an ATH day.

This is peak-thrust price action powered by the heaviest balance-sheet winners. It is not a sign to fade the market blindly — late-cycle rallies can run harder and longer than logic permits — but it does require discipline in entry timing and sector selection.

Macro & Policy Watch: The Fed Cut — With Conditions

The Fed delivered the expected cut, but Powell applied the brakes on market exuberance, pushing December cut odds lower:

“December is not a given.”

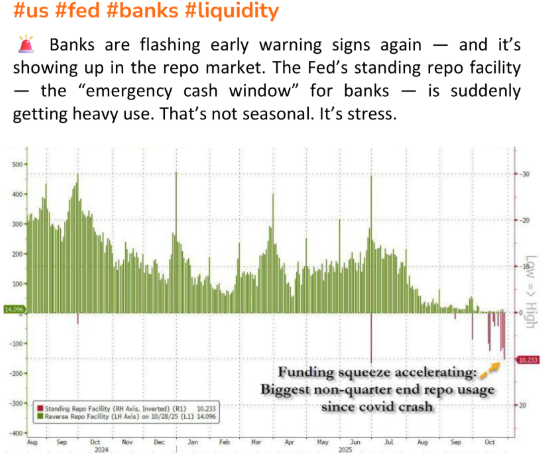

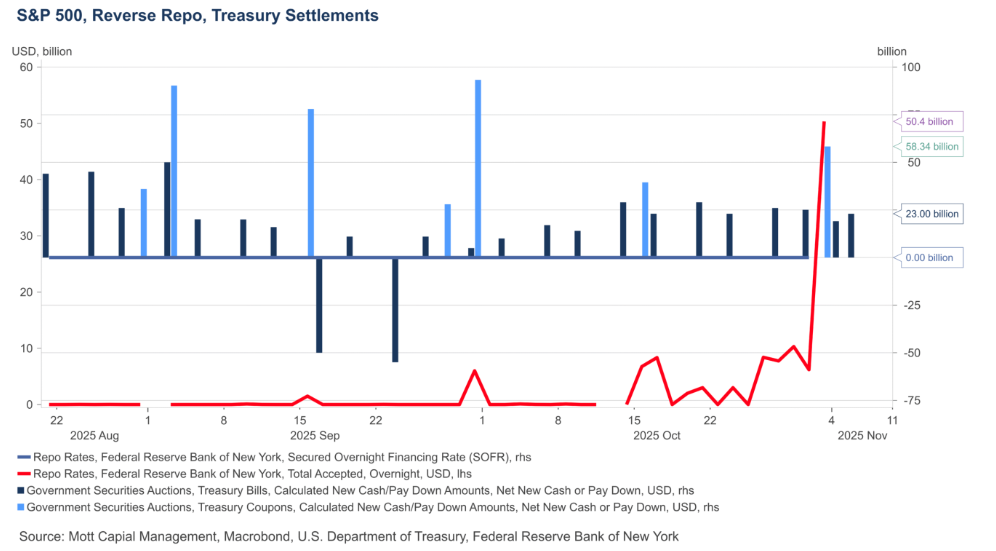

The message shook complacency. QT ends December 1st, shifting the liquidity map toward a quasi-QE regime as maturities are reinvested. Yet repo usage spiked to the highest level since 2021 — a funding stress signal worth respecting as cash tightens under the surface.

Geopolitically, the US-China truce stabilises short-term risk, but semiconductor protectionism and supply-chain sovereignty continue. Europe’s semiconductor seizure signals that this remains a global industrial arms race.

Tariff litigation moves to the Supreme Court this week. If reciprocal tariffs are ruled illegal, cash refunds could generate a temporary liquidity pulse; if preserved, inflationary pressure persists into 2026. Markets are positioning for volatility, not policy whiplash.

Technical & Sentiment Breakdown: Strength on Stilts

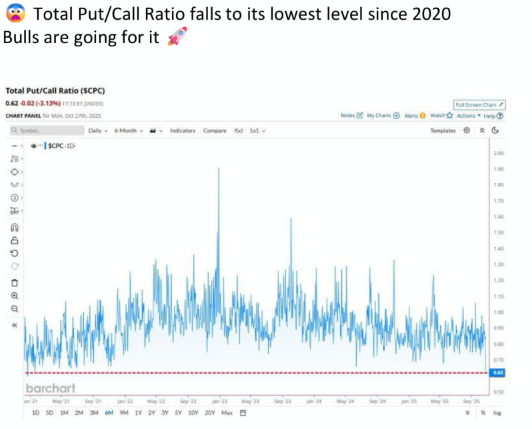

Breadth deterioration is now structural, not situational. Semiconductors continue to lead, but the distance from long-run averages is widening. Extreme call activity, collapsing put-call ratios, and short-covering squeezes signal late-stage chase behaviour.

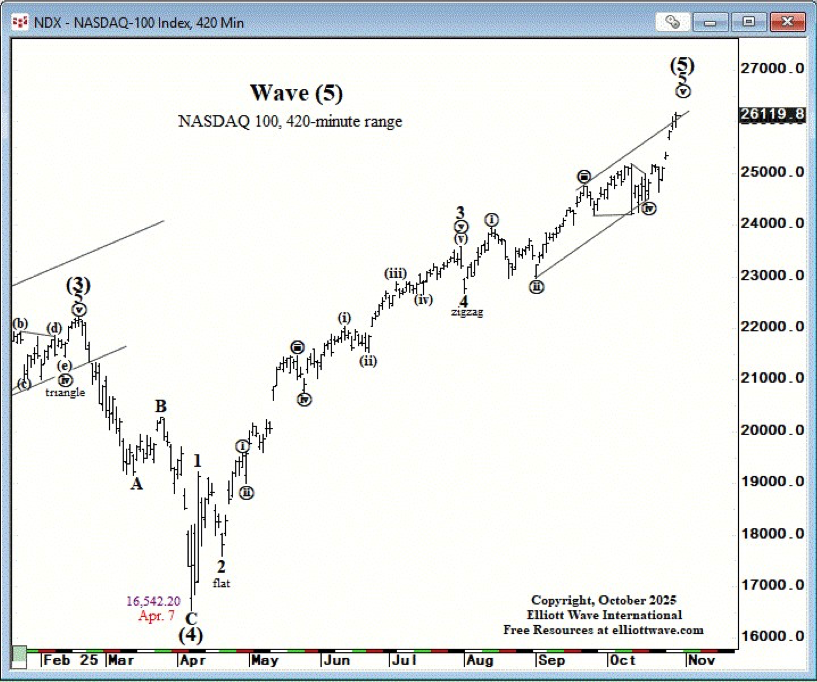

The Nasdaq shows overthrow characteristics. This is constructive long-term but fragile short-term — the kind of structure where shallow dips matter and sloppy entries get punished.

Momentum remains bullish. Participation does not. The tape can still run, but investors must respect the dynamic:

- Buy weakness, not strength

- Ride leaders, avoid laggards

Recent price action also reflects forced flows — particularly in mega-caps — while many mid-cap and cyclical pockets continue to lag. This is still a market where strong names grind higher, but weaker parts of the tape remain under pressure, reinforcing that rallies are being driven by capital concentration rather than broad risk appetite.

Last Week’s Recap: Earnings, Liquidity Signals, and Commodity Rotation

Markets kicked off cautiously but rallied into Friday as Powell’s tone shifted from “cut path certainty” to “data-dependent caution,” while the Trump–Xi optics improved sentiment, and earnings reinforced the structural bull case. Liquidity questions surfaced via repo activity, but equity flows remained firm.

Key Highlights

Macro

- Powell cooled expectations for a December cut, moving markets from ~95% certainty to a coin flip.

- QT ends December 1st, supporting liquidity.

- Repo stress appeared, signalling funding pressure under the surface.

China

- A one-year trade truce eased geopolitical tension.

- Semiconductor policy remains confrontational.

- Supply-chain nationalism is entrenched, not receding.

Earnings

- Megacap tech confirmed another wave of AI spending into 2026+.

- Alphabet and Amazon executed strongly.

- Nvidia’s deal cadence accelerated.

- Meta’s debt-funded capex put pressure on sentiment but affirmed competitive necessity.

Commodities

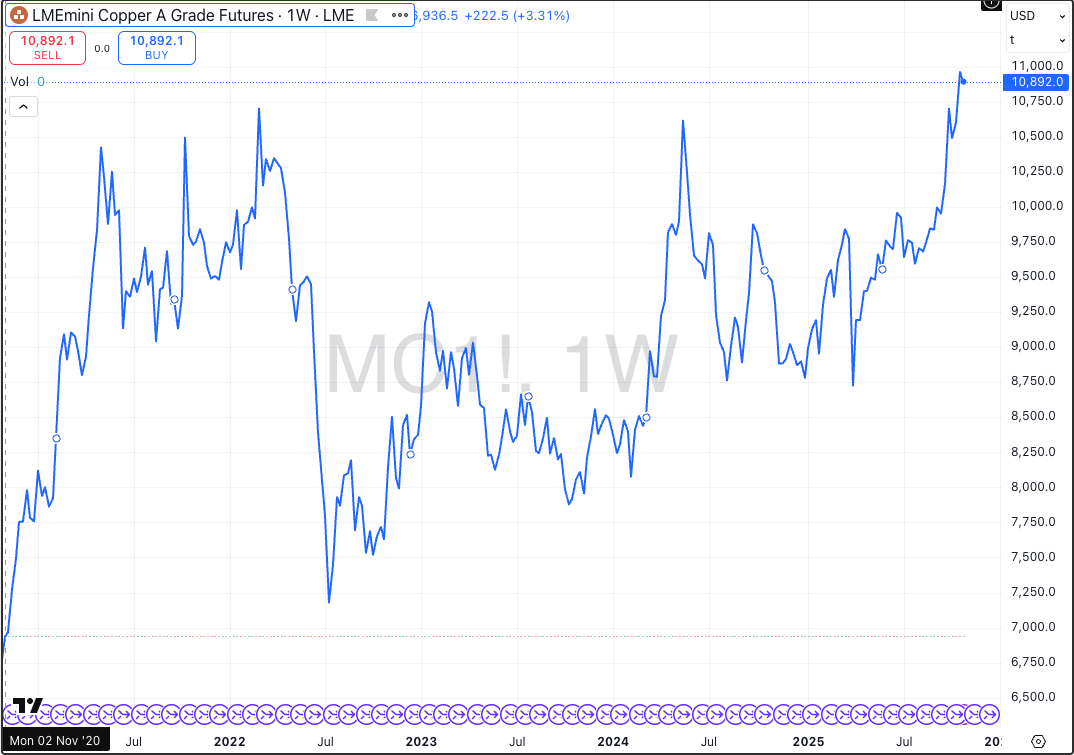

- Copper confirmed super-cycle leadership on supply tightness and industrial capex.

- Gold broke $4k, tested lower, and stabilised — still structurally bullish but vulnerable if USD firms.

Crypto

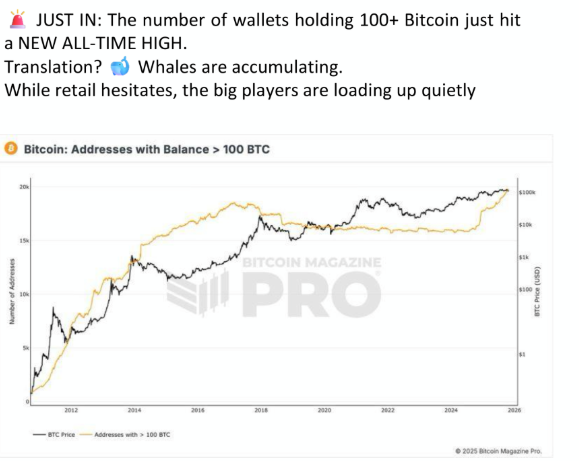

- No “Uptober” rally; crypto remains range-bound as policy delays weigh.

- Large wallet accumulation continues — long-term investors are quietly positioning.

The week reinforced a maturing melt-up dynamic: strength remains concentrated and liquidity-sensitive.

The Week Ahead: Central Banks, Shutdown Data Filters, and Earnings Rotation

Four major central bank decisions and a broad earnings slate shape the week ahead. With the US government data limited, traders will lean on ISMs, PMIs, ADP, and Challenger job cuts to gauge labour elasticity and inflation stickiness.

Monday, Nov 3

- Japan: Culture Day (Holiday)

- France: Industrial Production

- U.S.: ISM Manufacturing, PMI, Bill Auctions

- Earnings: Berkshire Hathaway, Palantir, Hims & Hers

Tuesday, Nov 4

- RBA Decision

- India: Manufacturing PMI

- U.S.: JOLTS, Redbook, GDPNow

- Earnings: Uber, Shopify, Pfizer, AMD, BP, SuperMicro

Wednesday, Nov 5

- India Holiday – Guru Nanak Jayanti

- Eurozone & UK PMIs

- U.S.: ADP, ISM Services

- Earnings: Novo Nordisk, McDonald's, Qualcomm, ARM

Thursday, Nov 6

- BoE Decision

- Swiss Unemployment

- US Productivity & Unit Labour Costs

- Earnings: Moderna, Airbnb, DraftKings, ConocoPhillips

Friday, Nov 7

- China Trade Balance

- U.S.: Michigan Sentiment & Inflation Expectations

- Canada: Jobs

- Earnings: Duke Energy, Six Flags, Wendy’s

Alpha Takeaway: Melt-Up Still On — But Breathing Heavy

The melt-up remains intact. Liquidity is shifting bullish, earnings leadership is real, and seasonal flows favour continuation. But breadth fractures, option skew, and funding stress argue for precision and patience.

Equities

Leadership is narrow but powerful.

- Buy controlled dips in dominant tech & infra names

- Avoid laggards below trend

- Rotation risk rises if earnings disappoint in second-tier names

Gold & Silver

Gold’s break and retest near $4,000 is pivotal.

- A hold maintains the structural bull

- Failure opens $3,800–3,550 risk

- Watch real yields and the USD path into December

Crypto

- Positioning reset is broadly complete.

- Institutional accumulation continues.

- If liquidity stabilises post-QT shift, crypto could break ranges in late November.

Macro

The cut was expected; the conditional tone was not.

- The liquidity shift on December 1 is key

- If funding stress abates, upside resumes

- If not, volatility returns quickly

The market remains bullish — but levered, narrow, and sensitive to liquidity tremors. Trade strength tactically, buy weakness methodically, and stay aware that this phase rewards discipline more than enthusiasm.