Volatility Awakens, Tariff Shocks, and the Return of “Voltober”

After months of low-volatility drift, markets finally got their reality check. Positioning had become stretched, sentiment complacent, and the VIX complacently low. It only took a spark — Trump’s latest tariff salvo against China — to send volatility ripping higher and equities tumbling into a long-overdue correction.

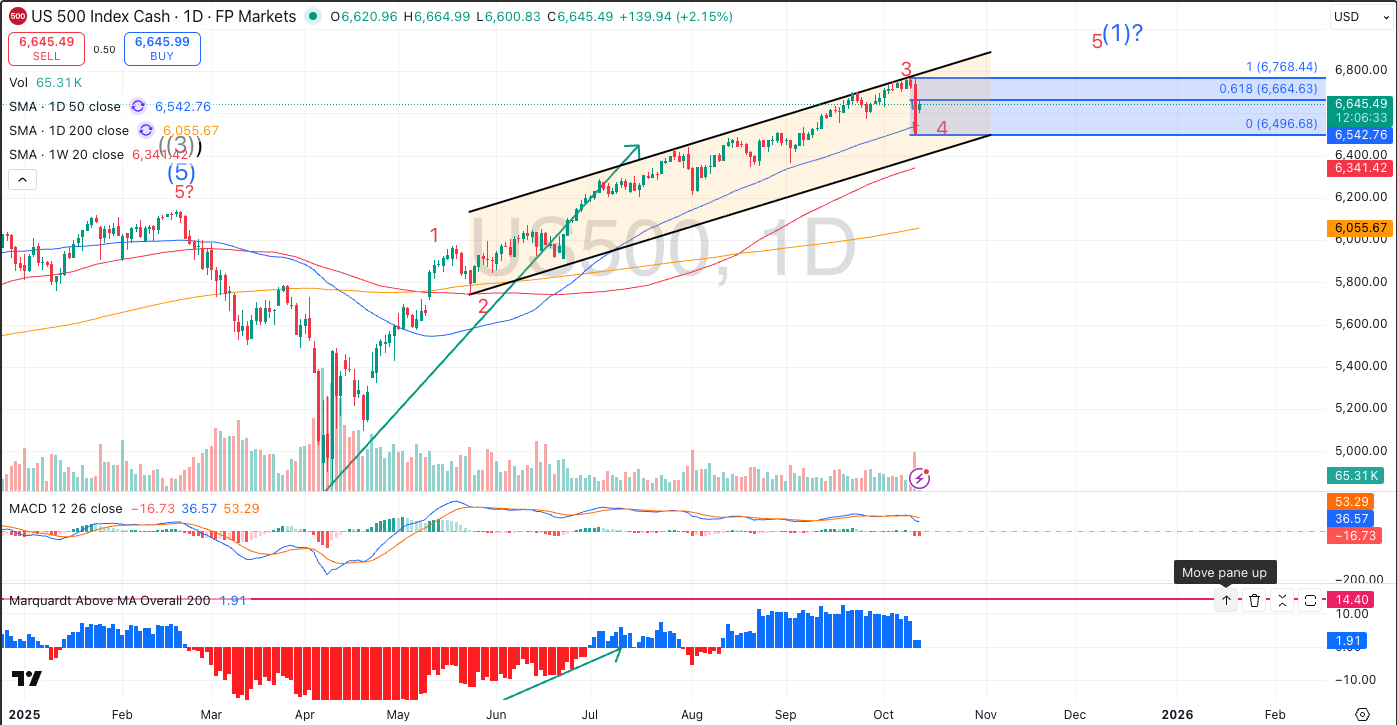

Friday’s close on the lows was ominous, but as any trader knows, Fridays rarely mark the bottom. The futures bounce that followed looks more like a reflex than a reversal — we’ll need a classic three-wave pattern and a solid retest of late-session lows to confirm that the impulsive uptrend is still intact.

Market Overview: When Calm Turns to Chaos

Everything was ticking along in “low-vol land” — until it wasn’t. The U.S. equity rally, driven by concentrated AI mania and short-volatility flows, finally met resistance. Fundamentals hadn’t broken, but sentiment clearly had.

Trump’s renewed spat with China, suggesting Xi “won’t want to put China into depression,” became the catalyst for what the charts had already warned: divergence, stretched sequences, and non-confirmations at all-time highs.

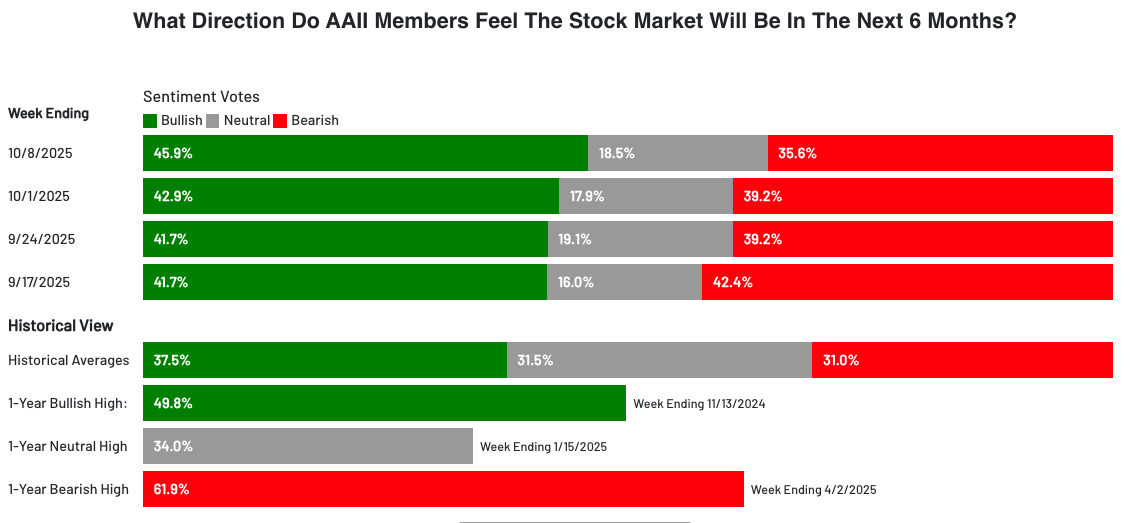

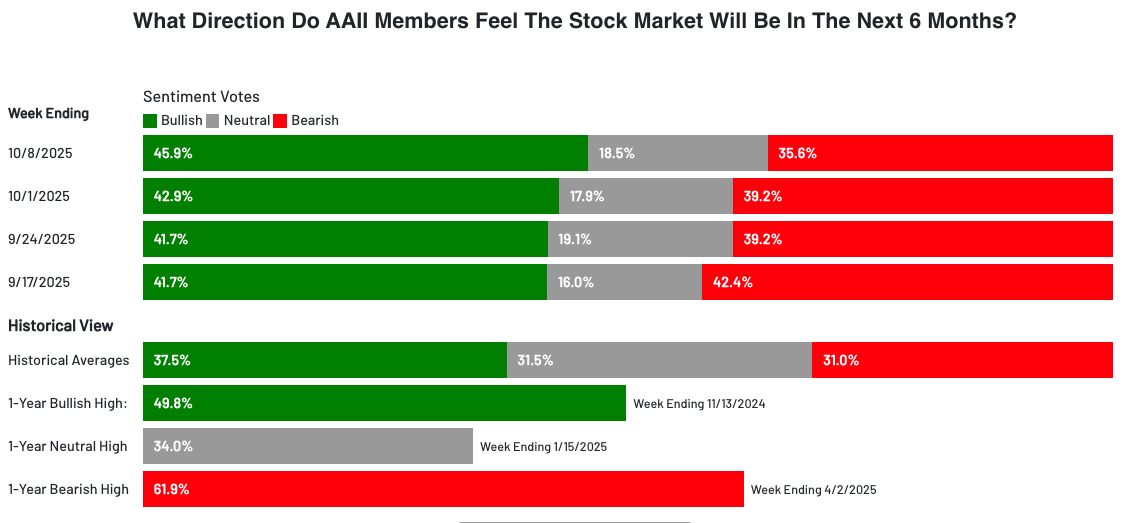

The AAII sentiment data confirmed the froth — high bulls, few bears, and almost no undecided participants — a classic setup for a sentiment snapback.

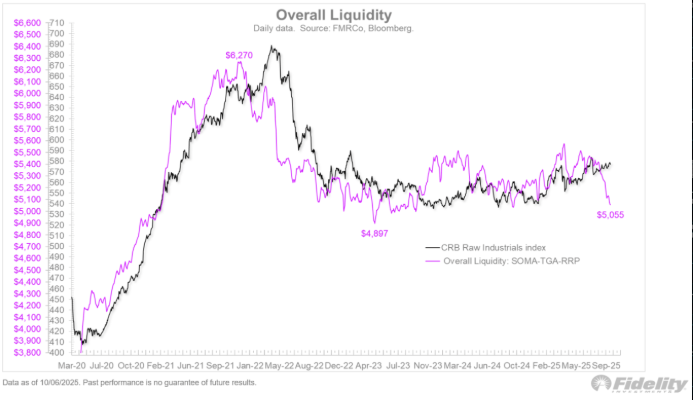

Even the put-call ratios reflected complacency: a 0.81 equity P/C and only moderate index hedging via a 1.2 index ratio. But the market had quietly flipped to a negative gamma regime into Friday’s close, setting up a self-reinforcing sell dynamic that reversed only after Monday’s technical rebound.

Macro & Policy Watch: Fragile Fundamentals and Political Fractures

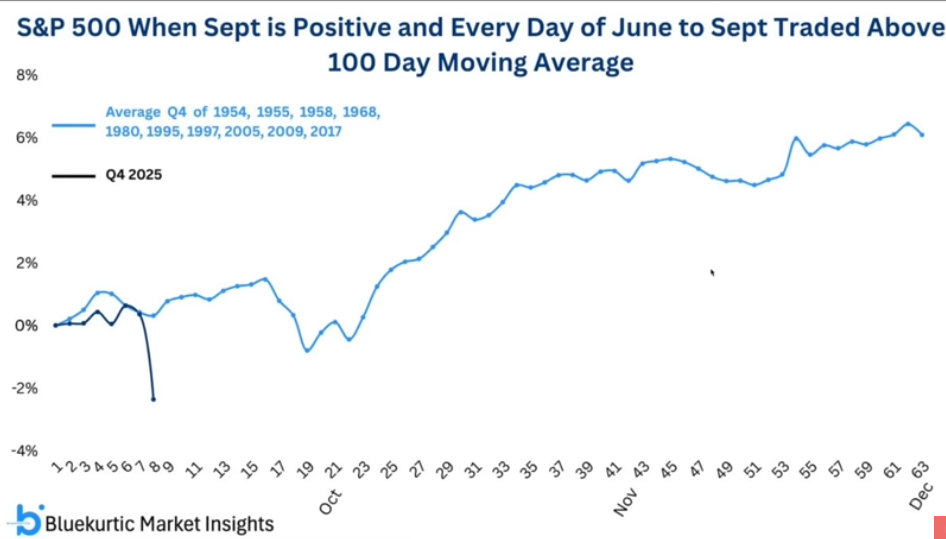

The macro backdrop remains fragile but not broken. Fundamentals suggested a seasonal pullback was overdue. The U.S. government shutdown continues to cast uncertainty across data releases — even as the Bureau of Labour Statistics recalled key workers to deliver the CPI print due October 24th, which remains critical for Social Security adjustments and Fed calibration.

In Europe, data disappointed again — Germany’s numbers remain weak, while ECB officials turned hawkish amid structural stagnation and political fractures in France. The IMF and World Bank meetings this week may set the tone for global coordination — or confirm the lack of it.

Geopolitical Watch

- Trump landed in Israel to bask in the peace-deal spotlight (without the Nobel).

- France continues to simmer politically, Japan’s coalition collapsed, and Argentina needed yet another U.S. Treasury bailout.

- The U.S. military payroll risk due to the shutdown looms large.

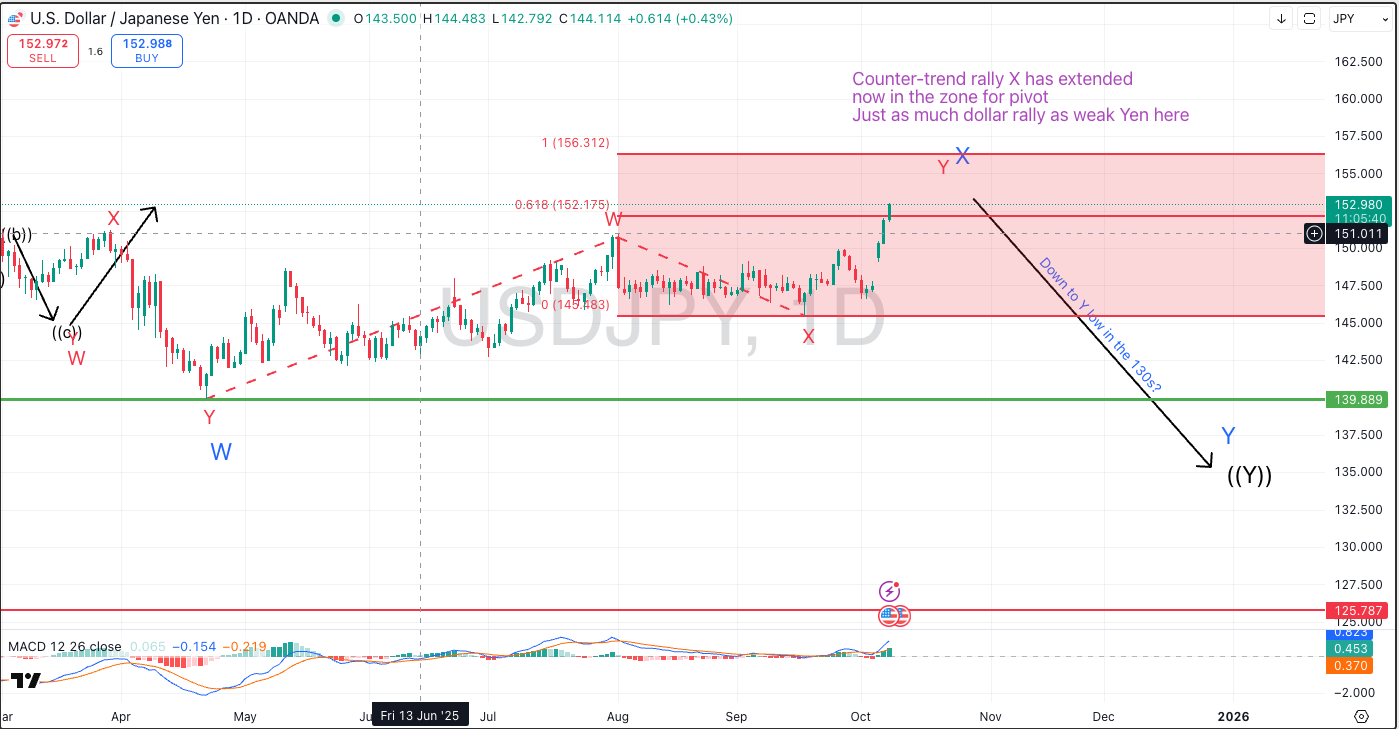

Monetary policy chatter adds complexity: the Fed remains open to defensive cuts but faces rising inflation stickiness. ECB leans hawkish, the BoE is split, and Japan’s transition of leadership could redefine its tightening trajectory. Yen stability remains a key macro pivot.

Technical & Sentiment Breakdown: The Volatility Reprice Takes Hold

The technicals screamed pullback long before headlines hit. SPX futures bounced 1.5%, touching resistance near 6650 — just below the 61.8% Fib retracement — but failed to sustain it.

Negative gamma dynamics faded as call-heavy positioning around 6500 cushioned downside volatility. Still, the shift from positive to negative gamma zones is a trader’s warning: liquidity providers are no longer stabilisers.

The VIX’s move into the mid-20s and the reversal of its 20-day moving average is crucial. We now have “Voltober” in full swing — both implied and realised vol are rising in tandem for the first time since the Japanese carry-trade unwind earlier this year.

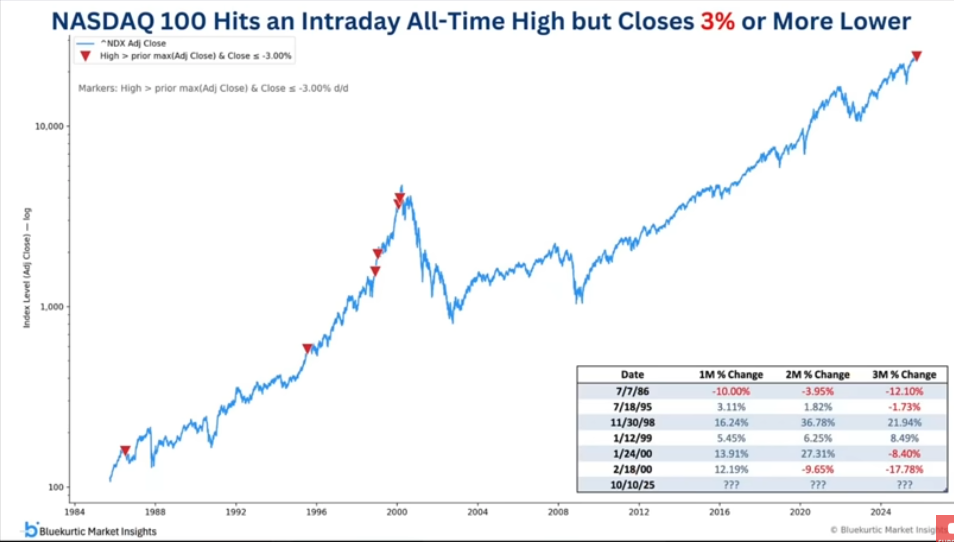

The divergence between NAS100 and its volatility index (VXN) — highlighted last week — played out precisely. That’s textbook sentiment exhaustion.

Volume data also confirmed distribution:

- Only ~50% of SPX components remain above their 200DMA

- New highs-minus-lows turned decisively negative over shorter windows

Still, the broader uptrend remains technically valid if Friday’s low holds. An expanded flat correction (wave 4) scenario could mean Friday marked a mid-structure low — not an end.

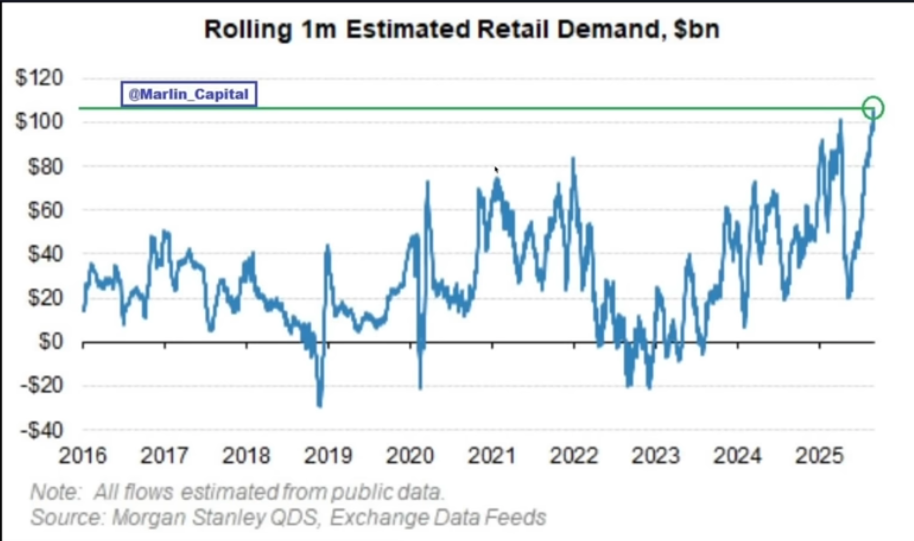

Retail leveraged exposure is at extremes again — margin longs, leveraged ETFs, and call buying are crowding the tape.

Last Week’s Recap – Voltober Begins

The long-awaited correction finally arrived as Trump’s renewed tariff rhetoric against China triggered a surge in volatility and flushed out crowded risk positions.

- U.S. indices snapped their low-volatility drift as VIX and VXN spiked into the 20s, ending months of calm.

- The selloff was broad-based — led by technology and momentum names — but disciplined, with no signs of panic liquidation.

- European data disappointed again, reinforcing the region’s macro underperformance.

- Japan’s political uncertainty added to global unease.

- Earnings momentum remained resilient.

- Risk flows rotated into commodities, particularly gold and silver, which both broke fresh highs amid renewed safe-haven demand.

Asia lagged, weighed down by China tech and export concerns, while retail sentiment flipped sharply from euphoria to caution. What began as a complacent “Uptober” turned into Voltober — a live test of conviction and positioning discipline.

The Week Ahead – Data Returns, Volatility Remains

With the U.S. still partially shut down, traders will key in on global data, earnings kick-offs, and high-profile Fed commentary ahead of the pre-meeting blackout.

Monday, Oct 13, 2025

- U.S. & Canada Holidays (Columbus Day, Thanksgiving)

- IMF Meetings continue

- Watch early futures positioning and volatility flows

Tuesday, Oct 14, 2025

- U.K. Employment & Wages

- Germany ZEW Economic Sentiment

- U.S. NFIB Small Business Optimism

- Major Bank Earnings: JPM, Citi, BlackRock, GS

Wednesday, Oct 15, 2025

- China CPI/PPI

- U.S. CPI (Key: BLS recalls staff for release)

- Eurozone Industrial Production

- Fed Beige Book

Thursday, Oct 16, 2025

- U.S. Retail Sales & PPI

- Philly Fed Manufacturing Index

- ECB’s Lagarde & Fed Waller speeches

Friday, Oct 17, 2025

- Eurozone Final CPI

- U.S. Housing Starts & Industrial Production

- IMF Annual Meetings (Final Day)

Buyback blackouts peak mid-month, and volatility tends to seasonally rise in October — pullbacks here could be tactical entry zones for year-end positioning.

Alpha Takeaway: Voltober Has Arrived — Risk-On, But Fragile

Markets remain broadly risk-on, but the tone has turned increasingly fragile. AI exuberance, heavy positioning, and stretched liquidity have kept the melt-up alive, yet cracks beneath the surface are widening. The sharp rise in volatility marked a necessary reset — not the end of the trend.

Key Themes

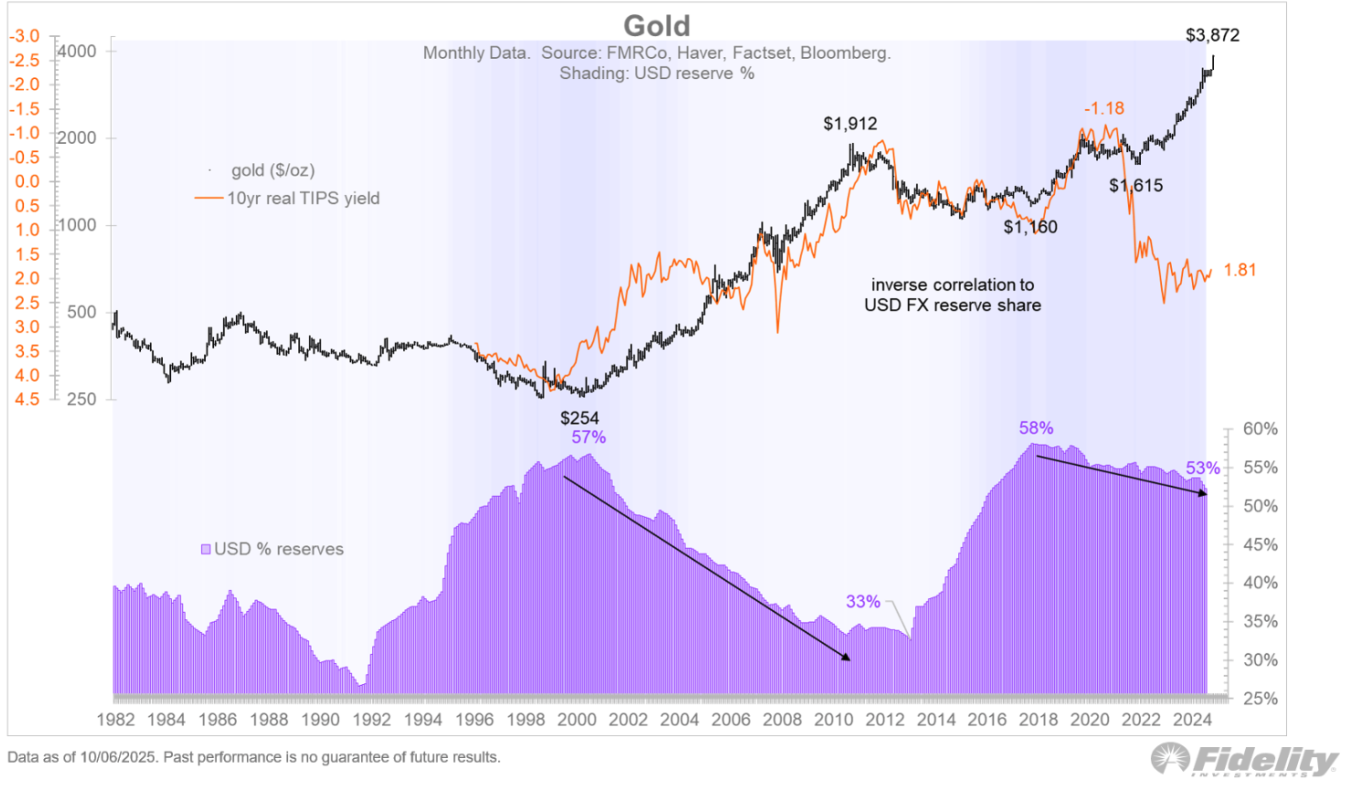

Gold

Gold is pushing into record territory, its rate of change approaching historical extremes — a potential exhaustion zone even as inflows accelerate.

Crypto

Crypto is enjoying its own “Voltober” resurgence, with Bitcoin confirming its wave-4 low and institutional participation expanding.

Equities

Equities remain structurally supported by liquidity, earnings, and dovish bias, but leverage and sentiment are overheated. The base case remains a shallow 5–7% correction before the uptrend resumes into year-end as volatility normalises and breadth stabilises.

“This isn’t a bear market — it’s a volatility reprice. Still in uptrend, still risk-on. Just smaller stakes both ways.”

Our Stance

- Equities: Stay long but trim leverage; buy pullbacks near key support zones.

- Gold & Silver: Momentum strong but extended — partial profit-taking prudent.

- Crypto: Constructive structure; momentum can extend further.

- Macro Focus: Fed data blackout implications, IMF meeting tone, and OPEC’s volume-first policy stance.