Parabolic Moves, AI Mania, and the Wall of Worry

Markets continue to climb the wall of worry, ignoring macro caution as liquidity, leverage, and AI optimism propel equities into parabolic mode. Despite talk of exhaustion, positioning remains aggressive and sentiment confident. Private equity is pouring billions into AI and data centres, even as MIT research warns 95% of these ventures could fail. It’s a classic late-cycle cocktail: abundant liquidity, selective breadth, and traders still “buying the dip” while ignoring the cracks underneath.

Market Overview: Calm Indices, Euphoric Internals

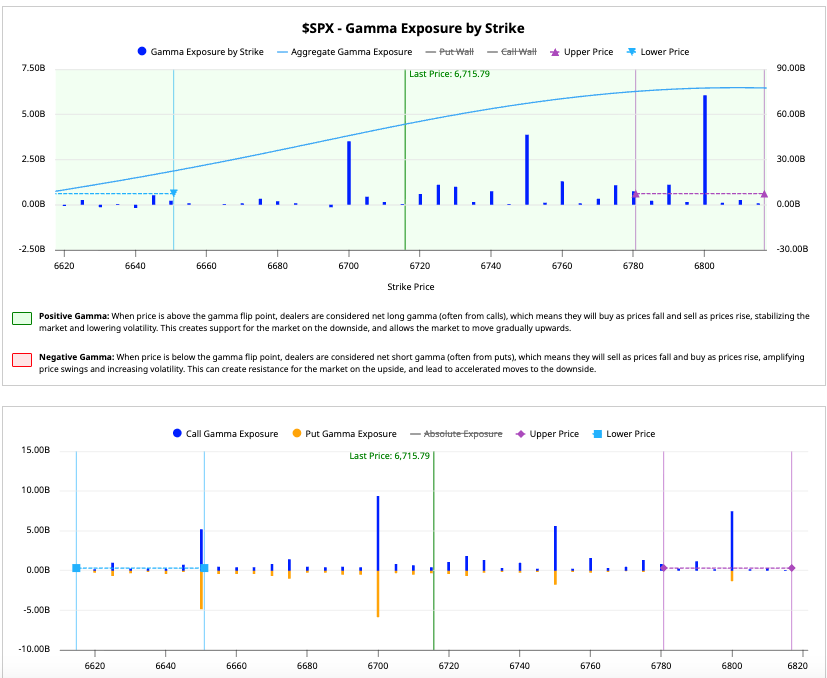

Despite rising recession chatter, the market refuses to break stride. After a brief stretch of negative gamma in late Q3, options positioning flipped back into positive territory — a key driver behind the relentless upward drift.

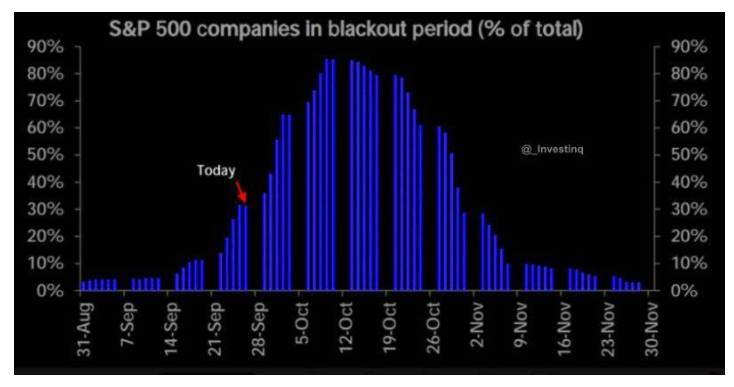

Flows remain robust. Bank of America data confirms renewed equity inflows, while insider selling remains muted. Although buyback blackout windows are emerging, the overall liquidity backdrop stays strong.

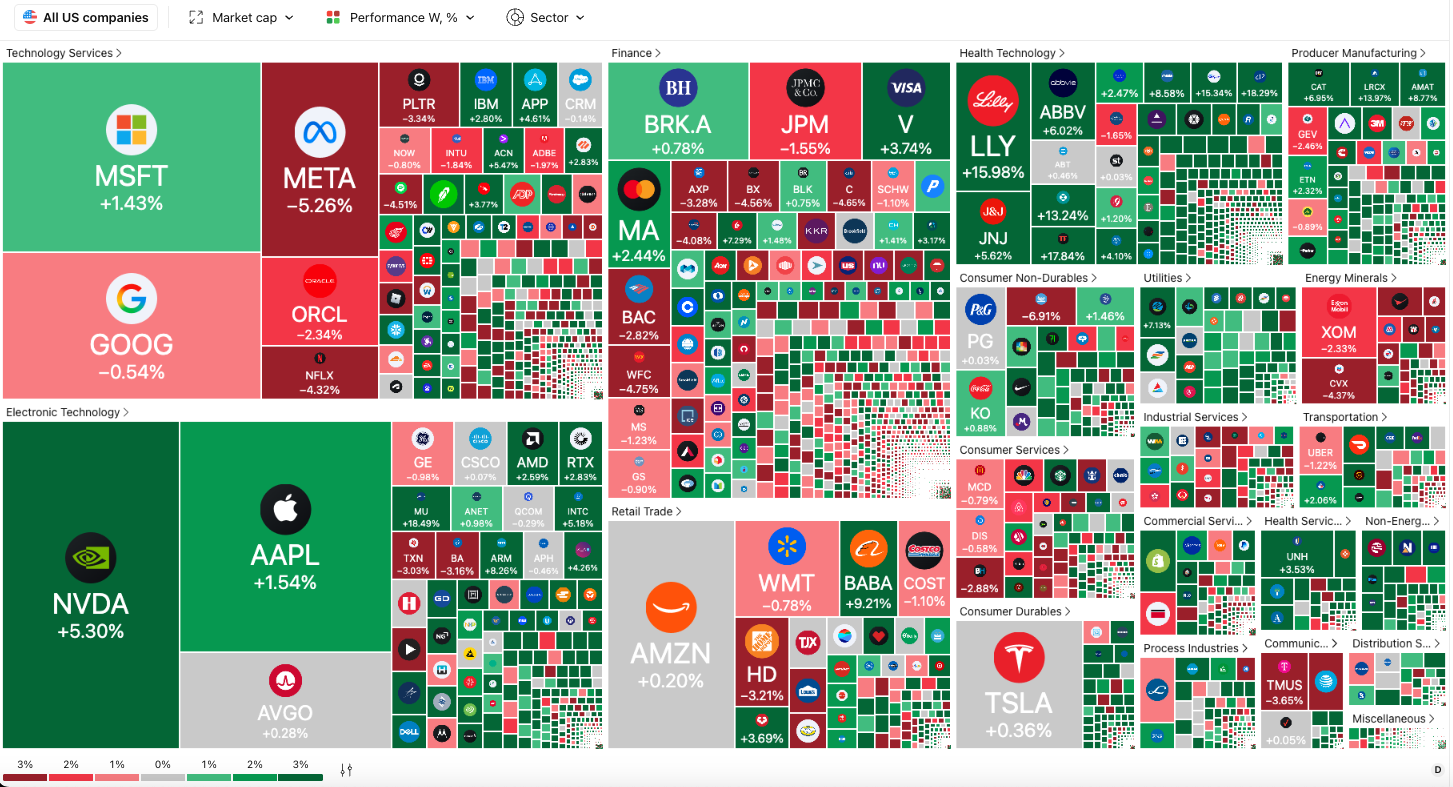

Breadth, too, remains supportive. Advance/Decline lines continue to print fresh highs, defying the “narrow leadership” narrative and keeping volatility pinned.

In short, the market’s surface calm hides mounting leverage and complacency — the same mix that often fuels year-end surges before volatility returns.

Macro & Policy Watch: The Fed’s Blind Spot and Data Delays

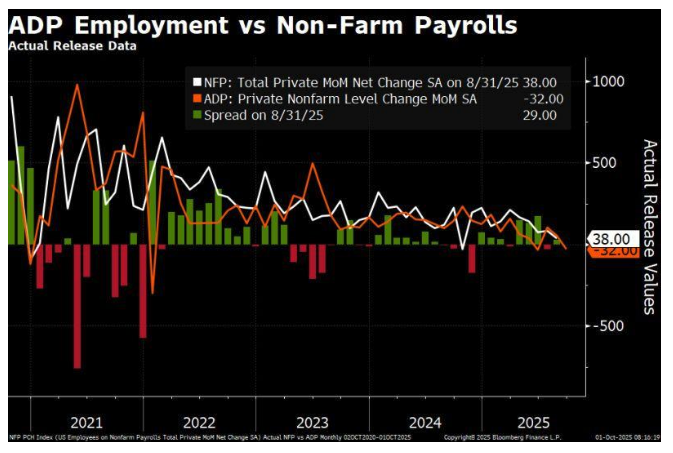

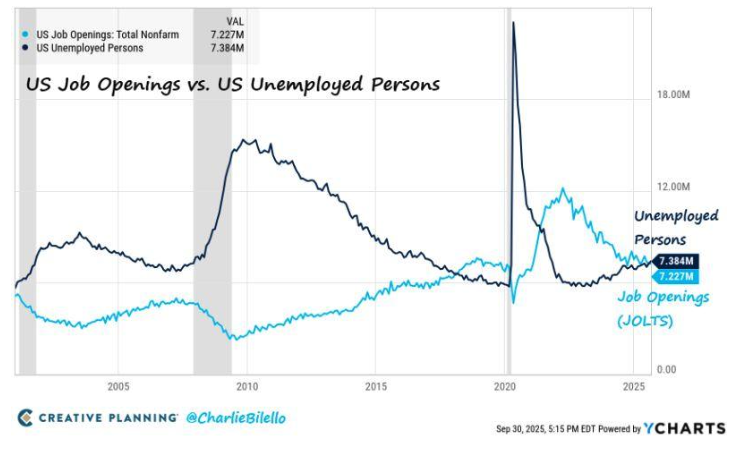

The ongoing U.S. government shutdown has disrupted critical economic data releases — leaving the Fed partially blind. With NFP and CPI potentially delayed, traders are relying on private indicators like ADP and JOLTS, both flashing early signs of labour softening.

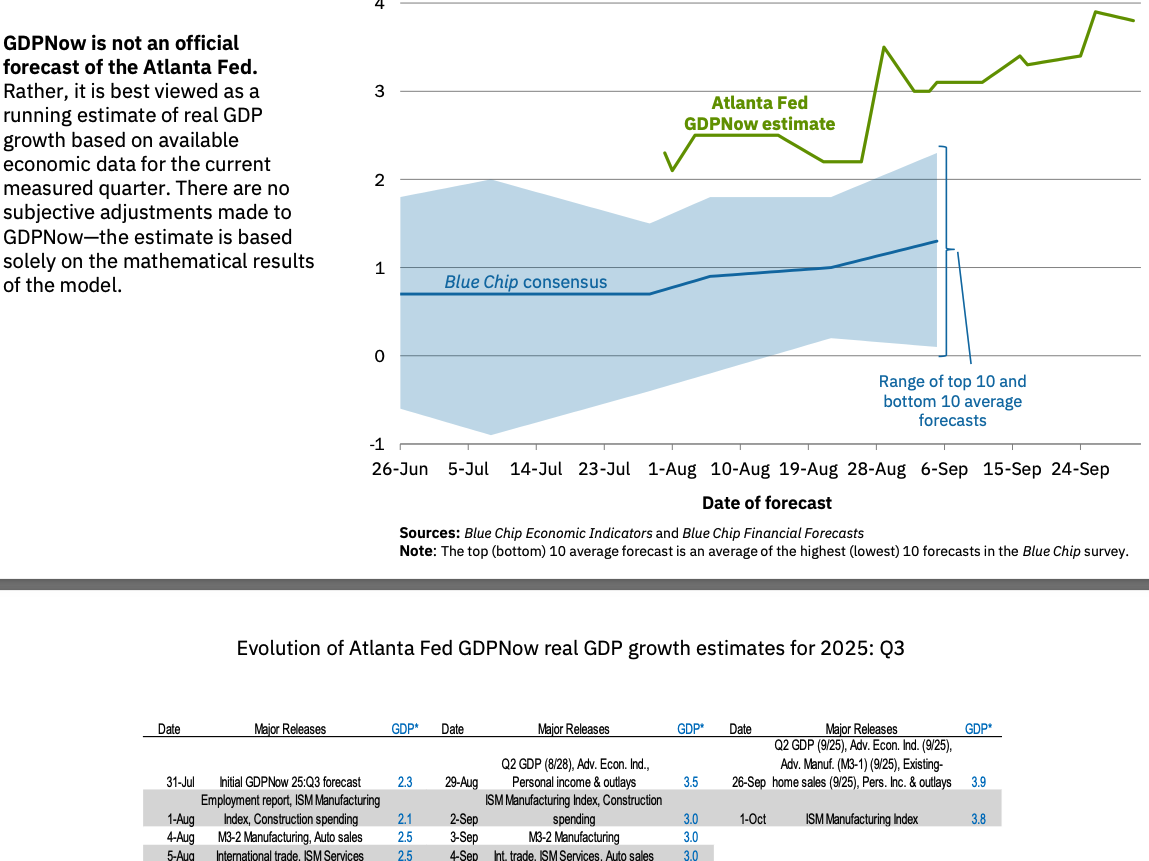

Yet, the Atlanta Fed GDPNow model still pegs Q3 growth at 3.8%, confirming that real activity remains firm.

Yields remain stable, and the bond market shows no panic. Heavy truck sales — a leading recession proxy — are rolling over modestly but not collapsing. Fiscal expansion and policy support next year could easily offset these early signs of fatigue.

The analyst’s note summarises it best: “The key question isn’t if the Fed cuts, but whether it starts cutting inside or outside a recession.” For now, it still looks like the former.

Japan also remains in focus. LDP leader Sanae Takaichi’s policy stance continues to align fiscal spending with BOJ support — reinforcing Japan’s role as a global liquidity anchor.

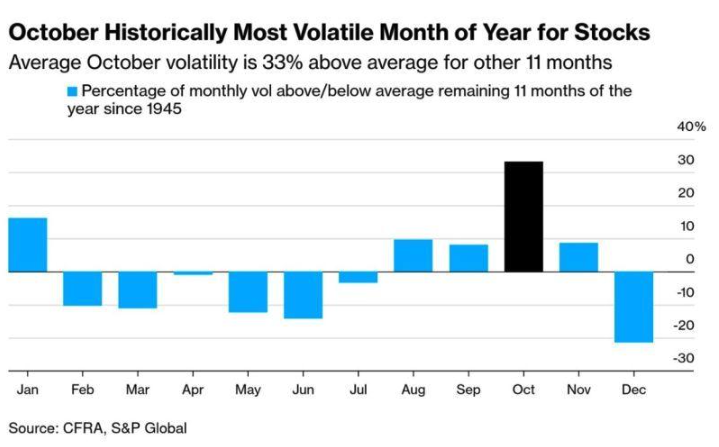

Technical & Sentiment Breakdown: Late-Cycle Leverage and Behavioural Traps

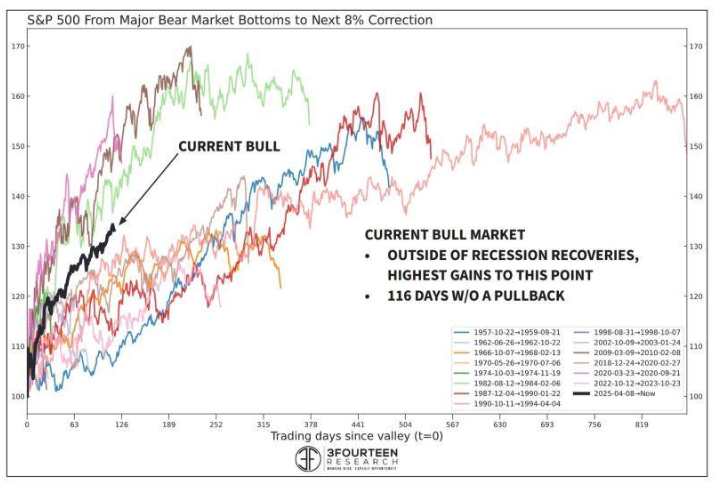

The ongoing rally now ranks as the fourth-strongest bull run in modern history — and the largest non-recessionary one ever. The last three of similar magnitude all paused briefly at this stage before the Q4 melt-up.

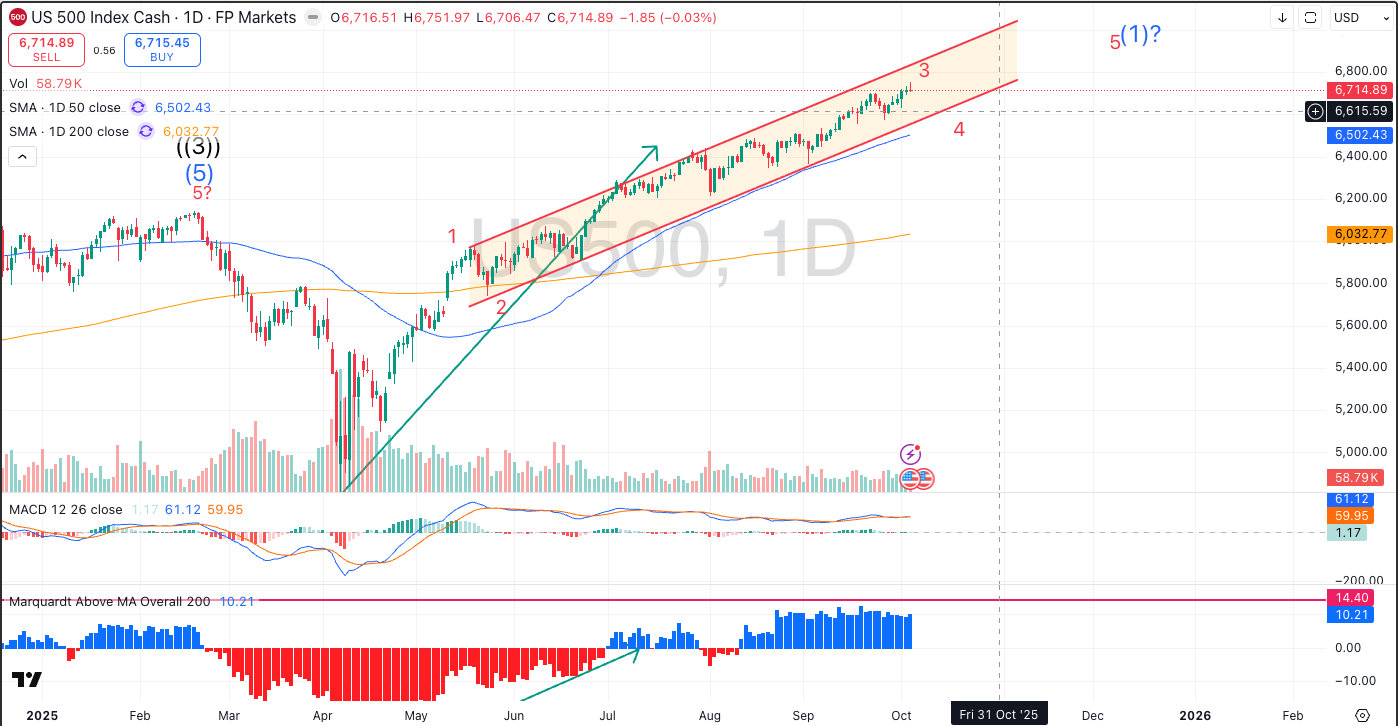

The S&P 500 remains in a structured uptrend, consolidating through an ABC correction around key support zones.

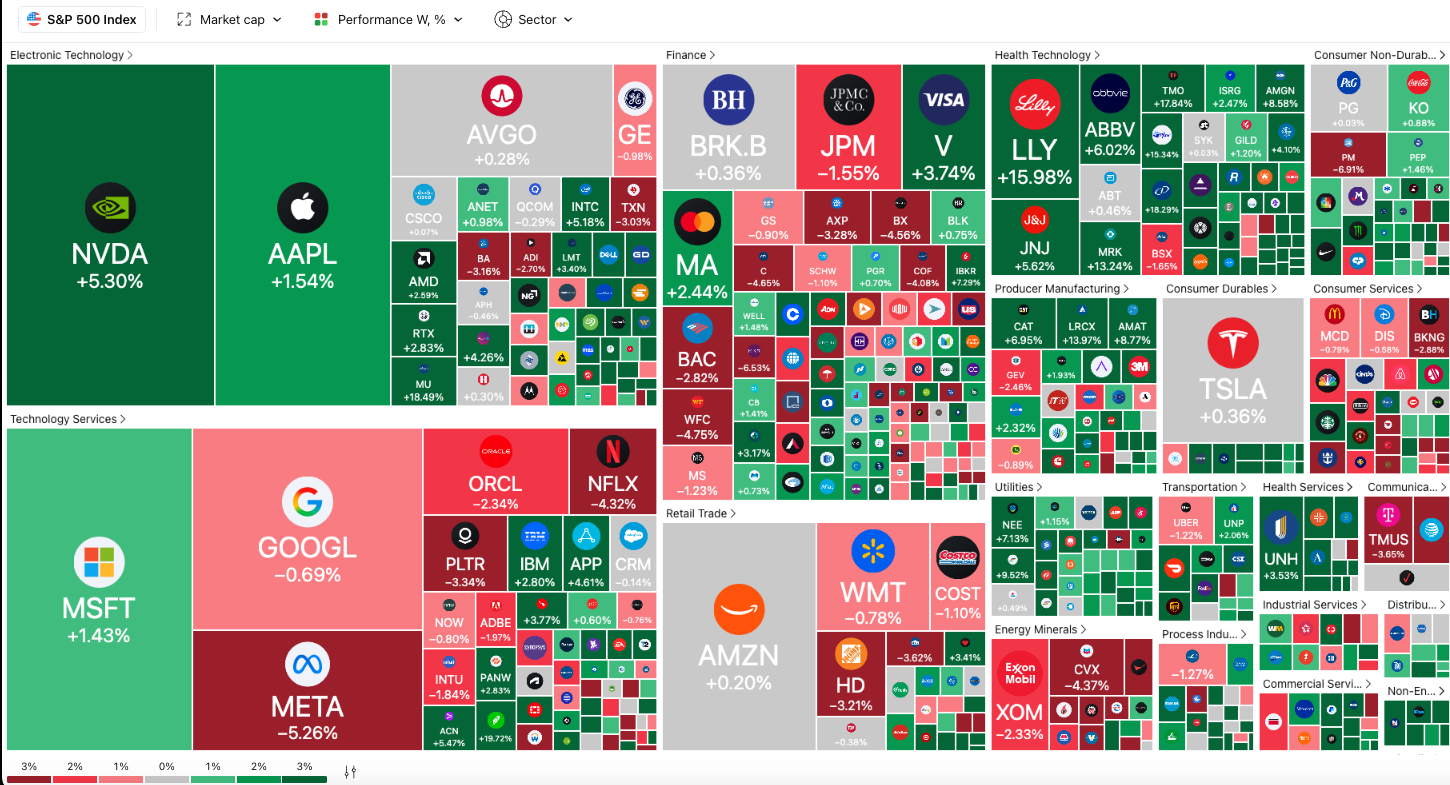

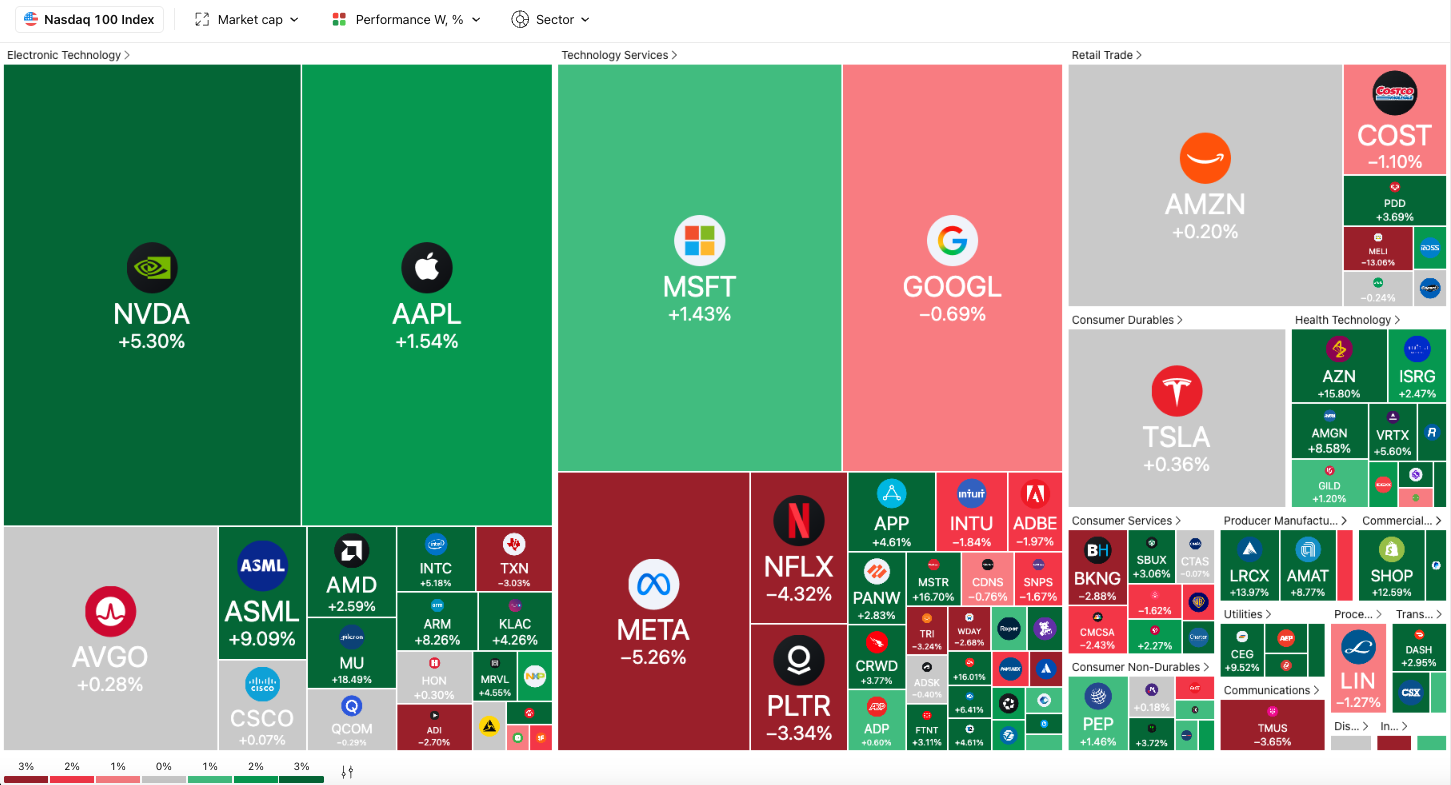

The NASDAQ 100 shows a similar rhythm — strong AI and semiconductor leadership, but emerging divergences between price and momentum. These divergences hint at a potential sentiment inflexion before the next leg higher.

Sector Rotation

- Energy’s prior dominance faded as oil sold off.

- Small caps rebounded on rate-cut optimism.

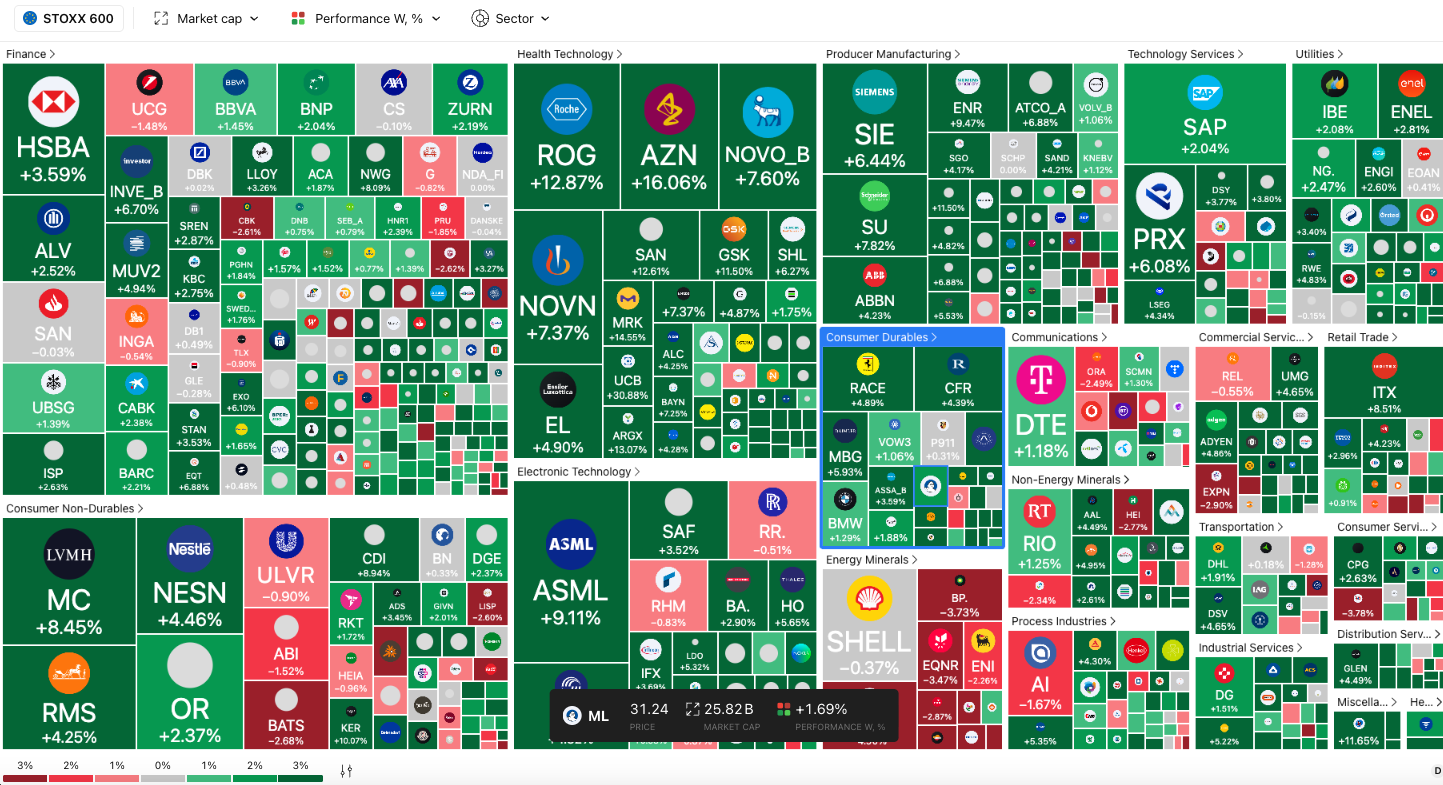

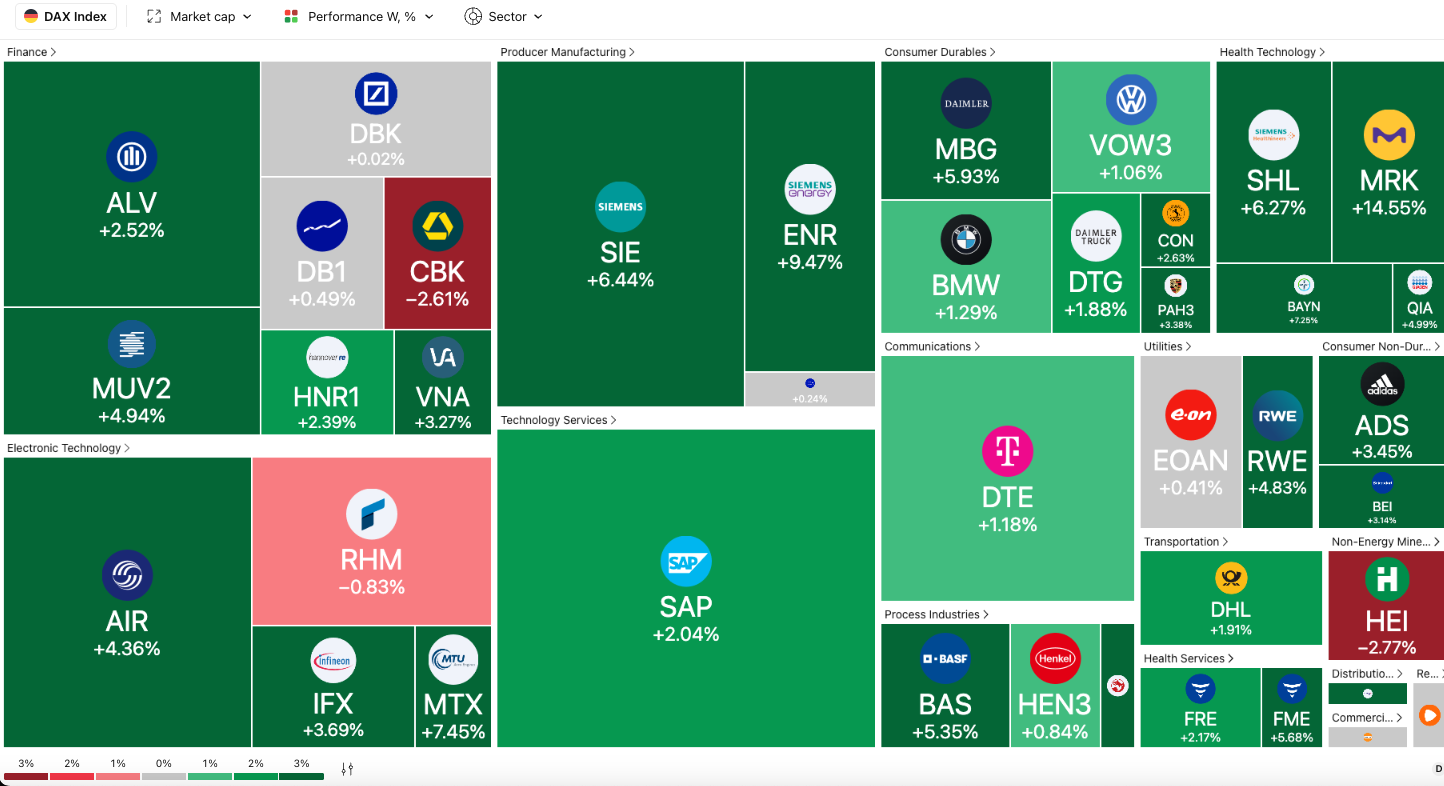

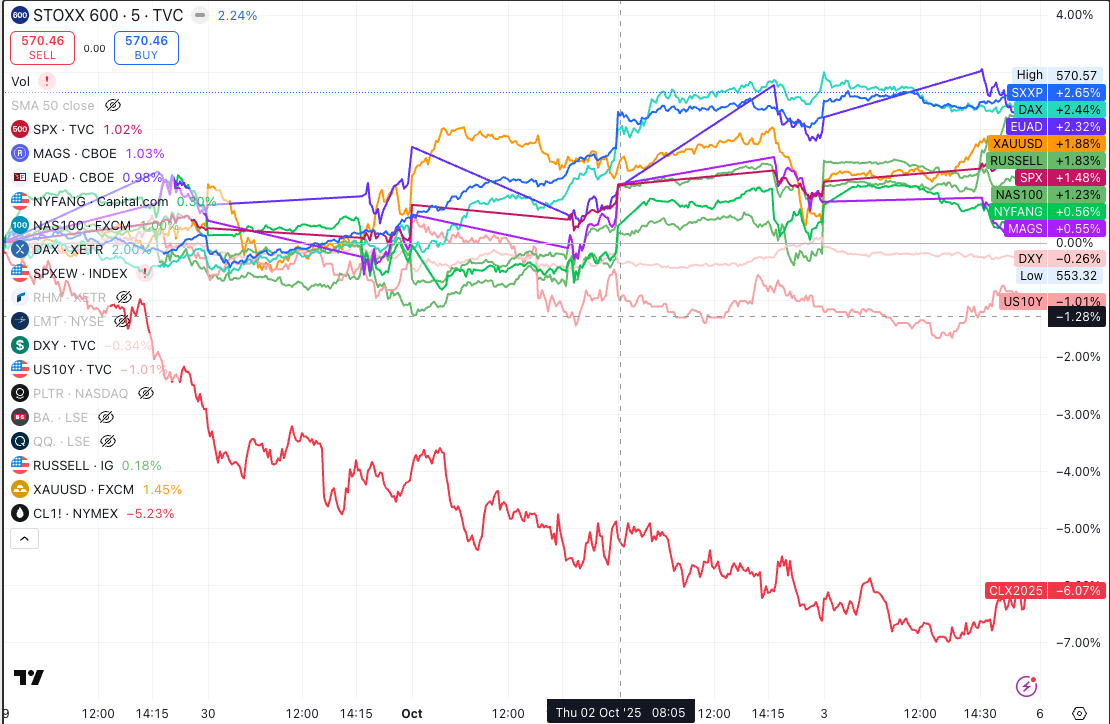

- Europe’s Stoxx600 and DAX continue to outperform, supported by industrials and defence exposure.

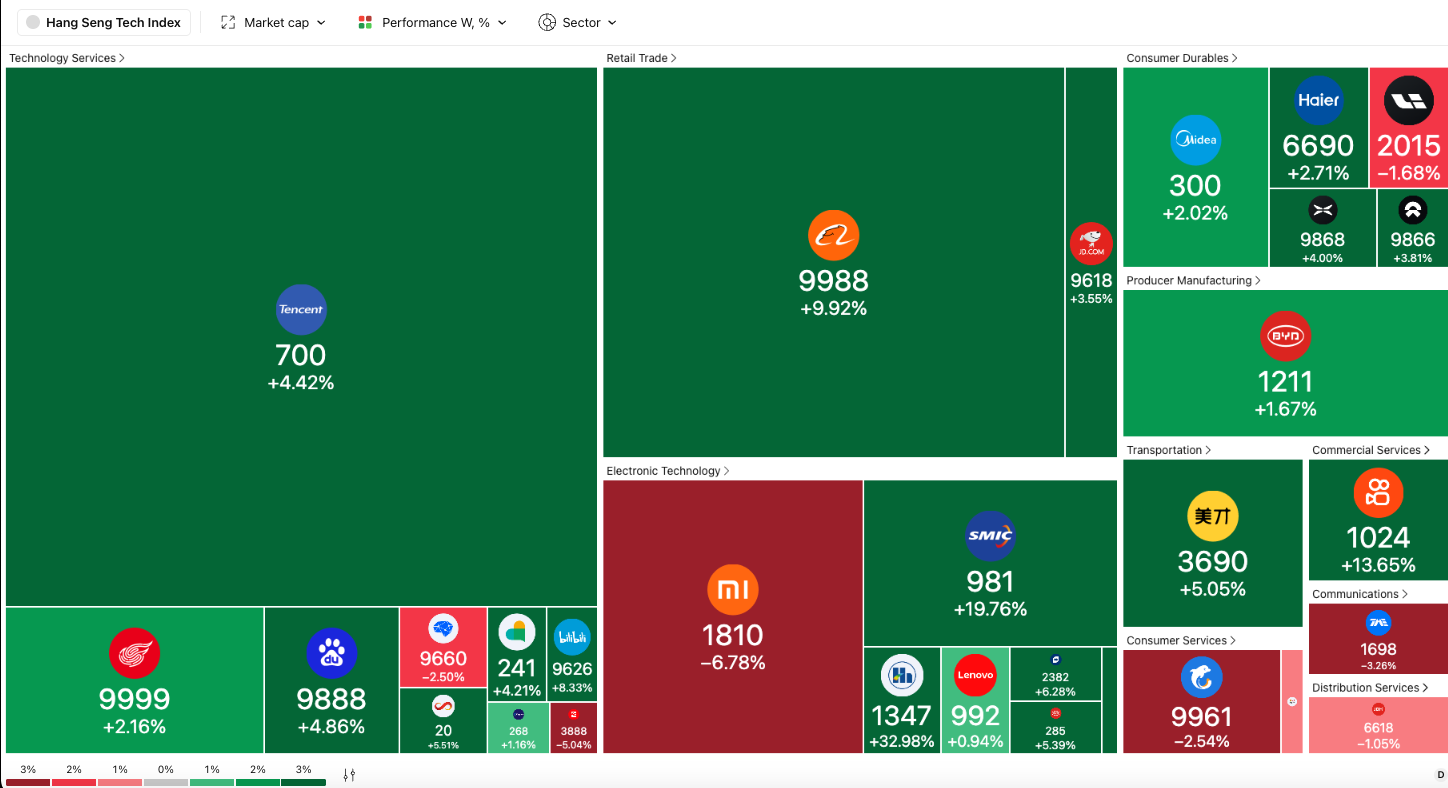

- China’s tech sector remains a standout performer, helped by consistent inflows and improving policy sentiment.

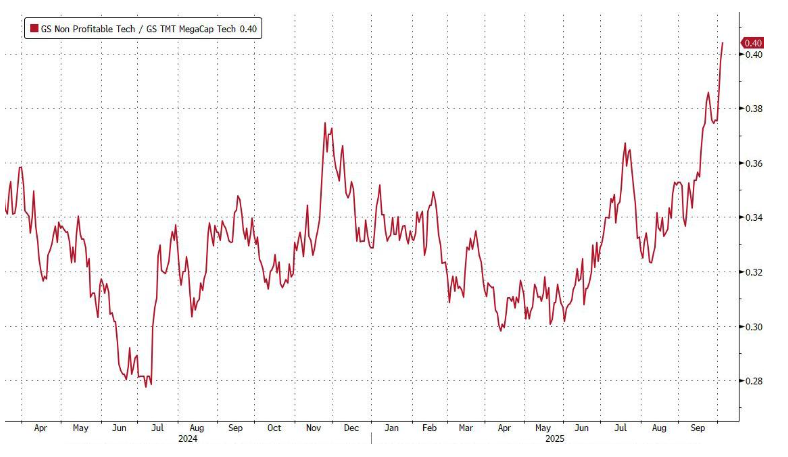

However, the most telling sign of excess is the surge in non-profitable tech stocks — a clear echo of 1999-style risk-taking. The analyst’s warning is blunt: “Buy it until you lose, because when you want to sell, there won’t be any bids.”

Volatility remains compressed, but behavioural sentiment is stretched. Options skew suggests traders are heavily leaning long gamma again — a condition that often precedes volatility shocks when positioning unwinds.

Buyback blackout windows peak mid-month, historically coinciding with tactical lows before year-end rallies.

Despite these cyclical dynamics, the broader message stays the same: the trend is up, participation is solid, and dips remain shallow.

Last Week’s Recap: Uptober Ignites

Markets entered October with strong momentum — risk assets rose broadly across regions and asset classes.

- Europe led with the DAX and Stoxx600 setting fresh highs.

- Gold and Silver continued to surge as safe-haven and speculative demand merged.

- U.S. small caps (R2K) outperformed as rate-cut bets returned.

- Oil sold off sharply after OPEC+ shifted focus to volume over price control.

Asia joined the risk-on tone, with China tech driving inflows and Japan reaffirming fiscal expansion. In the U.S., mega-cap tech consolidated while cyclicals caught up.

The first week of “Uptober” lived up to its seasonal reputation — a broad, liquidity-fueled rally.

The Week Ahead – Macro Data Cluster and Central Bank Focus

With official data limited, traders will focus on speeches, private reports, and volatility dynamics.

Monday, Oct 6, 2025

- China National Day Holiday

- Eurozone Retail Sales, Construction PMIs

- ECB Speakers: de Guindos, Lane, Lagarde

- BOE’s Andrew Bailey

Tuesday, Oct 7, 2025

- JPY Household Spending, NZ Business Confidence

- NY Fed Consumer Inflation Expectations

- Atlanta GDPNow Q3 Update

- Fed’s Bostic speaks

Wednesday, Oct 8, 2025

- RBNZ Rate Decision

- BOE MPC Pill

- FOMC Minutes (September Meeting)

Thursday, Oct 9, 2025

- ECB Meeting Minutes

- Fed Powell & Bowman speeches

- U.S. Jobless Claims (subject to release)

Friday, Oct 10, 2025

- University of Michigan Sentiment

- CAD & U.S. Employment Reports (delayed due to shutdown)

With buyback blackouts peaking mid-month and volatility seasonality turning higher, tactical pullbacks could offer short-term entry points for year-end positioning.

Alpha Takeaway: Risk-On, But Handle With Care

Markets remain firmly risk-on, but the tone is late-cycle and increasingly fragile. AI mania, record liquidity, and heavy positioning keep the melt-up alive, but cracks are forming under the surface.

Key Themes

Gold

Gold is running at record highs, its rate of change nearing historical peaks — a potential exhaustion signal even as inflows accelerate.

Crypto

Crypto is enjoying a classic “Uptober” rally, with Bitcoin confirming its wave-4 low and institutional flows climbing.

Equities

Equities remain supported by liquidity and seasonality, but leverage and sentiment are overheated. The base case remains a shallow 5–7% correction before new highs into year-end.

“Don’t want to be Cassandra — but beware of the risks anyway.

Still in uptrend, still risk-on. Just smaller stakes both ways.”

Our Stance

- Equities: Stay long but trim leverage; buy pullbacks.

- Gold & Silver: Momentum strong but extended — partial profit-taking prudent.

- Crypto: Remains constructive; momentum can run further.

- Macro Focus: Fed data blackout impact and OPEC volume strategy.