Fed’s First Cut, China’s Deflation Shock, and Gold at Record Highs

Markets head into one of the heaviest central bank weeks of 2025 with the Fed poised for its first rate cut in nine months, China sliding deeper into deflation, and gold streaking toward new records. Traders are bracing for dot-plot surprises, cross-asset whipsaws, and a liquidity surge that could either extend the rally or trap late buyers.

Market Overview – A Cut is Coming, but at What Cost?

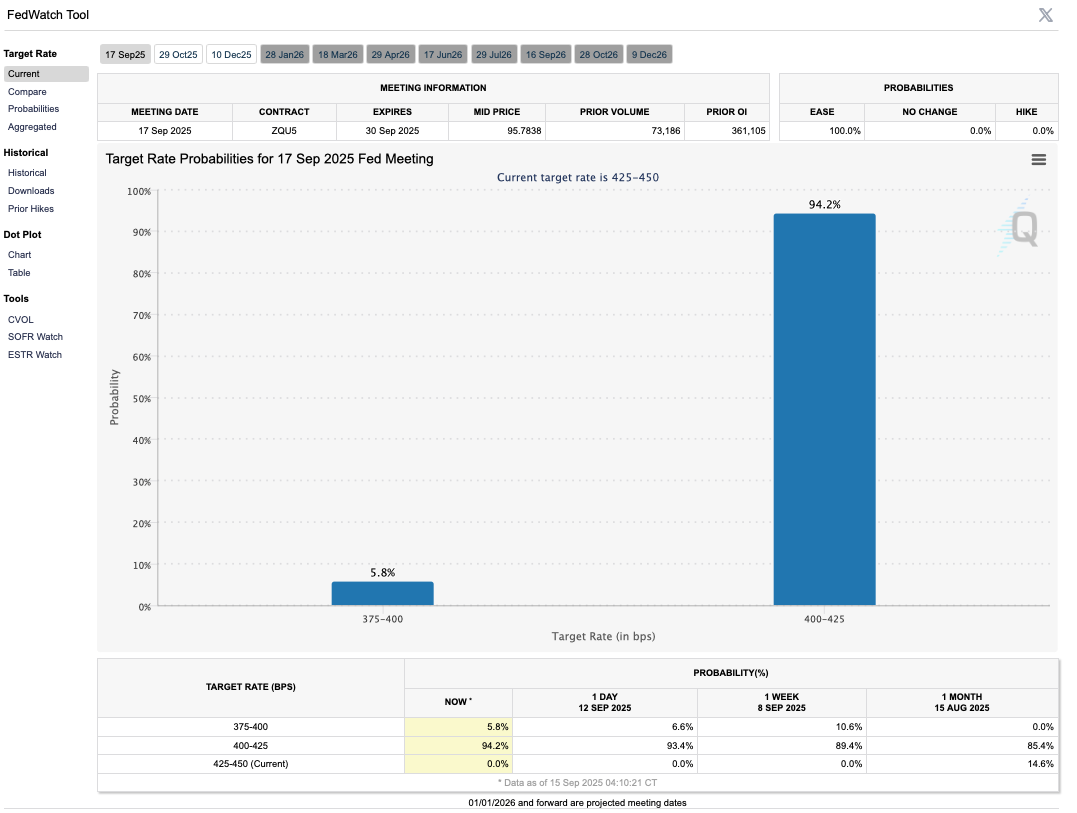

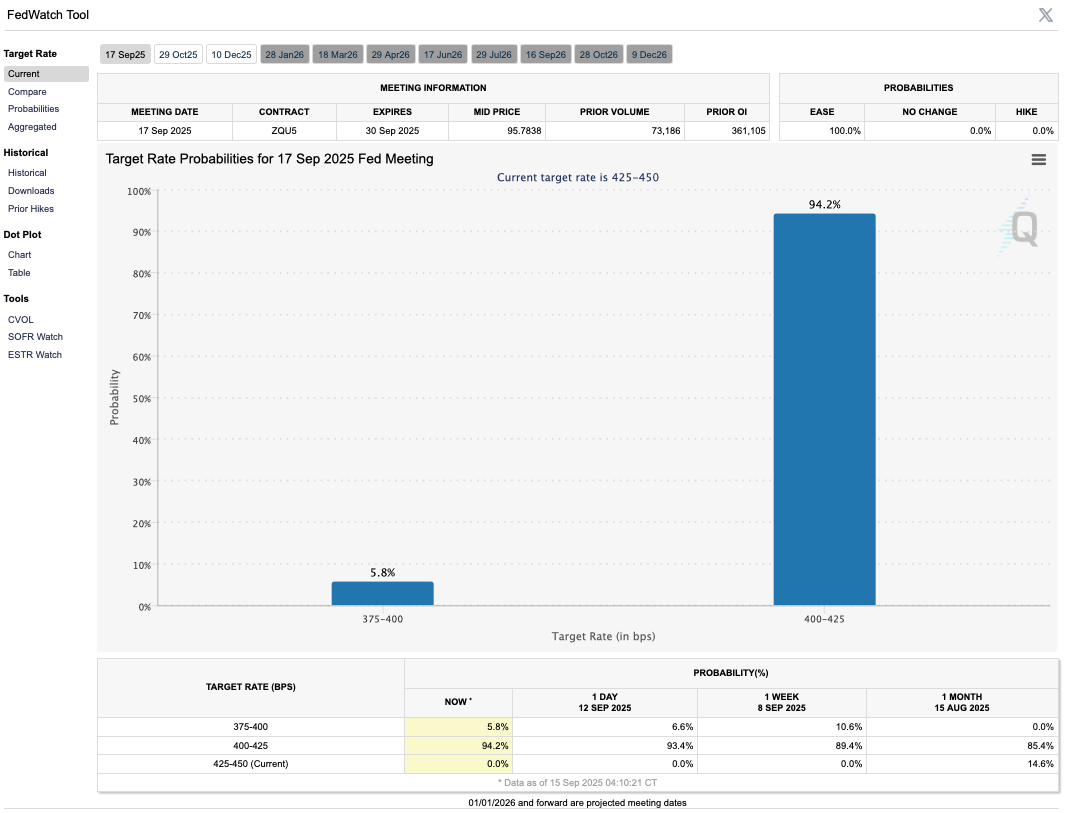

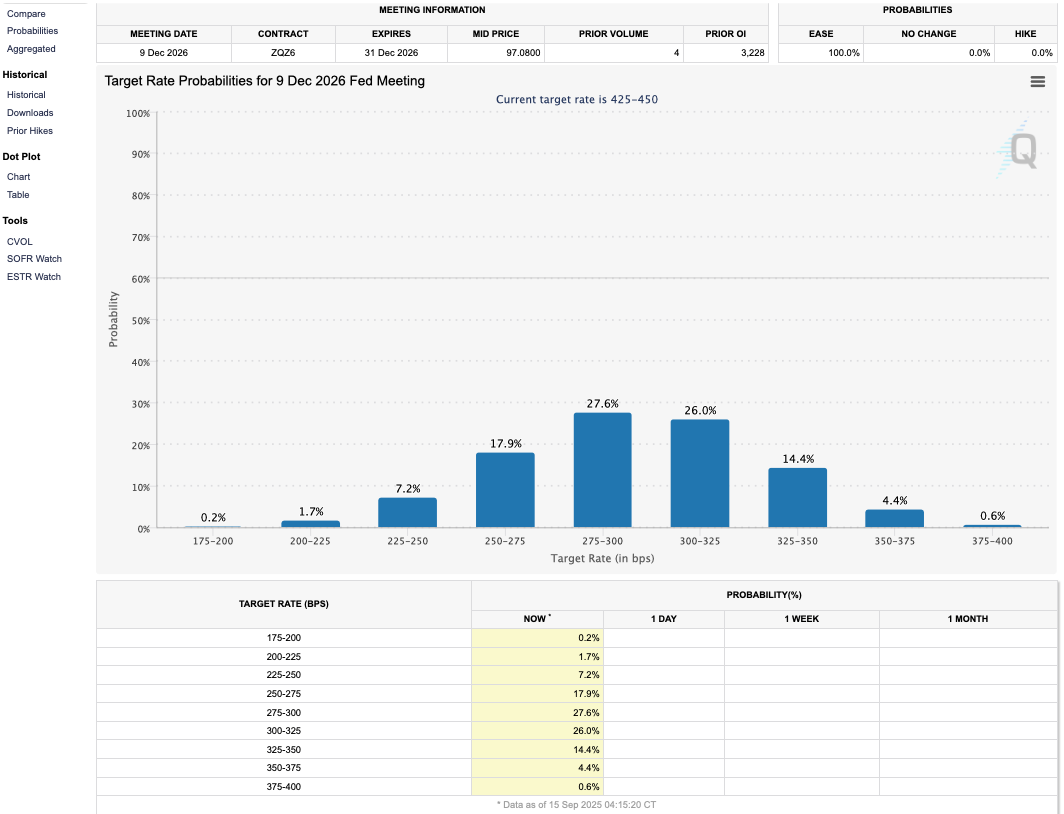

Last week’s softer U.S. labour data and weak PPI opened the door for the Fed to cut rates at Wednesday’s FOMC, taking the target to 4.0–4.25%. Markets are already pricing in 75 bps of cuts by year-end, with a 97% probability according to CME data.

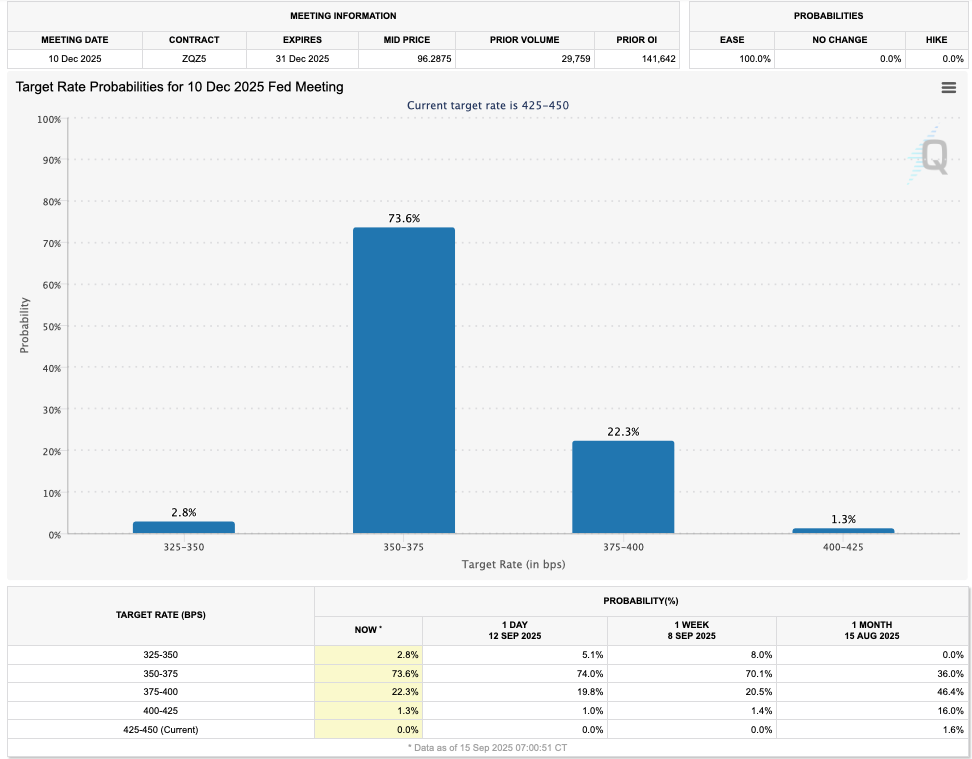

But the bigger question is the path of cuts into 2026. Traders are watching the dot plot to see whether the Fed endorses the market’s -150 bps by 2026 versus the current -100 bps. Meanwhile, the 10-year yield’s “risk-on” line at 4% and “risk-off” line at 4.5% offers a simple roadmap for positioning.

Personnel risk adds drama: Lisa Cook’s legal case and Stephen Miran’s possible dissent (in favour of 50 bp) could inject intraday volatility.

Macro & Policy Watch – Global Easing Blitz Meets China’s Drag

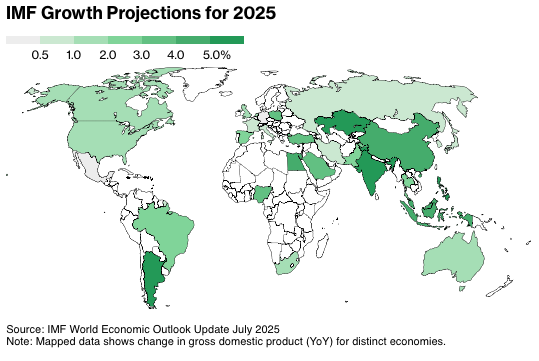

Roughly 40% of the world economy faces rate decisions this week. Canada (-25 bp expected), Norway (-25 bp expected), and BOE (unchanged) join the Fed, while Brazil and the BOJ also take the stage. Easy policy is the week’s central theme, but any outsized Fed cut would roil Treasuries and global risk assets.

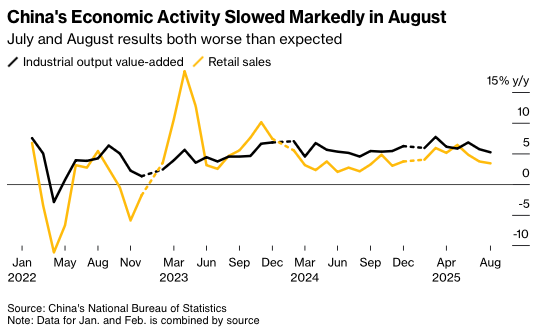

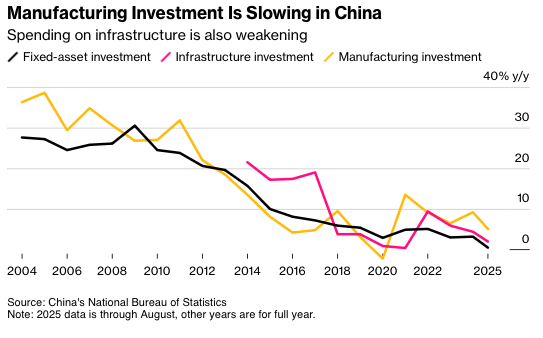

China is the other macro pivot. Retail sales and investment missed forecasts, unemployment ticked higher, and deflation deepened—casting doubt on Q3/Q4 global growth assumptions. Stimulus is still limited, leaving markets to guess when the fiscal hammer drops.

The UK, meanwhile, posted flat GDP with industrial production reversing sharply and manufacturing output sliding. Services and construction managed small gains, but not enough to justify another BOE cut yet.

Technical & Sentiment Breakdown – Gold’s Fib Power and NAS100’s Breakout

Gold – From Textbook Fib to Textbook Breakout

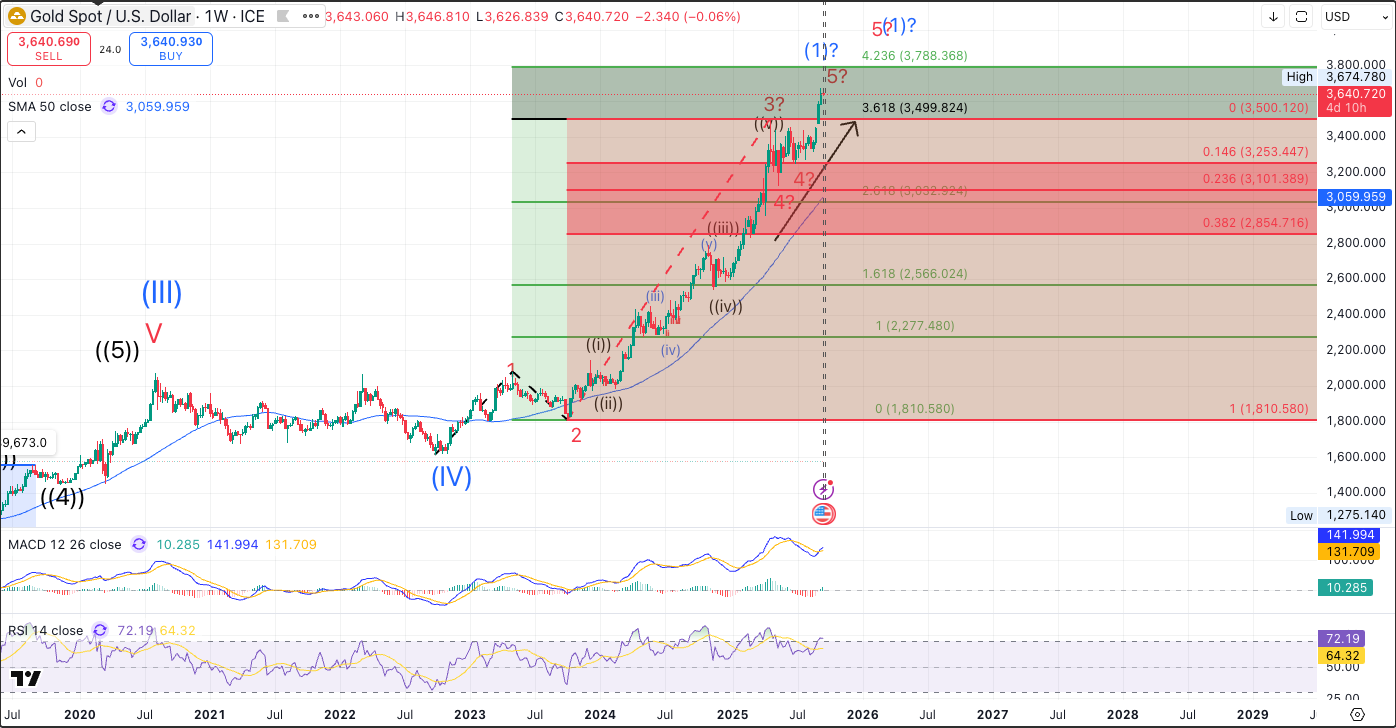

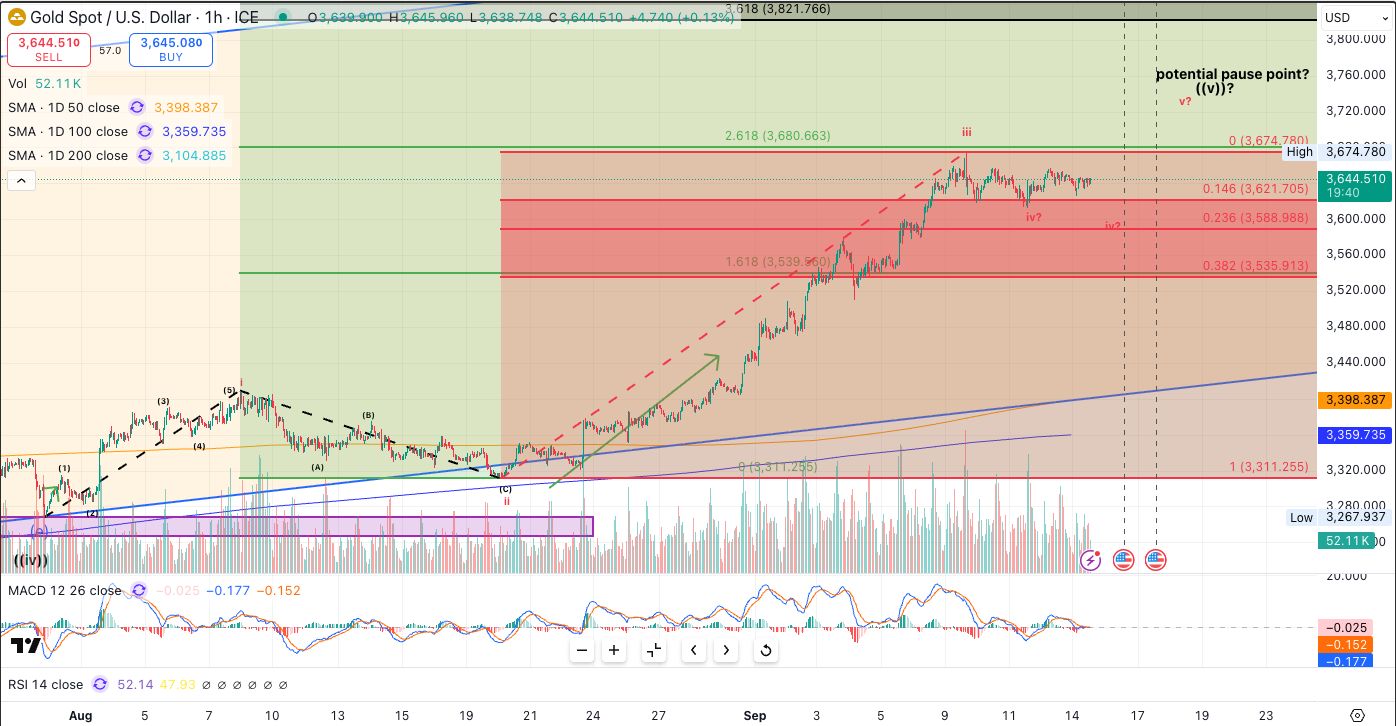

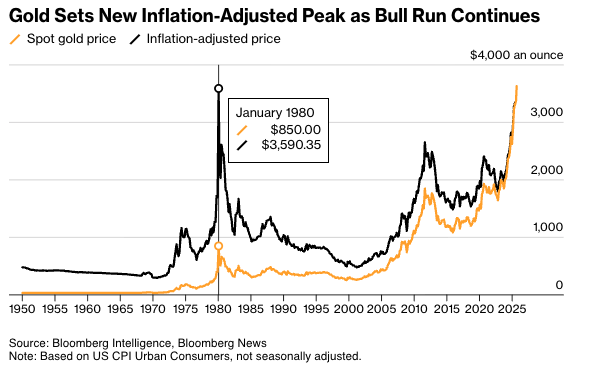

Gold has gained nearly 40% YTD and now trades above $3,600—its strongest week in months and beyond its inflation-adjusted 1980 high. Weakening real yields, dovish monetary policy, and a soft dollar fuel this surge.

Long-term Fibonacci extensions nailed the $3,500 top of wave 3 (3.618 extension). The ABCDE triangle retraced to the 0.146 level at $3,253 before breaking higher. Using i = v projections, a move toward ~$3,720 is in play before the next pause. Short term, expect 3,500–3,650 consolidation before a new ATH above 3,700.

Equities – Breakout or Fakeout?

Dow, NAS100, and SPX all hit new highs. Tesla surged 12.85% on the week while semiconductors reached record peaks. Yet, with FOMC week and heavy expiries ahead, NAS100 could be staging an “expanding flat” fakeout before resuming higher.

In the UK, FTSE miners Rio Tinto, Glencore, and Anglo American drive index strength as M&A speculation heats up, while gold miners like Hochschild and Fresnillo extend the sector’s standout YTD performance.

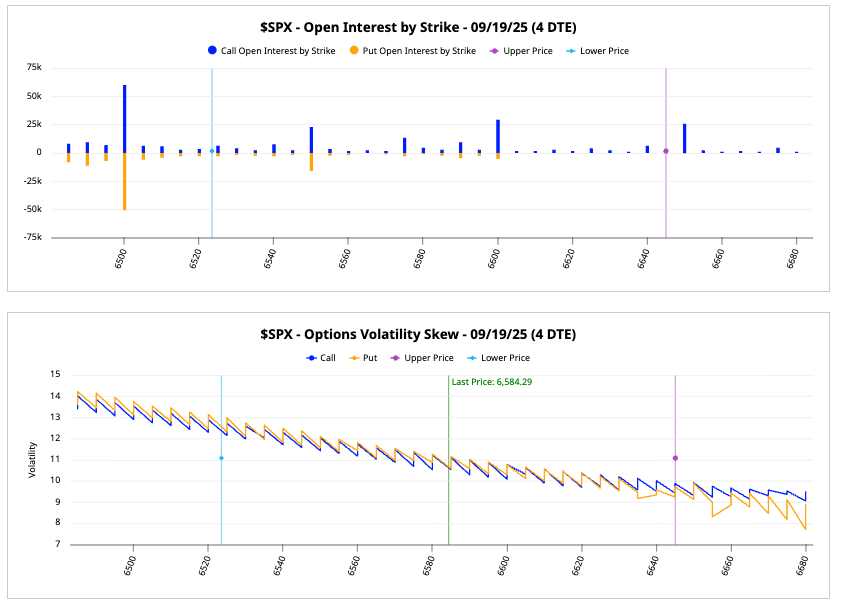

Positioning – Skew Shifts into Fed

Call skew shows upside appetite into the Fed, but Friday expiries revealed downside skew—signalling hedges that could unwind or neutralise post-FOMC.

Last Week’s Recap – Soft Labour, Strong Gold, Fragile China

US CPI : 2.9% YoY in August, up from 2.7%, but still supportive of cuts.

Jobless Claims : Jumped to 263k, the highest since 2023, reinforcing the Fed’s dovish lean.

China : Retail sales and fixed-asset investment were weaker than expected.

Commodities : Silver up, gold at highs above $3,600, dollar eased.

Equities : Tesla and Micron led gains; Oracle slipped after a sharp rally.

Markets now await Powell’s SEP remarks at 19:00 UK on Wednesday. The median dot is expected to still show two cuts this year, with more cuts in 2026 than previously projected.

The Week Ahead – Central Bank Cluster and Retail Sales Tes

Monday 15th Sep 2025

- CNY data: Retail Sales, Fixed Asset Investment, Unemployment Rate

- NY Empire Manufacturing Index

- Rightmove HPI UK

Tuesday 16th Sep 2025

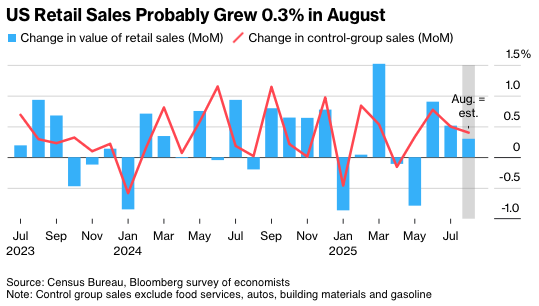

US Retail Sales (+0.3% forecast) and Control Group

CAD CPI

German ZEW & EZ Labour Costs

UK Wages & Employment

US Industrial Production, Import/Export Prices

Wednesday 17th Sep 2025

JPY Trade Balance

GBP CPI

CAD BOC Rate Decision (-25 bp expected)

FOMC Rate Decision 19:00 UK + SEP/Dot Plot

Brazil Rate Decision

Mortgage & Housing Starts US

Thursday 18th Sep 2025

NZD GDP

AUD Employment

Norway Rate Decision (-25 bp expected)

BOE Rate Cut Decision

US Claims, Philly Fed, Leading Index

FedEx Earnings

Friday 19th Sep 2025

BOJ Rate Decision (unchanged expected)

UK Retail Sales

CAD Retail Sales

GER PPI

VIX/Index Expiries

Big picture: as long as growth holds up, policy is easing, and liquidity is ample, dips are likely to be bought. But the cluster of data plus expiries creates headline risk and intraday swings—tight stops and level discipline recommended.

Alpha Takeaway: Play the Levels, Not the Hype

Rate cuts are now at the centre of the market’s crosshairs. With multiple central banks moving this week, liquidity is abundant, but direction isn’t guaranteed. The setup favours tactical trades over sweeping bets.

Our stance:

Equities: Major indices hit fresh highs, but the NAS100’s breakout could still be an “expanding flat” before true higher highs. Semiconductors lead, but watch for consolidation around expiries.

Gold: The metal’s nearly 40% YTD gain puts it at extended levels. Fib targets point to ~$3,720, but the 3,500–3,650 zone may act as a near-term range best to manage entries and avoid chasing.

China & Global Macro: China’s deflation and slowing investment raise red flags for Q3/Q4 global growth. Stimulus remains the wildcard, but global easing still underpins risk sentiment.

Volatility & Positioning: Expiries and central bank decisions dominate this week’s flows. Skew shows hedges leaning downside into FOMC look to fade extremes as positioning resets post-announcements.

This week rewards nimble execution, disciplined levels, and a willingness to pivot fast rather than anchoring to one outcome.